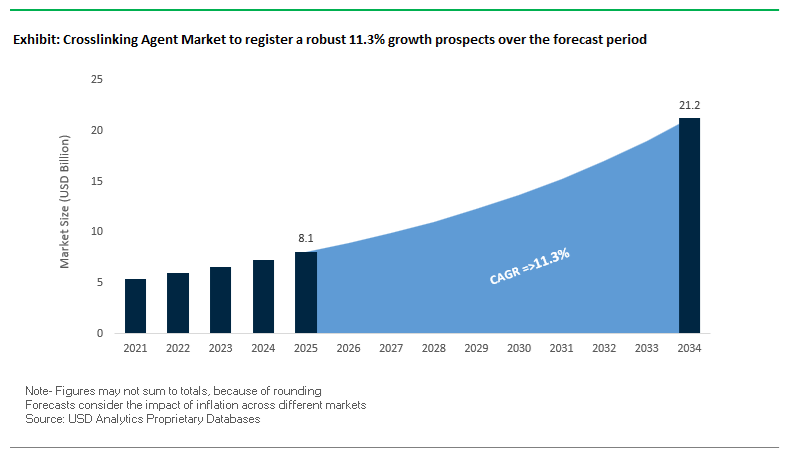

The global crosslinking agent market is witnessing increased demand from end-user industries with increasing preference for coating durability, chemical resistance, and lifecycle performance for higher asset value and maintenance economics. Valued at USD 8.1 billion in 2025 and projected to reach USD 21.2 billion by 2034 at a CAGR of 11.3%, the market’s growth reflects rising specification intensity across automotive OEM coatings, industrial protective systems, aerospace composites, and advanced adhesive formulations. As manufacturers push for longer service intervals, thinner coating builds, and higher operating temperatures, crosslinking agents are no longer auxiliary additives but core enablers of modern performance-driven material systems.

Demand is being structurally reshaped by the transition toward high-solids, waterborne, and low-VOC formulations, alongside tighter OEM durability requirements. Amino and isocyanate crosslinkers remain dominant in automotive and heavy industrial coatings because they deliver predictable film hardness, solvent resistance, and weatherability under aggressive service conditions. Manufacturer-qualified melamine-formaldehyde systems demonstrate resistance to 72-hour exposure in 10% sulfuric acid, supporting their continued use in coil coatings, appliance finishes, and industrial enamels. In parallel, aliphatic polyisocyanates, widely specified in OEM clearcoats and protective topcoats, consistently retain over 90% gloss after 2,000 hours of QUV-A exposure, a performance threshold aligned with long-term exterior durability requirements in automotive, aerospace, marine, and bridge coatings. These benchmarks explain why crosslinker selection is increasingly dictated by end-use exposure profiles rather than cost per kilogram.

At the same time, sustainability and production efficiency are redefining competitive differentiation. Waterborne and bio-based crosslinkers, including polyfunctional aziridines and carbodiimides, are gaining adoption in architectural coatings, wood finishes, and flexible packaging adhesives as formulators target VOC levels below 50 g/L to comply with EU REACH, EPA, and CARB limits. Beyond compliance, fast-reacting crosslinkers are unlocking measurable operational gains: in reactive hot-melt adhesive (RHM) systems, modern crosslinking chemistries enable attainment of approximately 80% of final bond strength within 24 hours, accelerating line speeds and reducing work-in-progress inventory in packaging, electronics assembly, and consumer goods manufacturing. Over the forecast period, market momentum will increasingly favor crosslinking agents that combine regulatory compliance, predictable cure kinetics, and compatibility with automated, high-throughput manufacturing, reinforcing their role as a foundational technology in next-generation coatings, adhesives, and composite systems.

The global crosslinking agent industry is undergoing rapid transformation as chemical producers pursue capacity expansion, bio-based product innovation, and digital process optimization to support the next generation of coating and adhesive systems.

In May 2025, Arkema’s Bostik division announced a $27 million investment in its Middleton, Massachusetts facility to enhance production of high molecular weight polyesters, foundational materials in heat-activated and recyclable adhesives. This expansion not only strengthens Arkema’s position in the reactive hot melt and flexible packaging sectors but also aligns with the global transition toward compostable and recyclable materials.

Meanwhile, BASF Corporation continues to focus on self-crosslinking acrylic dispersions under its Joncryl® and Acronal® product lines, optimized for glycol ether-free, low-VOC wood coatings and printing inks. By integrating rapid cure capability with exceptional gloss retention, BASF is meeting the increasing demand for eco-efficient coating solutions in both decorative and industrial markets.

In late 2024, Evonik Corporation reinforced its dominance in isophorone chemistry with the expansion of its VESTANAT® polyisocyanate portfolio for light-stable polyurethane coatings used in wind turbine blades and automotive exteriors. Similarly, Dow Chemical Company advanced its SI-LINK™ moisture-curable silane systems, critical in wire and cable insulation to meet RoHS and UL-44 compliance standards for modern electrical infrastructure.

Nippon Shokubai, through its ZIRCOSTAR™ hybrid particles and EPOCROS™ WS/K series, continued leveraging proprietary synthesis technologies to support crosslinking in water-based formulations for optical, electronic, and high-performance coatings. On a regulatory front, new PFAS restrictions imposed across the EU and US in late 2024 accelerated the shift toward non-fluorinated carbodiimide and epoxy crosslinkers, as formulators seek environmentally compliant alternatives with equal or superior water repellency.

Furthermore, industry consolidation reshaped the value chain landscape. Honeywell’s $18.6 billion acquisition of Carrier Global’s Access Solutions in September 2024 expanded its footprint in the HVAC and coatings infrastructure segments, major consumers of polyurethane-based crosslinked coatings. The merger between Synopsys and ANSYS, anticipated in early 2025, also carries downstream implications by enabling AI-optimized composite material simulation, ultimately improving epoxy and polyurethane crosslinker design precision.

The transition toward low-temperature and energy-efficient crosslinking systems represents a critical trend in the global coatings, composites, and polymer markets. The increasing demand for energy savings, faster processing speeds, and compatibility with temperature-sensitive substrates has accelerated R&D into reactive systems that cure effectively under ambient or near-ambient conditions.

Industrial validation has demonstrated tangible performance and cost benefits. For instance, low-temperature-curing powder coatings combined with infrared (IR) booster drying have been reported to enhance energy efficiency by up to 50%, translating into annual energy cost savings of several hundred thousand euros for large-scale industrial plants. The optimization not only aligns with global decarbonization goals but also supports manufacturers’ sustainability KPIs by minimizing carbon footprint per production unit.

Additionally, moisture-accelerated polyurethane crosslinking systems exhibit remarkable process efficiency, with studies reporting hardness development 5–10 times faster than traditional thermally cured coatings. The rapid-curing behavior enables a 30–100% increase in production throughput, making it ideal for high-speed finishing lines in automotive, aerospace, and construction applications.

From a substrate protection standpoint, low-temperature crosslinkers are essential for processing heat-sensitive materials, including advanced aluminum alloys (e.g., 2024-grade used in aerospace). Military coatings research drives the need to achieve full crosslinking at or below 120°C, ensuring material integrity while achieving maximum coating durability. The adoption of these advanced, energy-efficient systems is set to redefine curing technologies, promoting operational cost efficiency and improved sustainability across industrial value chains.

Stringent regulatory restrictions on isocyanates and VOC emissions are reshaping formulation strategies across the crosslinking agent landscape. The global shift toward non-isocyanate, low-VOC, and label-free crosslinkers is leading to the rapid development of safer, high-performance alternatives with reduced toxicity and enhanced environmental profiles.

One of the most notable advancements is the adoption of polycarbodiimide (PCD) crosslinkers, which provide non-mutagenic, label-free alternatives to conventional isocyanates and aziridines in waterborne coatings and adhesives. PCD-based systems allow room-temperature curing, offer excellent pot life, and significantly improve film toughness and water resistance. Experimental data indicates that the inclusion of PCD crosslinkers in waterborne polyurethane (WPU) adhesives can reduce the water swelling rate from over 400% to nearly 126%, confirming the improvement in crosslinked network density and hydrophobicity.

Parallel R&D in Non-Isocyanate Polyurethane (NIPU) technology is opening pathways to bio-based production models. A 2024 academic breakthrough demonstrated vegetable-oil-derived NIPU adhesives with a lap shear strength of 8.26 MPa, proving their ability to compete with petroleum-based analogs in high-strength applications. As regulatory pressure intensifies, particularly in Europe and North America under REACH and OSHA standards, non-isocyanate systems are poised to dominate coatings, adhesives, and flexible polymer formulations across industries.

The accelerating production of bio-based plastics, resins, and coatings has created a crucial need for compatible crosslinking technologies that can enhance mechanical and thermal performance, ensuring these materials achieve parity with conventional petrochemical polymers. Crosslinkers are becoming the functional bridge between sustainability and performance, particularly in applications requiring chemical durability and dimensional stability.

For example, in thermoplastic systems such as bio-based polyethylene or polyethylene blends, the integration of peroxide crosslinkers can improve thermal deformation resistance by over 22%, elevating peak heat distortion temperatures to approximately 80°C. The modification directly expands the use of bio-derived polymers in automotive and industrial applications where heat exposure is significant.

Similarly, in natural polymer systems, notably gelatin and polysaccharide films—crosslinking has been shown to increase denaturation temperatures from 43°C to over 72°C, significantly improving stability and tensile properties for biomedical and packaging applications. The rising demand for biocompatible and recyclable polymer systems has made chemical crosslinking indispensable to the functionality of next-generation sustainable materials.

The exponential growth of the electric vehicle (EV) market has introduced a lucrative frontier for the crosslinking agent industry. With battery architectures becoming more energy-dense, compact, and thermally complex, advanced crosslinkers play a critical role in improving mechanical resilience, electrochemical stability, and thermal management within lithium-ion and solid-state batteries.

In Silicon (Si)-based anodes, which experience up to 300% volumetric expansion during charge-discharge cycles, 3D crosslinked polymer binders are vital for dissipating internal mechanical stress. Cutting-edge research has demonstrated that dynamic covalent bond networks—incorporating boronic ester and hydrogen bonding mechanisms—help maintain electrode integrity under extreme cycling conditions.

Experimental results further highlight that 3D crosslinked binder systems in LiFePO4 cathodes preserve capacity retention over 200 charge-discharge cycles, significantly outperforming traditional polyvinylidene fluoride (PVDF) binders that degrade rapidly under similar conditions. Additionally, crosslinked matrices enhance thermal and electrochemical stability, minimizing side reactions at elevated temperatures and ensuring long-term battery safety.

The crosslinking revolution extends to battery pack materials, including sealants, encapsulants, and thermal interface materials (TIMs), where controlled crosslinked networks provide the thermal conductivity and mechanical adhesion required for next-generation EV designs. As global EV production scales, the demand for advanced polymeric crosslinkers for energy storage materials is expected to rise sharply through 2030 and beyond.

Crosslinking Agent Market Share Insights, 2025-2034

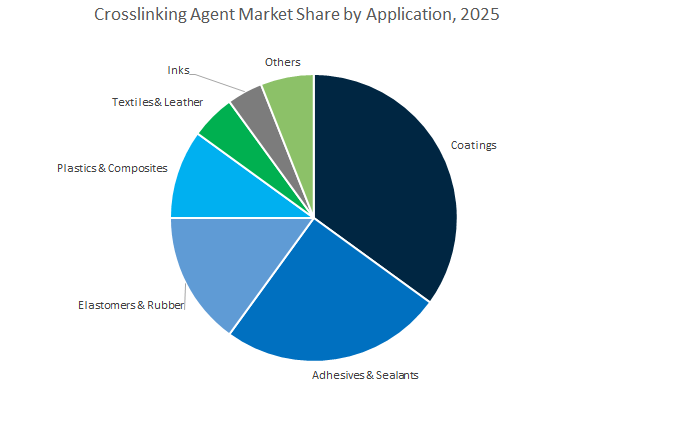

The coatings segment remains the largest consumer of crosslinking agents, accounting for 32.6% of the projected 2025 market share. Crosslinkers are indispensable in formulating high-performance coatings that exhibit superior chemical resistance, weatherability, hardness, and gloss retention—qualities essential in automotive, architectural, industrial, and protective coatings. Polyisocyanates, melamine formaldehyde, and blocked isocyanates are among the most commonly used crosslinkers in two-component polyurethane and alkyd systems, enabling the formation of durable thermoset films. The rise in eco-friendly and high-solids coatings further boosts demand for advanced low-VOC crosslinkers such as polycarbodiimides and aziridines. As industries transition to waterborne and UV-curable technologies, crosslinking agents that can function efficiently under low-temperature and high-efficiency curing conditions are becoming increasingly important, reinforcing the segment’s dominance.

The adhesives and sealants industry holds the second-largest market share at 21.9%, fueled by the need for stronger, more durable, and heat-resistant bonding materials. Crosslinking agents are central to the conversion of thermoplastic polymers into robust thermoset networks, providing critical improvements in cohesive strength, chemical resistance, and environmental durability. In polyurethane adhesives, isocyanate-based crosslinkers are widely employed for their moisture-curing capability, while polyfunctional aziridines and carbodiimides enhance the performance of waterborne adhesives. Epoxy systems rely heavily on amine and anhydride crosslinkers for structural bonding in automotive, aerospace, and electronics assembly.

Beyond coatings and adhesives, elastomers and plastics represent substantial application segments that account for a significant portion of market demand. In elastomers and rubber, crosslinking (or vulcanization) is the foundational process that transforms soft, sticky polymers into elastic, resilient materials suitable for tires, seals, and hoses. Sulfur-based and peroxide crosslinkers dominate this domain, while newer formulations are designed for improved heat and aging resistance. In plastics and composites, crosslinking agents such as peroxides, silanes, and triallyl isocyanurate enhance thermal stability, solvent resistance, and mechanical strength, extending the utility of thermoplastics in high-performance applications like cable insulation and automotive components. The textiles, inks, and biomedical sectors represent smaller but growing markets. In textiles, crosslinkers impart wrinkle resistance, wash durability, and flame retardancy, while in printing inks, they improve adhesion, rub resistance, and drying speed.

The liquid form dominates the global crosslinking agent market, representing 64.2% of the total share in 2025. This dominance stems from their superior mixing uniformity, compatibility with liquid resin systems, and adaptability to continuous production processes. Liquid crosslinkers are widely used across coatings, adhesives, sealants, and polymer compounding, where controlled viscosity and easy dispersion are crucial for achieving consistent curing reactions. In particular, polyisocyanates, amine-based, and epoxy crosslinkers are the backbone of liquid formulations, ensuring precise reaction kinetics in solvent-borne and waterborne systems. The segment also benefits from strong alignment with global manufacturing trends toward automated, high-throughput production lines, where liquid forms support consistent dosing and reduced processing time. Additionally, liquid crosslinkers play a key role in the rapid expansion of UV-curable and two-component systems, especially in industrial coatings and flexible packaging applications where performance, clarity, and speed of cure are critical.

Powder crosslinking agents occupy the second-largest share, primarily serving applications that involve dry polymer systems or powder processing, such as powder coatings, hot-melt adhesives, and thermoplastic composites. They are integral to polyester–epoxy hybrid systems, where they enable crosslinking during the curing stage without the need for solvents. Powder crosslinkers also provide excellent shelf stability and are easily blended into dry formulations, making them ideal for environmentally friendly and solvent-free production environments. With the global shift toward sustainable manufacturing, powder-based formulations are gaining traction due to their near-zero VOC emissions and waste reduction benefits, particularly in industrial and architectural coatings markets.

Meanwhile, solid and granular crosslinkers serve specialized roles in high-temperature polymer processing and vulcanization, such as in rubber compounding, thermoset molding, and composite fabrication. Their physical stability allows for precise control over reaction timing and release, which is essential for large-scale industrial operations requiring consistent performance under heat and pressure. These forms are commonly used in cable insulation, molded rubber components, and high-performance plastics where mechanical strength, electrical insulation, and resistance to degradation are paramount.

The crosslinking agent market is dominated by leading chemical companies integrating polymer innovation, sustainability, and advanced curing chemistry. The competitive landscape is defined by large-scale producers like BASF, Dow, Evonik, Arkema, Nippon Shokubai, and Covestro, each pursuing specialized strategies across the coatings, adhesives, and composites sectors.

BASF continues to set the benchmark in sustainable coating chemistry, leveraging its vertically integrated operations and robust R&D infrastructure. Its Luwipal® and Plastopal® amino resins remain essential for baking finishes and OEM coatings, while the Joncryl® and Acronal® self-crosslinking systems lead the shift toward glycol ether-free, low-VOC wood coatings. The company’s Basonat® polyisocyanates form the backbone of high-durability polyurethane systems, ensuring optimal hardness, gloss, and chemical resistance. Combined with Tinuvin® light stabilizers, BASF offers complete performance enhancement packages for long-term exterior protection.

Dow has cemented its leadership in silane and peroxide crosslinking chemistry, particularly through its SI-LINK™ moisture-curable systems for wire and cable insulation. Its ENDURANCE™ polyethylene compounds deliver thermal stability and electrical reliability for high-voltage cable applications. Dow’s focus on water-tree retardant formulations and catalyst masterbatch integration significantly enhances curing speed and process efficiency for manufacturers.

Evonik stands as a global technology leader in isophorone diisocyanate (IPDI) and epoxy curing systems. Its VESTANAT® aliphatic polyisocyanates provide UV stability and high gloss retention, key for automotive and wind energy coatings. Complementary products such as Ancamine® and Ancamide® epoxy curing agents deliver superior mechanical strength and corrosion protection. Evonik’s R&D also prioritizes latency-controlled imidazole systems (Imicure®) and VESTAGON® solid crosslinkers for powder coatings, ensuring consistent curing in high-speed industrial applications.

Arkema, through its Bostik division, is intensifying investments in reactive and sustainable adhesive technologies. The company’s $27 million expansion in Middleton, MA, underscores its commitment to high molecular weight polyester production, foundational for heat-activated and recyclable adhesives. Arkema’s synergy between specialty polymers and adhesives enables high-performance bonding for flexible packaging and transportation materials, while its recyclable polyester adhesives cater to the circular economy trend.

Nippon Shokubai excels in functional monomer and fine particle technology, supplying EPOCROS™ WS/K oxazoline polymers that serve as efficient crosslinkers in waterborne coatings and adhesives. Its SOLIOSTAR™ hybrid fine particles enhance hardness and optical clarity, while POLYMENT™ aminoethylated polymers deliver tailored adhesion and film properties. The company’s ongoing R&D into organic-inorganic hybrid crosslinkers positions it as a frontrunner in sustainable high-performance coating systems.

Covestro maintains strong leadership in polyurethane chemistry, producing large-scale volumes of MDI, TDI, and HDI isocyanates for coatings, adhesives, and elastomers. Its CO₂-based polyurethane raw materials highlight a strategic shift toward carbon-circular materials. The company also advances UV-curable systems utilizing functional oligomers and prepolymers, key for ultra-fast curing in automotive refinish and graphic coatings. Covestro’s expanding waterborne PUD portfolio relies on hydrophilic crosslinkers designed for next-generation eco-friendly polyurethane dispersions.

China continues to dominate the Asia-Pacific crosslinking agent market, driven by its rapid industrialization and regulatory transition toward low-VOC, waterborne chemistries. Wanhua Chemical Group Co., Ltd., a leading producer of isocyanate crosslinking agents, is significantly expanding its global reach through new facilities and exports of MDI and TDI-based crosslinkers for high-performance coatings. The government’s “Made in China 2025” initiative has mobilized investments into R&D for high-end crosslinking technologies catering to electronics, NEV batteries, and industrial coatings, reinforcing self-sufficiency in specialty chemicals.

Environmental policies, including the Blue Sky Protection Campaign, are accelerating the replacement of solvent-based crosslinkers with eco-compliant waterborne and powder coating alternatives. The establishment of integrated chemical parks across coastal provinces is enhancing vertical integration for feedstock production, reducing import dependency. The booming automotive and NEV sectors are the largest consumers of heat- and corrosion-resistant crosslinking agents, essential for battery encapsulation, lightweight composites, and e-mobility coatings. Meanwhile, the government’s support for biomedical and life sciences R&D has broadened applications of crosslinking reagents in tissue engineering and drug delivery.

Germany remains a core innovation hub in the European crosslinking agents industry, powered by its strong regulatory framework, automotive integration, and advanced R&D infrastructure. Leading chemical producers like BASF SE, Covestro AG, and Evonik Industries AG are developing bio-based polyisocyanate and urethane-alkoxysilane crosslinkers, aligning with the EU Circular Economy Action Plan and Green Deal mandates. German laboratories are pioneering non-isocyanate polyurethane (NIPU) systems, leveraging renewable feedstocks such as bio-derived diols and aliphatic amines.

Collaborations between crosslinking material suppliers and German automotive OEMs (BMW, Volkswagen) drive the creation of high-durability, scratch-resistant coatings for electric vehicle platforms. Additionally, AI-integrated digital synthesis is enhancing production accuracy for complex crosslinkers, ensuring low emissions and consistent curing performance. Regulatory pressures under REACH have fast-tracked the transition toward low-toxicity carbodiimide and blocked isocyanate systems, reducing occupational exposure risks. Germany’s commitment to wind energy and advanced composites continues to expand opportunities for crosslinkers with high fatigue resistance and long-term weatherability.

The U.S. crosslinking agent market is accelerating through government-backed infrastructure spending, sustainability initiatives, and cutting-edge research in epoxy, amine, and aziridine chemistries. Huntsman Corporation and Dow Inc. are expanding portfolios in specialty polyurethane and epoxy crosslinking agents for aerospace, oil & gas, and marine coatings, focusing on corrosion resistance and thermal endurance. Research led by the North Dakota State University Research Foundation is advancing biobased crosslinkers from vanillin and lignin, supporting the industry’s transition toward renewable, low-carbon materials.

The strong growth of the construction and woodworking sectors drives large-scale adoption of self-crosslinking acrylic latexes and one-component systems (1K) optimized for fast cure and low VOCs. Companies such as PolyAziridine LLC are pioneering water-based difunctional adhesive crosslinkers designed to enhance chemical and wet adhesion in waterborne coatings and inks. The surge in composite and 3D printing materials further strengthens U.S. leadership in next-generation crosslinkers engineered for defense, energy, and medical-grade polymers.

Japan’s crosslinking agent market stands at the forefront of high-performance electronic, automotive, and optical materials innovation. Companies like Nippon Shokubai Co. Ltd. are leading in ultra-pure specialty crosslinking monomers tailored for semiconductors, OLEDs, and optical adhesives. Advanced R&D focuses on UV-curable and heat-resistant epoxy crosslinkers that offer rapid curing, mechanical durability, and excellent thermal stability for miniaturized electronic assemblies.

Japanese research consortia are actively exploring photo-reversible and self-healing polymer networks, integrating smart crosslinking chemistries for future-ready protective coatings. As the automotive sector pivots toward lightweight vehicles and high-gloss finishes, demand is growing for precisely controlled crosslinking formulations in OEM and refinish coatings. Expansions in carbodiimide-based non-isocyanate crosslinkers also demonstrate Japan’s commitment to worker safety and environmental compliance in precision manufacturing.

South Korea’s rapid ascent as a global battery and display manufacturing hub makes it one of the most dynamic markets for crosslinking agents. Domestic chemical companies are developing specialized crosslinkers to improve the electrochemical and mechanical stability of lithium-ion batteries, targeting better thermal management and cycle life. The expansion of OLED and flexible display production has triggered rising adoption of optically clear, UV-stable crosslinking agents that retain flexibility and adhesion under repeated bending stresses.

R&D in elastomer and polymer modification is focused on optimizing crosslinking density and molecular uniformity, enhancing long-term seal integrity in EVs, smart devices, and packaging applications. South Korean firms are also engaging in partnerships with universities to commercialize next-gen polyfunctional crosslinkers for EV insulation coatings and adhesive films.

India’s fast-evolving construction, coatings, and automotive sectors are generating strong demand for high-performance crosslinking agents. The National Infrastructure Pipeline (NIP) and Smart City Mission projects are accelerating consumption of epoxy and polyurethane curing agents used in protective and architectural coatings. Domestic chemical manufacturers, under the “Make in India” framework, are scaling localized production of amino and aziridine crosslinkers, reducing import dependency and promoting self-reliance.

Growing regulatory focus on low-VOC, waterborne systems is transforming market preferences toward environmentally compatible formulations. Indian R&D efforts are intensifying on aqueous crosslinking technologies capable of delivering robust film integrity, especially for tropical and high-humidity construction environments. Moreover, expanding automotive and consumer goods manufacturing continues to require highly crosslinked adhesive systems with superior durability and aesthetic consistency.

Crosslinking Agent Market Report Scope

Crosslinking Agent Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.1 Billion

|

|

Market Size (2034)

|

$21.2 Billion

|

|

Market Growth Rate

|

11.3%

|

|

Segments

|

By Type (Isocyanate Crosslinking Agents, Amino Crosslinking Agents, Amine/Polyamide Curing Agents, Aziridine Crosslinking Agents, Carbodiimide Crosslinking Agents, Silane Crosslinking Agents, Peroxide Crosslinking Agents, Phenolic Crosslinkers, Bio-based/Natural Crosslinking Agents), By Application (Coatings, Adhesives & Sealants, Elastomers & Rubber, Plastics & Composites, Inks, Textiles & Leather, Pulp & Paper, Personal Care & Cosmetics, Biomedical & Pharmaceutical), By Form (Liquid Crosslinking Agents, Powder Crosslinking Agents, Solid/Granular Crosslinking Agents), By System Type (One-Component Crosslinking Systems, Two-Component Crosslinking Systems, Radiation-Cured Systems

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Covestro AG, Huntsman Corporation, Evonik Industries AG, Dow Inc., Wanhua Chemical Group Co., Ltd., Allnex GMBH, Aditya Birla Chemicals, Nippon Shokubai Co. Ltd., Mitsubishi Chemical Corporation, AkzoNobel N.V., Nouryon, Solvay S.A., Hexion Inc., Perstorp Holding AB

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Type/Chemistry

- Isocyanate Crosslinking Agents

- Amino Crosslinking Agents

- Amine/Polyamide Curing Agents

- Aziridine Crosslinking Agents

- Carbodiimide Crosslinking Agents

- Silane Crosslinking Agents

- Peroxide Crosslinking Agents

- Phenolic Crosslinkers

- Bio-based/Natural Crosslinking Agents

By Application/End-Use

- Coatings

- Adhesives & Sealants

- Elastomers & Rubber

- Plastics & Composites

- Inks

- Textiles & Leather

- Pulp & Paper

- Personal Care & Cosmetics

- Biomedical & Pharmaceutical

By Form

- Liquid Crosslinking Agents

- Powder Crosslinking Agents

- Solid/Granular Crosslinking Agents

By System Type

- One-Component Crosslinking Systems

- Two-Component Crosslinking Systems

- Radiation-Cured Systems

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- BASF SE

- Covestro AG

- Huntsman Corporation

- Evonik Industries AG

- Dow Inc.

- Wanhua Chemical Group Co., Ltd.

- Allnex GMBH

- Aditya Birla Chemicals

- Nippon Shokubai Co. Ltd.

- Mitsubishi Chemical Corporation

- AkzoNobel N.V.

- Nouryon

- Solvay S.A.

- Hexion Inc.

- Perstorp Holding AB

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Global Crosslinking Agent Market with a sharp focus on how chemistry choices translate into coating durability, adhesive cohesion, and composite reliability; it delivers analysis reviews of performance metrics (chemical/UV resistance, gloss retention, cure speed, film toughness), surfaces technology breakthroughs in low-VOC, non-isocyanate, and energy-efficient curing systems, and highlights end-use qualification pathways for automotive OEM, architectural, protective, and electronics applications. Mapping regulation to formulation strategy and capex to throughput gains, this report is an essential resource for CTOs, formulators, operations leaders, procurement teams, and investors aligning sustainability targets with high-performance results across coatings, adhesives & sealants, elastomers, plastics, inks, textiles, and biomedical uses.

Scope Highlights

Segmentation:

- By Type/Chemistry: Isocyanate Crosslinking Agents; Amino Crosslinking Agents; Amine/Polyamide Curing Agents; Aziridine Crosslinking Agents; Carbodiimide Crosslinking Agents; Silane Crosslinking Agents; Peroxide Crosslinking Agents; Phenolic Crosslinkers; Bio-based/Natural Crosslinking Agents.

- By Application/End-Use: Coatings; Adhesives & Sealants; Elastomers & Rubber; Plastics & Composites; Inks; Textiles & Leather; Pulp & Paper; Personal Care & Cosmetics; Biomedical & Pharmaceutical.

- By Form: Liquid Crosslinking Agents; Powder Crosslinking Agents; Solid/Granular Crosslinking Agents.

- By System Type: One-Component Crosslinking Systems; Two-Component Crosslinking Systems; Radiation-Cured Systems.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Frame: Historic data 2021–2024 and forecasts 2025–2034.

Companies: 15+ company analyses/profiles covering strategies, portfolios, capacity moves, and innovation pipelines.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.