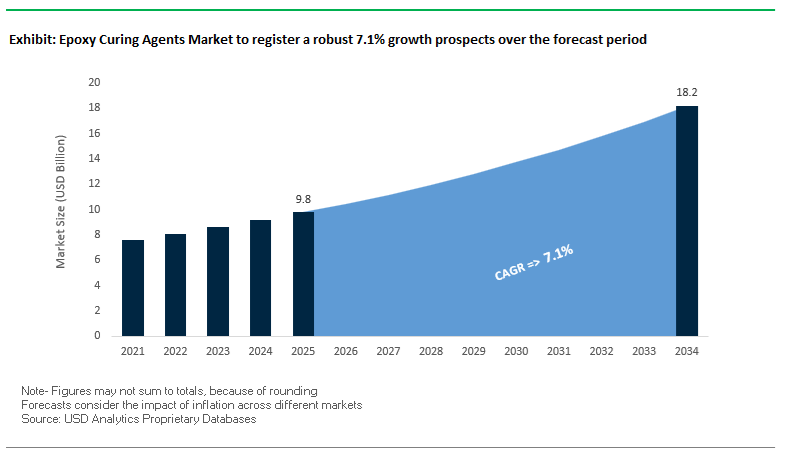

The Global Epoxy Curing Agents Market is projected to expand from USD 9.8 billion in 2025 to USD 18.2 billion by 2034, advancing at a CAGR of 7.1%, as curing chemistry becomes a decisive performance lever rather than a secondary formulation choice. Across protective coatings, fiber-reinforced composites, electrical insulation, and industrial flooring, curing agents directly govern crosslink density, glass transition temperature, chemical resistance, and application flexibility. As end-use industries move toward low-VOC systems, faster cure cycles, and longer service lifetimes, epoxy curing agents are increasingly specified to meet both performance and regulatory constraints simultaneously. This shift is especially pronounced in environments where downtime, corrosion risk, and thermal exposure translate directly into lifecycle cost and asset reliability.

From a formulation and processing standpoint, manufacturers are prioritizing curing agents that expand operating windows while simplifying application logistics. Phenalkamine curing agents derived from cashew nut shell liquid (CNSL) have become structurally important in marine, civil infrastructure, and tank lining coatings by enabling reliable curing at temperatures near 0°C, allowing year-round application and accelerated return-to-service without external heat input. In parallel, amine and cycloaliphatic amine systems, including IPDA derivatives, are enabling heat deflection temperatures above 100°C while maintaining low viscosity for resin infusion—an essential requirement in wind turbine blades and automotive composite structures where fiber wet-out and thermal endurance must be achieved concurrently. These developments reflect a broader industry demand for curing agents that improve throughput and application robustness without compromising mechanical or thermal performance.

Electrical and industrial coating applications are further elevating performance expectations. Alicyclic anhydride curing agents, widely specified in high-voltage insulation, are enabling glass transition temperatures approaching 180°C, supporting dielectric stability and long-term thermal endurance in transformers, switchgear, and power electronics. In epoxy powder coatings, dicyandiamide (DICY)-based accelerator systems continue to underpin film hardness, corrosion resistance, and heat stability in rebar, pipeline, and structural steel protection. Alongside these performance-driven trends, sustainability is no longer optional: polyamide curing agents containing 20–40% bio-based content are gaining qualification as formulators balance EHS compliance, low-VOC requirements, and decarbonization targets.

The past two years have seen strategic collaborations, capacity expansions, and product innovations redefining the epoxy curing agents landscape. Market leaders are focusing on renewable chemistry, EHS compliance, and production decarbonization, aligning with the global movement toward low-carbon industrial materials.

In March 2025, BASF SE and Sika AG jointly introduced Baxxodur® EC 151, a new amine-based curing agent tailored for epoxy flooring applications. Designed for ultra-low VOC systems, this hardener enables up to 66% faster curing even at low ambient temperatures (5–10°C), targeting high-traffic construction environments such as parking decks and industrial facilities. This collaboration underscores the ongoing shift toward productivity-optimized, sustainable construction adhesives.

By July 2025, Evonik Industries completed the transition of its Crosslinkers business line to 100% renewable electricity across global facilities in Germany, the UK, and the United States. The initiative aims to reduce Scope 1 and 2 emissions by one-third, reinforcing Evonik’s climate-neutral operations goal by 2050. The company’s efforts complement its earlier September 2024 launch of Ancamide 2853 and 2865, two nonylphenol-free, bio-based polyamide hardeners with 20–40% renewable content—engineered to meet stringent European and American EHS standards while offering flexibility and fast recoatability for protective coatings.

In August 2025, researchers achieved a major R&D breakthrough by synthesizing fully bio-based Schiff base epoxy curing agents from vanillin and amino acids. These agents demonstrated Tg values exceeding 141°C and superior mechanical strength, marking the next frontier in reprocessable and recyclable thermoset chemistry. Meanwhile, BASF’s December 2023 expansion of its Geismar, Louisiana site increased capacity for polyetheramines and specialty amine catalysts, strengthening global supply of amine-based epoxy hardeners used in wind turbine blades and aerospace composites.

Earlier developments such as Westlake Corporation’s AZURES product line (March 2023) and Huntsman’s acquisition of Gabriel Performance Products (January 2021) have reshaped the competitive landscape. Westlake’s SVHC- and CMR-free epoxy systems cater to the European coatings market, while Huntsman’s acquisition strengthened its mercaptan-based and anhydride hardener portfolio for fast-cure adhesives and electronics encapsulation. Furthermore, Huntsman’s joint venture with Zamil Group Holding (February 2010) expanded ethyleneamines production capacity (27,000 tonnes/year) in Saudi Arabia, providing a crucial precursor supply chain for high-volume amine curing agents across Asia and the Middle East.

Advances in Processing Efficiency, Green Chemistry & Thermal Engineering

Trend 1: Shift Toward Low-Temperature, Fast-Cure Epoxy Curing Agents for Composite Manufacturing Efficiency

Manufacturers in wind energy, automotive lightweighting, and industrial composites are rapidly adopting low-temperature, fast-cure epoxy curing agents to shorten production cycles and reduce energy costs. Technologies such as Evonik’s ultra-fast curing agent (Ancamine 2844), which delivers a 4.5-hour drying time at just 5°C, are transforming coating performance under cold and variable outdoor conditions. In wind turbine blade manufacturing, where massive molds require significant heating energy, next-generation amine hardeners enable faster demolding and dramatically improved throughput. Research on modified imidazole systems—such as the DGEBA/1C2E4MIM formulation that fully cures in 15 minutes at 120°C while achieving glass transition temperatures above 155°C—demonstrates how one-component, fast-cure solutions are enabling precisely controlled curing in automated processes including VARI and LCM.

Trend 2: Expansion of Waterborne & High-Solid Hardeners for VOC-Compliant Industrial Coatings

Stringent VOC and worker-safety regulations are accelerating the adoption of waterborne and high-solid epoxy hardeners across industrial coatings, concrete protection, and confined-space applications. Waterborne epoxy systems are engineered for high water-vapor permeability, enabling application on young concrete (<28 days) while avoiding osmotic blistering—an issue common with solvent-based coatings. These formulations allow fast return-to-service in construction projects and provide superior adhesion in high-moisture conditions. At the same time, zero-VOC, plasticizer-free hardeners—such as Evonik’s newer curative chemistries—support safe application in tanks, ships, and electronics facilities. High-solid, low-viscosity curing agents provide excellent flow and leveling while achieving >48% volume solids and <100 g/L VOC, matching solvent-based performance without environmental penalties.

New Material Frontiers in Bio-Circular Chemistry & Electronics Thermal Management

Opportunity 1: Bio-Based and Recyclable Hardener Systems for Circular Economy Compliance

Circular economy mandates are unlocking major innovation in bio-based epoxy hardeners and recyclable curing technologies. High-performance bio-epoxy systems are achieving 28–70% bio-carbon content while retaining strong mechanical and thermal properties, as demonstrated by systems such as “Polar Bear.” Equally transformative are cleavable amine hardeners like Recyclamine, which allow CFRP composites to be chemically depolymerized under mild aqueous conditions—yielding clean carbon fibers and a reusable thermoplastic polymer. These innovations support both “design-for-recycling” and “design-from-recycled-materials” strategies. In electronics, bio-based anhydrides derived from renewable sources (e.g., succinic acid) are emerging as eco-friendly alternatives that deliver excellent electrical insulation and chemical resistance, accelerating adoption in green electronics manufacturing.

Opportunity 2: Advanced Curing Agents for Thermal-Management-Driven Electronics Encapsulation

The surge in heat output from power electronics, EV inverters, LEDs, and high-density ICs is driving demand for epoxy curing agents engineered for thermal conduction, latency control, and high-temperature stability. Research shows remarkable gains in thermal conductivity—up to 1.72 W·m⁻¹·K⁻¹ using 80% hybrid fillers (Al₂O₃ + BN), an ~7.8× increase over pure epoxy matrices—enabled by compatible curing chemistries that maintain structural integrity. Companies like DELO are advancing latent-cure solutions such as DELO MONOPOX GE6515, which delivers 20 MPa strength on aluminum at 150°C while retaining 14 MPa at 200°C, and cures completely in 15 minutes at 130°C despite a working life of up to one week. Parallel research into dual-locked aminopyridine latent hardeners enables long shelf life with controlled curing between 120–154°C, reducing mixing defects and simplifying high-precision electronic packaging workflows.

Epoxy Curing Agents Market Share Insights, 2025-2034

Liquid epoxy curing agents represent the largest and most dynamic segment of the global epoxy curing agents industry, accounting for over 64% of the market share in 2025. Their dominance is attributed to their versatility, ease of formulation, and excellent compatibility with standard liquid epoxy resins. Liquid curing agents—such as amines, polyamides, and modified cycloaliphatics—enable precise control over reaction kinetics and viscosity, making them the preferred choice across coatings, adhesives, composites, and electrical applications. They offer exceptional processability, enabling uniform dispersion and controlled cure profiles essential for high-performance coatings and structural adhesives. In particular, epoxy coatings for marine, industrial, and automotive sectors rely heavily on liquid curing agents to achieve superior chemical resistance, mechanical strength, and weatherability. The segment continues to benefit from the growing trend toward low-VOC, solvent-free, and waterborne systems, with liquid curing agents designed for ambient-temperature curing gaining traction in environmentally regulated markets. Furthermore, innovations in bio-based amine and modified adduct formulations are expanding the appeal of liquid curing agents among manufacturers prioritizing sustainability and reduced carbon footprint.

olid epoxy curing agents hold a smaller but significant portion of the epoxy curing agents market, maintaining a strong foothold in high-performance powder coatings and electrical insulation applications. These agents—typically dicyandiamide (DICY), phenolic resins, or anhydrides—are valued for their extended shelf life, thermal stability, and low volatility. They enable the formulation of thermosetting powder coatings, offering outstanding chemical and corrosion resistance, which is critical for industrial machinery, appliances, and automotive components. In electrical and electronics applications, solid curing agents are preferred for producing epoxy-based encapsulants and insulators that must withstand high temperatures and electrical stresses.

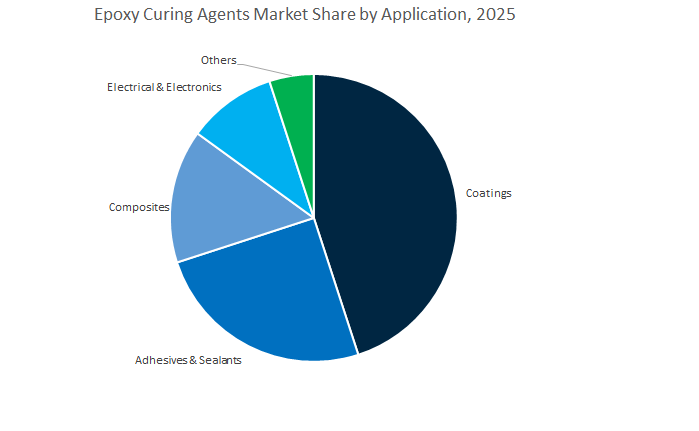

Coatings Segment Leads with 43.2% Share, Anchored by Expanding Infrastructure and Industrial Coating Demand

The coatings segment holds the largest share in the global epoxy curing agents market, accounting for 43.2% of total consumption in 2025. This dominance stems from epoxy’s unmatched performance in protective, industrial, and marine coatings, where curing agents play a vital role in defining the crosslinking density, chemical resistance, and durability of the final film. Coatings based on amine, polyamide, or anhydride curing agents offer superior adhesion, corrosion protection, and mechanical strength, making them indispensable in infrastructure maintenance, offshore structures, pipelines, and automotive refinishing. Rapid urbanization and industrialization, particularly in Asia-Pacific and the Middle East, continue to boost demand for epoxy-based anticorrosive coatings and floor coatings. In addition, the growing preference for low-VOC waterborne and high-solids formulations is driving innovation in amine-modified and accelerated curing systems designed to cure efficiently at lower temperatures. As global construction and manufacturing sectors expand, epoxy coatings remain the benchmark for long-lasting surface protection and mechanical integrity.

Epoxy curing agents are essential to the adhesives and sealants industry, a segment that continues to demonstrate robust growth due to the rising demand for lightweight, high-strength bonding solutions. Epoxy adhesives formulated with advanced curing agents—such as modified amines, aliphatic amides, and phenolic systems—deliver exceptional adhesion, high peel strength, and chemical resistance, making them ideal for automotive, aerospace, construction, and electronics assembly. Structural bonding applications, including metal-to-composite joints and composite repair, rely heavily on curing agents that provide controlled flexibility and temperature stability. In construction, epoxy sealants cured with polyamide or amine systems ensure watertight, weather-resistant joints for both new and refurbished infrastructure. Additionally, the ongoing trend toward low-temperature and fast-curing formulations supports productivity in industrial assembly lines. With advancements in toughened epoxy systems and hybrid chemistries, this segment is expected to see continued expansion across both high-performance and general-purpose bonding markets.

Beyond traditional sectors, the “Others” segment—comprising civil engineering, 3D printing, and niche industrial uses—is rapidly expanding as epoxy curing agents find novel applications in modern manufacturing and infrastructure. In civil engineering, epoxy curing agents are used to modify concrete and improve adhesion, durability, and resistance to moisture and chemicals in repair mortars and grouts. The additive manufacturing (3D printing) industry is emerging as a promising frontier, leveraging fast-curing, low-viscosity epoxy systems that enable high-resolution printing of industrial, biomedical, and dental components. These specialized curing systems offer controllable reaction profiles compatible with digital manufacturing technologies such as UV-assisted and thermal-curing additive processes.

The Global Epoxy Curing Agents Industry is characterized by strong R&D-driven players leveraging advanced amine chemistry, renewable raw materials, and application specialization. Key companies—Evonik Industries AG, Huntsman Corporation, BASF SE, Cardolite Corporation, and Kukdo Chemical Co., Ltd.—are driving performance and sustainability leadership across construction, marine, electrical, and composite markets.

Evonik Industries AG stands at the forefront of amine curing agent innovation, focusing on EHS-compliant, low-emission, and renewable crosslinking technologies. The company’s Ancamine® and Ancamide® portfolios feature bio-based contents up to 70%, catering to high-performance flooring, coatings, and adhesive systems. Evonik’s global R&D centers in Germany, the U.S., and China collaborate closely with formulators to tailor curing speed and mechanical properties for end-user specifications. Its 2025 transition to 100% renewable electricity underscores Evonik’s commitment to carbon neutrality and circular manufacturing.

Huntsman’s Advanced Materials division remains a major global force, offering Aradur® curing agents and Araldite® epoxy resins across 2,000+ customers in 30 countries. Following its acquisition of Gabriel Performance Products and CVC Thermoset Specialties, the company enhanced its range of mercaptan-based fast-cure and toughened epoxy systems. Huntsman’s expertise spans e-mobility, aerospace, and defense, providing thermal management and structural bonding adhesives for EV battery housings and aircraft composite panels. Its portfolio is widely approved across 200+ OEM specifications, reflecting deep technical validation and reliability.

BASF SE leverages its Baxxodur® curing agents to offer amine and polyetheramine solutions optimized for construction, composites, and coatings. The company’s 2025 collaboration with Sika AG yielded Baxxodur® EC 151, reducing VOC emissions by up to 90% and curing time by two-thirds compared to standard systems. BASF’s large-scale amine catalyst production at Geismar (Louisiana) ensures a reliable global supply chain, while its data-driven application support helps customers optimize pot life and exothermic profiles for precision applications.

Cardolite Corporation is the global leader in CNSL-derived phenalkamine hardeners, offering cold-cure, corrosion-resistant solutions for marine, offshore, and civil engineering coatings. Its products deliver fast overcoating and humidity tolerance, curing even at sub-zero conditions. With up to 50% renewable content, Cardolite’s phenalkamine and phenalkamide technologies enable low-VOC, high-solids coating formulations, reducing downtime in heavy-duty maintenance environments such as refineries and offshore rigs.

Kukdo Chemical Co., Ltd. is a vertically integrated Asian powerhouse in epoxy resins and curing agents, serving high-volume electrical, electronics, and automotive markets. Its diverse portfolio includes liquid amines, polyamides, and anhydride curing agents, optimized for PCB encapsulation, automotive coatings, and industrial laminates. With a strong production base across Korea, China, and Southeast Asia, Kukdo ensures consistent supply for global OEMs while investing in curing kinetics optimization for high-temperature stability and energy-efficient processing.

China continues to dominate the global epoxy curing agents market, supported by sweeping regulatory reform, manufacturing modernization, and massive construction and automotive demand. The introduction of new national standards GB 30981.1-2025 and GB 30981.2-2025—focused on limiting harmful substances in coatings—marks a decisive step toward low-VOC and non-amine curing technologies. The standards are reshaping industrial and architectural coating formulations, directly stimulating demand for aliphatic and cycloaliphatic amine curing agents designed for environmental compliance and superior corrosion resistance.

The country’s expansion of two-pack epoxy coatings for infrastructure applications—bridges, tunnels, and industrial flooring—continues to propel consumption of cost-effective yet high-durability amine-based curing agents. State-led industry consolidation is stabilizing feedstock supply chains, particularly for epichlorohydrin, reducing volatility in raw material prices. In parallel, the booming automotive and EV manufacturing sectors are increasingly incorporating epoxy-based adhesives and coatings for lightweight component bonding and battery encapsulation. Supported by national green manufacturing initiatives, China is solidifying its position as both the largest producer and consumer of environmentally compliant epoxy curing agents globally.

The United States epoxy curing agents market is advancing rapidly through innovations in composite materials, advanced manufacturing, and defense-grade bonding systems. Huntsman Corporation has taken a technological leap by integrating AI and machine learning platforms to optimize curing agent synthesis—reducing batch-to-batch variability by 40% and accelerating product development timelines. The aligns with the U.S. strategy to strengthen domestic manufacturing resilience under new industrial policies.

The adoption of anhydride and latent epoxy curing agents in aerospace and automotive applications is rising sharply due to their superior thermal stability and fatigue resistance, essential for Carbon Fiber Reinforced Plastics (CFRP) used in lightweight structural components. Simultaneously, the U.S. Environmental Protection Agency (EPA) continues to influence the industry with its VOC and toxic substance control frameworks, encouraging widespread use of water-based epoxy systems and low-toxicity phenalkamine hardeners in industrial flooring, protective coatings, and civil engineering. As the U.S. manufacturing sector embraces digital innovation and green compliance, the nation’s R&D leadership continues to redefine global standards for high-performance epoxy curing agents and sustainable composite systems.

Germany remains at the forefront of Europe’s high-performance epoxy curing agents market, leveraging its strong industrial base and sustainability-focused R&D ecosystem. Evonik Industries AG continues to expand production and application R&D for amine curing agents tailored to wind turbine manufacturing and on-site blade repair, addressing the rising need for fatigue-resistant and long-gel-time formulations. The directly supports Europe’s wind capacity expansion, which increasingly depends on advanced epoxy composite systems for larger, more efficient turbine blades.

Simultaneously, BASF SE is pioneering bio-based epoxy hardeners derived from renewable feedstocks to align with ECHA’s sustainability mandates and the European Green Deal. The materials promise performance parity with petroleum-derived counterparts while reducing carbon intensity. In addition, German R&D institutions are developing ultra-fast latent curing technologies optimized for 3D printing and additive manufacturing, enabling precision bonding in thermoset part production. Germany’s convergence of Industry 4.0 manufacturing, automotive lightweighting, and renewable energy R&D firmly positions it as a leader in next-generation, sustainable epoxy curing agent development.

India’s epoxy curing agents industry is experiencing robust growth, propelled by rapid industrialization, infrastructure development, and the localization of manufacturing. Leading domestic chemical producers such as Aditya Birla Chemicals and Atul Limited have expanded their epoxy resin and hardener portfolios, targeting the booming construction and industrial coatings segments. The government’s ongoing investment in smart city, rail, and urban infrastructure projects has intensified demand for polyamide and polyamine curing agents used in high-performance concrete bonding, crack injection, and flooring adhesives.

Beyond construction, India’s drive to establish itself as an electronics and semiconductor manufacturing hub is creating strong market traction for high-purity epoxy encapsulant curing agents with ultra-low voiding and excellent dielectric strength. The country’s evolving automotive localization strategy under “Make in India” further encourages adoption of domestically produced crash-resistant epoxy adhesives and curing agents. With expanding manufacturing capacity, government incentives, and growing export competitiveness, India is emerging as a critical player in the Asia-Pacific epoxy curing agents supply chain, particularly in construction, electronics, and renewable energy applications.

The Netherlands has positioned itself as a strategic hub for epoxy curing agent production and export, particularly in high-performance coatings and wind energy applications. Following Westlake Epoxy’s acquisition of Hexion’s global epoxy business, the country hosts one of Europe’s most advanced manufacturing and R&D centers for epoxy resins and hardeners, catering to wind, automotive, and marine markets.

The focus on marine-grade and offshore epoxy curing agents has intensified as the country supports the North Sea’s offshore wind farm expansion, which requires corrosion-resistant, high-adhesion coatings for extreme maritime conditions. Dutch innovation is also emphasizing epoxy systems with extended pot life and superior hydrolytic stability, suitable for large-scale shipbuilding and maintenance. Combined with its strategic logistics network and access to the broader European market, the Netherlands plays an essential role in supplying specialized curing agents for renewable energy and heavy industrial coatings applications.

South Korea’s epoxy curing agents market continues to thrive on the back of its advanced electronics, EV battery, and shipbuilding industries. Domestic manufacturers such as Kukdo Chemical Co., Ltd. are at the forefront of developing high-thermal-conductivity and low-dielectric-loss epoxy curing agents, specifically engineered for 5G infrastructure, semiconductor encapsulation, and new energy vehicle (NEV) applications. The innovations are vital to ensuring superior thermal management and signal integrity in high-density electronic assemblies.

Korean chemical producers are also scaling production of cycloaliphatic amine curing agents and anhydride hardeners for global export, targeting the automotive composites and marine coatings markets. With a growing focus on advanced material engineering and energy-efficient curing technologies, South Korea is emerging as a regional leader in specialty epoxy hardeners for electronics, mobility, and heavy industry applications, further reinforcing Asia’s dominance in the epoxy curing agents market.

Epoxy Curing Agents Market Report Scope

Epoxy Curing Agents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9.8 Billion

|

|

Market Size (2034)

|

$18.2 Billion

|

|

Market Growth Rate

|

7.1%

|

|

Segments

|

By Chemistry Type (Amines, Anhydrides, Polymercaptans, Catalytic Curing Agents, Phenols), By Product Form (Liquid, Solid, Solution/Solvent-Cut), By Temperature (Low Temperature Cure, Medium Temperature Cure, High Temperature Cure), By Application (Paints and Coatings, Adhesives and Sealants, Composites, Electrical and Electronics, Civil Engineering), By End-Use Industry (Building & Construction, Automotive & Transportation, Wind Energy & Power, Marine, Aerospace, Electrical & Electronics, General Industrial Manufacturing

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Huntsman Corporation, Evonik Industries AG, BASF SE, Cardolite Corporation, Olin Corporation, Kukdo Chemical Co., Ltd., Aditya Birla Chemicals Limited, Mitsubishi Chemical Corporation, Hexion Inc., Westlake Epoxy, Solvay S.A., Lonza Group AG, Kumho P&B Chemicals Inc., Nan Ya Plastics Corporation, Sika AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Chemistry Type

- Amines

- Anhydrides

- Polymercaptans

- Catalytic Curing Agents

- Phenols

By Product Form

- Liquid

- Solid

- Solution/Solvent-Cut

By Cure Speed/Temperature

- Low Temperature Cure

- Medium Temperature Cure

- High Temperature Cure

By Application

- Paints and Coatings

- Adhesives and Sealants

- Composites

- Electrical and Electronics

- Civil Engineering

By End-Use Industry

- Building & Construction

- Automotive & Transportation

- Wind Energy & Power

- Marine

- Aerospace

- Electrical & Electronics

- General Industrial Manufacturing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Huntsman Corporation

- Evonik Industries AG

- BASF SE

- Cardolite Corporation

- Olin Corporation

- Kukdo Chemical Co., Ltd.

- Aditya Birla Chemicals Limited

- Mitsubishi Chemical Corporation

- Hexion Inc.

- Westlake Epoxy

- Solvay S.A.

- Lonza Group AG

- Kumho P&B Chemicals Inc.

- Nan Ya Plastics Corporation

- Sika AG

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Epoxy Curing Agents Market end-to-end, delivering analysis reviews on demand drivers, specification shifts, and procurement risks while benchmarking cure profiles, crosslink density, and lifetime performance across high-solids, waterborne, and solvent-free systems. It highlights breakthroughs in bio-circular amine chemistries, low-temperature/fast-return flooring hardeners, and high-Tg anhydride platforms for electrification and composites—translating lab metrics (Tg/HDT, dielectric strength, corrosion panels, salt-spray, humidity/UV aging) into plant-ready selection guidance. With vendor capability mapping, compliance pathways (VOC/REACH/worker safety), and total-applied-cost playbooks for coatings, adhesives, composites, and electrical insulation, this report is an essential resource for R&D leaders, operations managers, and sourcing teams seeking durable performance with lower emissions and cycle times.

Scope Highlights

Segmentation:

- By Chemistry Type: Amines; Anhydrides; Polymercaptans; Catalytic Curing Agents; Phenols.

- By Product Form: Liquid; Solid; Solution/Solvent-Cut.

- By Cure Speed/Temperature: Low Temperature Cure; Medium Temperature Cure; High Temperature Cure.

- By Application: Paints & Coatings; Adhesives & Sealants; Composites; Electrical & Electronics; Civil Engineering.

- By End-Use Industry: Building & Construction; Automotive & Transportation; Wind Energy & Power; Marine; Aerospace; Electrical & Electronics; General Industrial Manufacturing.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Frame: Historic data 2021–2024 and forecast data 2025–2034.

Companies: Analysis/profiles of 15+ companies covering technology focus, strategic moves, certifications, and sustainability initiatives.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.