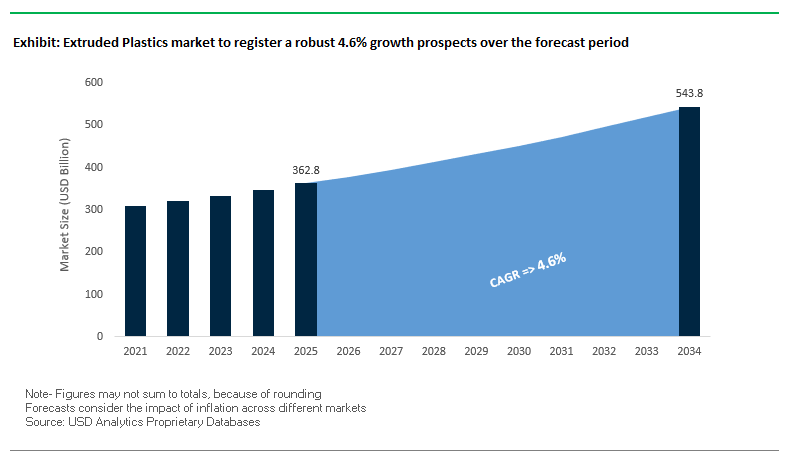

Market Overview: Extruded Plastics Market to Reach $543.8 Billion by 2034 at 4.6% CAGR

The global extruded plastics market is forecast to grow from $362.8 billion in 2025 to $543.8 billion by 2034, registering a steady CAGR of 4.6%. Extrusion technology underpins a wide array of industries ranging from packaging and construction to automotive and medical devices because of its efficiency in producing continuous products with consistent cross-sections. For industry professionals and buyers, this market represents both a cornerstone of global manufacturing and a fast-evolving sector where sustainability, speed, and digital transformation are redefining competitiveness.

Key Insights for buyers and professionals:

- High-Speed Production Gains: Extrusion lines now run 20% faster than five years ago, delivering higher volumes for pipes, films, and sheets.

- Sustainable Integration: Companies are incorporating up to 100% recycled or bio-based plastics in extrusion, reducing environmental footprints while maintaining performance.

- Smart Factories: Over 50% of new extrusion equipment in North America and Europe integrates IoT and AI systems, enabling predictive maintenance and real-time monitoring.

- Advanced Co-Extrusion: Modern equipment produces up to nine-layer films, crucial for high-barrier food packaging and specialized medical-grade sheets.

Market Analysis: Sustainability, Acquisitions, and Technology Fuel Growth

The extruded plastics industry is being reshaped by strategic acquisitions, material innovation, and recycling-driven breakthroughs, with 2024–2025 marking pivotal shifts.

In August 2025, Covestro acquired Swiss firm Pontacol, a specialist in multi-layer adhesive films, expanding its reach in medical and specialty film markets. The same month, Jindal Poly Films approved a scheme of arrangement, signaling potential restructuring or consolidation to streamline global operations. Also in July 2025, Sigma Stretch Film committed $39 million to expand facilities in Georgia, boosting stretch film production for packaging and industrial sectors.

Mergers are reshaping the supply chain as well. In April 2025, International Paper finalized its $9.9 billion acquisition of DS Smith, consolidating resources for packaging materials that feed directly into extrusion demand. In January 2025, Davis-Standard acquired Extrusion Technology Group (ETG), strengthening its machinery portfolio with brands like battenfeld-cincinnati. Meanwhile, BASF announced in March 2025 it would exit its Styrodur business to sharpen focus on Neopor and Styropor, materials critical for protective and insulating extrusion applications.

Sustainability milestones are also defining market direction. In February 2025, PureCycle received a Plastics Sustainability Award for its PureFive™ recycled polypropylene (PP) resin, a breakthrough enabling high-quality extrusion-grade recycled plastics. Further back in December 2024, Sonoco divested its Thermoformed and Flexibles Packaging business for $1.8 billion, narrowing its focus toward industrial paper and molded solutions, including extruded applications.

Trends and Opportunities Defining the Future of the Extruded Plastics Market

Strategic Reshoring and Capacity Expansion in North America

The extruded plastics market is witnessing a pronounced shift towards reshoring and capacity expansion across North America. This movement is being fueled by ongoing supply chain disruptions, geopolitical instability, and favorable government initiatives that encourage domestic production. For critical industries such as healthcare, automotive, and infrastructure, ensuring a resilient supply of extruded plastic products has become a strategic imperative.

A 2023 report from the Plastics Industry Association (PLASTICS) underscored the central role of the plastics industry in U.S. manufacturing, supplying materials that underpin millions of jobs. In response, companies are rapidly expanding plastics processing and extrusion facilities across the United States and Canada to reduce dependence on offshore supply. This domestic investment trend is not only addressing supply security but is also aligning with policies that promote “Made in the U.S.A.” quality assurance, intellectual property protection, and tighter production oversight.

Government support further amplifies this reshoring wave. The U.S. International Trade Administration emphasized that localized production improves control over product standards while minimizing exposure to global supply disruptions. For the extruded plastics industry, this translates into faster innovation cycles, improved supply chain resilience, and increased opportunities for serving growth sectors such as medical devices, electric vehicles, and renewable energy infrastructure.

Accelerated Adoption of Advanced Recyclates in Coextrusion Processes

Parallel to reshoring, sustainability has become a defining trend, with the industry accelerating the adoption of post-consumer recycled (PCR) content through coextrusion technology. Coextrusion enables manufacturers to integrate recycled plastics within multi-layered structures without compromising performance. By embedding recycled layers between virgin polymer skins, companies can achieve high PCR usage while preserving product strength, barrier protection, and visual appeal.

Chemical recycling is also advancing the integration of previously non-recyclable mixed-polymer waste streams into extrusion feedstocks. Companies such as Condale Plastics are working with suppliers exploring depolymerization processes that yield high-quality recycled materials, positioning coextrusion as a cornerstone of the circular economy for plastics.

Major global brands are directly influencing this trend by demanding recyclable and sustainable packaging. Firms such as Nestlé and Unilever are piloting mono-material packaging solutions with elevated PCR content, which intensifies demand for extruded film and sheet technologies that blend sustainability with regulatory compliance. This not only helps companies achieve corporate ESG goals but also enhances consumer acceptance of recycled plastics in mainstream applications.

Development of High-Barrier Monomaterial Structures for Recyclability

One of the most transformative opportunities in the extruded plastics packaging market is the innovation of monomaterial flexible structures with high-barrier properties. Historically, multi-material laminates have been used to achieve barrier protection for food and pharmaceutical packaging, but these designs are notoriously difficult to recycle. The move towards monomaterial structures such as all-PE or all-PP extrusions addresses this challenge while aligning with global recyclability mandates.

The European Union’s Packaging and Packaging Waste Regulation (PPWR) is a powerful driver, mandating full recyclability of packaging by 2030. Companies like DNP Group have already demonstrated progress with mono-PE packages capable of delivering high oxygen and water vapor barriers. Similarly, Jindal Films is advancing polypropylene films engineered for aroma, gas, and moisture protection, which can effectively replace aluminum foil and metallized PET laminates.

Consumer expectations further reinforce this opportunity. As eco-conscious purchasing rises, shoppers increasingly seek brands using recyclable and environmentally responsible packaging. Companies investing in advanced extrusion technologies that enable monomaterial, high-barrier films will not only comply with regulations but also capture a competitive advantage in an era of growing sustainability scrutiny.

Precision Extrusion for Medical and Pharmaceutical Applications

The expanding global healthcare market, driven by aging populations and rising demand for advanced therapies, creates a lucrative opportunity for precision extrusion in medical and pharmaceutical applications. Extruded components such as micro-tubing, multi-lumen catheters, and specialized drug delivery devices require extremely tight tolerances, biocompatibility, and compliance with stringent regulatory standards.

The miniaturization of medical devices is a central driver. Companies like Teleflex Medical OEM are pushing the boundaries of micro-extrusion, producing tubing as small as 0.005 inches in outer diameter for minimally invasive surgical tools. This level of precision allows for innovations in procedures that reduce patient recovery time and enhance clinical outcomes.

Moreover, the complexity of multi-lumen tubing, capable of performing multiple functions within a single device, highlights how extrusion technology supports next-generation drug delivery and diagnostic solutions. Advanced die designs and real-time monitoring ensure dimensional accuracy and quality control, which are critical for FDA and EMA regulatory compliance.

For stakeholders, precision extrusion represents a high-margin growth avenue that combines technology leadership with expanding global demand in medical devices and pharmaceuticals. Manufacturers that invest in advanced tooling, cleanroom facilities, and process monitoring will position themselves at the forefront of this opportunity.

Competitive Landscape: Global Leaders Driving Extrusion Innovation and Circularity

The extruded plastics market is highly competitive, with global chemical giants, machinery specialists, and integrated solution providers driving value through sustainability, automation, and advanced materials.

Dow Inc. Expanding Polyethylene Resin Leadership with Circular Polymers

Dow remains a dominant supplier of polyethylene (PE) resins, the most widely used raw material for extrusion in films, pipes, and coatings. The company’s strategic roadmap includes Valuing Nature and Advancing a Circular Economy, with heavy investments in recycling and renewable feedstocks. A recent collaboration with Fuenix Ecogy Group enables Dow to produce circular polymers from plastic waste, reinforcing its leadership in sustainable extrusion resins.

BASF SE Focusing on Neopor and Styropor in EPS-Based Extrusion

BASF’s plastics portfolio spans polyethylene, polystyrene, and polyamides, all critical for extrusion. Its ChemCycling™ initiative is central to producing plastics from chemically recycled waste. In March 2025, BASF exited its Styrodur business to concentrate resources on Neopor and Styropor EPS, while investing in 50,000 tons of new Neopor capacity at Ludwigshafen. This reflects its targeted strategy to dominate sustainable and high-value extrusion materials.

Davis-Standard, LLC Strengthening Global Machinery Capabilities with ETG Acquisition

As a leading manufacturer of extrusion equipment, Davis-Standard offers systems for films, sheets, profiles, and pipes. Its acquisition of ETG in January 2025 expanded its global footprint and enhanced its portfolio with brands like battenfeld-cincinnati. Recent innovations include the SHO Extruder, which delivers 20% higher output while maintaining energy efficiency. With deep engineering expertise, Davis-Standard excels at providing customized extrusion solutions for industries ranging from medical tubing to multilayer packaging.

KraussMaffei Driving Smart Manufacturing with “Plastics 4.0”

Germany’s KraussMaffei is a global leader in extrusion and compounding machinery, offering advanced single- and twin-screw extruders. Its Plastics 4.0 digitalization initiative provides predictive maintenance, real-time analytics, and networked systems, enabling highly automated extrusion lines. The company’s twin-screw extruders are especially valued for complex compounding, offering superior mixing and energy efficiency. KraussMaffei’s strategic white paper outlines the role of AI in boosting extrusion sustainability, positioning it as a frontrunner in digitalized manufacturing solutions.

Extruded Plastics market Share Insights

Blown Film Extrusion Leads Market Share by Process Type in Extruded Plastics

In 2025, blown film extrusion accounts for 35% of extruded plastics by process, reflecting its central role in flexible packaging from retail bags and stretch wrap to multi-layer barrier films for food. Its dominance is secured by continuous demand from FMCG and e-commerce, where film performance (sealability, puncture resistance, oxygen/moisture barriers) and high-throughput lines lower unit costs. Pipe & tubing extrusion at 25% remains the infrastructure backbone, with PVC, HDPE, and PEX serving water, sewer, irrigation, and building services; non-corrosive durability and capex-efficient installation keep share resilient amid global replacement cycles. Profile extrusion sustains share through building products (vinyl windows, decking, trims) that displace wood/metal for lower maintenance and better thermal performance. Sheet extrusion underpins rigid packaging and displays (thermoformed blisters/clamshells, signage), benefiting from retail-ready formats, while fiber extrusion holds a specialized niche in technical textiles and industrial fibers where tensile strength and chemical resistance are paramount. Overall, process-level share maps directly to packaging volume intensity, infrastructure capex cycles, and material substitution trends that favor engineered plastics.

Packaging Applications Dominate Market Share by Application in Extruded Plastics

By application, packaging captures 40% of extruded plastics demand in 2025, leveraging blown films and sheets to serve food, beverage, and consumer goods with consistent run-rates and SKU proliferation; the growth engine remains flexible packaging, even as recyclability and EPR policies push downgauging and recycled-content adoption. Building & construction at 30% provides long-cycle stability via pipes, window profiles, siding, and insulation tied to urbanization and retrofit programs. Automotive uses (interior trims, seals, hoses) expand as lightweighting and NVH control replace metal/rubber with engineered polymers, while electrical & electronics rely on extrusion for wire/cable insulation and conduits demanding flame retardancy and thermal stability. Medical maintains a high-value niche biocompatible tubing and device components with sterilization compatibility commanding premium pricing despite lower volumes. Share distribution mirrors three structural drivers: packaging throughput and line efficiency, infrastructure renewal in pipes/profiles, and component miniaturization with performance materials in mobility, electronics, and medical.

United States: Driving Extruded Plastics Growth Through Sustainability and Advanced Applications

The U.S. extruded plastics market is witnessing significant transformation driven by sustainable manufacturing and recycling initiatives. Industry leaders are investing heavily in post-consumer recycled (PCR) content, exemplified by the Heinz, Tesco, Berry Global, Plastic Energy, and SABIC collaboration, which produced Heinz Beanz Snap Pots using 39% recycled soft plastic. Additionally, the rapid adoption of automation and AI-driven manufacturing systems enhances production efficiency, predictive maintenance, and quality control, making the U.S. a global hub for technologically advanced extrusion.

Key applications in automotive and healthcare sectors are major growth drivers. Lightweight and durable extruded plastics are increasingly used in electric vehicles and medical-grade tubing and components. Meanwhile, manufacturers navigate a complex regulatory environment, particularly concerning food-grade recycled plastics, where FDA’s “No Objection Letters” for recycled content play a pivotal role in ensuring compliance and facilitating innovation.

Germany: Leading Europe in Industrial Applications and Circular Economy Initiatives

Germany’s extruded plastics market is a key player in Europe, driven by robust demand from construction and automotive sectors. Extruded profiles are widely used for window frames, door systems, and vehicle interiors, valued for their durability, efficiency, and precision. The country is also a leader in promoting a circular economy, with a strong focus on recyclable and reusable plastics aligned with the European Green Deal. Collaborative initiatives between manufacturers and end-users aim to establish closed-loop systems for sustainable plastic use.

Technological leadership is another distinguishing factor. German companies are pioneering advanced extrusion machinery that optimizes material processing, boosts output, and reduces energy consumption. Strategic investments in automation and precision technology enable the country to maintain a competitive edge in both industrial and high-performance applications.

China: Expanding Extruded Plastics Production and Domestic Demand

China is a global leader in extruded plastics manufacturing, with massive production capacity supporting both domestic consumption and international exports. The country’s ability to produce a wide range of extruded products at competitive prices positions it as a critical global market driver. Rising domestic demand in construction, automotive, and packaging sectors is fueled by urbanization, industrial growth, and a growing middle class, which drives the need for extruded pipes, films, and profiles.

Governmental efforts are further shaping the market. The introduction of nine new national standards for recycled plastics, effective February 2026, emphasizes recyclability and fosters a more robust recycling ecosystem. To meet these requirements and high-volume demand, Chinese manufacturers are investing in advanced extrusion technology and automation, ensuring cost-effective, high-quality, and sustainable production.

India: “Make in India” and Plastic Parks Driving Market Expansion

The Indian extruded plastics market is growing rapidly under the “Make in India” initiative, which encourages both domestic production and foreign investment. Companies like Jindal Poly Films are expanding production capacities, strengthening India’s position as a regional manufacturing hub. The Plastic Parks Scheme provides shared infrastructure and operational support, reducing costs and facilitating new investments in extrusion technology.

Sustainability is a key focus, driven by Extended Producer Responsibility (EPR) regulations. Indian manufacturers are collaborating with recyclers to incorporate post-consumer recycled (PCR) content, aligning with global circular economy trends. The industry is also witnessing growth in applications across packaging, construction, and industrial sectors, supported by modern infrastructure and government incentives.

Brazil: Innovation in Bioplastics and Industrial Applications

The Brazilian extruded plastics market is primarily driven by food & beverage and civil construction sectors. Extruded pipes and profiles are essential for infrastructure projects, while extruded films and sheets are widely used in packaging consumer goods.

Sustainability initiatives are gaining momentum, particularly through innovation in bio-based plastics. Companies like Braskem are leading the development of green polyethylene derived from sugarcane ethanol, a sustainable raw material for extruded products. This aligns with global trends toward eco-friendly and circular packaging solutions, enabling Brazil to compete in both domestic and international markets.

Japan: High-Precision Manufacturing and Technological Innovation

Japan’s extruded plastics industry is distinguished by its focus on high-quality, precision manufacturing. The market caters to high-end applications in the automotive, electronics, and medical sectors, where component performance and reliability are critical.

Technological innovation is a defining feature. Japanese companies are developing multi-layer extrusion techniques for films with superior barrier properties and leveraging nanotechnology to enhance material performance. Strategic partnerships, such as the collaboration between Orbetron and Technovel Corporation, expand market reach and integrate advanced extrusion solutions across Japan and North America, reinforcing Japan’s position as a technology-driven extruded plastics hub.

Extruded Plastics Market Report Scope

Extruded Plastics market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$362.8 Billion

|

|

Market Size (2034)

|

$543.8 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Resin Type (Polyethylene, Polypropylene, Polyvinyl Chloride, Polystyrene, Other Resins), By Process Type (Profile Extrusion, Sheet Extrusion, Blown Film Extrusion, Pipe & Tubing Extrusion, Fiber Extrusion), By Application (Packaging, Building & Construction, Automotive, Electrical & Electronics, Medical, Other Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Chemical Company, LyondellBasell Industries Holdings N.V., ExxonMobil Corporation, SABIC, Sinopec Corp., Formosa Plastics Corporation, Braskem S.A., REHAU AG + Co, Pexco, JM Eagle, Inc., Solvay S.A., Mitsubishi Chemical Corporation, DuPont de Nemours, Inc., Westlake Chemical Corporation, PolyOne Corporation (Avient Corporation)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Extruded Plastics Market Segmentation

By Resin Type

- Polyethylene

- Polypropylene

- Polyvinyl Chloride

- Polystyrene

- Other Resins

By Process Type

- Profile Extrusion

- Sheet Extrusion

- Blown Film Extrusion

- Pipe & Tubing Extrusion

- Fiber Extrusion

By Application

- Packaging

- Building & Construction

- Automotive

- Electrical & Electronics

- Medical

- Other Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Extruded Plastics Market

- Dow Chemical Company

- LyondellBasell Industries Holdings N.V.

- ExxonMobil Corporation

- SABIC

- Sinopec Corp.

- Formosa Plastics Corporation

- Braskem S.A.

- REHAU AG + Co

- Pexco

- JM Eagle, Inc.

- Solvay S.A.

- Mitsubishi Chemical Corporation

- DuPont de Nemours, Inc.

- Westlake Chemical Corporation

- PolyOne Corporation (Avient Corporation)

*List not Exhaustive

Research Coverage

This report investigates the global extruded plastics market, highlighting breakthroughs in multi-layer coextrusion, precision extrusion for medical applications, and circular economy integration. USDAnalytics’ analysis reviews market dynamics driven by strategic acquisitions, sustainability innovations, digitalized manufacturing, and regional reshoring trends, emphasizing opportunities for manufacturers, machinery suppliers, and end-users seeking high-performance, cost-efficient extrusion solutions. This report is an essential resource for packaging engineers, construction planners, automotive component designers, and medical device developers, offering actionable insights on emerging resin types, advanced extrusion techniques, and recycled-content applications. Historical data from 2021 to 2024 and forecast data through 2034 illustrate shifts in demand for polyethylene, polypropylene, PVC, polystyrene, and other resins across profile, sheet, blown film, pipe & tubing, and fiber extrusion processes. Market highlights include packaging, building & construction, automotive, electrical & electronics, and medical applications, alongside competitive analysis of 15+ global companies driving innovation, automation, and sustainability in the extruded plastics industry. The report also examines technological adoption in smart factories, high-speed production lines, and coextrusion strategies that balance regulatory compliance with performance, offering stakeholders a comprehensive perspective on growth drivers, risks, and opportunities.

Scope Highlights:

- Segmentation: By Resin Type (Polyethylene, Polypropylene, Polyvinyl Chloride, Polystyrene, Other Resins); By Process Type (Profile Extrusion, Sheet Extrusion, Blown Film Extrusion, Pipe & Tubing Extrusion, Fiber Extrusion); By Application (Packaging, Building & Construction, Automotive, Electrical & Electronics, Medical, Other Applications)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Historical & Forecast Data: Historic data from 2021 to 2024 and forecast data from 2025 to 2034

- Companies Covered: Analysis/profiles of 15+ companies, including Dow Chemical Company, LyondellBasell Industries, ExxonMobil Corporation, SABIC, Sinopec Corp., Formosa Plastics, Braskem S.A., REHAU AG, Pexco, JM Eagle, Solvay S.A., Mitsubishi Chemical, DuPont, Westlake Chemical, and Avient Corporation

Methodology

This report leverages a combination of primary and secondary research to provide an authoritative view of the extruded plastics market. Primary research included consultations with extrusion engineers, production managers, sustainability specialists, and R&D directors to validate trends in recycled-content integration, high-barrier monomaterial solutions, and precision medical extrusion. Secondary sources included corporate filings, industry whitepapers, patent databases, government regulations, and academic studies to track technology adoption, capacity expansions, mergers, and environmental compliance. Market sizing and forecasts were generated using top-down and bottom-up approaches, accounting for resin consumption, process-specific demand, and application-level growth across regions. Competitive benchmarking examined innovation in extrusion equipment, multi-layer films, and circular economy initiatives. USDAnalytics applied cross-validation and triangulation to ensure accuracy, offering industry professionals insights to enhance operational efficiency, regulatory compliance, and strategic decision-making in both mature and emerging extrusion markets.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.