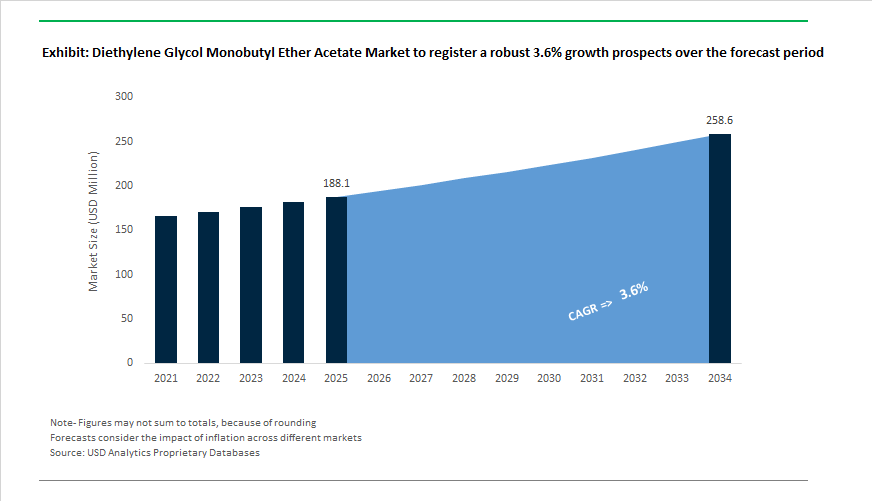

Diethylene Glycol Monobutyl Ether Acetate Market to Reach $258.6 Million by 2034 at 3.6% CAGR Amid Capacity Rationalization and Regulatory-Driven Reformulation

The Diethylene Glycol Monobutyl Ether Acetate (DBA) Market is projected to grow from $188.1 Million in 2025 to $258.6 Million by 2034, reflecting a CAGR of 3.6%. DBA, widely used as a high-boiling solvent and retarder in architectural coatings, industrial inks, electronics cleaning fluids, and specialty process applications, is navigating a period of strategic rationalization and regulatory realignment. The 2024–2026 period marks a structural transition, characterized by selective production exits, feedstock volatility in the ethylene oxide and acetic acid chains, and growing demand for electronic-grade and low-VOC formulations.

In 2024, Eastman Chemical reinforced the positioning of DB Acetate as a Low Vapor Pressure VOC coalescent for latex paints, emphasizing high blush resistance and slow evaporation to comply with tightening environmental standards in low-pH architectural coatings. A parallel shift emerged in electronics manufacturing, where demand increased for high-resistance DBA grades suitable for dielectric-sensitive electronic coatings and precision distillation processes. This specialty demand trend accelerated through 2024, signaling a move toward value-added solvent differentiation rather than pure volume growth.

Pricing and supply adjustments intensified across 2025 and early 2026. Dow Chemical implemented a $0.05 per pound increase for its glycol ether portfolio in North America in January 2025, citing rising energy indices and cost support from upstream ethylene oxide production. During May 2025, printing ink manufacturers highlighted DBA’s adoption in sustainable screen-printing inks, leveraging its slow volatilization and low water solubility for stable high-temperature industrial printing. Dow and its Sadara joint venture optimized esterification operations in Jubail during 2025, enhancing performance glycol ester output to meet demand in the Middle East and Asia-Pacific. However, structural capacity adjustments followed. KH Neochem announced in December 2025 the permanent halt of DBA production at its Yokkaichi plant, citing weak demand recovery and rising manufacturing costs. This decision reflects broader solvent rationalization trends. LyondellBasell raised its cost improvement target to $1.3 billion by year-end 2026, initiating reviews of intermediates and derivatives portfolios that could further reduce exposure to lower-margin solvent lines.

Regulatory changes have significantly reshaped production methodologies and regional trade flows. The EU transition period for tin-based catalysts ended on January 31, 2026, compelling European producers to pivot toward tin-free esterification routes to comply with updated REACH and British Coatings Federation safety requirements. Reliance Industries implemented pricing revisions in January 2026 in India to offset acetic acid feedstock volatility, reinforcing India’s growing role as a demand center for oxygenated solvents. BASF accelerated development of its Zhanjiang Verbund site during 2025–2026, strengthening regional supply of intermediates required for advanced glycol ether esters in automotive coatings. Tokyo Chemical Industry expanded dispatch capabilities from Hyderabad in 2025, enabling same-day shipment of >98.0% purity DBA for pharmaceutical and electronics R&D applications. These developments illustrate a bifurcated market structure: rationalized commodity capacity in mature regions alongside high-purity and application-specific growth corridors in Asia-Pacific and emerging industrial hubs.

Trends and Opportunities Shaping the Diethylene Glycol Monobutyl Ether Acetate (DGBEA) Market

Regulatory Phase-Out Accelerates Exit from Consumer and DIY Coatings

- The regulatory reclassification of DGBEA as a Category 1B reprotoxic substance has become the most decisive force shaping market demand. With the European Chemicals Agency expanding the SVHC Candidate List to 251 substances as of November 2025, compliance obligations under REACH Article 33 have materially altered formulation economics. Any article containing more than 0.1% DGBEA by weight now requires mandatory disclosure within 45 days of a consumer request, significantly increasing reputational and compliance risks for brand owners.

- This has triggered a rapid withdrawal of DGBEA from architectural, decorative, and do-it-yourself paint formulations. Regulatory tracking and industry disclosures from mid-2025 indicate that more than 60% of European paint manufacturers have already reformulated away from DGBEA to retain EU Ecolabel eligibility, which explicitly excludes SVHC-listed solvents. As a result, DGBEA demand in consumer coatings is witnessing substitution toward lower-toxicity glycol ethers, ester-alcohol blends, and fully waterborne systems becoming the default pathway.

Consolidation in High-Solids Automotive and Aerospace Coatings

- In contrast to consumer markets, DGBEA remains a performance-critical solvent in specific industrial coatings where defect tolerance is near zero. High-solids automotive refinish coatings, which are gaining share in a global refinish market valued at approximately USD 13.2 billion in 2025, rely on DGBEA as a tail solvent to manage flow, leveling, and film formation. Its high boiling point enables controlled evaporation, preventing solvent pop, blistering, and cratering in thick clearcoat systems increasingly specified for electric vehicles and premium finishes.

- The aerospace sector reinforces this niche demand. As aircraft production and maintenance cycles normalize toward pre-pandemic volumes by late 2025, specialty epoxy primers and topcoats continue to depend on DGBEA to maintain gloss, flow, and uniform film build under variable hangar temperatures. In these applications, regulatory exposure is mitigated by closed industrial use, trained handling protocols, and low-volume, high-value consumption patterns, allowing DGBEA to retain relevance despite broader market contraction.

Tail Solvent and Flow Modifier in Vat Photopolymerization 3D Printing

- One of the most promising growth avenues for DGBEA lies in advanced 3D printing technologies, particularly vat photopolymerization processes such as SLA and DLP. As high-resolution printing expands into dental, medical, and aerospace components, resin viscosity control and dimensional accuracy have become critical bottlenecks. Research published in August 2025 highlights solvent selection as the dominant factor influencing volumetric shrinkage, with volatile solvents causing dimensional losses of up to 30%.

- DGBEA is being evaluated as a modified glycol solvent capable of reducing epoxy acrylate resin viscosity without inducing excessive shrinkage. Its balanced evaporation profile improves layer-to-layer adhesion and mitigates delamination in complex geometries. These attributes are particularly relevant for medical-grade printed parts undergoing regulatory review in 2025, positioning DGBEA as a functional enabler in a high-margin, low-volume segment rather than a bulk solvent.

Precision Carrier for PFPE and Semiconductor Lubrication Systems

- The push toward smaller semiconductor nodes and cleaner manufacturing environments is creating another specialized outlet for DGBEA. In the formulation and application of perfluoropolyether lubricants used in vacuum pumps, wafer-handling systems, and lithium-ion battery manufacturing equipment, carrier solvents must evaporate completely without leaving residues. DGBEA’s clean evaporation profile allows lubricant OEMs to meet stringent ASTM E595 outgassing limits, including total mass loss below 1%.

- This zero-deposit behavior is critical in semiconductor fabs and aerospace systems, where even trace carbonaceous residues can cause stiction, bearing failure, or electrical shorting. With global semiconductor equipment spending projected to increase again in 2025, demand for precision-applied, contamination-free lubrication is rising. Within this context, DGBEA functions as a high-value processing aid, supporting a narrow but defensible demand stream aligned with advanced manufacturing and electronics reliability requirements.

Diethylene Glycol Monobutyl Ether Acetate (DGBA) Market Share Anlaysis

Market Share by Application: Coalescing Aids and Coatings Drive Core Demand

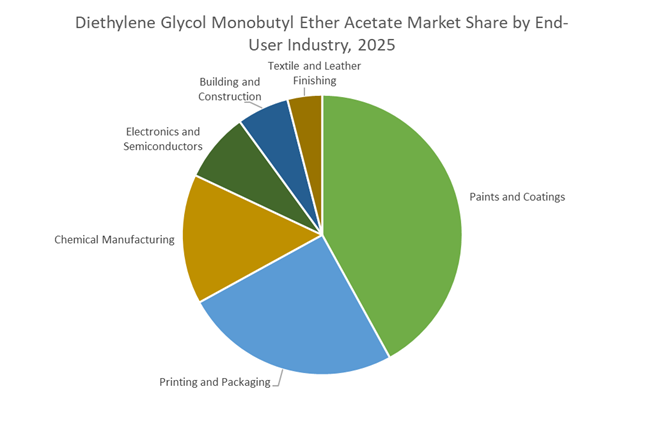

Coalescing aids account for 35% of DGBA market demand in 2025, positioning diethylene glycol monobutyl ether acetate as a critical performance additive in low-VOC, waterborne coatings. DGBA’s high boiling point and strong solvency enable effective latex film formation in architectural and industrial paints, supporting smooth finishes and defect-free curing. Printing inks represent a significant secondary segment, particularly in gravure and screen printing, where DGBA’s slow evaporation improves flow, leveling, and color consistency. Process solvents and retarder solvents support chemical synthesis and high-build coatings by minimizing blushing and solvent popping. Specialty cleaning agents use DGBA for precision removal of oils, greases, and flux residues, while chemical intermediates remain a smaller niche. From an end-user perspective, paints and coatings dominate with 42% share, followed by printing and packaging, chemical manufacturing, and rapidly growing electronics and semiconductor cleaning. Building and construction, plus textile and leather finishing, further reinforce DGBA’s role across advanced coating additives, specialty solvents, and high-purity cleaning formulations.

Market Share by End-Use Industry: Solvent Performance Anchors Growth Across Coatings and Cleaning

Solvents lead the global DGBA market with 42% share, driven by diethylene glycol monobutyl ether’s ability to dissolve resins, polymers, and oils while providing extended open time through slow evaporation. Coalescing agents form the second-largest segment, supporting ambient film formation in low-VOC architectural paints and industrial coatings. Cleaning and detergents represent a major demand pillar, using DGBA in hard-surface cleaners, industrial degreasers, and textile processing where deep penetration and water compatibility are essential. Chemical intermediates and formulation additives remain smaller but strategic applications. By end-use, paints and coatings account for about 40% of consumption, followed by printing, packaging and inks, and cleaning products. Electronics and semiconductors are a fast-growing high-purity segment, while automotive, agrochemicals, pharmaceuticals, cosmetics, and oilfield chemicals provide diversified downstream demand. Together, these sectors position DGBA as a cornerstone glycol ether solvent for coatings performance, industrial cleaning, and specialty chemical manufacturing.

Competitive Landscape of the Diethylene Glycol Monobutyl Ether Acetate (DGBEA) Market

The Diethylene Glycol Monobutyl Ether Acetate market is shaped by vertically integrated chemical majors and specialty solvent leaders, with competitiveness in 2026 driven by LVP-VOC compliance, waterborne coatings adoption, electronics cleaning demand, and secure ethylene oxide supply chains across North America, Europe, and Asia-Pacific.

Eastman Chemical leads premium DGBEA solvents for automotive and coil coatings

Eastman Chemical Company is a clear market leader in high-performance DGBEA solvents, positioning Eastman™ DB Acetate as a low-volatility, slow-evaporation solution for demanding industrial coatings. The product dominates Auto OEM and coil coatings, where it functions as a retarder solvent and coalescing aid to deliver smooth, high-gloss finishes with strong electrical resistance. Eastman’s 2026 strategy centers on LVP-VOC compliance, aggressively promoting DGBEA under California ARB regulations for both consumer and industrial formulations. Recent innovation includes specialized urethane-grade solvents with ultra-low moisture content, preventing side reactions in polyurethane systems and reinforcing Eastman’s leadership in premium glycol ether acetate applications.

Dow Inc. drives volume leadership through vertically integrated E-Series glycol ethers

Dow Inc. leverages its massive E-Series glycol ether platform to supply DGBEA at scale, supported by deep backward integration into ethylene oxide and butanol. This insulation from 2024–2025 supply shocks has enabled Dow to lead North American DGBEA sales by volume in 2026, particularly through long-term contracts with architectural paint manufacturers. Dow’s DGBEA is a critical coalescent in waterborne coatings, enabling durable film formation at low temperatures. In early 2026, the company introduced digitalized supply-chain tools allowing customers to track real-time CO2e footprints, aligning solvent procurement with sustainability goals while reinforcing Dow’s strength in high-volume, water-based resin systems.

BASF strengthens Europe’s DGBEA supply with REACH-compliant and bio-based innovation

BASF SE anchors the European market with its Butyl Diglycol Acetate (BDGA), prized for broad resin compatibility across acrylics, epoxies, and PVC plastisols. BASF’s DGBEA portfolio meets stringent REACH environmental standards, making it a preferred solvent for electronics cleaning and sensitive industrial coatings. In 2026, BASF began piloting bio-based and circular-carbon feedstocks to develop a greener BDGA variant targeting eco-conscious consumer cleaning applications. The company also expanded specialty solvent distribution in China and India to capture the region’s 7.2% CAGR in automotive electronics, reinforcing BASF’s position in high-purity flux removal and advanced surface-cleaning formulations.

LyondellBasell targets inks and toners with consistency-driven glycol ether acetates

LyondellBasell Industries is a key supplier to the global printing ink and toner industry, where its Glycol Ether DB Acetate is valued for mild odor, partial water solubility, and viscosity stabilization. The product acts as a coupling agent in complex aqueous and non-aqueous systems, making it essential for silk-screen inks and ballpoint pen pastes. In 2026, LyondellBasell emphasized operational resilience, optimizing European assets toward high-margin glycol ether esters amid energy volatility. Strategic ethylene supply agreements keep its Oyster Creek and Rotterdam sites operating at peak capacity, ensuring reliable DGBEA availability for specialty ink and graphic applications worldwide.

SABIC accelerates Asian DGBEA growth through mega-scale petrochemical investments

SABIC is rapidly expanding its footprint in glycol intermediates, supported by the launch of its $6.4 billion Fujian petrochemical complex in China in early 2026, significantly increasing regional ethylene glycol derivative capacity. SABIC’s “Chemistry that Matters™” strategy prioritizes decarbonized ethylene oxide production via partnerships with Scientific Design and Linde, targeting a 30% emissions reduction by 2030. With brand value reaching $4.7 billion in 2026, SABIC benefits from proximity to Asia’s manufacturing hubs, enabling cost-efficient DGBEA exports to Japanese and South Korean electronics markets while transitioning from commodity supply to specialty solvent solutions.

United States: Cost Inflation Management and Regulatory-Driven Solvent Substitution

The U.S. diethylene glycol monobutyl ether acetate market in 2025 has been shaped by a combination of price recalibration, regulatory tailwinds, and short-term feedstock disruptions. Effective March 15, 2025, integrated producers including Dow implemented price increases of roughly $0.04 per pound across glycol ether portfolios. This adjustment reflected persistent volatility in ethylene oxide feedstocks and higher operating costs associated with energy, logistics, and compliance. The pricing action was broadly absorbed by downstream coatings and industrial formulators, indicating DBEA’s entrenched role as a performance-critical solvent rather than a discretionary additive.

Regulation has further reinforced DBEA’s positioning. Under reinforced Clean Air Act guidance in 2025, the U.S. Environmental Protection Agency continued to push LVP-VOC formulations, favoring solvents with low vapor pressure and stable evaporation profiles. DBEA has emerged as a preferred coalescent in low-pH latex paints and high-bake enamels, particularly where film formation and flow must be balanced against emission constraints. Supply-side resilience was tested in February 2025 when an Arctic blast caused freeze-offs across the Gulf Coast, temporarily curtailing ethylene oxide output and tightening spot availability. This disruption accelerated sourcing shifts toward domestic, integrated suppliers such as Eastman and Dow, a trend reinforced by February 2025 trade measures that raised tariffs on select imported intermediates. Eastman’s 2025 expansion of its Solvents for Coatings portfolio further highlighted DBEA’s value in automotive OEM electrostatic spray systems, where blush resistance and electrical insulation are critical performance attributes.

China: Capacity Scale-Up and Export Price Discipline

China’s DBEA market reflects a classic scale-versus-balance dynamic, with aggressive capacity additions now intersecting with export price recalibration. A pivotal development was BASF’s 200,000-ton-per-year glycol ether facility at its Nanjing Verbund site, inaugurated in April 2024 and fully optimized by 2025. This plant is strategically oriented toward high-purity DBEA grades for electronics, inks, and advanced coatings, reinforcing China’s ambition to internalize specialty solvent supply within integrated petrochemical ecosystems.

Parallel investments continue to reshape the downstream landscape. SABIC’s $6.5 billion Fujian petrochemical complex has progressed into the integration phase, enabling captive ethylene glycol and ether derivative streams to serve China’s large textile finishing and printing ink sectors. Under the national AI + Petrochemicals initiative, DBEA has gained traction as a precision solvent in photoresist stripping and screen-printing inks for advanced semiconductor packaging. However, late-2025 inventory build-ups prompted Chinese exporters to lower offers to around $1,350 per metric ton to defend market share in Southeast Asia and India. This disciplined pricing underscores China’s dual strategy of capacity leadership while maintaining export competitiveness amid regional oversupply.

India: Import Substitution and Infrastructure-Led Demand

India’s DBEA market is increasingly defined by self-reliance policies and structurally resilient domestic demand. In 2025, the Department of Pharmaceuticals confirmed that the Production Linked Incentive scheme had successfully localized several solvent-grade glycol ethers, reducing dependence on Chinese imports for pharmaceutical extraction and formulation processes. This localization has improved supply security for high-specification solvents used in APIs and specialty formulations, where DBEA’s solvency and evaporation control are valued.

Demand momentum has been reinforced by public infrastructure spending. The 2025–2026 Union Budget’s increased allocations for smart cities and urban renewal have driven consumption of heavy-duty protective coatings and coil coatings, segments where DBEA functions as a retarder solvent to ensure uniform film build and surface finish. Pricing dynamics reflect this balance. By September 2025, Indian DBEA prices stabilized near $1,196 per metric ton, supported by consistent offtake from printing inks and aerosol applications despite a softer industrial recovery in parts of the Asia-Pacific region. This stability highlights India’s transition from a price-taker market toward one anchored by domestic demand fundamentals.

Saudi Arabia: Low-Carbon Differentiation and Automotive Finishes

Saudi Arabia’s DBEA strategy centers on downstream diversification and carbon intensity reduction rather than pure volume expansion. Following the SABIC–Scientific Design memorandum of understanding signed in early 2024 and operationalized through 2025, the Kingdom has accelerated decarbonization of its ethylene oxide and glycol value chain. The objective is to supply low-carbon DBEA grades that align with the sustainability criteria increasingly imposed by European coatings and automotive customers.

This strategy is operationalized through the Sadara Chemical Company, which optimized its E-series glycol ether production during 2025 to boost output of high-boiling ester solvents. These grades are specifically targeted at high-bake automotive finishes, where thermal stability and controlled evaporation are essential. Saudi Arabia’s competitive advantage lies in its ability to combine feedstock integration, scale, and emerging low-carbon credentials, positioning DBEA as a differentiated export rather than a commodity solvent.

Germany and the European Union: Compliance-Driven Premiumization

Within Europe, and particularly Germany, the DBEA market is shaped by regulatory stringency, energy cost pressures, and compliance-driven solvent substitution. In May 2025, BASF expanded its portfolio of construction chemical raw materials, primarily focused on polyethylene glycols but sharing upstream integration with glycol ether acetate chains. This integration enhances regional supply security for DBEA amid broader European feedstock constraints.

Regulatory pressure is intensifying. Effective January 2026, the European Chemicals Agency introduced stricter workplace exposure limits for glycol ethers, encouraging formulators to shift toward lower-volatility options such as DBEA. While this regulatory environment supports DBEA demand, it also contributes to higher costs. By September 2025, German market prices reached approximately $1,477 per metric ton, the highest globally, reflecting elevated energy prices and cumulative environmental compliance fees. The result is a structurally premium market where DBEA adoption is driven as much by regulatory necessity as by performance advantages.

Comparative Snapshot: Diethylene Glycol Monobutyl Ether Acetate Market by Region

Diethylene Glycol Monobutyl Ether Acetate Market Country Level Snapshot

|

Region

|

Primary Market Driver

|

Strategic Focus

|

Structural Outcome

|

|

United States

|

LVP-VOC regulations and cost pass-through

|

Domestic sourcing, OEM coatings

|

Stable demand with integrated supply preference

|

|

China

|

Capacity expansion and export balance

|

High-purity grades, price discipline

|

Scale leadership with competitive export pricing

|

|

India

|

Import substitution and infrastructure spend

|

Pharma solvents, protective coatings

|

Demand stability and reduced import exposure

|

|

Saudi Arabia

|

Decarbonization and downstream diversification

|

Low-carbon DBEA, automotive finishes

|

Differentiated export positioning

|

|

Germany / EU

|

REACH compliance and energy costs

|

Low-volatility solvent substitution

|

Premium pricing and compliance-led demand

|

Diethylene Glycol Monobutyl Ether Acetate Market Report Scope

Diethylene Glycol Monobutyl Ether Acetate Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$188.1 Million

|

|

Market Size (2034)

|

$258.6 Million

|

|

Market Growth Rate

|

3.6%

|

|

Segments

|

By Grade (Industrial Grade, High Purity Grade, Low-VOC Grade), By Application (Coalescing Aids, Retarder Solvents, Printing Inks, Process Solvents, Specialty Cleaning Agents, Chemical Intermediates), By End-User Industry (Paints and Coatings, Printing and Packaging, Electronics and Semiconductors, Chemical Manufacturing, Building and Construction, Textile and Leather Finishing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Inc., Eastman Chemical Company, BASF SE, SABIC, LyondellBasell Industries N.V., Huntsman Corporation, Shell Chemicals, INEOS Oxide, Nippon Shokubai Co., Ltd., Jiangsu Yida Chemical Co., Ltd., Shiny Chemical Industrial Co., Ltd., Indorama Ventures Public Company Limited, Balaji Amines Limited, Tokyo Chemical Industry Co., Ltd., China Petroleum & Chemical Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Diethylene Glycol Monobutyl Ether Acetate Market Segmentation

By Grade

- Industrial Grade

- High Purity Grade

- Low-VOC Grade

By Application

- Coalescing Aids

- Retarder Solvents

- Printing Inks

- Process Solvents

- Specialty Cleaning Agents

- Chemical Intermediates

By End-User Industry

- Paints and Coatings

- Printing and Packaging

- Electronics and Semiconductors

- Chemical Manufacturing

- Building and Construction

- Textile and Leather Finishing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Diethylene Glycol Monobutyl Ether Acetate Industry

- Dow Inc.

- Eastman Chemical Company

- BASF SE

- SABIC

- LyondellBasell Industries N.V.

- Huntsman Corporation

- Shell Chemicals

- INEOS Oxide

- Nippon Shokubai Co., Ltd.

- Jiangsu Yida Chemical Co., Ltd.

- Shiny Chemical Industrial Co., Ltd.

- Indorama Ventures Public Company Limited

- Balaji Amines Limited

- Tokyo Chemical Industry Co., Ltd.

- China Petroleum & Chemical Corporation

*- List not Exhaustive