Corrugated Bulk Bins Market Overview: Growth Toward $22.3 Billion by 2034

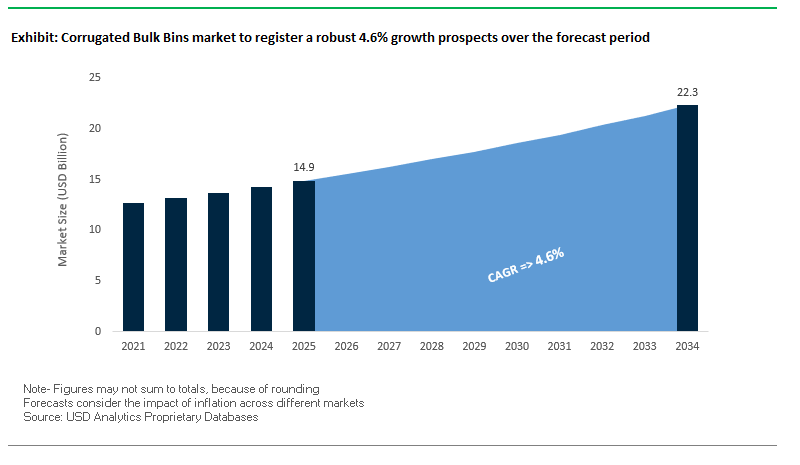

The global corrugated bulk bins market is forecast to expand from $14.9 billion in 2025 to $22.3 billion by 2034, registering a CAGR of 4.6%. Corrugated bulk bins have become an indispensable component of the global packaging industry, serving industries that require durable yet lightweight solutions for storage, transportation, and logistics. They offer the dual advantage of load-bearing strength and sustainability, making them increasingly preferred over wood or steel alternatives. For professionals and buyers, key questions include: How will rising recyclability standards shape future adoption? How will agriculture and perishables continue to drive demand? And what role will AI-driven design and automation play in optimizing corrugated bin performance?

Key Insights include:

- Heavy-Duty Performance: Triple-wall corrugated bulk bins can support loads of over 1,500 kg, making them a cost-effective replacement for wood and steel bins.

- Recycling Infrastructure: North America achieved a 93% recycling rate for old corrugated containers (OCC) in 2022, demonstrating industry leadership in circular economy practices.

- Agricultural Applications: Corrugated bins with wet-strength liners protect fruits, vegetables, and perishables, maintaining freshness and reducing spoilage during global transport.

- Logistics Optimization: Their lightweight design lowers freight costs and fuel consumption, directly benefiting supply chain efficiency while reducing carbon footprints.

The market’s expansion is being powered by sustainability regulations, innovations in automated fit-to-product packaging, and ongoing substitution of plastics and wood, positioning corrugated bulk bins as a critical enabler of circular and cost-efficient logistics.

Market Analysis: AI, Sustainability, and Strategic Expansion Reshaping the Industry

The corrugated bulk bins industry is undergoing significant transformation, characterized by AI-driven design optimization, sustainability commitments, and global consolidation.

In September 2025, industry publications highlighted how AI and predictive analytics are optimizing corrugated bulk bin designs ensuring specific load requirements are met while reducing material usage. This not only improves bin efficiency but also reduces environmental impact. In August 2025, RKW Group partnered with Dow to commercialize recycled-content shrink films, underscoring the broader push to integrate PCR materials across packaging categories, including liners for corrugated bins.

In July 2025, the merger of Smurfit Kappa and WestRock was finalized, creating Smurfit WestRock, a powerhouse expected to reshape competitive dynamics across corrugated packaging globally. Earlier in May 2025, DS Smith launched DryPack in North America, a recyclable corrugated solution designed to replace EPS foam in seafood packaging, setting a benchmark for sustainable food logistics.

Other notable developments include March 2025, when WestRock and Liberty Coca-Cola Beverages installed equipment to replace plastic rings with recyclable paperboard carriers further evidence of the shift away from plastic. In January 2025, Smurfit Kappa invested $5.1 billion in a new corrugated plant in North Africa, strengthening its regional presence. The same month, a report identified the rise of fit-to-product automated packaging as a major trend, extending into bulk bin design to reduce filler materials and improve cost efficiency.

Trends and Opportunities Transforming the Corrugated Bulk Bins Market

Integration of IoT and Digital Tracking Technologies

Corrugated bulk bins are transitioning from traditional passive packaging into smart, data-generating assets that provide real-time visibility across the supply chain. Manufacturers are embedding RFID tags, GPS trackers, and IoT-enabled sensors into corrugated structures to create actionable intelligence for logistics optimization. For instance, RFID integration allows warehouses to automate inventory counts and track shipments from the production floor to distribution centers, significantly reducing reliance on outdated paper-based systems.

Advanced condition-monitoring sensors take this innovation a step further by tracking temperature, humidity, and shock levels. This functionality is particularly important for industries such as pharmaceuticals, food, and chemicals, where exposure to damaging conditions can cause costly product loss. By continuously monitoring environmental factors, companies can validate product integrity and meet strict quality assurance standards. The data collected from IoT-enabled corrugated bulk bins is also being leveraged for predictive analytics. Historical insights help supply chain managers identify risky transit routes, anticipate bottlenecks, and implement proactive measures, making corrugated bins a cornerstone of intelligent logistics networks.

Adoption of High-Performance Coatings for Extreme Conditions

To compete with reusable plastic containers (RPCs) and expand into new industrial use cases, corrugated bulk bin manufacturers are investing in advanced coating technologies. Traditional wax-based coatings, which are difficult to recycle, are being phased out in favor of water-based, repulpable coatings that provide comparable moisture resistance while enabling recyclability. These new coatings address sustainability concerns and allow corrugated bins to re-enter the paper recycling stream, creating both environmental and economic benefits.

Beyond moisture barriers, modern coatings are being engineered for oil resistance, scuff protection, and enhanced stackability, opening opportunities in food, beverages, and chemicals where packaging performance is critical. Some leading manufacturers have also developed coated corrugated bins capable of withstanding multiple supply chain trips, positioning them as a cost-effective alternative to RPCs. This capability addresses end-user demand for durability, recyclability, and lower capital costs, enabling corrugated bulk bins to capture greater market share in industrial sectors traditionally dominated by rigid packaging.

Development of Lightweighting and Structural Optimization Technologies

Lightweighting presents a major opportunity to reduce costs, improve logistics efficiency, and align with corporate sustainability commitments. Academic and industry research is increasingly focused on optimizing flute and liner combinations in corrugated boards, using advanced modeling and simulation tools to achieve required stacking strength while minimizing material usage. This not only reduces raw material costs but also decreases shipping weight, which translates into significant fuel savings and lower Scope 3 emissions for brands.

Lightweight corrugated bulk bins provide a compelling eco-friendly solution for manufacturers under pressure to reduce their carbon footprint and report measurable sustainability progress. By demonstrating reduced emissions and packaging efficiency improvements, brands can strengthen their ESG performance and gain a competitive edge in markets where sustainability credentials are now a critical purchasing factor.

Expansion into Closed-Loop, Reusable Systems with Take-Back Programs

The transition from single-use corrugated bins to closed-loop, reusable ecosystems is emerging as a high-growth opportunity. Packaging suppliers are developing business models around reverse logistics, asset pooling, and service-based solutions, enabling customers to reuse corrugated bulk bins multiple times. This reduces waste and provides a lower total cost of ownership compared to traditional one-way packaging.

Circular economy initiatives are also advancing, with suppliers investing in systems that reprocess corrugated polypropylene and recycled fibers into new high-quality packaging materials. By managing reusable ecosystems, packaging companies can unlock new revenue streams through long-term service contracts, offering value-added solutions such as cleaning, repair, and IoT-enabled tracking. This not only secures customer loyalty but also positions corrugated bulk bins as a strategic enabler of circular supply chains for global brands.

Competitive Landscape: Global Leaders Driving Corrugated Bulk Bin Innovations

The corrugated bulk bins market is shaped by multinational leaders that emphasize sustainability, product strength, and design innovation. Companies are competing by offering fit-for-purpose, recyclable, and cost-efficient solutions for agriculture, food, beverage, and industrial clients.

Smurfit WestRock expands global presence with sustainable bulk bins

Smurfit WestRock delivers a wide range of corrugated bulk packaging, including Octabins and pallet packs for bulk food and industrial goods. Its strength lies in a vertically integrated model, spanning forestry to finished bins. The July 2025 merger of Smurfit Kappa and WestRock created a global packaging leader with scale advantages and innovation capacity. The company is advancing designs like DryPack for seafood and paperboard beverage carriers, accelerating the transition away from EPS and plastics.

International Paper Company emphasizes recyclable corrugated solutions

International Paper provides customized corrugated bulk bins for industrial and agricultural use, recognized for their high strength and moisture-resistant coatings. As one of the largest producers of paperboard and linerboard from renewable resources, International Paper ensures sustainable sourcing. Its bins are widely adopted for produce logistics, where wet-strength liners are critical. The company continues to invest in manufacturing expansions and efficiency improvements, reinforcing its global leadership.

Packaging Corporation of America (PCA) strengthens industrial applications

PCA’s corrugated bulk bins, including its BulkMaster™ and Grid-Lok series, are engineered for stacking, stability, and automation compatibility. The company’s strength lies in customer-centric engineering, tailoring designs with features like reinforced flanges, self-locking bottoms, and coatings for industry-specific needs. PCA’s bins are especially popular in warehousing and agriculture, where they offer eco-friendly alternatives to plastic containers.

DS Smith Plc pioneers DryPack for perishable logistics

DS Smith is a recognized leader in sustainable corrugated packaging, with bulk bin solutions optimized for both transport and retail display. In May 2025, it launched DryPack for the seafood sector, replacing non-recyclable EPS foam. Its strategy centers on its purpose of “Redefining Packaging for a Changing World”, supported by investments in recycling infrastructure and supply chain optimization. DS Smith’s bins are a top choice for brands looking to enhance sustainability without compromising performance.

Mondi Group integrates corrugated with circular economy strategy

Mondi provides heavy-duty corrugated bins and bulk liquid containers combining durable liners with corrugated strength. In June 2025, it launched the re/cycle PaperPlus Bag Advanced, showcasing innovation in paper-based packaging. Mondi is committed to a 2030 circular economy strategy, validated by the Science Based Targets initiative (SBTi), with heavy investment in renewable energy such as its Slovakia biomass power plant. These moves position Mondi as a key innovator in corrugated sustainability.

Corrugated Bulk Bins Market Share Insights

Pallet Packs Lead Market Share by Product Type

Pallet packs (bulk boxes) dominate the corrugated bulk bins market with a 45% share in 2025, making them the industrial workhorse across diverse applications. Their universal pallet-sized design ensures seamless compatibility with forklifts, pallet jacks, and automated warehouse systems, which significantly reduces handling costs and improves supply chain efficiency. The balance between structural strength, cost-effectiveness, and sustainability has cemented pallet packs as the go-to solution for industries ranging from food to chemicals. Octabins, holding 25% of the market, are increasingly preferred for very heavy-duty loads such as auto parts or bulk food ingredients, thanks to their octagonal design that offers superior stacking strength. A rising trend is their dual function as retail-ready displays, allowing brands to leverage large printing surfaces for impactful marketing while cutting secondary packaging costs. Totes capture strong share as the preferred solution for in-plant logistics, particularly in automotive and electronics assembly, where efficient movement of small parts is critical. Hinged bulk bins cater to closed-loop logistics systems with reusable durability, aligning with sustainability goals in industries like automotive. Finally, custom containers address niche applications, offering specialized features such as internal supports, unique stacking designs, or moisture-resistant coatings to meet highly specific customer requirements.

Food & Beverage Drives Market Share by End-Use Industry

The food and beverage industry accounts for 30% of corrugated bulk bins demand in 2025, making it the single largest end-use segment. Bulk bins are essential for transporting raw commodities like grains, flour, and sugar as well as packaged finished goods, with moisture-resistant coatings and food-safe liners ensuring product integrity during storage and transit. Industrial equipment and parts represent 25% of the market, relying heavily on Octabins and pallet packs for shipping dense, high-value machinery and automotive components. Their ability to withstand rough handling and prevent costly damages makes corrugated solutions indispensable. Agriculture is another major driver, using breathable, stackable bins for moving fruits and vegetables from farms to processing facilities, highlighting their critical role in fresh food logistics. Electrical and electronics industries utilize partitioned totes and bins to protect sensitive components from abrasion and electrostatic discharge during assembly, supporting just-in-time manufacturing models. Chemicals and pharmaceuticals represent smaller but high-value segments, requiring lined bins with superior moisture barriers and chemical resistance to safeguard powders, pigments, and pharmaceutical raw materials. Collectively, these end-use industries underscore how corrugated bulk bins remain indispensable in balancing cost-efficiency, performance, and sustainability across global supply chains.

United States: Driving Sustainability with High-Strength Corrugated Bulk Bins

The U.S. corrugated bulk bins market is experiencing a strong shift from traditional wood and plastic containers toward recyclable corrugated alternatives, driven by growing corporate sustainability goals. Companies are increasingly adopting paper-based bulk packaging solutions to reduce environmental impact while maintaining durability for supply chain operations.

The rapid expansion of e-commerce and global logistics is a major catalyst, as corrugated bulk bins offer lightweight, collapsible designs that reduce shipping weight, fuel costs, and warehouse storage space. Innovations in triple-wall corrugated bins provide the strength of wood while remaining significantly lighter, making them ideal for transporting heavy, delicate, or high-value products. Advanced manufacturing technologies, including AI-powered vision systems for quality control, ensure consistent strength, durability, and performance, reinforcing their appeal in industrial, retail, and logistics sectors.

Germany: Leading Europe in Sustainable and Industrial Corrugated Solutions

Germany is at the forefront of sustainable packaging, with the corrugated bulk bins market focusing on high-recycled-content materials and full recyclability, in line with the European Green Deal. Manufacturers are replacing heavier metal and plastic alternatives with paper-based solutions, such as Mondi’s TankerBox, which enhances shipping capacity while reducing maintenance and environmental costs.

The market is predominantly B2B-driven, particularly in the automotive and industrial sectors, where lightweight, durable, and stackable packaging is essential for transporting parts and equipment efficiently. Germany’s emphasis on sustainable industrial logistics is encouraging continued innovation in high-performance corrugated bulk bins, including advanced design methods to maximize load capacity and minimize material usage.

China: Meeting Massive Industrial and E-Commerce Demand with Efficient Corrugated Bins

China dominates the global corrugated bulk bins market due to its expansive industrial manufacturing base and large consumer market. Industries ranging from food and beverages to electronics and automotive drive consistent high-volume demand for durable and protective bulk packaging.

Government initiatives aimed at modernizing logistics and supply chains further fuel demand, encouraging the adoption of cost-effective and efficient corrugated bulk bins. Chinese manufacturers are investing heavily in large-scale automated production lines, enabling high-volume output at competitive prices. The rapid growth of e-commerce in China has also increased the need for protective, lightweight, and stackable packaging solutions capable of handling high-frequency shipments while maintaining product integrity.

India: Cost-Effective and Innovative Corrugated Packaging for Agriculture and Food

India’s corrugated bulk bins market is significantly influenced by the country’s agricultural and food sectors, where the need for hygienic, stackable, and lightweight packaging for fresh produce, poultry, and processed foods is growing rapidly. Government initiatives to improve cold storage and supply chain infrastructure are further driving adoption, including export-grade bins for international shipments.

Cost-effectiveness is a key factor in India, making corrugated bulk bins a preferred alternative to wood and plastic containers. Domestic manufacturers are innovating to produce a wide range of specifications and load capacities, leveraging advanced design and manufacturing technologies to meet the diverse needs of industrial, agricultural, and retail clients. The focus on efficiency and sustainability positions India as a growing market for eco-friendly bulk packaging solutions.

Brazil: Sustainable and Lightweight Corrugated Bins for Agricultural Exports

Brazil’s corrugated bulk bins market is primarily driven by the country’s agricultural export sector, where high-strength, durable containers are essential for transporting bulk commodities like coffee, grains, and fresh produce over long distances. The market is also focused on lightweighting and sustainability, replacing heavier wood and plastic containers with recyclable corrugated alternatives to reduce transportation costs and environmental impact.

Brazilian manufacturers are innovating to deliver eco-friendly, high-performance corrugated bulk bins, aligning with global sustainability trends while maintaining product protection and operational efficiency. These solutions are increasingly adopted across both domestic logistics and export supply chains, reinforcing Brazil’s role as a significant player in the global corrugated bulk bins market.

Corrugated Bulk Bins Market Report Scope

Corrugated Bulk Bins market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$14.9 Billion

|

|

Market Size (2034)

|

$22.3 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Product Type (Pallet Packs, Hinged Bulk Bins, Totes, Octabins, Other Bulk Containers), By Format (Single Wall, Double Wall, Triple Wall), By Load Capacity (Less than 500 kg, 500–1500 kg, More than 1500 kg), By End-Use Industry (Food & Beverages, Industrial Equipment & Parts, Chemicals, Agriculture, Electrical & Electronics, Pharmaceuticals, Other End-Users)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

International Paper Company, WestRock Company, Greif, Inc., Mondi Group, Smurfit Kappa Group plc, Packaging Corporation of America, DS Smith plc, Sonoco Products Company, Shandong Yifeng Packing Technology Co., Ltd., The D.S. Smith Group, B&B Box Co., Inc., Tri-Wall Limited, Indevco Paper Containers, VISY Industries Australia Pty Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Corrugated Bulk Bins Market Segmentation

By Product Type

- Pallet Packs

- Hinged Bulk Bins

- Totes

- Octabins

- Other Bulk Containers

By Format

- Single Wall

- Double Wall

- Triple Wall

By Load Capacity

- Less than 500 kg

- 500–1500 kg

- More than 1500 kg

By End-Use Industry

- Food & Beverages

- Industrial Equipment & Parts

- Chemicals

- Agriculture

- Electrical & Electronics

- Pharmaceuticals

- Other End-Users

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Corrugated Bulk Bins Market

- International Paper Company

- WestRock Company

- Greif, Inc.

- Mondi Group

- Smurfit Kappa Group plc

- Packaging Corporation of America

- DS Smith plc

- Sonoco Products Company

- Shandong Yifeng Packing Technology Co., Ltd.

- The D.S. Smith Group

- B&B Box Co., Inc.

- Tri-Wall Limited

- Indevco Paper Containers

- VISY Industries Australia Pty Ltd.

*List not Exhaustive

Research Coverage

This USDAnalytics report investigates the global corrugated bulk bins market, highlighting breakthroughs in AI-driven design, sustainability initiatives, and innovative coatings for extreme conditions. The analysis reviews historical market trends from 2021 to 2024 and provides forecasts from 2025 to 2034, focusing on structural optimization, lightweighting technologies, and integration with smart logistics solutions. This report highlights the evolution of corrugated bins from traditional passive packaging into data-enabled assets, exploring applications in agriculture, food and beverage, industrial equipment, and pharmaceuticals. It reviews emerging opportunities such as IoT-enabled tracking, reusable closed-loop systems, and advanced moisture- and oil-resistant coatings. The report also profiles 15+ leading companies including Smurfit WestRock, International Paper, DS Smith, Mondi Group, Packaging Corporation of America, WestRock, Greif, and Sonoco Products Company analyzing strategic expansions, mergers, and product innovations that are reshaping the competitive landscape. This report is an essential resource for supply chain managers, packaging engineers, brand owners, and investors seeking insights into recyclability, operational efficiency, and the next-generation corrugated bulk bin designs that are transforming global logistics networks.

Scope Highlights:

- Segmentation: By Product Type (Pallet Packs, Hinged Bulk Bins, Totes, Octabins, Other Bulk Containers); By Format (Single Wall, Double Wall, Triple Wall); By Load Capacity (Less than 500 kg, 500–1500 kg, More than 1500 kg); By End-Use Industry (Food & Beverages, Industrial Equipment & Parts, Chemicals, Agriculture, Electrical & Electronics, Pharmaceuticals, Other End-Users).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historical and Forecast Data: Historical data from 2021 to 2024 and forecast data from 2025 to 2034.

- Company Analysis: In-depth coverage of 15+ leading companies, including International Paper Company, WestRock Company, Greif, Inc., Mondi Group, Smurfit Kappa Group plc, Packaging Corporation of America, DS Smith plc, Sonoco Products Company, Shandong Yifeng Packing Technology Co., Ltd., B&B Box Co., Inc., Tri-Wall Limited, Indevco Paper Containers, VISY Industries Australia Pty Ltd, and others.

Methodology

The study employs a comprehensive methodology combining primary and secondary research to provide accurate market insights. USDAnalytics conducted interviews with industry stakeholders such as corrugated bulk bin manufacturers, packaging engineers, logistics experts, and sustainability consultants to validate key trends. Secondary research included corporate reports, trade publications, academic studies, and government regulations. Quantitative analysis involved historical market sizing, CAGR calculations, and detailed segmentation by product type, format, load capacity, and end-use industry. Forecasting applied scenario-based modeling, accounting for sustainability regulations, automation adoption, e-commerce growth, and technological innovation. Competitive intelligence included company profiling, strategic initiatives, mergers, acquisitions, and product launches, offering industry professionals actionable insights into market evolution, operational efficiencies, and supply chain optimization.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.