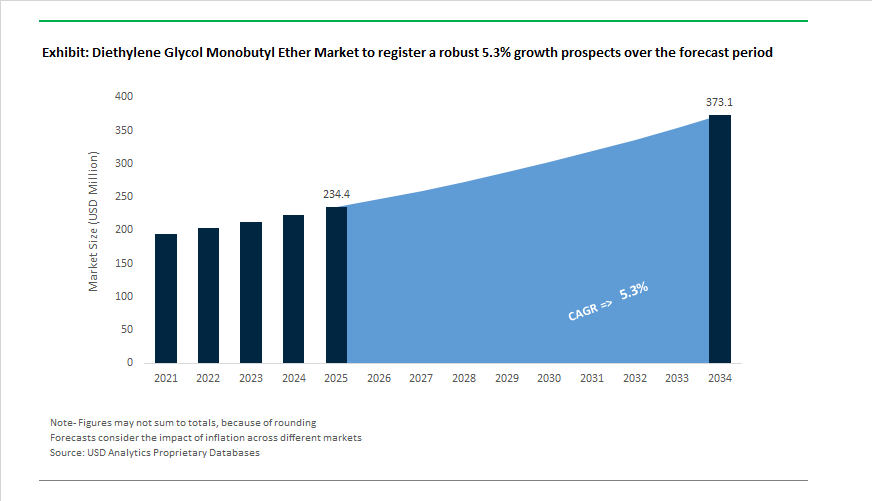

Diethylene Glycol Monobutyl Ether Market to Reach $373.1 Million by 2034 at 5.3% CAGR Amid Capacity Rationalization and High-Purity Demand Shift

The Diethylene Glycol Monobutyl Ether (DEGBE) Market is projected to expand from $234.4 Million in 2025 to $373.1 Million by 2034, registering a CAGR of 5.3%. DEGBE remains a critical high-boiling glycol ether solvent used in automotive OEM coatings, industrial cleaners, electronics processing fluids, and specialty formulations requiring controlled evaporation and strong solvency power. The 2024–2026 cycle reflects a structural transition in the glycol ether value chain, shaped by European capacity rationalization, feedstock integration strategies in North America, and Asia’s expanding export dominance.

In July 2024, BASF secured ISCC PLUS certification across its global alcohols, glycol ethers, and acetate production sites, enabling the commercialization of Low-PCF and Ccycled® DEGBE variants. This certification directly supports automotive and industrial coating formulators seeking mass-balance renewable content and chemically recycled feedstock solutions. Through 2024 and 2025, the market simultaneously shifted toward Ultra-High Purity (>99.5%) DEGBE grades, driven by semiconductor manufacturing and 5G-compatible electronic substrate production. Electronic-grade specifications demand extremely low moisture and impurity profiles, positioning DEGBE as a specialty solvent rather than a bulk industrial intermediate in advanced electronics applications.

Feedstock security and pricing dynamics intensified in 2025. Dow announced a $0.05 per pound price increase for its glycol portfolio in August 2025, citing petrochemical feedstock volatility and operating cost pressure. In October 2025, Dow and MEGlobal expanded their ethylene supply agreement by an additional 100 KTA from Gulf Coast operations, strengthening integration at Oyster Creek and ensuring long-term stability for ethylene glycol and downstream ether derivatives. Adoption of DEGBE accelerated in 2025 within high-solid, low-VOC automotive OEM coatings. Major coatings manufacturers leveraged its slow evaporation profile to maintain wet-edge stability in robotic paint lines operating with reduced solvent volumes, aligning with global VOC reduction mandates.

Structural rationalization defined late 2025 and early 2026. KH Neochem confirmed in December 2025 the permanent shutdown of DEGBE production at its Yokkaichi plant, citing sluggish demand recovery and elevated fixed costs. Dow approved a restructuring of European upstream assets in June 2025, targeting EBITDA uplift beginning mid-2026. LyondellBasell reported a $738 million net loss for 2025 in January 2026, attributing margins that were 45% below historical averages, yet signaling optimism for 2026 as capacity rationalizations rebalance supply. Trade data released in January 2026 confirmed India’s emergence as the dominant supplier of glycol ethers to the European Union, accounting for over 65% of EU imports in 2024, reflecting Europe’s manufacturing contraction and Asia’s competitive cost structure. BASF announced the opening of a Global Digital Hub in Hyderabad in Q1 2026, integrating AI and digital twin modeling to accelerate customized solvent formulation development. In February 2026, Silox India secured ₹300–360 crore for expansion in Dahej, strengthening high-purity solvent output for pharmaceutical-grade processing and export markets. These developments indicate a market increasingly polarized between rationalized Western commodity capacity and high-specification growth corridors in Asia-Pacific and electronics-driven segments.

Trends and Opportunities Transforming the Diethylene Glycol Monobutyl Ether (DGBE) Market

Regulatory Phase-Out Accelerates Reformulation in Consumer and Architectural Products

- Regulatory pressure across the European Economic Area has triggered a structural decline in DGBE usage within consumer-facing applications. Following the European Chemicals Agency’s expansion of the REACH Candidate List to 251 substances by November 2025, DGBE has become a focal point under the EU Chemicals Strategy for Sustainability. Mandatory disclosure of concentrations exceeding 0.1% by weight in the SCIP database has increased compliance costs and reputational risk for brand owners, particularly in decorative paints, wood stains, and household cleaners.

- As a result, architectural coating manufacturers are rapidly transitioning toward Ecolabel-compliant solvent systems. Industry disclosures from 2024 and 2025 indicate widespread substitution of DGBE with propylene glycol ethers and alternative low-toxicity coalescents to maintain uniform global formulations. Toxicological assessments from Health Canada during 2024–2025, highlighting severe eye irritation and potential sensitization risks in undiluted form, have further reinforced preemptive reformulation strategies. This trend signals that DGBE demand in consumer markets is not cyclical but structurally contracting, with limited prospects for recovery.

Entrenchment in High-Performance Industrial Polyurethane Dispersions and Inks

- While consumer usage declines, DGBE remains deeply embedded in professional and industrial formulations where its solvency profile is difficult to replicate. In the solvent polyurethane dispersions segment, valued at approximately USD 1.56 billion in 2025, DGBE functions as a critical coalescing aid that enables uniform film formation in waterborne systems. Its high boiling point and strong coupling efficiency support durable automotive and metal coatings designed for high abrasion and chemical exposure, aligning with annual global vehicle production approaching 100 million units by late 2025.

- Beyond coatings, DGBE plays a vital role in industrial inkjet printing and textile dyeing. Technical data from 2025 supplier dossiers confirms that DGBE ensures controlled wetting and penetration in high-speed digital textile lines without bleeding or feathering. This performance attribute is particularly relevant in Asia-Pacific manufacturing hubs, where automated textile printing capacity is expanding to meet fast-fashion and customized apparel demand. In these applications, DGBE’s value proposition is anchored in process reliability rather than volume consumption.

Aqueous Photoresist Strippers and Post-Etch Cleaning in Semiconductor Fabrication

- One of the most attractive growth avenues for DGBE lies in advanced semiconductor manufacturing. As chipmakers transition toward sub-5 nanometer nodes, there is a clear shift toward aqueous-based photoresist strippers that minimize damage to fragile low-k dielectrics. By the end of 2024, aqueous systems accounted for an estimated 45% of the global photoresist stripper market, and this share continues to rise in 2025.

- DGBE is a key functional component in these formulations due to its ability to swell and penetrate cross-linked photoresist layers following high-dose ion implantation. With more than USD 200 billion in new fabrication investments underway globally under initiatives such as the U.S. CHIPS Act and parallel programs in Europe and South Korea, demand for post-etch residue removal chemistries is intensifying. In this context, ultra-high-purity DGBE supports yield optimization in AI and 5G chip production, positioning it as a high-margin specialty solvent rather than a commodity chemical.

Fire-Resistant Hydraulic Fluids for Mining, Steel, and Aviation Systems

- Fire-resistant hydraulic fluids represent another structurally resilient opportunity for DGBE. HFC water-glycol fluids account for roughly 30% of the USD 1.56 billion global fire-resistant fluids market in 2025, with strong uptake in steel mills, mining operations, and aviation ground support equipment. In these systems, DGBE functions as a coupling agent that stabilizes additive packages, preventing phase separation under extreme thermal stress.

- The aerospace and marine sectors are increasingly specifying HFC fluids to meet stringent fire safety and operational reliability standards. DGBE’s ability to act as both a viscosity index improver and solubilizing agent ensures consistent performance across wide temperature ranges, including offshore wind platforms and airport ground operations. This positions DGBE as a safety-critical formulation component in regulated industrial environments where substitution risks are carefully evaluated.

Market Share Analysis of the Diethylene Glycol Monobutyl Ether (DGBE) Market

Market Share by Application: Solvents Lead DGBE Consumption While Coalescing Agents Accelerate Low-VOC Coatings Adoption

In 2025, the Diethylene Glycol Monobutyl Ether (DGBE) market by application is led by solvents, accounting for 42% market share, driven by DGBE’s exceptional ability to dissolve oils, resins, and polymers. Its high boiling point and slow evaporation profile support extended open time and controlled drying, making it indispensable in specialty formulations. Coalescing agents represent the second-largest segment, where DGBE enables film formation in waterborne coatings and adhesives by temporarily plasticizing latex particles, supporting the global shift toward low-VOC architectural and industrial coatings. Cleaning and detergents form a strong mid-tier segment, leveraging DGBE’s low surface tension for industrial degreasers, hard-surface cleaners, and textile scouring. Chemical intermediates remain niche, supplying esters and derivatives for pharmaceuticals and agrochemicals, while additives play a minor but strategic role as coupling, leveling, and wetting agents. Growing demand for sustainable solvents and high-performance water-based formulations continues to reinforce DGBE’s market relevance.

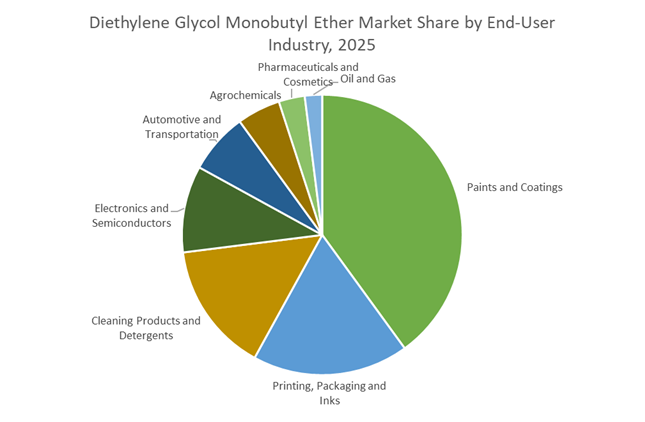

Market Share by End-User Industry: Paints and Coatings Dominate While Electronics Drive High-Purity DGBE Demand

The DGBE market by end-user industry is dominated by paints and coatings with 40% share, supported by rising consumption in waterborne architectural paints, industrial coatings, and specialty finishes as manufacturers prioritize low-VOC compliance and coating performance. Printing, packaging, and inks follow closely, using DGBE in gravure, flexographic, and screen printing to maintain viscosity stability, prevent nozzle clogging, and enhance flow and leveling. Cleaning products and detergents represent a substantial segment, integrating DGBE into household and industrial cleaners for effective grease and soil removal. Electronics and semiconductors are a fast-growing high-value segment, relying on ultra-pure DGBE for circuit board cleaning and photoresist formulations. Automotive and transportation applications include coatings and component cleaning, while agrochemicals, pharmaceuticals and cosmetics, and oil and gas remain smaller niches, serving specialized solvent and formulation needs in regulated and performance-driven environments.

Competitive Landscape of the Diethylene Glycol Monobutyl Ether (DGBE) Market

The Diethylene Glycol Monobutyl Ether (DGBE) market in 2026 is defined by vertically integrated petrochemical majors and specialty solvent leaders competing on LVP-VOC compliance, ethylene oxide integration, sustainable solvent technologies, and high-margin applications across coatings, electronics, pharmaceuticals, inks, and industrial cleaning.

Dow Inc. dominates global DGBE capacity with LVP-VOC smart solvent leadership

Dow Inc. is the undisputed global leader in Diethylene Glycol Monobutyl Ether, holding over 25% of total glycol ether capacity, reinforced by its 50% stake in the Sadara joint venture. Its flagship BUTYL CARBITOL™ Solvent delivers superior coalescing and coupling for water-reducible coatings. In early 2026, Dow prioritized Asset Discipline, shifting toward high-margin pharmaceutical and electronics grades following a $0.05/lb price hike in 2025. Deep vertical integration via its ethylene oxide network and Sadara’s cost-advantaged Saudi hub secures APAC and MEA supply. Dow’s core edge lies in LVP-VOC engineered DGBE, enabling customers to meet California ARB and U.S. EPA solvent regulations.

BASF SE strengthens Europe and South Asia with near-zero SVOC solvent innovation

BASF SE anchors the European DGBE market through its Verbund manufacturing model, delivering cost-efficient and sustainable glycol ether solutions. In February 2026, BASF commissioned a new dispersions line in Mangalore, India, producing advanced low-VOC solvents and binders for South Asian architectural coatings. Its 2026 Near-Zero SVOC initiative targets healthier indoor environments by reducing semi-volatile organic compounds in interior paints. BASF also opened a Digital Hub in Hyderabad to deploy AI for solvent logistics optimization and carbon footprint reduction. The company remains a leading supplier to printing inks and textile dyeing, where DGBE stabilizes drying profiles and ensures color consistency.

SABIC accelerates Asian DGBE supply through mega-scale petrochemical expansion

SABIC has rapidly evolved into a global DGBE force, supported by the startup of its $6.5 billion Fujian petrochemical complex in China in early 2026, sharply increasing regional ethylene glycol derivative capacity. SABIC’s Diethylene Glycol Technical Grade is prized for extreme hygroscopicity and low vapor loss, making it ideal for high-spec industrial brake fluids. A 2026 MoU with Scientific Design and Linde advances carbon-capture integration across ethylene oxide assets, reinforcing SABIC’s decarbonization roadmap. With unmatched proximity to feedstocks, SABIC executes a cost-leadership strategy in merchant DGBE while expanding exports across Asia-Pacific electronics and industrial fluid markets.

Eastman Chemical advances premium DGBE additives for architectural and textile finishes

Eastman Chemical Company positions DGBE as a premium retarder solvent for architectural and coil coatings, enhancing flow, leveling, and surface aesthetics. In February 2026, Eastman implemented an off-list price increase for glycol ethers, citing strong demand from building, construction, and consumables sectors. Its high-purity DB Solvent is widely adopted in high-end industrial finishes, while Eastman’s Naia™ technology platforms now incorporate DGBE-derived additives that improve cellulose fiber tenacity in textiles. The company leads in Sustainability Transparency, offering Environmental Product Declarations (EPDs) that help customers achieve GreenGuard certifications and comply with tightening indoor air quality standards.

LyondellBasell optimizes DGBE production for cleaning agents and industrial solvents

LyondellBasell Industries plays a pivotal role in North America and Europe, with strong penetration in cleaning agents, a segment projected to exceed $165 million by 2030. Its DGBE is valued for dissolving oils and greasy soils, making it essential in industrial cleaners, PVC stabilizers, and metal detergents. In early 2026, LyondellBasell launched a Cash Improvement Plan, prioritizing high-efficiency solvent lines over commodity intermediates to boost profitability. Backed by Texas refinery integration and proprietary Oxyfuels technology, the company dynamically balances antifreeze and solvent production, ensuring flexible DGBE output aligned with real-time market demand.

United States: Price Leadership Anchored in Feedstock Security and Low-VOC Incentives

The U.S. diethylene glycol monobutyl ether market in 2025–2026 has been shaped by deliberate price leadership and structural feedstock assurance. Effective January 6, 2025, Dow implemented a $0.05 per pound increase across E-series glycol ethers, specifically impacting Butyl Carbitol. This was followed by an additional $0.05 per pound increase effective November 6, 2025, reflecting sustained volatility in raw materials and energy inputs. These adjustments were largely absorbed by downstream coatings, construction chemicals, and personal care formulators, underlining DGBE’s role as a performance-critical, high-boiling solvent rather than a discretionary input.

Supply resilience has become a defining differentiator. In October 2025, Dow and MEGlobal finalized a strategic agreement to secure an additional 100 KTA of ethylene from Gulf Coast operations, stabilizing the integrated production of E-series glycol ethers. Regulatory tailwinds further reinforced demand. Under the EPA’s 2025 Clean Air Act updates, federal incentives expanded for facilities transitioning to low-vapor-pressure solvents, positioning DGBE as a preferred coalescent in green-label architectural and industrial coatings. Demand has also diversified into personal care, where late-2024 consumer data showed a 14.6% year-over-year increase in e-commerce sales, translating into a 9% rise in high-purity DGBE consumption for advanced cosmetic formulations. Following early-2025 Arctic Blast disruptions, producers invested in freeze-resistant Gulf Coast logistics, improving winter reliability for ethylene oxide derivatives.

China: Integrated Capacity Expansion and Carbon-Aware Export Strategy

China’s DGBE landscape is defined by scale, integration, and a growing emphasis on product carbon footprint differentiation. On November 25, 2025, BASF commissioned a high-performance dispersant line at its Nanjing Verbund site, leveraging integrated glycol ether production to serve fast-growing automotive and industrial coatings demand across Asia. This move coincides with the broader ramp-up of the SABIC Fujian petrochemical complex, which reached 87% completion by Q3 2025 and is scheduled for full start-up in Q3 2026. The complex will add 1.8 million metric tons of derivatives, including E-series glycol ethers, reinforcing domestic supply depth.

Sustainability credentials are becoming commercially material. Since mid-2025, BASF’s Nanjing cluster has operated on 100% renewable electricity, delivering a measurable 4% reduction in the carbon footprint of glycol and amine derivatives. Pricing dynamics reflect robust domestic pull. In June 2025, China’s spot benchmark for Butyl Carbitol reached $1,963 per metric ton, supported by renewed activity in textiles and electronics cleaning. Export strategies are evolving in parallel. Producers in the Jiangbei New Material Technology Park are pivoting toward low-PCF DGBE grades to maintain access to European markets under the Carbon Border Adjustment Mechanism, signaling a shift from volume-led exports to compliance-led competitiveness.

India: Quality Enforcement and Housing-Led Demand Acceleration

India’s DGBE market is transitioning from import dependence toward regulated self-sufficiency. In March 2025, the Department of Chemicals and Petrochemicals revised Quality Control Orders covering ethylene glycols and ethers, mandating strict BIS certification for both imported and domestic DGBE. This move elevated baseline purity expectations for pharmaceutical and electronics applications and raised entry barriers for sub-standard material.

Demand growth is structurally linked to construction. Under the Housing for All initiative, India is projected to add 11.5 million homes annually through 2026, catalyzing a sharp increase in water-borne decorative paints where DGBE functions as a critical film-forming and flow-control agent. To support this growth, chemical producers in the Gujarat PCPIR hub announced late-2025 capital expenditures to install domestic etherification units, targeting a reduction in the current 35% import reliance on Chinese Butyl Carbitol. Regulatory scrutiny is also tightening in pharmaceuticals. The CDSCO’s 2025 protocol updates require GC-MS validation for DGBE used in topical extractions, reinforcing demand for traceable, pharma-grade supply.

Germany and the European Union: Energy-Driven Premiums and Functional Diversification

Within the European Union, Germany represents a high-cost, high-compliance DGBE market. In June 2025, German Butyl Carbitol prices reached $2,021 per metric ton, the highest among major regions, reflecting elevated energy costs and the cumulative impact of REACH fee increases effective November 2025. Despite these pressures, demand remains resilient due to regulatory alignment and functional specialization.

Automotive applications are expanding beyond coatings. German OEMs, including Volkswagen Group, have increased the use of DGBE-based additives in 2026-model heavy-duty diesel engines to enhance urea-based SCR system efficiency under sub-zero conditions. At the same time, circular economy pilots are gaining traction. In late 2025, the Heerenveen site in the Netherlands, coordinated with German R&D centers, began piloting circular glycol ethers derived from chemically recycled polyolefins, targeting a 15% reduction in virgin feedstock use by 2027. This positions DGBE within Europe’s broader materials circularity agenda.

Saudi Arabia: Integrated Scale and Downstream Value Capture

Saudi Arabia’s strategy in the DGBE market emphasizes downstream value creation and price competitiveness. In late 2025, SABIC’s leadership confirmed the deployment of 12 proprietary technologies, including nine in-house patents, across new global facilities to prioritize high-value derivatives such as DGBE over commodity ethylene glycol. This strategic pivot is supported by world-scale integration at the Sadara complex, operated by Sadara Chemical Company.

The outcome is pricing stability and export leverage. By mid-2025, Saudi DGBE benchmarks stood at $1,784 per metric ton, the most competitive among major producing regions. Integrated feedstocks, energy cost advantages, and technology ownership allow Saudi producers to supply consistent volumes while meeting the evolving performance and sustainability requirements of downstream coatings, industrial cleaning, and specialty formulation markets.

Comparative Snapshot: Diethylene Glycol Monobutyl Ether Market by Region

Diethylene Glycol Monobutyl Ether Market Country Level Snapshot

|

Region

|

Primary Market Driver

|

Strategic Focus

|

Structural Outcome

|

|

United States

|

Cost pass-through and low-VOC incentives

|

Feedstock security, coatings and personal care

|

Stable demand with domestic sourcing preference

|

|

China

|

Integrated capacity and CBAM readiness

|

Scale plus low-PCF differentiation

|

Strong domestic pricing with compliant exports

|

|

India

|

QCO enforcement and housing growth

|

Import substitution, decorative paints

|

Rapid demand growth with rising quality thresholds

|

|

Germany / EU

|

Energy costs and REACH compliance

|

Automotive additives, circular pilots

|

Premium pricing and functional diversification

|

|

Saudi Arabia

|

Integrated scale and IP deployment

|

High-value derivatives, export competitiveness

|

Lowest regional pricing with downstream value capture

|

Diethylene Glycol Monobutyl Ether Market Report Scope

Diethylene Glycol Monobutyl Ether Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$234.4 Million

|

|

Market Size (2034)

|

$373.1 Million

|

|

Market Growth Rate

|

5.3%

|

|

Segments

|

By Purity Grade (High Purity Grade, Industrial Grade), By Application (Coalescing Agents, Solvents, Cleaning and Detergents, Chemical Intermediates, Additives), By End-User Industry (Paints and Coatings, Printing, Packaging and Inks, Electronics and Semiconductors, Automotive and Transportation, Pharmaceuticals and Cosmetics, Agrochemicals, Oil and Gas)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Inc., BASF SE, SABIC, LyondellBasell Industries N.V., Eastman Chemical Company, Huntsman Corporation, Nippon Shokubai Co., Ltd., China Petroleum & Chemical Corporation, INEOS Oxide, Indorama Ventures Public Company Limited, Jiangsu Yida Chemical Co., Ltd., Shiny Chemical Industrial Co., Ltd., Balaji Amines Limited, Tokyo Chemical Industry Co., Ltd., Hubei Xianlin Chemical Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Diethylene Glycol Monobutyl Ether Market Segmentation

By Purity Grade

- High Purity Grade

- Industrial Grade

By Application

- Coalescing Agents

- Solvents

- Cleaning and Detergents

- Chemical Intermediates

- Additives

By End-User Industry

- Paints and Coatings

- Printing, Packaging and Inks

- Electronics and Semiconductors

- Automotive and Transportation

- Pharmaceuticals and Cosmetics

- Agrochemicals

- Oil and Gas

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Diethylene Glycol Monobutyl Ether Industry

- Dow Inc.

- BASF SE

- SABIC

- LyondellBasell Industries N.V.

- Eastman Chemical Company

- Huntsman Corporation

- Nippon Shokubai Co., Ltd.

- China Petroleum & Chemical Corporation

- INEOS Oxide

- Indorama Ventures Public Company Limited

- Jiangsu Yida Chemical Co., Ltd.

- Shiny Chemical Industrial Co., Ltd.

- Balaji Amines Limited

- Tokyo Chemical Industry Co., Ltd.

- Hubei Xianlin Chemical Co., Ltd.

*- List not Exhaustive