Market Overview: Sustainable and High-Performance Packaging Driving Market Growth

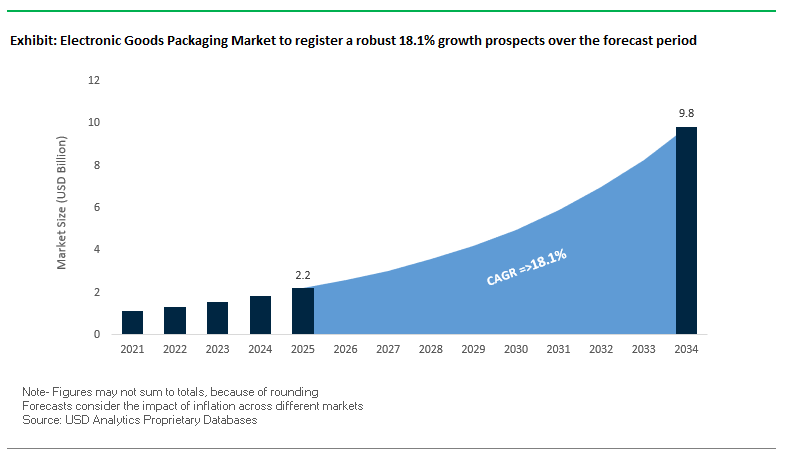

The Global Electronic Goods Packaging Market is projected to expand from USD 2.2 billion in 2025 to USD 9.8 billion by 2034, growing at a CAGR of 18.1%. This rapid growth underscores the critical role packaging plays in the global electronics supply chain, where performance, sustainability, and brand experience are equally important. Unlike general packaging, electronic goods packaging must balance product protection, e-commerce optimization, and circular economy goals.

The market is driven by rising demand for high-performance protection systems that shield fragile electronic components against temperature fluctuations, humidity, and physical shock. The e-commerce boom has heightened the importance of packaging as the first physical interaction point between consumers and brands, driving the need for premium and innovative unboxing experiences. At the same time, sustainability imperatives are pushing adoption of recycled paperboard, molded pulp, and high-PCR plastics, with governments enforcing stricter waste regulations.

Semiconductor and high-tech electronics packaging trends are also reshaping the industry. The focus on miniaturization and high-performance computing has created demand for specialized packaging solutions capable of supporting system-in-package (SiP) architectures and heterogeneous integration.

Key Insights for Industry Professionals:

- Market size: USD 2.2B (2025) → USD 9.8B (2034), CAGR 18.1%.

- E-commerce packaging is a major driver, with branding and consumer engagement becoming central.

- Sustainability shift toward recycled, compostable, and PCR-based materials.

- Thermal and electrical protection critical for semiconductor and advanced computing components.

- Smart packaging with NFC, RFID, and QR codes enabling consumer engagement and supply chain visibility.

Market Analysis: Recent Developments in the Global Electronic Goods Packaging Industry

The global electronic goods packaging sector is highly dynamic, with companies accelerating innovation in sustainable materials, protective performance, and digital integration.

In August 2025, Amphenol Corporation announced a USD 10.5B acquisition of CommScope’s Connectivity and Cable Solutions division, reinforcing its presence in IT and data center markets. This move is expected to drive demand for advanced protective packaging for fiber optic interconnects. Also in August, an industry report highlighted increased R&D in packaging materials designed to endure thermal stress and extreme conditions in semiconductor logistics.

July 2025 saw multiple developments: Sonoco Products Company committed USD 30M to expand its adhesives and sealants production, strengthening packaging material supply for electronics. The Amcor–Berry Global merger closed, creating a packaging giant with expanded capabilities in electronics packaging. Meanwhile, Antalis Packaging launched its “eRange” sustainable packaging boxes, crafted from FSC®-certified and 100% recyclable materials for e-commerce electronics.

Earlier, in May 2025, the International Paper–DS Smith merger was finalized, consolidating leadership in paper-based protective solutions for electronics. In April 2025, DS Smith was recognized for innovations such as fiber-based alternatives to plastic bubble wrap, enhancing fragile goods protection.

Sustainability partnerships are also shaping the industry. In February 2025, Sealed Air partnered with Best Buy to provide packaging solutions with high recycled content, including advanced BUBBLE WRAP® with PCR content, reducing virgin plastic use in electronics shipments.

Game-Changing Trends and Opportunities Transforming the Electronic Goods Packaging Market

Rapid Adoption of Engineered Fiber-Based Cushioning and Molded Solutions

The electronic goods packaging market is witnessing a decisive transition from expanded plastic foams (EPS, EPE) to molded fiber and corrugated paper-based cushioning. This trend is driven by growing consumer demand for plastic-free unboxing, regulatory frameworks like Extended Producer Responsibility (EPR), and corporate commitments to eliminate single-use plastics. For example, India’s E-Waste (Management) Rules, 2022 require manufacturers and importers to manage post-consumer waste, pushing brands to adopt recyclable materials. Electronics companies are actively partnering with molded fiber specialists to design custom-fit, biodegradable, and recyclable packaging solutions that meet both durability and compliance needs. This has opened new growth avenues, with molded fiber now applied across categories including laptops, printers, and even heavy industrial electronics. The shift also reshapes supplier relationships—packaging manufacturers are evolving into strategic design partners, co-developing sustainable, circular solutions with brands. This material shift not only reduces plastic waste but also strengthens brand equity by aligning packaging with environmental and consumer expectations.

Integration of Smart, Connected Packaging for Authentication and Engagement

Another major trend in the electronic goods packaging industry is the integration of smart packaging technologies such as QR codes, NFC chips, and unique serialization. These tools address the dual challenge of counterfeit prevention and consumer engagement. With counterfeiting posing a multibillion-dollar threat to global electronics, brands are embedding digital markers that allow consumers to instantly verify product authenticity. At the same time, these smart elements transform packaging into a digital gateway for product tutorials, warranty registration, loyalty programs, and cross-selling opportunities. For example, a global electronics company leveraged NFC tags in packaging to link consumers to interactive content, demonstrating how packaging can enhance both security and marketing. Packaging suppliers that offer end-to-end smart packaging platforms—from code generation to data analytics—position themselves as strategic partners in supply chain visibility and brand protection. This convergence of packaging and digital ecosystems is creating a more data-driven, connected value chain, opening new revenue streams while strengthening consumer trust in electronic brands.

Development of High-Barrier, Recyclable Paper-Laminated Films for Static Protection

One of the most pressing opportunities in the electronic goods packaging sector lies in developing recyclable or compostable alternatives to current metallized static-dissipative films, which are critical for safeguarding circuit boards and sensitive components. Traditional multi-material laminates used for electrostatic discharge (ESD) protection are difficult to recycle, contaminating existing waste streams. With static discharges capable of destroying microelectronics, demand for sustainable, high-barrier packaging is immense. Research is accelerating around monomaterial films such as polyethylene (PE) and polypropylene (PP) that deliver antistatic and protective properties while being easier to recycle. Companies pioneering these materials are positioning themselves as key players in the shift toward a circular electronic goods packaging economy. By balancing functionality with sustainability, these solutions appeal to brands under pressure to comply with waste management laws and meet ESG commitments. This innovation fosters collaboration between materials scientists, chemical companies, and packaging manufacturers, creating an ecosystem that can reshape static protection in electronics packaging.

Implementation of Hyper-Localized, Right-Sized Packaging On-Demand

The explosive growth of e-commerce and direct-to-consumer (D2C) electronics sales is fueling demand for right-sized, on-demand packaging solutions. Automated systems that cut, print, and assemble packaging tailored to individual orders are increasingly deployed at regional fulfillment centers. These solutions dramatically reduce corrugated board usage, void fill, and dimensional weight shipping costs, which represent a significant burden for electronics brands. For instance, a logistics company with automated carton forming systems reported processing up to 400,000 right-sized packages monthly, illustrating the scalability of this model. Beyond cost savings, localized right-sizing aligns with sustainability goals by minimizing material waste and lowering carbon footprints. This opportunity is also reshaping supply chains, as packaging suppliers collaborate with logistics providers and brand owners to deploy digitally integrated packaging ecosystems. By providing customized, sustainable, and efficient packaging, companies in the electronic goods packaging market gain a competitive advantage in the fast-evolving e-commerce landscape, where consumer expectations for sustainability and convenience continue to rise.

Competitive Landscape: Key Companies Shaping the Electronic Goods Packaging Industry

The electronic goods packaging market is led by global players combining protective technology, sustainability, and large-scale distribution to meet the needs of electronics and semiconductor industries.

Smurfit Kappa leverages WestRock merger for corrugated electronics packaging

As part of Smurfit WestRock, Smurfit Kappa is a global leader in paper-based packaging. It provides custom corrugated boxes, buffers, and inserts optimized for e-commerce and electronic goods. Following its merger, the company benefits from an expanded global footprint and shared best practices. Its strategic focus is on sustainable corrugated packaging with strong unboxing appeal.

Sealed Air strengthens protective solutions with recycled content initiatives

Sealed Air Corporation, renowned for BUBBLE WRAP® and protective foams, is a leader in electronics packaging. In February 2025, it partnered with Best Buy to expand use of recycled-content packaging in electronics logistics. With applications spanning laptops, TVs, and semiconductors, its strategy centers on automation, circularity, and reducing virgin plastic.

Amcor expands with Berry merger and smart packaging innovations

Following its merger with Berry Global (July 2025), Amcor is a powerhouse in consumer and electronics packaging. Known for integrating NFC and QR codes into flexible and rigid formats, Amcor enhances product tracking and consumer engagement. Its commitment to making all packaging recyclable by 2025 reflects its sustainability leadership, particularly in e-commerce-ready solutions.

Antalis launches sustainable eRange for e-commerce electronics

Antalis, a major European distributor, is strengthening its electronics packaging offering with its July 2025 eRange launch. This new line provides recyclable, FSC-certified, tape-free boxes tailored for secure electronics shipping. Combined with its acquisitions in e-commerce packaging, Antalis is well-positioned to serve Europe’s booming online electronics market.

Sonoco invests in adhesives and molded fiber for electronics protection

Sonoco Products Company is a diversified packaging supplier with a strong electronics focus. In July 2025, it invested USD 30M to expand adhesives and sealants capacity, crucial for electronics packaging integrity. Sonoco also delivers molded fiber cushions, corrugated containers, and custom protective designs, emphasizing its commitment to “Better Packaging. Better Life.

Electronic Goods Packaging Market Share Insights

Boxes Dominate Market Share by Product Type in Electronic Goods Packaging

Boxes account for 45% of the electronic goods packaging market, making them the undisputed leader by product type. Their dominance stems from their role as the primary outer packaging for nearly all consumer and industrial electronics. Folding cartons and rigid boxes not only provide the structural protection required to safeguard sensitive goods during complex global logistics but also deliver the premium unboxing experience that has become central to brand storytelling in high-value consumer electronics. For smartphones, laptops, and wearables, the box is both a protective vessel and a marketing platform, often integrating advanced printing, embossing, and sustainable materials to reinforce brand equity. Their share is further cemented by the ability to accommodate internal protective solutions such as trays, blisters, and foam inserts, making boxes the anchor of multipack systems that balance aesthetics, compliance, and protection.

Consumer Electronics Drive Market Share by End-User in Electronic Goods Packaging

Consumer electronics represent 55% of demand in the electronic goods packaging industry, underscoring how high-volume, brand-driven devices shape packaging requirements. Smartphones, tablets, laptops, and wearables dominate this segment, and each product cycle fuels a surge in packaging innovation. Here, packaging is not simply protective but a strategic tool for differentiation, sustainability positioning, and regulatory compliance. Companies leverage sophisticated folding cartons, premium rigid boxes, and high-resolution printing to deliver shelf appeal while embedding anti-counterfeit features like holograms and QR codes for authentication. As e-commerce accelerates, consumer electronics packaging must also ensure durability through extended shipping networks without compromising visual appeal, further reinforcing why this segment secures the largest market share.

United States Electronic Goods Packaging Market Driven by Smart Packaging and Sustainability Initiatives

The United States electronic goods packaging market is shaped by federal and state-level regulations, including the Department of Energy’s updated energy efficiency standards for electronic devices, which are driving demand for compact, lightweight, and cost-efficient packaging. Regulatory oversight by the FTC and EPA ensures compliance with labeling and recycling programs, pushing manufacturers to adopt eco-friendly packaging solutions.

Technological advancements are transforming the market with smart packaging innovations, including QR codes and NFC-enabled labels that enhance supply chain traceability and provide consumer engagement through product information or augmented reality experiences. Corporate investments are also accelerating growth; for instance, Menasha Packaging Company LLC acquired Color-Box from Georgia-Pacific LLC in February 2022 to strengthen its consumer electronics packaging capabilities. Key applications are concentrated in e-commerce and direct-to-consumer (DTC) electronics, where high-performance, sustainable, and customizable packaging solutions are in increasing demand. Trade tariffs on imported materials like aluminum and steel have further incentivized the use of alternative materials and domestic production.

Germany Electronic Goods Packaging Market Pioneering Circular Economy and Digital Product Transparency

Germany’s electronic goods packaging market is guided by stringent European Union regulations and national sustainability policies, which encourage energy efficiency and environmental responsibility. The country is a leader in circular economy practices, emphasizing recycled and reusable materials in packaging design and production. German consumers demand durable, premium packaging that balances functionality with eco-conscious attributes, influencing manufacturers to innovate continuously.

Technological advancements include machinery capable of handling sustainable materials, digital product passports, and watermarks that enhance material transparency and recyclability. Key applications include high-end electronics packaging for residential and commercial markets, with a focus on premium, energy-efficient products. Germany’s “Plattform Industrie 4.0” initiative supports the integration of cyber-physical systems and IoT into production, increasing operational efficiency and enabling smart, automated packaging lines.

China Electronic Goods Packaging Market Expanding Through Green Policies and Automation

China’s electronic goods packaging market is heavily influenced by the government’s “dual carbon” initiative, which promotes energy efficiency, recycling, and the use of sustainable materials across the industrial sector. The 2024 “Action Plan for Promoting Large-Scale Equipment Updates and Consumer Goods Replacement” encourages companies to adopt eco-friendly production methods, which benefits the electronic packaging segment directly.

Technological advancements, including automation, AI integration, and “5G plus industrial internet,” are optimizing production efficiency and enhancing flexible manufacturing capabilities. Domestic manufacturing is prioritized, with local companies expanding capacity to meet the growing demand for high-quality, circular packaging solutions. Rapid growth in e-commerce, consumer electronics, and urbanization is further propelling demand for innovative, durable, and environmentally responsible electronic goods packaging in China.

India Electronic Goods Packaging Market Accelerating with Smart City Projects and Domestic Manufacturing

India’s electronic goods packaging industry is benefitting from government initiatives such as “Housing for All” and the development of smart cities, which are stimulating demand for modern packaging solutions. The “Make in India” initiative also encourages local production, fostering technology transfer and infrastructure growth.

Corporate investments are rising, with new production facilities targeting high-quality and eco-friendly packaging. Technological adoption, including automation and modern materials, allows companies to produce innovative solutions suitable for India’s diverse consumer electronics market. Key applications are driven by the expansion of residential and commercial electronics sales, particularly through e-commerce channels. Regulatory support for circular economy practices is creating opportunities for sustainable and recyclable packaging solutions.

Brazil Electronic Goods Packaging Market Expanding Through Regulatory Support and Green Manufacturing

Brazil’s electronic goods packaging market is heavily influenced by ABNT and INMETRO standards, which set stringent quality and safety requirements. Compliance with these regulations ensures high-quality packaging while promoting sustainable practices.

Technological advancements, including robotics and AI, are enhancing manufacturing efficiency and product quality. Corporate investments in new facilities, such as Wheaton’s interactive design facility in São Paulo, support innovation in sustainable packaging solutions. Key applications include electronics for new construction, renovation, and consumer retail segments, where there is rising demand for eco-friendly, energy-efficient packaging. The market is experiencing growth driven by green manufacturing initiatives and increased consumer awareness of sustainability in packaging.

Electronic Goods Packaging Market Report Scope

Electronic Goods Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.2 Billion

|

|

Market Size (2034)

|

$9.8 Billion

|

|

Market Growth Rate

|

18.1%

|

|

Segments

|

By Product Type (Boxes, Blister Packs, Bags, Trays, Other Packaging Types), By Material Type (Plastic, Paper & Paperboard, Foam, Others), By End-User (Consumer Electronics, Industrial Electronics, Medical Electronics, Automotive Electronics, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Smurfit Kappa Group plc, Huhtamaki Oyj, International Paper Company, DS Smith plc, WestRock Company, Sonoco Products Company, Sealed Air Corporation, Rengo Co., Ltd., Billerud AB, Pregis LLC, Sonoco Products Company, Graphic Packaging Holding Company, Greif, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Electronic Goods Packaging Market Segmentation

By Product Type

- Boxes

- Blister Packs

- Bags

- Trays

- Other Packaging Types

By Material Type

- Plastic

- Paper & Paperboard

- Foam

- Others

By End-User

- Consumer Electronics

- Industrial Electronics

- Medical Electronics

- Automotive Electronics

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Electronic Goods Packaging Market

- Amcor plc

- Mondi Group

- Smurfit Kappa Group plc

- Huhtamaki Oyj

- International Paper Company

- DS Smith plc

- WestRock Company

- Sonoco Products Company

- Sealed Air Corporation

- Rengo Co., Ltd.

- Billerud AB

- Pregis LLC

- Sonoco Products Company

- Graphic Packaging Holding Company

- Greif, Inc.

* List Not Exhaustive

Methodology

USDAnalytics employed a rigorous, multi-layered research methodology to analyze the Global Electronic Goods Packaging Market, integrating both primary and secondary research to provide comprehensive, actionable insights for industry professionals. Primary research included structured interviews with packaging manufacturers, electronics OEMs, logistics providers, and sustainability consultants to understand demand drivers, technological adoption, and regulatory compliance. Secondary research leveraged company reports, press releases, government policies, trade publications, patents, and industry journals to validate market size, growth forecasts, and competitive dynamics. Quantitative analysis projected market growth, CAGR, and segmentation by product type, material, and end-user, while qualitative assessment emphasized emerging trends such as sustainable molded fiber solutions, smart packaging with NFC and QR codes, recyclable high-barrier films, and right-sized on-demand packaging. USDAnalytics also examined regional dynamics across the U.S., Germany, China, India, and Brazil, evaluating regulatory frameworks, green policies, e-commerce adoption, and technological innovations including automation and AI integration. This methodology ensures a precise, data-driven outlook, enabling stakeholders to make strategic, operational, and investment decisions in the fast-evolving electronic goods packaging sector.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.