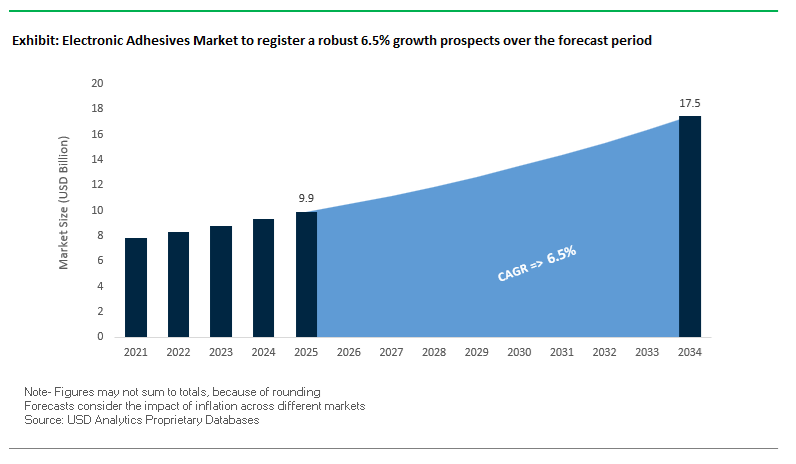

The Global Electronic Adhesives Market is poised for robust growth, projected to expand from approximately USD 9.9 billion in 2025 to USD 17.4 billion by 2034, reflecting a strong CAGR of around 6.5% as advanced electronics continue to evolve. This growth is underpinned by ongoing innovation in semiconductor packaging, EV power electronics, high-performance computing (HPC) platforms, and highly compact consumer devices, driving demand for adhesives that deliver not only reliable bonding but also essential functional properties such as thermal management, electrical insulation, stress mitigation, and environmental robustness. As demand for heterogeneous integration, including 2.5D and 3D packaging — escalates, manufacturers are calling for adhesive solutions that meet higher performance thresholds for conductivity, dielectric control, and mechanical integrity in ever-smaller form factors.

Leading chemical and materials giants including Henkel AG & Co. KGaA, 3M Company, Dow Inc., H.B. Fuller Company, and Sika AG maintain significant market influence with broad portfolios of epoxy, silicone, acrylic, and specialty adhesive systems tailored for electronics assembly and encapsulation applications. These firms leverage deep technical capabilities to co-develop bespoke solutions with OEMs across automotive, consumer electronics, and industrial segments, frequently reinvesting in R&D to stay ahead of material performance demands. Other prominent suppliers in the space include Arkema S.A., BASF SE, Evonik Industries AG, Dymax Corporation, and Avery Dennison, each contributing differentiated chemistries such as UV-curable systems, thermally conductive gels, and low-dielectric materials that respond to evolving industry requirements. Beyond the global tier, regional and niche specialists like Panacol-Elosol, Master Bond Inc., and Permabond LLC further diversify the competitive landscape with customized adhesives for specific electronic and industrial applications.

Further, next-generation die-attach adhesives demonstrate enhanced adhesion strength and thermal robustness at lower processing temperatures, addressing reliability challenges in high-stress semiconductor and power modules. Thermal interface materials (TIMs) and thermally conductive silicones are engineered to withstand elevated junction temperatures typical of 800 V EV systems and Generation 7 IGBTs, critical for automotive and industrial electrification platforms. Low dielectric constant (Dk) adhesives are prioritized in HPC and high-speed communications to preserve signal integrity and minimize energy loss, while room-temperature-cure RTV silicones optimize throughput in high-volume surface-mount technology (SMT) assembly environments.

In September 2025, 3M joined the JOINT3 consortium, a pivotal collaboration aimed at developing manufacturing tools optimized for 515 x 510 mm panel-level organic interposers. This initiative underscores the ongoing industrial pivot toward large-panel advanced packaging for AI and high-performance computing (HPC) chips, significantly driving demand for high-reliability bonding materials and thermal management adhesives in semiconductor production lines.

During the same month (September 2025), Dow introduced DOWSIL™ EG-4175 Silicone Gel, a specialized encapsulant for EV and renewable power systems capable of resisting 180°C junction temperatures while offering self-healing characteristics. This breakthrough enhances long-term protection and thermal endurance in Insulated Gate Bipolar Transistor (IGBT) modules, positioning Dow at the forefront of automotive-grade silicone innovation.

In May 2025, Henkel (Loctite) completed a major R&D and application center expansion in Shanghai, strengthening its leadership in flexible electronics, 5G device assembly, and foldable display adhesives. This move reflects the growing Asia-Pacific innovation hub status, especially as regional OEMs invest heavily in next-generation consumer electronics. Earlier in April 2025, H.B. Fuller achieved qualification from a major automotive OEM for its high-modulus polyurethane adhesive, designed for battery-to-chassis bonding—a critical step toward enhanced EV battery structural integrity and thermal safety compliance.

The February 2025 acquisition by a leading global chemical company of a U.S.-based manufacturer of silver-filled electrically conductive adhesives (ECAs) further strengthened the market’s high-frequency material portfolio, especially in RFID and IoT sensor integration. Similarly, 3M’s December 2024 launch of a skin-friendly medical adhesive capable of maintaining adhesion for 28 days marked a significant milestone in wearable medical device adhesives, opening long-term opportunities in biosensor technology and digital healthcare.

Meanwhile, in November 2024, the U.S. Department of Commerce introduced new domestic sourcing incentives for specialty precursors used in advanced electronic adhesives, aligning with national supply chain security goals. The October 2024 commissioning of a new adhesive manufacturing facility in Southeast Asia by a global industry leader further highlighted the regional expansion trend, particularly for thermally conductive gap fillers and potting materials serving EV and high-performance electronics markets.

The rapid adoption of wide-bandgap (WBG) semiconductors, such as Silicon Carbide (SiC) and Gallium Nitride (GaN), in automotive, aerospace, and telecommunication systems has created unprecedented thermal and mechanical demands. The is accelerating the shift toward high-thermal-conductivity, low-stress die-attach adhesives that can manage extreme junction temperatures without compromising reliability.

Traditional conductive adhesives with a thermal conductivity of around 1.5 W/(m·K) are no longer adequate for today’s high-power applications. In response, cutting-edge die-attach formulations are achieving thermal conductivities exceeding 90 W/(m·K) using silver and copper nanofiller systems, offering exceptional heat dissipation for EV inverters, SiC MOSFETs, and 5G RF amplifiers.

Simultaneously, minimizing mechanical stress on dissimilar materials (e.g., Si die on Cu substrates) has become a design priority. State-of-the-art low-stress die-attach pastes can achieve curvature radii of up to 100,000 mm, a hundredfold improvement over conventional materials, reducing warpage and mechanical strain in automotive-grade and military power modules.

In addition, snap-cure, one-component adhesives are enabling high-volume automated manufacturing. Modified cyanate ester-based formulations that fully cure in under 2 minutes at 200°C are increasingly being integrated into EV power module and 5G base station assembly lines, balancing throughput, adhesion strength, and thermal efficiency for next-generation production demands.

The miniaturization of components in flexible electronics, MEMS, and advanced packaging has triggered an industry-wide shift toward low-temperature and rapid-curing adhesives that protect heat-sensitive materials while maximizing production efficiency.

UV-LED-curable adhesives have become the standard in consumer and automotive electronics, offering instant polymerization within seconds under narrow-band UV light (365–395 nm). These formulations use next-generation photoinitiator systems that achieve precise depth curing, preventing thermal distortion and surface warping in delicate optical and sensor components.

Parallel advancements in low-temperature curing epoxies and silicones—with full cure achievable between 80°C and 120°C—are critical for assembly of MEMS sensors, camera modules, and organic flexible substrates. These adhesives provide robust adhesion while significantly reducing CTE-induced stress, ensuring long-term performance stability for high-reliability devices.

In high-speed manufacturing environments, dual-cure systems combining UV and thermal activation are becoming the go-to solution. They ensure comprehensive polymerization even in shadowed or recessed areas, guaranteeing consistent adhesion in multi-layer circuit assemblies and LED modules.

The semiconductor industry’s transition from monolithic designs to Heterogeneous Integration (HI) and chiplet-based architectures has created a transformative demand for precision-engineered adhesives that enable dense 3D packaging and ultra-fine interconnects.

Modern System-in-Package (SiP) configurations require ultra-thin, uniform bonding interfaces. Manufacturers are developing Die-Attach Films (DAF) with controlled thicknesses between 8 and 10 microns, offering exceptional planarity and stress control for multi-die stacking. These films are critical for memory stacking, logic-interposer bonding, and System-on-Chip (SoC) module fabrication.

Further, one-component epoxy film adhesives featuring low ionic impurities and high mechanical strength are becoming integral to multi-chip module (MCM) applications. Tests demonstrate die shear strength exceeding 40 kgf for 2 mm × 2 mm dies, even after extensive humidity and temperature cycling—an essential metric for high-I/O-density chiplet systems used in AI processors, 5G chips, and automotive ECUs.

As the global battery industry accelerates toward Solid-State Battery (SSB) commercialization, the demand for advanced adhesives and sealants engineered for solid electrolytes and rigid ceramic interfaces is expanding rapidly. These materials must withstand high mechanical stresses, provide perfect hermetic sealing, and deliver strong dielectric properties across wide temperature ranges.

Major automakers and battery developers are aggressively investing in SSB development. For instance, Toyota’s announced SSB launch by 2027–2028—promising a 10-minute charge time and 50% higher energy density—is setting a benchmark for the industry. The scale-up of such initiatives requires a steady supply of electrically insulating, thermally stable adhesives suitable for module bonding, electrolyte encapsulation, and pack sealing.

Silyl-modified polymers (SMPs) and methyl methacrylate (MMA)-based structural adhesives are emerging as key candidates for SSB production. Their ability to deliver high breakdown strength (>15 kV/mm) and volume resistivity (>10¹⁴ Ω·cm) ensures superior insulation and safety within high-voltage environments. Additionally, their flexibility mitigates the thermal cycling stress between dissimilar interfaces, enhancing battery module longevity.

Electronic Adhesives Market Share Insights, 2025-2034

Paste adhesives dominate the global electronic adhesives market, accounting for the largest share thanks to their unmatched versatility and compatibility with a wide range of semiconductor and PCB assembly processes. Their paste-like consistency allows for precise dispensing, stencil printing, or screen application, which is crucial in surface-mount technology (SMT), die attach bonding, and chip packaging. These adhesives provide excellent thixotropy and viscosity control, ensuring consistent deposit shape, minimal voiding, and high placement accuracy—key parameters for high-reliability microelectronic assemblies. The strong adoption of paste formulations in semiconductor back-end manufacturing reflects their ability to deliver thermal conductivity, electrical insulation, and mechanical stability under harsh operational conditions. Additionally, with the increasing miniaturization of electronic components and the rise of 3D IC packaging, pastes optimized for low-temperature curing and fine-pitch dispensing are becoming integral to high-performance device production. Their proven process reliability, broad substrate compatibility, and adaptability across consumer electronics, automotive, and telecommunications electronics ensure paste adhesives remain the cornerstone of the global electronic bonding landscape.

Film Adhesives Secure 27.4% Market Share, Driven by Precision in Semiconductor and Display Assembly

Film adhesives represent a rapidly expanding, high-value segment in the electronic adhesives market, holding a significant share due to their precision, cleanliness, and suitability for automated manufacturing. Used extensively in semiconductor packaging and display bonding, these pre-formed adhesives—such as Die Attach Film (DAF) and Anisotropic Conductive Film (ACF)—enable accurate, repeatable bonding without excess material or contamination. DAF technology supports the thinning and stacking of dies for 3D IC packaging, facilitating higher integration density and improved thermal management in smartphones, memory devices, and processors. Similarly, ACFs are indispensable for fine-pitch interconnections in LCD, OLED, and flexible displays, offering both electrical conductivity and mechanical adhesion in one step. The demand for cleanroom-compatible, low-outgassing, and heat-resistant films is surging as the industry shifts toward miniaturized, high-density electronics.

Liquid and tape adhesives, while smaller in market share, play indispensable roles across a range of niche and protective electronic applications. Liquid adhesives are widely used for potting, encapsulation, and conformal coating, forming protective barriers against moisture, chemicals, and vibration—especially critical for automotive, industrial, and aerospace electronics. Their ability to flow into small voids and coat complex geometries ensures robust protection for sensitive components like sensors, microcontrollers, and power modules. Meanwhile, adhesive tapes—including thermal interface tapes, double-coated tapes, and EMI-shielding tapes—provide rapid, clean, and precise bonding solutions for electronic assembly lines. They are ideal for bonding heat sinks, attaching shielding cans, and mounting displays or sensors, significantly reducing curing time and enabling automation-friendly workflows. These materials also cater to the demand for reworkability, low-VOC formulations, and cleanroom compatibility in high-value production environments.

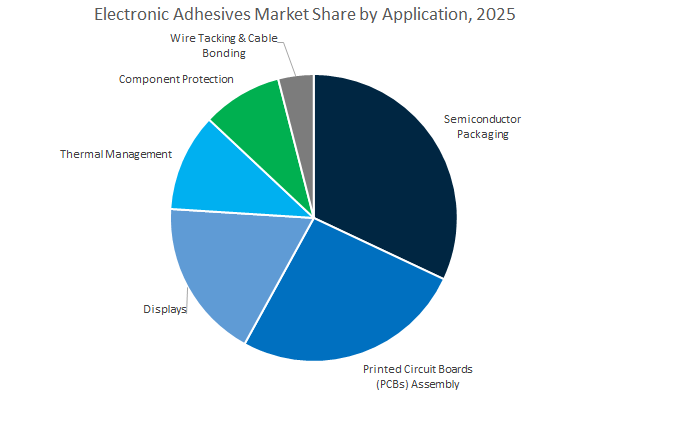

Semiconductor packaging dominates the global electronic adhesives industry, representing the most critical and technologically advanced application segment. Adhesives in this field perform multiple essential functions—die attach, underfill, encapsulation, and lid sealing—to protect fragile silicon dies and maintain device performance under thermal and mechanical stress. The continuous scaling of semiconductor nodes and the adoption of 3D integration, fan-out wafer-level packaging (FOWLP), and system-in-package (SiP) designs have elevated the performance demands placed on adhesives. They must offer high thermal conductivity, electrical insulation, and low ionic contamination while withstanding high processing temperatures. In advanced semiconductor packaging, the trend toward lead-free and low-temperature curing materials is accelerating due to environmental compliance and energy efficiency goals. The growing production of AI processors, EV chips, and 5G baseband semiconductors further amplifies the need for adhesives that ensure thermal stability and reliability.

PCB assembly represents the foundation of global electronic adhesive consumption, encompassing applications such as SMT component bonding, conformal coating, and solder mask reinforcement. The sector’s large-scale, repetitive production of consumer electronics, computing devices, and industrial controllers drives continuous demand for adhesives that combine fast processing, thermal stability, and excellent substrate adhesion. Adhesives in PCB assembly must survive reflow soldering cycles, provide mechanical reinforcement to prevent solder joint cracking, and enhance overall board rigidity. As PCBs become increasingly complex—with multilayer, high-density interconnect (HDI), and flexible circuits—the role of adhesives in ensuring mechanical integrity and electrical reliability is expanding. Additionally, automated dispensing and screen-print-compatible materials are gaining traction as manufacturers aim to optimize production efficiency.

The displays and thermal management segments are emerging as two of the fastest-growing areas in the global electronic adhesives market. In the displays segment, optically clear adhesives (OCAs) are critical for laminating touch panels, smartphone screens, and automotive displays, providing high transparency, UV stability, and bubble-free adhesion. The growing popularity of flexible OLED and microLED displays has further increased demand for flexible, reworkable, and low-outgassing adhesive systems. In thermal management, adhesives are pivotal for bonding heat sinks, thermal interface materials (TIMs), and power modules, particularly in EVs, data centers, and consumer electronics. The surge in high-wattage components and miniaturized designs has made thermal adhesives central to preventing overheating and ensuring device longevity. Manufacturers are also developing silicone- and epoxy-based thermally conductive materials with enhanced dielectric strength and environmental safety.

The competitive landscape of the global electronic adhesives market is defined by technological leadership, sustainability-driven R&D, and end-use diversification across key players. Major manufacturers—Henkel, Dow, 3M, H.B. Fuller, and Shin-Etsu Chemical—are actively developing tailored adhesive solutions for semiconductor packaging, automotive electronics, flexible circuits, and medical wearables. These companies are strategically investing in next-generation materials emphasizing thermal stability, low VOC content, and integration with automated assembly systems to enhance production efficiency and reliability.

Henkel continues to drive innovation through its Mobility and Electronics business segment, addressing global megatrends such as electrification, connectivity, and autonomous driving. Under its Loctite brand, the company provides a wide range of structural adhesives, thermal interface materials, and gap fillers for EV and consumer electronics applications. Henkel’s engineering support services—including prototyping and design validation—enable seamless integration within automated assembly lines. Its November 2023 launch of IBOA-free light-cure medical adhesives showcases Henkel’s proactive commitment to safety and biocompatibility in healthcare applications.

Dow Inc. maintains global leadership in silicone and polyurethane adhesive chemistry, providing critical materials under its DOWSIL™ portfolio. The company’s innovations—such as DOWSIL™ TC-2035 CV Adhesive and TC-4551 CV Gap Filler—offer controlled volatility and superior reliability near sensitive electronic circuits, making them ideal for ADAS, LiDAR, and battery management systems. Dow’s focus on automotive electronics and e-mobility solutions underscores its dedication to delivering high-performance, thermally stable silicone systems that enable safer and more efficient electronic designs.

3M leverages over 50 technology platforms to advance microelectronics manufacturing, with expertise in semiconductor packaging adhesives, Optically Clear Adhesives (OCAs), and Boron Nitride Cooling Fillers. Its September 2025 participation in the JOINT3 consortium positions the company as a key collaborator in developing panel-level organic interposers for HPC and AI chips. With a strong foothold in high-purity materials and film solutions, 3M continues to improve yield, reliability, and signal transfer efficiency across semiconductor and display manufacturing lines.

H.B. Fuller has carved a distinct niche with its Smart Vehicle (SV) product line—covering Bond, Protect, Seal, and Therm series—designed for thermal management and structural reinforcement in EV electronics. The company’s EV Protect™ family integrates flame-retardant foams and lightweight adhesives for thermal runaway prevention and NVH reduction in battery modules. By targeting Cell-to-Carrier bonding and mica shield integration, H.B. Fuller reinforces its leadership in EV battery safety and high-voltage component durability.

Shin-Etsu Chemical stands out as a leading supplier of silicone-based electronic materials in the Asia-Pacific region. Its portfolio spans molding compounds, liquid encapsulants, and thermally conductive compounds tailored for LED lighting and power device modules. The company’s latest capacity expansion in its silicone division aims to meet surging demand from 5G and EV markets, reinforcing its long-term commitment to advanced encapsulation and moisture-resistant adhesives for military-grade and aerospace electronics.

The U.S. electronic adhesives market is surging on the back of the CHIPS and Science Act, with $450+ billion in announced fab, packaging, and materials investments (as of Aug-2024) and a projected tripling of U.S. wafer capacity by 2032. The capital wave is translating directly into multi-year orders for die-attach adhesives, capillary underfill, non-conductive pastes, and thermally conductive encapsulants designed for heterogeneous integration and advanced packaging lines. Parallel DoD supply-chain security programs are steering R&D toward domestically sourced, high-reliability bonding chemistries for aerospace/defense electronics, with rigorous thermal shock, vibration, and outgassing requirements.

On the demand side, accelerating EV and ADAS penetration is expanding specifications for thermally stable, low-modulus TIM adhesives in BMS, inverters, and sensor control units. Leading U.S. materials suppliers are entering co-development partnerships (Apr-2024) with OEMs/OSATs to tailor rheology, cure kinetics, and filler morphology for next-gen fan-out/WLP—while a policy and customer push toward low-VOC, eco-friendly formulations is speeding adoption of water-borne and solvent-reduced systems in cleanroom-adjacent assembly.

China remains a volume anchor for electronic bonding solutions as policymakers target ~7% CAGR for large-scale electronic information manufacturers (late-2025 action plan). IC exports rose 11.6% in 2024, reinforcing upstream demand for ECAs, ACFs, underfills, and TIM adhesives across smartphones, servers, and power electronics. Domestic roadmaps (e.g., Made in China 2025) prioritize localization of high-performance electronic adhesives to reduce import reliance, while new procurement preferences for “Made in China” components reshape competitive dynamics for foreign brands.

End-markets are broadening: large-screen TVs ≥75" (targeting >40% penetration) and the fast-growing server industry (>¥400B output) are catalyzing upgrades to optically clear adhesives, perimeter sealants, and high-conductivity TIMs for thermal management in data centers. Concurrently, flexible electronics and advanced displays are accelerating investment in ACF/ECAs with finer particle distribution, lower ionic contamination, and controlled modulus for bend/fold use-cases.

South Korea’s leadership in memory, logic, and displays sustains premium demand for electrically and thermally conductive adhesives tailored to high-density chip packaging. Display majors are scaling UV-cured, rapid-tack adhesives for flexible OLED and MicroLED—prioritizing ultra-clean cure, low haze, and high adhesion after thermal cycling. Semiconductor champions are qualifying ultra-low-viscosity underfills for flip-chip and WLP, optimizing capillary flow, fillet control, and warpage reduction at ever-tighter pitches.

In e-mobility, Korea’s giga-scale battery programs are standardizing encapsulants and potting compounds with enhanced thermal stability, flame retardancy, and shock resistance for modules/packs. Telco and consumer-device ecosystems are adopting reactive adhesives that meet 5G reliability standards, while chemical producers expand silicone adhesive capacity to serve image sensors and memory markets that require superior moisture barrier and dielectric properties.

Germany’s precision manufacturing base—spanning premium automotive, industrial controls, and power electronics—is a core consumer of high-temperature epoxy, UV/light-cure, and thermally conductive adhesives. EU environmental policy is accelerating the shift to water-borne and solvent-free electronic adhesives, rewarding suppliers with demonstrably lower VOC and life-cycle impacts. Automakers’ ADAS/ECU platforms are specifying robust die-attach and structural bonding that survive rapid thermal transients and harsh NVH profiles, while machine builders adopt high-reliability epoxies for sensors and actuators in Industry 4.0 cells.

Innovation momentum remains strong: a leading German chemical producer launched bio-based electronic adhesives (Mar-2024), widening sustainable options for assembly lines. Meanwhile, thermally conductive systems (ceramic-filled silicones/epoxies) are scaling with the miniaturization of industrial motor drives and EV power modules. Capacity additions for UV/light-cure materials in Europe target faster cycle times, in-line inspection readiness, and lower energy footprints on automated lines.

Japan continues to set global benchmarks in die-attach film (DAF), non-conductive paste (NCP), and optical encapsulation for advanced memory and logic. Capacity expansions (Jul-2024) are aligned to semiconductor and display growth, while telecom OEMs ramp encapsulation adhesives for optical transceivers in 5G/Fiber networks to ensure low insertion loss and long-term hermeticity. R&D is deepening in polyimide/silicone adhesives with high glass-transition temperatures and low modulus for MEMS and sensors, balancing stress relief with package integrity.

Japan’s medical device segment elevates demand for ultra-pure, biocompatible bonding systems for wearables and surgical electronics. In printed and flexible electronics, Japanese firms lead with functional conductive inks and ECAs optimized for stretchability, bend radius endurance, and stable conductivity—critical in flex PCBs, HMIs, and smart surfaces.

As the world’s core advanced foundry and OSAT hub, Taiwan is the largest aggregate consumer of underfills, die-attach materials, NCP/NCF, and reworkable epoxies for sub-5nm logic and chiplet/SiP architectures. The ongoing expansion of CoW, 3D stacking, and SiP is increasing demand for low-stress, high-Tg bonding with fine fillet control and minimal warpage. Industry and government are reinforcing local supply chains for semiconductor-grade epoxies and silicones, reducing exposure to global shocks.

R&D and capex are flowing into temporary bonding/debonding adhesives (TBA) for ultra-thin wafer handling and 3D integration, as well as reworkable systems that enable yield rescue in high-value assemblies. Taiwan’s display makers simultaneously lift consumption of optically clear adhesives (OCA) and edge sealants that deliver bubble-free lamination, optical clarity, and UV/thermal stability for monitors and mobile screens.

Electronic Adhesives Market Report Scope

Electronic Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9.9 Billion

|

|

Market Size (2034)

|

$17.4 Billion

|

|

Market Growth Rate

|

6.5%

|

|

Segments

|

By Resin Type (Epoxy, Silicone, Acrylic, Polyurethane, Cyanoacrylate, Polyimide, Other), By Product Type (Electrically Conductive Adhesives, Thermally Conductive Adhesives, UV/Light-Cure Adhesives, Structural Electronic Adhesives, Die Attach Adhesives, Underfill Adhesives, Encapsulants & Potting Compounds, Conformal Coatings, Solder Alternatives), By Form (Paste, Liquid, Film, Tape), By Application (Printed Circuit Boards Assembly, Semiconductor Packaging, Displays, Thermal Management, Component Protection, Wire Tacking & Cable Bonding), By End-Use Industry (Consumer Electronics, Automotive Electronics, Communications, Industrial Electronics, Medical Devices, Commercial Aviation & Defense), By Curing Mechanism (Thermal Cure, UV/Visible Light Cure, Room Temperature Cure, Dual Cure

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, The 3M Company, H.B. Fuller Company, Arkema SA, Dow Inc., Sika AG, Dymax Corporation, Lord Corporation, Indium Corporation, Evonik Industries AG, Wacker Chemie AG, Master Bond Inc., DELO Industrial Adhesives, Hitachi Chemical, Shin-Etsu Chemical Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type

- Epoxy

- Silicone

- Acrylic

- Polyurethane

- Cyanoacrylate

- Polyimide

- Other

By Product Type

- Electrically Conductive Adhesives

- Thermally Conductive Adhesives

- UV/Light-Cure Adhesives

- Structural Electronic Adhesives

- Die Attach Adhesives

- Underfill Adhesives

- Encapsulants & Potting Compounds

- Conformal Coatings

- Solder Alternatives

By Form

By Application

- Printed Circuit Boards Assembly

- Semiconductor Packaging

- Displays

- Thermal Management

- Component Protection

- Wire Tacking & Cable Bonding

By End-Use Industry

- Consumer Electronics

- Automotive Electronics

- Communications

- Industrial Electronics

- Medical Devices

- Commercial Aviation & Defense

By Curing Mechanism

- Thermal Cure

- UV/Visible Light Cure

- Room Temperature Cure

- Dual Cure

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- The 3M Company

- H.B. Fuller Company

- Arkema SA

- Dow Inc.

- Sika AG

- Dymax Corporation

- Lord Corporation

- Indium Corporation

- Evonik Industries AG

- Wacker Chemie AG

- Master Bond Inc.

- DELO Industrial Adhesives

- Hitachi Chemical

- Shin-Etsu Chemical Co., Ltd.

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Electronic Adhesives Market with deep-dive analysis reviews of demand drivers across semiconductor packaging, EV power electronics, 5G/edge hardware, advanced displays, and flexible electronics. It highlights materials innovation in thermally conductive yet electrically insulating systems, low-dielectric epoxies for signal integrity, UV/dual-cure platforms for high-throughput lines, and rugged encapsulants for harsh environments. We map value pools to manufacturing realities—rheology windows, cure kinetics, outgassing/ionic purity, and UL/flammability and reliability gates—while profiling capacity shifts, regionalization, and sustainability pivots. Coverage of panel-level packaging, chiplet/SiP interconnects, and EV thermal safety underscores where performance and cost converge. Featuring comparative scorecards, cost-to-serve benchmarks, and adoption roadmaps, this report is an essential resource for materials leaders, process engineers, sourcing and category managers, and strategy teams seeking defensible choices as breakthroughs in advanced packaging and e-mobility re-shape specifications.

Scope Highlights

Segmentation:

- By Resin Type: Epoxy; Silicone; Acrylic; Polyurethane; Cyanoacrylate; Polyimide; Other.

- By Product Type: Electrically Conductive Adhesives; Thermally Conductive Adhesives; UV/Light-Cure Adhesives; Structural Electronic Adhesives; Die-Attach Adhesives; Underfill Adhesives; Encapsulants & Potting Compounds; Conformal Coatings; Solder Alternatives.

- By Form: Paste; Liquid; Film; Tape.

- By Application: Printed Circuit Boards Assembly; Semiconductor Packaging; Displays; Thermal Management; Component Protection; Wire Tacking & Cable Bonding.

- By End-Use Industry: Consumer Electronics; Automotive Electronics; Communications; Industrial Electronics; Medical Devices; Commercial Aviation & Defense.

- By Curing Mechanism: Thermal Cure; UV/Visible Light Cure; Room Temperature Cure; Dual Cure.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Frame: Historic data (2021–2024) and forecast data (2025–2034).

Companies: 15+ company analyses/profiles covering portfolios, capacity moves, partnerships, M&A, and pipeline innovations.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.