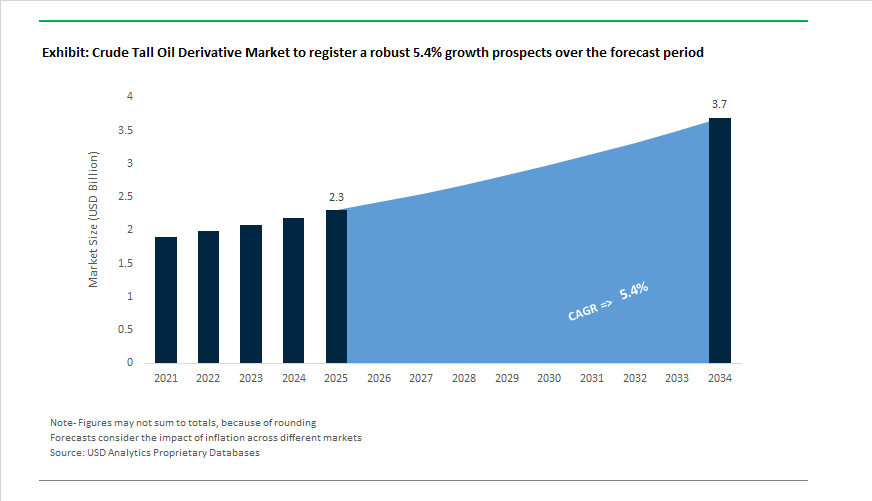

Crude Tall Oil Derivative Market to Reach $3.7 Billion by 2034 at 5.4% CAGR Amid Portfolio Realignment and Biofuel Diversification

The Crude Tall Oil Derivative Market is projected to grow from $2.3 billion in 2025 to $3.7 billion by 2034, registering a CAGR of 5.4%. Crude tall oil derivatives including tall oil fatty acids (TOFA), tall oil rosin, distilled tall oil (DTO), and tall diesel remain essential feedstocks for adhesives, printing inks, rubber compounding, coatings, lubricants, animal nutrition, and renewable fuels. Market growth is being driven by expanding demand for bio-based hydrocarbon oils, sustainable aviation fuel, renewable diesel, and certified low-carbon pine chemicals. At the same time, leading producers are restructuring refinery footprints and renegotiating long-term CTO supply agreements to mitigate feedstock volatility and margin compression.

A major inflection point occurred in February 2024, when Kraton Corporation launched its SYLVASOLV™ 1000 product under the SYLVASOLV™ biobased oil platform. Derived entirely from crude tall oil, this hydrocarbon oil targets agricultural applications by enhancing fertilizer coating performance and pesticide delivery efficiency while reducing dependence on petroleum-based carriers. In April 2024, the St1 and SCA joint venture began commercial operations at its Gothenburg biorefinery in Sweden, converting CTO and waste fats into Sustainable Aviation Fuel and renewable diesel, significantly expanding CTO-to-biofuel capacity in the Nordic region. During 2024, SunPine AB reported record production at its Piteå facility, highlighting growing demand for bio-rosin fractions in adhesives and printing inks as customers shift toward renewable resin systems. Forchem strengthened the specialty segment in 2024–2025 through expanded distribution of its Progres® feed additive derived from tall oil resin acids, supported by field data confirming reduced antibiotic usage in livestock and earning multiple EU innovation recognitions.

Strategic portfolio rationalization intensified in February 2025, when Ingevity disclosed a $100 million payment to terminate a long-term CTO supply contract, reducing exposure to high-cost feedstock as it pivots toward higher-margin Performance Materials. In May 2025, UPM cancelled its planned Rotterdam biomass-to-fuels refinery following a technical and commercial review, redirecting capital toward its Lappeenranta biofuels site and Leuna biochemicals expansion instead of expanding large-scale CTO fuel capacity in Europe. In September 2025, Ingevity entered into a definitive agreement to divest its North Charleston CTO refinery and much of its Industrial Specialties product line to Mainstream Pine Products, reinforcing its strategic repositioning. Pricing pressures became evident in November 2025, when Kraton announced at least a 10% TOFA price increase in EMEA effective January 2026, citing persistent inflation and production cost challenges. Sustainability certification accelerated in January 2026, as Kraton’s Panama City facility achieved ISCC PLUS certification, enabling mass-balance tall oil derivatives for adhesives, coatings, and tire markets that require traceable renewable content. Leadership transition at Ingevity in January 2026, with the appointment of Sangwoo Ryu as CEO, aligns with the company’s continued streamlining through 2026. UPM further reinforced its sustainability positioning by receiving a Leadership score in the CDP 2025 assessment, underscoring the increasing importance of transparent carbon accounting and renewable feedstock integration across the global crude tall oil derivative value chain.

Trends and Opportunities in the Global Crude Tall Oil (CTO) Derivative Market

Feedstock Scarcity Driving Long-Term Offtake and Vertical Integration

- The structural limitation of CTO supply is intensifying competition for feedstock and accelerating a decisive shift away from spot-market procurement toward long-term offtake agreements and vertically integrated models. As global kraft pulp capacity grows at a slower pace than biofuel and biochemical demand, CTO availability is becoming increasingly constrained. In August 2025, Kraton Corporation and International Paper entered into a Strategic Continuity of Services Agreement to secure uninterrupted CTO supply for Kraton’s Savannah operations. This agreement reflects a broader industry pattern in which derivative producers are locking in multi-year access to pine-based pulping by-products to protect operational continuity.

- Pricing power is increasingly shifting toward feedstock holders and biofuel-aligned processors. In the EMEA region, constrained fractionation capacity and rising input costs prompted Kraton to announce a general price increase of 10% or more on all Tall Oil Fatty Acids, effective January 1, 2026. This move underscores the growing influence of renewable fuel producers, particularly those supplying sustainable aviation fuel, who can absorb higher feedstock premiums compared with traditional alkyd resin, ink, and adhesive manufacturers. As a result, CTO derivatives are moving from cost-driven commodity positioning toward value-based pricing models.

Advanced Fractionation Unlocking Pharmaceutical and Personal Care Grades

- To maximize value extraction from limited CTO volumes, processors are investing heavily in advanced fractionation and purification technologies. By late 2025, membrane separation, multi-stage distillation, and enzymatic refining had reached commercial-scale deployment, enabling the production of ultra-pure oleic and linoleic acid streams with improved color stability, reduced odor, and tighter compositional control. These attributes are essential for personal care and cosmetic formulations, where bio-based origin alone is insufficient without sensory and performance consistency.

- This trend is reinforcing the shift of CTO fractions into circular and premium polymer applications. In October 2025, UPM Biofuels and LUMENE expanded their collaboration to develop cosmetics packaging based on wood-derived plastics produced from bio-naphtha. This forest-to-face value chain demonstrates how CTO derivatives are increasingly diverted away from low-grade fuel uses and into higher-margin, circular materials aligned with brand-level sustainability commitments and clean-label positioning.

CTO as a Critical Feedstock for Sustainable Aviation Fuel Expansion

- The global push toward aviation decarbonization is positioning CTO as one of the most strategic residue-based feedstocks for the Hydroprocessed Esters and Fatty Acids pathway. Regulatory mandates are providing long-term demand visibility. As of January 2025, the European Union implemented a mandatory 2% SAF blending requirement, with the target set to rise to 6% by 2030. This regulatory baseline has catalyzed large-scale capacity investments, including Neste’s €2.5 billion expansion of its Rotterdam renewables refinery, a cornerstone of its plan to reach 6.8 million tons of renewable production capacity by 2027.

- Strategic offtake agreements are reinforcing CTO’s role in aviation fuel supply chains. In late 2025, Neste finalized SAF supply partnerships with Cathay Group, United Airlines, and DHL Express at Singapore Changi Airport. These agreements highlight how residue-based feedstocks such as CTO are becoming indispensable for airlines and logistics providers seeking to meet near-term emissions targets in the absence of scalable synthetic fuel alternatives.

Tall Oil Sterols as High-Margin Inputs for Nutrition, Pharma, and Cosmeceuticals

- Beyond fuels, CTO-derived sterols are emerging as a high-margin growth avenue, particularly as a reliable alternative to soy-based phytosterols. CTO sterols offer greater supply consistency and lower exposure to agricultural seasonality, making them attractive for functional nutrition and pharmaceutical applications. During 2024 and 2025, industry leaders such as BASF with its Vegapure® portfolio and Cargill with CoroWise® expanded sterol-fortified offerings, with growing interest in CTO-based sterols as precursors for steroid Active Pharmaceutical Ingredients.

- Cosmeceuticals represent an additional premium outlet. Clinical evaluations conducted in 2025 confirmed that tall oil sterol esters enhance skin barrier function and emulsion stability in high-end formulations, delivering approximately 25% higher moisture retention compared with synthetic mineral oils. This performance advantage is accelerating adoption in anti-aging and sensitive-skin products, positioning CTO sterols at the core of the rapidly expanding nature-identical and bio-based personal care ingredient market.

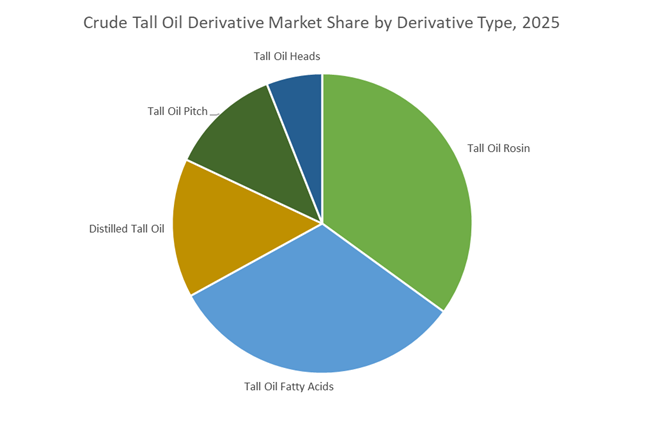

Crude Tall Oil Derivative Market Share and Segmentation Insights

Derivative Type Breakdown: Tall Oil Rosin Leads While Fatty Acids Support Industrial Bio-Based Transition

Tall oil rosin holds approximately 35% market share in 2025, driven by extensive use in pressure-sensitive adhesives, road marking paints, paper sizing, and rubber emulsifiers as a renewable alternative to petroleum-based resins. Tall oil fatty acids (TOFA) closely follow, valued for versatility in alkyd resins, dimer acid production, lubricant esters, and corrosion inhibitors, reinforcing the shift toward bio-based industrial feedstocks. Distilled tall oil occupies a midstream position, supplying metalworking fluids, oilfield chemicals, and emulsifiers where moderate purity is sufficient. Tall oil pitch represents a significant residual stream used as a biofuel in pulp mills, asphalt modifier, and low-grade binder, reflecting full-value utilization of the crude tall oil chain. Tall oil heads, the light fraction, are primarily consumed as fuel or specialty solvents, contributing lower value but maintaining volume significance within integrated biorefinery operations.

Application Segmentation: Adhesives Anchor Demand as Biofuels and Coatings Drive Growth

Adhesives and sealants account for 28% of crude tall oil derivative consumption, leveraging tall oil rosin in hot-melt and pressure-sensitive systems aligned with growing bio-based content mandates. Biofuels represent one of the fastest-expanding segments, with distilled tall oil and pitch upgraded to renewable diesel and biodiesel under hydrotreating pathways supported by European and North American blending regulations. Paints and coatings utilize TOFA-derived alkyd resins and rosin esters in architectural enamels and printing inks, benefiting from green formulation trends. Bio-based chemicals form a strategic segment producing dimer acids, polyamide resins, and ester derivatives for specialty uses. Lubricants and metalworking fluids capitalize on biodegradable TOFA esters, particularly in environmentally sensitive forestry and marine settings. Construction materials incorporate tall oil pitch in asphalt modification, while oilfield chemicals use TOFA-based emulsifiers and corrosion inhibitors for offshore and environmentally regulated drilling operations.

Competitive Landscape of the Crude Tall Oil Derivative Market

The Crude Tall Oil Derivative Market is increasingly shaped by bio-based chemicals, advanced refining technologies, and sustainability-driven demand across adhesives, asphalt, lubricants, biofuels, and specialty surfactants, with leading players competing on feedstock security, vertical integration, and low-carbon innovation.

Kraton drives premium CTO derivatives with ISCC PLUS-certified pine chemistry

Kraton Corporation is the world’s largest producer of pine-based chemicals, holding a dominant position in refining crude tall oil into high-value specialty derivatives. Its SYLVATAL™ distilled tall oil and SYLVAROS™ tall oil rosin brands are industry benchmarks for adhesives, rubber compounding, and road construction. In early 2026, Kraton implemented a 10%+ global price increase across TOFA and CTO refinery products to offset logistics inflation and feedstock competition. The company also achieved ISCC PLUS certification at its Panama City facility, enabling mass-balance certified bio-based offerings. With a strategic focus on achieving a carbon-negative footprint and five EcoVadis Platinum awards, Kraton is aggressively targeting Europe’s growing “green premium” market.

Ingevity refocuses CTO refining toward asphalt, lubricants, and energy materials

Ingevity Corporation is a major global CTO refiner, specializing in performance chemicals for pavement, oilfield, and industrial applications. In late 2025 and early 2026, the company divested its non-core industrial specialties business for $110 million, sharpening its focus on high-growth segments such as lithium-ion battery materials and advanced bio-chemicals. Its Evotherm® warm-mix asphalt technology uses tall oil derivatives to enable lower-temperature paving, significantly reducing CO2 emissions. Ingevity’s Altapyne™ TOFA products are widely used in lubricants and metalworking fluids to enhance lubricity and corrosion resistance. Deep vertical integration in oilfield chemicals further strengthens its position in high-performance drilling emulsifiers.

UPM Biofuels transforms CTO into renewable diesel and next-generation bio-chemicals

UPM Biofuels has redefined CTO utilization by converting it directly into renewable diesel and bio-naphtha at its Lappeenranta Biorefinery, the world’s first facility dedicated to this pathway. Integrated within UPM’s pulp and paper ecosystem, the company benefits from a stable internal CTO supply, largely insulated from market price volatility. Strategically, UPM is expanding into bio-chemicals, positioning CTO derivatives as alternatives to fossil-based PET and mono-ethylene glycol. Recent validation of CTO-derived naphtha as a drop-in feedstock for sustainable plastics underscores its circular economy ambitions. This feedstock-to-fuel integration places UPM at the forefront of energy-focused CTO derivative innovation.

Forchem targets ultra-low sulfur TOFA for high-purity European applications

Forchem Oyj operates one of the world’s most modern CTO fractionation plants, emphasizing precision refining and niche purity grades. During 2025–2026, the company optimized fractionation processes to deliver ultra-low sulfur tall oil fatty acids aligned with evolving European marine fuel and lubricant standards. Forchem dominates the regional surfactant and soap markets, where its TOFA serves as a bio-based alternative to palm oil and tallow fatty acids. Its strategic focus on coatings and inks prioritizes color stability and low odor performance. Located at the Port of Rauma, Finland, Forchem benefits from direct access to Nordic CTO streams, reinforcing its competitiveness in specialty derivative markets.

SunPine scales tall oil diesel while unlocking pharmaceutical sterol value

SunPine AB represents the energy-driven evolution of CTO refining, producing renewable “Tall Diesel” fully compatible with existing engines. Its expanded Piteå facility now supplies over 100 million liters of tall oil-based green diesel annually to Sweden, contributing to an estimated 250,000 tonnes of CO2 reduction per year versus fossil fuels. Beyond fuels, SunPine has developed proprietary processes to extract tall oil sterols, increasingly used in pharmaceutical and food applications for cholesterol management. This dual focus on renewable energy and high-value bio-actives positions SunPine as a key innovator bridging CTO derivatives and sustainable mobility.

United States: Refining Rationalization and Biofuel-Led Demand Rebalancing

The United States crude tall oil derivatives market is undergoing a decisive structural reset driven by asset reallocation and policy-induced feedstock diversion. In September 2025, Ingevity Corporation announced the divestiture of its North Charleston, South Carolina CTO refinery alongside most of its Industrial Specialties portfolio for $110 million, with closure targeted for early 2026. This transaction signals a consolidation of domestic CTO refining capacity and a sharper focus on higher-margin specialties rather than capital-intensive fractionation. Parallel macro signals reinforced this shift. Data released by the U.S. Energy Information Administration showed a 17% drawdown in total distillate inventories during H1 2025, catalyzed by a 35% year-on-year decline in renewable diesel and biodiesel consumption. Producers responded by stabilizing supply through petroleum-based blends while reassessing CTO allocation across chemical versus fuel pathways.

Policy is set to reverse part of that trend. The proposed 2026 biodiesel mandate from the U.S. Environmental Protection Agency increases obligations by 56 %, an action expected to redirect more than 300,000 metric tons of CTO from traditional uses such as alkyd resins into biofuel streams. To preserve operational continuity amid these shifts, Kraton Corporation and International Paper executed a Strategic Continuity of Services Agreement in August 2025 to secure CTO fractionation at the Savannah, Georgia site. Innovation remains active in specialty niches. Late-2025 commercialization of Sylfat™ TOFA blends with enhanced oxidative stability expanded CTO-derived lubricants into EV thermal management and transmission fluids, while updated U.S. construction standards accelerated the use of tall oil rosin tackifiers in green building adhesives aligned with decarbonization goals.

Finland: Biorefinery Maturity and Export-Led Bioeconomy Scale

Finland continues to set the global benchmark for integrated CTO biorefining and export-oriented specialization. The Fintoil Hamina Biorefinery reached full capacity in 2025, processing more than 200,000 tons of crude tall oil annually while deploying low-carbon heat recovery systems that cut CO₂ emissions by roughly 80% versus conventional distillation. This operational maturity underpins Finland’s ability to defend CTO availability amid intensifying competition from pulp feedstocks. Downstream diversification is accelerating. UPM Biofuels marked the tenth anniversary of its Lappeenranta biorefinery in April 2025 by launching a collaboration with LUMENE, replacing fossil plastics with wood-based BioVerno naphtha in primary packaging.

Strategic focus has tightened. In May 2025, UPM discontinued plans for a second biorefinery in Rotterdam, reallocating capital toward expanding Lappeenranta and accelerating commercialization of CTO-derived Sustainable Aviation Fuel in 2026. Specialty additives are also scaling. Forchem Oyj introduced the ISCC PLUS-certified CirKular+™ line in late 2025, targeting plastics upcycling with 100% renewable CTO inputs. Anchoring these moves, Finland’s 2025–2030 Bioeconomy Strategy positions Tall Oil Fatty Acid as a priority renewable export, maintaining stable volumes despite rising internal competition for pine-based residues.

Sweden: Biomaterials Elevation and Forest Asset Optimization

Sweden’s CTO derivative strategy centers on value maximization through biomaterials leadership and supply chain integration. Effective January 1, 2026, Stora Enso will implement a revised reporting structure elevating Biomaterials to a core segment, following the strategic separation of Swedish forest assets. This reclassification reflects a deliberate pivot toward monetizing pine-based chemical precursors, including CTO derivatives, as long-cycle specialty materials rather than low-margin byproducts. Environmental performance metrics reinforce the value proposition. In 2025, Stora Enso reported that its renewable materials portfolio enabled customers to avoid approximately 14 million tonnes of CO₂e by substituting fossil-based inputs.

Supply chain efficiency is being sharpened in parallel. A strategic review concluded in November 2025 by Swedish authorities and Stora Enso streamlined central European sawmilling operations, creating a more integrated and cost-competitive model for crude tall oil collection across Nordic sites. The outcome strengthens feedstock security and lowers unit costs for CTO derivatives destined for adhesives, coatings, and renewable materials markets across Europe.

China: Import Substitution and Infrastructure-Led Absorption

China’s engagement with crude tall oil derivatives is increasingly policy-directed, emphasizing import substitution and infrastructure-scale absorption. Under the 2025–2026 Petrochemical Growth Plan, authorities prioritized domestic production of high-purity Tall Oil Rosin for paper sizing and rubber processing to reduce dependence on imported gum rosin. This specialization favors CTO-derived resins with consistent molecular profiles suitable for high-speed papermaking and tire compounding.

Infrastructure demand provides a secondary pull. In 2025, China led the Asia-Pacific region in adopting tall oil pitch as an asphalt emulsifier for Green Highway projects, leveraging sustainability mandates that reward renewable binders and improved pavement durability. This application channel supports steady absorption of heavier CTO fractions and embeds tall oil derivatives into long-life public assets.

Comparative Snapshot: Country-Level Strategic Positioning in Crude Tall Oil Derivatives

Crude Tall Oil Derivative Market County Level Snapshot

|

Country / Region

|

Strategic Driver

|

Priority Applications

|

Direction of CTO Utilization

|

|

United States

|

Asset divestiture and biofuel mandates

|

Biodiesel, EV lubricants, green adhesives

|

Reallocation from chemicals to fuels with specialty innovation

|

|

Finland

|

Biorefinery scale and exports

|

Bio-naphtha, SAF, plastics additives

|

High-efficiency refining and export leadership

|

|

Sweden

|

Biomaterials monetization

|

Renewable materials, adhesives

|

Value uplift via integrated forest assets

|

|

China

|

Import substitution and infrastructure

|

Paper sizing, rubber, green asphalt

|

Domestic TOR production and heavy-fraction absorption

|

Crude Tall Oil Derivative Market Report Scope

Crude Tall Oil Derivative Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.3 Billion

|

|

Market Size (2034)

|

$3.7 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Derivative Type (Tall Oil Fatty Acids, Tall Oil Rosin, Distilled Tall Oil, Tall Oil Pitch, Tall Oil Heads), By Application (Bio-Based Chemicals, Biofuels, Adhesives and Sealants, Paints and Coatings, Lubricants and Metalworking Fluids, Oilfield Chemicals, Construction Materials), By End-Use Industry (Automotive and Transportation, Building and Construction, Pulp and Paper, Pharmaceuticals and Personal Care, Oil and Gas, Packaging)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kraton Corporation, Ingevity Corporation, UPM-Kymmene Oyj, Stora Enso Oyj, Forchem Oyj, SunPine AB, Mercer International Inc., Harima Chemicals Group, Inc., Neste Oyj, Pine Chemical Group Oy, DRT, Eastman Chemical Company, Fintoil, Ilim Group JSC, Georgia-Pacific Chemicals LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Crude Tall Oil Derivative Market Segmentation

By Derivative Type

- Tall Oil Fatty Acids

- Tall Oil Rosin

- Distilled Tall Oil

- Tall Oil Pitch

- Tall Oil Heads

By Application

- Bio-Based Chemicals

- Biofuels

- Adhesives and Sealants

- Paints and Coatings

- Lubricants and Metalworking Fluids

- Oilfield Chemicals

- Construction Materials

By End-Use Industry

- Automotive and Transportation

- Building and Construction

- Pulp and Paper

- Pharmaceuticals and Personal Care

- Oil and Gas

- Packaging

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Crude Tall Oil Derivative Industry

- Kraton Corporation

- Ingevity Corporation

- UPM-Kymmene Oyj

- Stora Enso Oyj

- Forchem Oyj

- SunPine AB

- Mercer International Inc.

- Harima Chemicals Group, Inc.

- Neste Oyj

- Pine Chemical Group Oy

- DRT

- Eastman Chemical Company

- Fintoil

- Ilim Group JSC

- Georgia-Pacific Chemicals LLC

*- List not Exhaustive