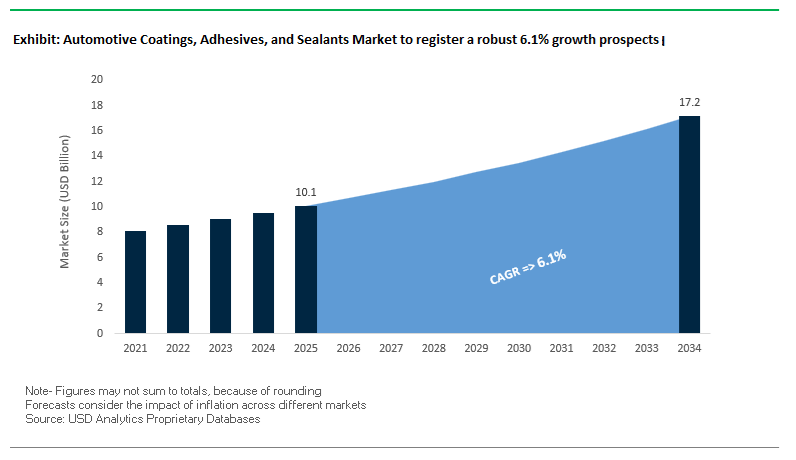

The automotive coatings, adhesives, and sealants market has become strategically critical as OEMs redesign vehicles around electrification, lightweight architectures, and tightening environmental compliance. Valued at USD 10.1 billion in 2025 and projected to reach USD 17.2 billion by 2034 at a CAGR of 6.1%, the market is no longer driven by surface finishing alone, but by the need for integrated material systems that support production efficiency, safety, and lifecycle durability. Automotive manufacturers are consolidating coatings, bonding, sealing, acoustic, and thermal protection functions into coordinated chemical platforms to meet rising expectations on emissions reduction, energy efficiency, and platform scalability across ICE, hybrid, and battery electric vehicles.

A core structural shift reshaping demand is the transformation of paint shops and body assembly operations. OEM adoption of 3-Wet Process coating systems—combining primer, basecoat, and clearcoat into a single bake cycle—has emerged as a manufacturing inflection point, reducing paint shop cycle times by up to 35% while materially lowering energy consumption and CO₂ emissions per vehicle. In parallel, waterborne and high-solids coating technologies have become the dominant production standard, with VOC levels consistently below 250 g/L to comply with regulatory limits across North America, Europe, and Asia. These shifts reflect OEM priorities to decarbonize high-energy manufacturing stages without sacrificing throughput, finish quality, or corrosion protection.

Electrification is accelerating substitution away from legacy materials toward high-performance protective and functional chemistries. In EV platforms, thermal barrier coatings and intumescent materials are increasingly specified to deliver a minimum 15-minute thermal protection delay during battery thermal runaway events, supporting enclosure integrity and occupant safety mandates. Exterior durability requirements are also rising, with ceramic-reinforced clearcoats achieving approximately 90% gloss retention after 1,000 wash and abrasion cycles, extending repaint intervals and lowering warranty exposure. Inside the vehicle, liquid-applied sound dampeners are displacing asphalt-based pads, delivering 3–5 dB cabin noise reduction while cutting weight and improving acoustic tuning—particularly critical for premium and electric vehicles where drivetrain noise masking is absent.

Over the forecast period, competitive advantage will hinge on manufacturers’ ability to scale low-VOC, energy-efficient coating lines, integrate multifunctional adhesive and sealant systems, and meet evolving OEM sourcing requirements around safety validation, process efficiency, and global regulatory alignment.

The global automotive coatings, adhesives, and sealants industry is undergoing technological and strategic realignment as key suppliers pivot toward sustainability, EV integration, and smarter manufacturing.

In October 2025, PPG Industries announced a joint solvent recycling initiative with SAIC General Motors in China, aimed at recovering 50% of used cleaning solvents in OEM paint shops. This project significantly reduces hazardous waste and reinforces PPG’s leadership in sustainable automotive coatings. During the same month, PPG also showcased its EV Total System Solutions at a leading North American battery show, emphasizing integrated battery coatings, adhesives, and sealants designed for thermal management and fire protection — underscoring how coatings chemistry is becoming a strategic part of EV system design.

In September 2025, Axalta Coating Systems unveiled its Voltatex™ 4224 impregnating resin, a high-thermal conductivity formulation that reduces electric motor weight by over 15% and lowers thermal stress by up to 30°C. This advancement directly supports the lightweighting and efficiency goals of next-generation electric drive systems. Earlier, in June 2025, BASF SE initiated construction of a new OEM coatings plant in Münster, Germany, dedicated to manufacturing sustainable automotive coatings for the European market — highlighting a strong regional commitment to eco-efficient production technologies.

In May 2025, BASF divested its decorative paints business in Brazil to Sherwin-Williams, refocusing on core high-performance segments such as automotive OEM coatings and Chemetall surface treatments, which are critical for substrate adhesion and corrosion resistance. Meanwhile, Kansai Paint (March 2025) influenced global design directions with its 2025–2026 Trend Colours Collection, shaping aesthetic decisions for next-generation mobility designs worldwide.

R&D excellence continued to define the year as Axalta (February 2025) received Edison and BIG Innovation Awards for its EV material science breakthroughs, while PPG (December 2024) expanded its Color Innovation Studio in China to enhance localized color-matching capabilities for Asian OEMs, reflecting a strategic focus on regional customization and digital design integration.

The global automotive industry is undergoing a paradigm shift toward low-VOC, solvent-free, and bio-based coatings, adhesives, and sealants, driven by environmental regulations and automaker sustainability commitments. The trend is reshaping material formulation strategies, particularly in interior bonding and coatings, where indoor air quality (IAQ) and vehicle lifecycle carbon reduction are top priorities.

Global OEMs—including Volkswagen, Volvo, and BMW—have set internal VOC emission limits under standards like VW PV 3925, Volvo VCS 1027 2739, and BMW GS97014, which measure and restrict volatile emissions from interior materials. These standards are directly aligned with Vehicle Interior Air Quality (VIAQ) initiatives, compelling suppliers to replace traditional solvent-based adhesives with waterborne and reactive PUR hot melts that meet sub-20 g/L VOC thresholds mandated by the U.S. EPA and similar agencies worldwide.

Leading adhesive manufacturers are introducing bio-reactive PUR hot melts containing up to 40% renewable raw materials, optimized for electronics and trim assembly. These materials combine eco-certification compliance with high mechanical performance, illustrating the dual objective of sustainability and strength. Their adoption in automotive assembly lines—particularly for EV electronics bonding and acoustic panels—signals a new commercial benchmark for green chemistry in mobility manufacturing.

Several markets impose legally binding VOC concentration caps across adhesives and sealants—ranging from 30 to 850 g/L, depending on the product class. The regulatory enforcement accelerates investment in waterborne acrylics, silane-modified polymers (SMPs), and 100% solids polyurethane systems, all of which deliver zero-solvent emission profiles while enhancing production safety and compliance for OEMs and Tier 1 suppliers.

The electrification of vehicles has unlocked a new era for multi-functional automotive CAS materials, designed to manage heat, vibration, fire risk, and structural integrity within EV architectures. The role of adhesives and coatings extends far beyond aesthetics and bonding—they are becoming integral to battery performance, safety, and lightweighting.

Next-generation thermally conductive silicone encapsulants and potting compounds have achieved thermal conductivity up to 3.0 W/m·K, enabling precise heat dissipation from densely packed battery cells. Many of these materials are also UL 94 V-0 rated, meaning they self-extinguish within 10 seconds—an essential property for preventing thermal runaway in high-voltage battery modules.

To achieve range efficiency, EV manufacturers are adopting thermally conductive adhesives (TCAs) and high-strength epoxies capable of bonding aluminum, CFRP, and composite components with conductivity values of 1.5–2.0 W/m·K. These materials not only improve battery thermal equilibrium but also enhance pack rigidity, reducing overall vehicle weight without compromising crash resistance.

Advanced low-viscosity silicone sealants are being engineered for void-free encapsulation with low mechanical compression. The minimizes stress on delicate battery cells and prevents cracking under charge-discharge cycling, directly improving battery lifecycle durability.

By combining thermal conductivity, vibration absorption, and fire resistance within a single formulation, CAS suppliers are enabling the next generation of safe, high-performance EV battery systems, positioning themselves at the center of electric mobility innovation.

The emergence of Gigacasting (or Megacasting)—large, single-piece aluminum castings for underbody and structural frames—is reshaping adhesive and sealant usage in vehicle assembly. As automakers like Tesla, Toyota, and Volvo expand the technique, the demand for high-tolerance structural adhesives and flexible sealants is growing exponentially.

Gigacasting requires the integration of large aluminum sections with High-Strength Steel (HSS) and composite panels, posing challenges in joining materials with different mechanical and thermal properties. Advanced structural adhesives are emerging as the preferred solution over welding, as they mitigate brittle intermetallic formation and enhance crash durability through elastic bonding that absorbs differential expansion.

Aluminum’s coefficient of thermal expansion is significantly higher than steel, creating stresses at joints during thermal cycling. To address the, CAS manufacturers are developing semi-structural sealants with elongation above 300% and superior fatigue resistance. These products ensure durable bonding performance in large-format castings exposed to harsh temperature gradients.

High-viscosity, non-sag, gap-filling sealants are being tailored for automated robotic dispensing across large and complex geometries. The ensures consistent joint integrity and rapid cycle times—crucial for scaling Gigacasting to mass-market EV production.

As Advanced Driver-Assistance Systems (ADAS) and autonomous driving technologies expand, demand is surging for coatings and adhesives that ensure the durability, optical clarity, and precision performance of LiDAR, radar, and camera sensors integrated into vehicle exteriors.

LiDAR sensors depend on highly transparent materials capable of transmitting near-infrared (NIR) light with minimal loss. Advanced anti-reflective (AR) coatings with over 95% transmission efficiency at 905 nm and 1550 nm wavelengths are being commercialized to optimize object detection accuracy, directly influencing autonomous navigation reliability.

To withstand environmental exposure, CAS suppliers are developing hydrophobic and oleophobic coatings that provide self-cleaning functionality—repelling water, dust, and oil residues. These solutions ensure continuous sensor visibility under diverse climatic conditions, safeguarding the operational performance of ADAS and autonomous systems.

Radar sensors embedded behind body panels or bumpers demand low-dielectric coatings with uniform electromagnetic properties. Formulations with low dielectric constants (Dk < 3.0) and minimal dissipation factors (Df) ensure that radar signals remain undistorted while maintaining aesthetic uniformity across vehicle surfaces. The functional convergence of design and signal transparency represents a growing R&D frontier for CAS suppliers targeting next-generation connected mobility platforms.

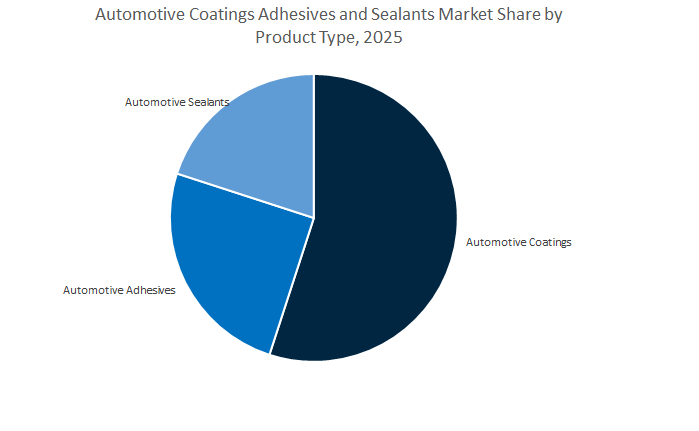

Automotive Coatings, Adhesives, and Sealants Market Share Insights, 2025-2034

The automotive coatings segment dominates the global automotive coatings, adhesives, and sealants (CAS) industry, accounting for approximately 55% of the total market share in 2025. This dominance is attributed to the critical role coatings play in vehicle aesthetics, corrosion protection, and long-term durability. Every vehicle, whether internal combustion or electric, undergoes a multi-layer coating process—including electrocoat (E-coat), primer, basecoat, and clearcoat—each serving a specific performance function. The coatings industry benefits from its high material value per vehicle and the extensive technological complexity of paint shop operations, making it the most value-intensive segment within the CAS value chain. Moreover, the growing demand for eco-friendly and energy-efficient coatings, such as waterborne, powder, and UV-curable systems, is transforming the automotive coatings landscape. As global automakers pursue carbon neutrality and reduced VOC emissions, coatings manufacturers are innovating with low-bake paints, self-healing clearcoats, and nanoceramic layers that extend surface longevity and improve vehicle gloss. Additionally, the proliferation of Electric Vehicles (EVs) and the need for lightweight, heat-dissipative, and static-resistant coatings are pushing the segment toward higher-performance chemistries, including ceramic-reinforced and anti-corrosion coatings tailored to battery housings and underbody protection.

The automotive adhesives segment stands as the fastest-growing area within the CAS market, driven by the accelerating global shift toward vehicle lightweighting, modular assembly, and electrification. Adhesives have become indispensable in replacing traditional mechanical fasteners, offering superior bonding strength, crash performance, and corrosion resistance, while reducing overall vehicle weight. Their growing adoption across Body-in-White (BIW) structural joints, glazing, interior trim, and EV battery modules underscores their versatility and expanding functional importance. The segment’s momentum is powered by reactive polyurethane (PU), epoxy, and acrylic-based adhesives, which provide exceptional strength and environmental durability across mixed-material assemblies—critical for modern vehicles utilizing aluminum, composites, and high-strength steels. Furthermore, Electric Vehicles (EVs) are dramatically increasing adhesive demand, as each battery pack requires thermal interface materials, cell/module bonding, and fire-retardant encapsulants, which contribute significantly to the CAS value per vehicle. The trend toward sustainable and recyclable bonding systems, including bio-based adhesives and reversible bonding chemistries, is reshaping OEM supply chains. As manufacturers push for lightweighting, safety, and reduced noise and vibration, adhesives are transitioning from supporting materials to strategic enablers of next-generation vehicle architectures.

The automotive sealants segment represents a vital, performance-critical pillar of the global CAS ecosystem, focusing on vehicle integrity, protection, and comfort. Sealants ensure long-term durability by providing waterproofing, dustproofing, corrosion resistance, and acoustical insulation across critical vehicle zones such as seams, welds, underbodies, and glazing joints. They are essential for achieving NVH (Noise, Vibration, and Harshness) control, thermal insulation, and structural stability, particularly in electric and hybrid vehicles, where cabin silence and component sealing are paramount. Modern sealant technologies—especially polyurethane, silicone, and modified silane polymer (MSP) systems—are designed for elasticity, high temperature resistance, and low shrinkage, allowing them to maintain tight seals across extreme operating conditions. As the global shift toward EV manufacturing accelerates, sealants are being re-engineered to support battery pack assembly, enclosure sealing, and fire resistance, addressing both safety and performance needs. Moreover, advanced robotic application systems and fast-curing chemistries are improving production efficiency in paint shops and assembly lines, reducing downtime and waste.

The Passenger Vehicle (ICE) segment continues to represent the largest share of the global automotive coatings, adhesives, and sealants industry, with a projected 55.4% market share in 2025. Despite the rapid rise of electrification, internal combustion engine (ICE) vehicles dominate global production volumes, especially in emerging markets such as India, ASEAN, and Latin America. This vast installed base ensures consistent, high-volume demand for CAS products across all manufacturing stages—from coating and bonding to sealing and finishing. ICE vehicles require multiple coating layers to withstand fuel exposure, exhaust heat, and environmental degradation, driving demand for high-durability epoxy primers, corrosion-resistant undercoats, and UV-stable clearcoats. Adhesives and sealants are equally critical for vibration damping, glass installation, trim bonding, and underbody sealing, ensuring comfort and longevity. While the per-vehicle CAS value in ICE models is lower compared to EVs, their sheer production scale sustains the segment’s dominance. In regions with gradual EV adoption, such as Southeast Asia and the Middle East, this segment will continue to underpin industry stability and serve as the volume backbone of the global CAS market through 2034.

The Passenger Vehicle (EV) segment is the fastest-growing and most value-intensive segment, capturing an estimated 25.2% market share in 2025 and expanding rapidly due to the global shift toward electrification, sustainability, and smart mobility. Electric Vehicles have a significantly higher CAS material value per unit, driven by their unique technical requirements: lightweight coatings for energy efficiency, thermally conductive adhesives for battery packs, and flame-retardant sealants for safety compliance. Adhesives play a particularly strategic role in EV production, replacing welds and bolts in battery cells, structural enclosures, and thermal interface materials (TIMs), helping manufacturers meet both weight reduction and thermal management goals. Coatings in EVs are engineered to provide electrostatic shielding, chemical resistance, and temperature stability, especially for battery housings and power electronics. Additionally, the segment benefits from the surge in automated manufacturing and modular construction, which relies heavily on adhesive and sealant precision. With global automakers investing in gigafactories and EV-focused assembly plants, the EV segment is expected to double its share within the next decade, driving profound innovation across the coatings and bonding materials ecosystem.

The commercial vehicle segment—comprising both Light Commercial Vehicles (LCVs) and Heavy Commercial Vehicles (HCVs)—represents a stable but high-value share of the automotive CAS industry. These vehicles require exceptionally durable coatings and sealants capable of withstanding prolonged exposure to extreme environmental and mechanical stresses. In HCVs, coatings must offer superior UV resistance, chip protection, and anti-corrosion performance for long-haul and off-road conditions, while sealants ensure air and water tightness in large cabin and trailer structures. LCVs, on the other hand, balance performance with cost efficiency, utilizing polyurethane adhesives and elastomeric sealants for body assembly, door panels, and cargo protection. The increasing use of adhesives in structural bonding and noise suppression is also enhancing comfort and aerodynamics, particularly in next-generation electric commercial fleets. As e-commerce and logistics growth propel urban delivery vehicle production, the demand for lightweight coatings and bonding materials tailored to LCVs is accelerating.

The global automotive coatings, adhesives, and sealants industry is dominated by companies with comprehensive portfolios and end-to-end integration capabilities across OEM coating systems, structural adhesives, and NVH sealants. The top market players — PPG Industries, BASF SE, Axalta Coating Systems, Henkel AG & Co. KGaA, Sika AG, and Kansai Paint Co., Ltd. —define the innovation trajectory for sustainable, high-performance vehicle finishing and bonding solutions.

PPG stands as a global single-source provider for OEM coating layers, adhesives, and battery protection materials. Its Optima Solutions™ portfolio streamlines paint shop efficiency by reducing energy and water consumption while eliminating hazardous chemicals. The company’s R&D focus on ceramic scratch-resistant clearcoats and powder primers enhances durability and reduces environmental footprint. PPG’s participation in EV thermal management projects reinforces its strategic goal of becoming the leading supplier for battery protection coatings and electronics adhesives. Its global color forecasting expertise continues to set trends for future vehicle aesthetics.

BASF leverages its Glasurit® 100 Line and R-M® AGILIS product families to achieve significant VOC reductions and energy efficiency improvements in OEM painting operations. The company’s Chemetall surface treatment technologies enable optimal substrate preparation, ensuring superior coating adhesion and corrosion resistance. BASF’s new Würzburg capacity expansion (2025) strengthens its European automotive coatings network. Its strategic roadmap toward net-zero by 2045 drives R&D into integrated process coatings and sustainable high-solids systems, consolidating its reputation as a global sustainability frontrunner.

Axalta continues to redefine mobility coatings technology, with its Voltatex™ line enabling motor weight reduction and thermal stress control for EV propulsion systems. Its HyperDyne™ and Lumeera™ coating technologies promote primerless applications and 3-wet process efficiency, shrinking OEM paint footprints. The company’s PACE Pilot Innovation Award (2025) underscores its leadership in OEM process optimization. Axalta’s five-point A-Plan emphasizes sustainable innovation, positioning the brand as a top-tier supplier of EV-related coating materials and electrical insulation systems.

Henkel leads the automotive adhesives and sealants sector with a strong emphasis on EV battery thermal management, Body-in-White (BIW) bonding, and acoustic dampening. Its Loctite® and Teroson® solutions enable multi-material structural assembly with fast-curing and solvent-free systems. Henkel’s application centers for e-mobility provide injectable thermally conductive adhesives (e.g., Loctite TLB 9300 APSi) for battery cooling and structural integrity. The company’s ongoing commitment to worker safety and sustainable chemistries supports global OEM adoption of low-VOC and non-hazardous adhesive formulations.

Sika’s expertise in elastic structural bonding and glass adhesive technology makes it a cornerstone supplier for automotive glazing and body assembly. Its Sikaflex® and SikaForce® product families deliver high-impact strength and primerless bonding across composite and lightweight vehicle structures. The Sika® Booster system enables controlled 1K polyurethane curing, enhancing process speed on high-throughput lines. Additionally, Sika supplies fully bonded body solutions for commercial vehicles, improving manufacturing simplicity and corrosion resistance.

Kansai Paint continues to dominate the Asia-Pacific coatings market through innovation in resin chemistry, dispersion agents, and color science. The company’s Global Color Concept influences OEM design palettes worldwide, while its R&D focus on functional coatings adds energy-saving, heat-reflective, and self-healing properties to automotive finishes. Kansai’s strength lies in localized production with global quality standards, ensuring consistent product performance for international OEM customers.

China continues to dominate the global automotive coatings and adhesives landscape, powered by the electrification boom and sustainability-driven production standards. The country’s EV coating technology advancements are led by major partnerships between domestic automakers and international chemical firms.

In March 2025, BASF Coatings and Li Auto Inc., one of China’s foremost New Energy Vehicle (NEV) leaders, signed a strategic cooperation Memorandum of Understanding (MoU) to drive innovations in low-carbon coating systems and digital manufacturing solutions. The collaboration emphasizes data integration, process automation, and the development of low-VOC, waterborne coatings tailored to China’s stringent environmental regulations.

The Chinese government’s tightening of VOC emission standards, particularly for automotive assembly and component plants in urban regions, is accelerating the industry-wide transition toward high-performance waterborne basecoats and sustainable primer systems. Simultaneously, adhesive manufacturers are prioritizing green chemistry and energy-efficient production, aligning with the national “Made in China 2025” initiative.

The integrated focus on sustainability and digitalization positions China as the benchmark for EV coatings and adhesive system innovation, catering to both domestic and global OEM platforms.

Germany remains a European leader in functional coatings and structural adhesive development, driven by lightweighting, energy efficiency, and safety compliance. The German automotive ecosystem—anchored by OEMs such as BMW, Volkswagen, and Mercedes-Benz—is leveraging R&D-intensive collaborations to enhance thermal management and acoustic performance in next-generation electric and hybrid vehicles.

Leading chemical manufacturers are investing in thermally conductive adhesives and intumescent coatings designed for EV battery packs, replacing traditional gap fillers with multifunctional materials that provide heat dissipation, compression, and fire protection. The formulations are critical for cell-to-cell bonding, ensuring both mechanical integrity and safety in thermal runaway events.

In 2025, BASF SE allocated a record R&D budget emphasizing sustainable automotive coatings and value-chain decarbonization. The development of Liquid-Applied Sound Damping (LASD) systems—based on advanced polymer dispersions—illustrates Germany’s precision focus on NVH (Noise, Vibration, and Harshness) optimization. Furthermore, robotic spray applications are being standardized across major European assembly lines for consistency and cost-efficiency.

Germany’s innovations in non-chrome primers, bio-based adhesives, and intumescent coatings continue to set global benchmarks for eco-friendly automotive manufacturing.

The United States automotive coatings and adhesives industry is advancing rapidly through smart coating innovation, sustainability programs, and multi-material adhesive film technologies. U.S.-based manufacturers are emphasizing high-durability, self-healing coatings, and energy-efficient refinish systems tailored for EVs, luxury vehicles, and aftermarket applications.

PPG Industries, Inc. continues to lead with its R&D focus on self-healing smart coatings, targeting luxury vehicle segments where surface protection, impact recovery, and optical clarity are critical. Axalta Coating Systems LLC is driving sustainability integration by developing low-VOC waterborne refinish solutions that reduce carbon emissions in automotive repair operations.

Additionally, 3M Company remains a global leader in advanced adhesive film solutions, introducing multi-layer systems for electronic bonding, structural reinforcement, and component protection. The films enable multi-material joining, supporting EV architectures that rely heavily on composite materials for weight reduction.

The U.S. market’s push toward energy-efficient, recyclable coatings and automated adhesive application technologies underscores its leadership in sustainable manufacturing and high-performance automotive materials.

Thailand is rapidly emerging as a regional powerhouse for automotive coatings and adhesives, fueled by government-backed EV initiatives and increasing foreign investment. The nation’s strategic location and strong manufacturing base make it a crucial supply hub for Southeast Asia’s automotive industry.

In 2025, PPG Industries inaugurated a new waterborne automotive coatings plant in Thailand, boosting regional capacity for eco-friendly, low-VOC coating systems. The investment supports Thailand’s policy ambition to become ASEAN’s leading EV production center, with manufacturers adopting high-solids coatings and advanced sealers for improved corrosion resistance and coating efficiency.

By promoting sustainable technology adoption, Thailand’s automotive manufacturing ecosystem aligns closely with international standards, especially those led by Japan, China, and South Korea. As a result, the Thai market is attracting increased participation from adhesive and coating specialists aiming to localize EV battery coating and sealing solutions.

Japan’s automotive coatings and adhesives industry is defined by its commitment to durability, functionality, and environmental stewardship. With global OEMs such as Toyota, Nissan, and Honda, the Japanese market prioritizes multi-functional polymer systems and coatings that enhance vehicle longevity and performance.

Companies like Toray Industries are pioneering functional polymer films that integrate with adhesives and coatings to improve lightweighting, anti-corrosion, and energy efficiency. The innovations are essential to meet next-generation EV platform requirements, emphasizing long-life clearcoat and epoxy-based anti-corrosion systems capable of withstanding extreme conditions.

Japan’s strong focus on precision and sustainability drives the development of high-durability coatings and smart adhesives that contribute to the global competitiveness of its automotive exports. As automakers transition toward battery-electric and hydrogen fuel cell vehicles, Japan continues to lead in the production of functional coating chemistries and environmentally resilient materials.

India’s automotive coatings and adhesives sector is expanding rapidly under the government’s “Make in India” and Production Linked Incentive (PLI) programs. With increasing emphasis on EV ecosystem localization, the country is seeing strong growth in battery component adhesives, thermal management sealants, and protective coatings.

Government incentives have accelerated Battery Electric Vehicle (BEV) production, prompting international and domestic chemical firms to invest in R&D for high-performance, thermally conductive adhesives used in battery pack assembly and cooling. Policy alignment discussions within the industry are also focused on harmonizing Goods and Services Tax (GST) on standalone batteries with complete EVs to ease cost pressures and stimulate adoption.

As India scales domestic production, manufacturers are prioritizing eco-friendly formulations and VOC-compliant coatings, ensuring global competitiveness while reducing environmental impact. The convergence of policy, investment, and innovation positions India as one of the fastest-growing automotive adhesive and coatings markets worldwide.

Automotive Coatings, Adhesives, and Sealants Market Report Scope

Automotive Coatings, Adhesives, and Sealants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$10.1 Billion

|

|

Market Size (2034)

|

$17.2 Billion

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Product Type (Automotive Coatings, Automotive Adhesives, Automotive Sealants), By Resin Type (Polyurethane, Epoxy, Acrylic, Alkyd, Silicone, Polyvinyl Chloride, Rubber, Styrenic Block Copolymers), By Technology (Waterborne Coatings, Solventborne Coatings, Powder Coatings, UV-Cured Coatings, High-Solids Coatings, Reactive, Hot Melt, Water-Based, Solvent-Based, Pressure Sensitive), By Application Process (Body-in-White / Paint Shop, Assembly, Power Train / Under-the-Hood), By Vehicle Type (Passenger Vehicles, Commercial Vehicles

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, PPG Industries, Inc., Axalta Coating Systems LLC, Henkel AG & Co. KGaA, Akzo Nobel N.V., Sika AG, 3M Company, H.B. Fuller Company, Nippon Paint Holdings Co., Ltd., The Sherwin-Williams Company, Dow Inc., Kansai Paint Co., Ltd., Arkema S.A., Wacker Chemie AG, Huntsman Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Type

- Automotive Coatings

- Automotive Adhesives

- Automotive Sealants

By Chemistry / Resin Type

- Polyurethane

- Epoxy

- Acrylic

- Alkyd

- Silicone

- Polyvinyl Chloride

- Rubber

- Styrenic Block Copolymers

By Technology

- Waterborne Coatings

- Solventborne Coatings

- Powder Coatings

- UV-Cured Coatings

- High-Solids Coatings

- Reactive

- Hot Melt

- Water-Based

- Solvent-Based

- Pressure Sensitive

By Application Process / Area

- Body-in-White / Paint Shop

- Assembly

- Power Train / Under-the-Hood

By Vehicle Type

- Passenger Vehicles

- Commercial Vehicles

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- BASF SE

- PPG Industries, Inc.

- Axalta Coating Systems LLC

- Henkel AG & Co. KGaA

- Akzo Nobel N.V.

- Sika AG

- 3M Company

- H.B. Fuller Company

- Nippon Paint Holdings Co., Ltd.

- The Sherwin-Williams Company

- Dow Inc.

- Kansai Paint Co., Ltd.

- Arkema S.A.

- Wacker Chemie AG

- Huntsman Corporation

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates how low-VOC coatings, advanced adhesives, and next-gen sealants are converging to enable lighter, quieter, and safer vehicles across ICE, hybrid, and EV platforms. Our analysis reviews integrated paint-shop processes (e.g., 3-Wet), waterborne/high-solids systems that compress cycle times, and EV-specific thermal/barrier solutions that fortify battery packs. It highlights multi-material bonding, primerless LSE adhesion, LASD-driven NVH gains, and intumescent/ceramic technologies designed for fire safety and durability. Capturing cost-per-body impacts, energy use, and compliance trajectories, the study surfaces breakthroughs in recyclable chemistries and debottlenecked application methods that raise first-pass yield. From strategy to line execution, this report is an essential resource for OEM engineering, procurement, and operations leaders seeking EV readiness, sustainability alignment, and process efficiency.

Scope Includes

- By Product Type: Automotive Coatings; Automotive Adhesives; Automotive Sealants

- By Chemistry / Resin Type: Polyurethane; Epoxy; Acrylic; Alkyd; Silicone; Polyvinyl Chloride; Rubber; Styrenic Block Copolymers

- By Technology: Waterborne Coatings; Solventborne Coatings; Powder Coatings; UV-Cured Coatings; High-Solids Coatings; Reactive; Hot Melt; Water-Based; Solvent-Based; Pressure Sensitive

- By Application Process / Area: Body-in-White / Paint Shop; Assembly; Power Train / Under-the-Hood

- By Vehicle Type: Passenger Vehicles; Commercial Vehicles

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Timeframe: Historic data 2021–2024 and forecasts 2025–2034.

- Companies: 15+ company analysis/profiles.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.