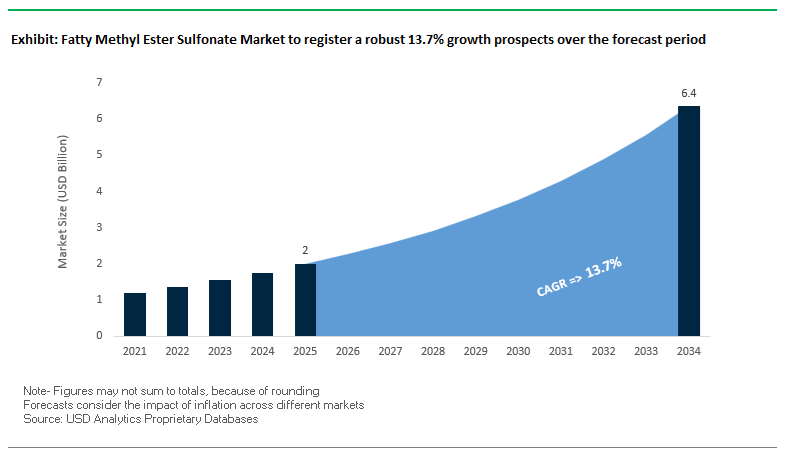

Fatty Methyl Ester Sulfonate (MES) Market Size to Reach $6.4 Billion by 2034 Driven by Bio-Based Surfactant Demand

The Global Fatty Methyl Ester Sulfonate (MES) Market is witnessing strong momentum as industries increasingly shift toward bio-based surfactants, sustainable detergent formulations, and renewable cleaning ingredients. The market is projected to grow from $2 billion in 2025 to $6.4 billion by 2034, expanding at a CAGR of 13.7% during the forecast period. This growth is primarily driven by the rising demand for biodegradable surfactants in household detergents, industrial cleaning solutions, and personal care products, combined with stricter environmental regulations encouraging the replacement of petroleum-derived surfactants such as Linear Alkylbenzene Sulfonate (LAS). MES, derived mainly from vegetable oils such as palm oil and coconut oil, offers superior biodegradability and strong cleaning performance, making it a preferred ingredient in next-generation sustainable detergent formulations.

From a sustainability perspective, the renewable carbon efficiency of MES surfactants is a major factor accelerating adoption. Leading manufacturers such as KLK OLEO have achieved a Renewable Carbon Index (RCI) close to 1.0 for MES product lines including PALMFONATE, indicating that nearly 100% of the carbon content originates from renewable vegetable feedstocks. Regulatory frameworks are also reinforcing MES demand. Under EU REACH Annex XVII biodegradability requirements, detergent surfactants must demonstrate at least 60% biodegradation within 28 days, a threshold consistently exceeded by MES. Additionally, formulation studies indicate that MES blended with alcohol ether sulfates can reduce skin irritation levels by approximately 20% to 30%, making it highly suitable for sensitive skin detergents, baby care products, and natural personal care formulations. On the production side, advanced sulfonation technologies introduced between 2024 and 2025 have reduced global production costs for bio-based surfactants by approximately 3.2%, improving the economic competitiveness of MES against petrochemical alternatives.

Market Analysis: Industry Developments and Strategic Expansion in the MES Ecosystem

The Fatty Methyl Ester Sulfonate market is undergoing significant transformation driven by capacity expansion, supply chain integration, and regulatory-driven reformulation strategies across the global surfactant industry. One of the key market developments occurred in February 2026, when KLK OLEO established a new representative office in Mumbai, India, aiming to strengthen its presence in the rapidly expanding Indian home care and industrial cleaning markets, where demand for plant-based surfactants and sustainable detergent ingredients is accelerating. In the same month, the U.S. Environmental Protection Agency updated its Safer Choice ingredient list to include several MES-derived surfactants, providing detergent manufacturers in North America with stronger regulatory alignment and eco-labeling advantages.

Product innovation and manufacturing investments in 2025 further accelerated market adoption. In October 2025, Hindustan Unilever launched a glycolipid and MES-based handwash product line in India, which quickly gained traction among environmentally conscious consumers and highlighted the growing retail demand for biodegradable surfactant systems. In September 2025, Croda International inaugurated a bio-based surfactant joint venture facility in Shanghai, China, designed to support the rapidly expanding clean beauty and sustainable skincare markets, where high-purity MES surfactants are increasingly utilized in facial cleansers and specialty formulations. Additionally, in August 2025, Wilmar International acquired a 50% stake in PZ Wilmar (Nigeria) to strengthen its upstream palm oil supply chain, ensuring stable feedstock availability for downstream MES production.

Strategic sustainability initiatives and regulatory changes are also reshaping market dynamics. In June 2025, Lion Corporation joined the Japan Sustainable Palm Oil Network (JaSPON) as part of its Lion Eco-Challenge 2050 initiative, committing to expanded use of RSPO-certified MES in carbon-neutral laundry detergents. Earlier in April 2025, KLK Emmerich GmbH acquired Temix Oleo in Italy, significantly expanding its fatty methyl ester sulfonates and specialty esters portfolio while strengthening distribution across the European surfactant market. Regulatory transparency requirements are also driving formulation changes. In January 2025, California’s Cleaning Product Right to Know Act came into full effect, compelling consumer brands to disclose detergent ingredients and accelerating the replacement of synthetic sulfonates with plant-based MES surfactants to support clean-label claims. Earlier developments in August 2024 saw Henkel Adhesives Technologies report strong growth in its laundry and home care segment in India, attributing performance gains to increased adoption of sustainable surfactant technologies including MES. Similarly, in May 2024, Vantage Specialty Chemicals announced a capacity expansion at its Leuna, Germany facility focused on bio-based surfactant chemistries to meet tightening European environmental standards for industrial cleaning products.

Trends and Opportunities in the Fatty Methyl Ester Sulfonate (MES) Market

Strategic Capacity Expansion for High-Growth Detergent Markets in Asia-Pacific

Asia-Pacific remains the structural growth engine for MES, supported by rising urbanization, expanding middle-class consumption, and policy support for bio-based surfactants. To capture this demand, major oleochemical producers are commissioning world-scale MES facilities close to palm oil feedstock sources, improving cost control and supply security.

In 2024–2025, KLK OLEO expanded its PALMFONATE MES portfolio by leveraging vertically integrated operations across Malaysia and Indonesia. With 16 operating facilities supplying more than 120 countries, KLK OLEO has significantly reduced exposure to feedstock price volatility, a historical bottleneck for MES scale-up. This integration enables stable pricing for detergent manufacturers in cost-sensitive emerging markets.

A parallel transition is underway at the brand-owner level. Lion Corporation, in its May 2025 Integrated Report, reaffirmed its Vision2030 strategy centered on plant-based surfactants. Lion has progressively replaced petroleum-derived Linear Alkylbenzene Sulfonate with MES in laundry powders, reporting 30 to 50% higher detergency performance in hard-water regions such as Southeast Asia and India. This performance advantage is critical in markets where water hardness routinely degrades conventional anionic surfactants.

From a cost and logistics perspective, MES is gaining traction in compact and concentrated detergent formats. Technical benchmarks from late 2025 indicate that MES-based formulations achieve equivalent stain removal at lower dosages, enabling FMCG leaders such as Procter & Gamble to reduce packaging material usage and transportation costs while maintaining cleaning efficacy.

Reformulation of Clean Label Household Cleaners to Replace Harsh Anionics

Consumer-driven demand for mild, sulfate-free cleaning products is reshaping household and personal care formulations. MES is increasingly positioned as a skin-compatible anionic surfactant capable of replacing Sodium Lauryl Sulfate and Sodium Laureth Sulfate without compromising foam quality or grease removal.

In early 2025, the “gentle cleaning” segment expanded rapidly across hand dishwashing liquids and multi-purpose cleaners. MES is being marketed as a low-irritation surfactant that delivers a smooth, dense lather, aligning with growing sensitivity to skin health and long-term exposure concerns. This shift is reinforced by environmental performance. MES is fully biodegradable and exhibits lower aquatic toxicity than petrochemical surfactants, supporting corporate sustainability commitments.

By December 2025, consumer research indicated that more than four-fifths of global buyers expect visible environmental responsibility from brands. As a result, MES has become a core ingredient in green product portfolios, enabling manufacturers to justify premium pricing while meeting eco-label criteria.

From a formulation standpoint, scientific advances have removed historical limitations. Research published in the Journal of Colloid and Interface Science in 2024 showed that MES performance below its Krafft point can be significantly improved through mixed micellar systems. This has enabled stable liquid detergent formulations optimized for cold-water washing, an increasingly important feature as energy-efficient laundering becomes standard.

High-Active, Low-Dust MES for Industrial and Institutional Cleaning

The Industrial and Institutional cleaning segment is transitioning toward solid and highly concentrated formats to reduce water transport and storage inefficiencies. This shift creates a high-value opportunity for engineered MES flakes and powders with enhanced handling characteristics.

In mid-2025, suppliers focused on developing high-active MES powders exceeding 90% purity with low dust generation. These products are well suited for commercial laundry pods, dishwashing blocks, and institutional cleaners where dosing accuracy and operator safety are critical. MES’s inherent resistance to calcium and magnesium ions further strengthens its position in hospitality and healthcare cleaning, where hard water conditions often reduce surfactant effectiveness.

Compared to LAS, MES maintains detergency without forming insoluble residues, reducing reliance on chelating agents and lowering total formulation costs. Safety considerations are also influencing procurement decisions. By September 2025, safety audits highlighted a growing preference for flake and pelletized MES forms that minimize airborne dust during detergent manufacturing, improving compliance with workplace exposure standards.

Enhanced Oil Recovery Applications in Mature and High-Salinity Reservoirs

Beyond detergents, MES is emerging as a credible bio-based surfactant for chemical Enhanced Oil Recovery in mature oil fields. This application is gaining attention in regions with high-salinity reservoirs where conventional petroleum sulfonates underperform.

A December 2025 study published in ACS Physical Chemistry Au demonstrated that MES retains functionality in brines containing up to 700 mM sodium chloride and temperatures reaching 80°C. Under these conditions, MES-based formulations reduced oil–water interfacial tension to as low as 0.02 mN/m, effectively altering reservoir wettability and mobilizing trapped hydrocarbons.

Experimental data from late 2025 indicates recovery factors exceeding 28% in spontaneous imbibition tests, representing a robust improvement over traditional surfactants that often precipitate in harsh reservoir environments. This performance profile positions MES as both a technical and economic alternative for tertiary recovery.

In Indonesia and parts of the Middle East, governments are actively promoting palm-derived MES for EOR as part of broader energy security strategies. By substituting imported petrochemical surfactants with domestically produced oleochemicals, MES-based EOR aligns with cost containment goals while supporting greener oilfield chemistry.

Fatty Methyl Ester Sulfonate Market Share and Segmentation Insights

Palm Oil Dominates FMES Raw Material Supply Due to Cost Efficiency and Optimal Surfactant Fatty Acid Profile

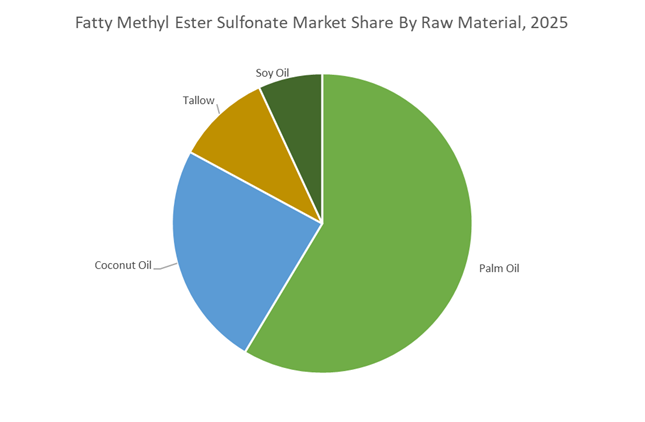

Palm oil accounted for 58.60% of the Fatty Methyl Ester Sulfonate (FMES) market raw material share in 2025, making it the leading feedstock for global FMES production. Palm-derived fatty acids provide the optimal balance of lauric and myristic acid chains, which are essential for producing high-performance anionic surfactants used in detergents, household cleaning products, and industrial cleaning formulations. Compared with other vegetable oils, palm oil offers superior oil yield per hectare, stable global supply chains, and lower feedstock production costs, allowing manufacturers to maintain competitive pricing for bulk surfactant ingredients. In 2025, the FMES supply chain has undergone a major transformation driven by sustainability commitments across the global home care and personal care industries. Large multinational detergent brands have pledged 100% sustainably sourced palm derivatives, resulting in more than 85% of palm oil used in FMES production now being RSPO-certified. Importantly, manufacturers are transitioning from mass balance sourcing toward segregated RSPO-certified supply chains, allowing traceable sustainability claims on finished cleaning products. This shift strengthens palm oil’s dominance in the fatty methyl ester sulfonate market, particularly in environmentally positioned detergents and eco-friendly surfactant formulations.

Technical Grade FMES Leads Market Volume Supported by Large-Scale Detergent and Industrial Cleaning Demand

Technical Grade Fatty Methyl Ester Sulfonate captured 64.80% of the global FMES market share in 2025, reflecting its dominant use across high-volume detergent, household cleaning, and institutional cleaning product manufacturing. Technical grade FMES provides the required surface-active performance, foaming properties, and biodegradability needed in laundry detergents, dishwashing liquids, and industrial cleaning formulations, while maintaining a lower production cost due to less stringent purity requirements compared with personal care grade materials. The economics of large-scale surfactant production strongly favor technical grade FMES, particularly for mass-market detergent brands and institutional hygiene solutions, where cost efficiency and functional performance outweigh ultra-high purity specifications. However, 2025 market dynamics reveal an important grade migration trend within the fatty methyl ester sulfonate industry. While technical grade continues to dominate overall volume, food and personal care grade FMES is emerging as the faster-growing premium segment, driven by rising demand for mild, biodegradable surfactants in skin care cleansers, shampoos, and eco-labeled personal care formulations. In response, leading FMES manufacturers are investing in advanced purification systems, higher-grade ester feedstocks, and food-grade certifications, enabling them to access higher-margin specialty applications within the expanding green surfactants market.

Competitive Landscape in Fatty Methyl Ester Sulfonate Market

KLK OLEO Leads the Global Fatty Methyl Ester Sulfonate Market Through Vertical Integration

KLK OLEO positions itself as the market leader in palm-based anionic surfactants. Its PALMFONATE product line—available in powder, flake, and paste formats—features high active matter levels (minimum 78% in powder grade) and strong calcium ion tolerance, making it highly suitable for heavy-duty laundry detergents and hard-water applications. The company’s competitive advantage lies in full vertical integration, spanning palm oil plantations to downstream MES production, ensuring cost control and supply chain stability amid volatile feedstock pricing. With a Renewable Carbon Index (RCI) of approximately 1.0, KLK OLEO emphasizes bio-based surfactant positioning aligned with global decarbonization trends. During 2025–2026, production optimization initiatives in Southeast Asia and the successful integration of Temix Oleo in Italy expanded its high-end oleochemical footprint in Europe, strengthening its presence in premium personal care surfactant formulations and industrial cleaning applications.

Lion Corporation Pioneers Carbon-Neutral MES Innovation in Asia

Lion Corporation remains a technological pioneer in methyl ester sulfonate commercialization, having developed the first continuous sulfonation process for Alpha-Olefin Sulfonates (AOS) before advancing MES manufacturing. The company focuses on high-purity MES and Methyl Ester Ethoxylates (MEE) derived entirely from renewable plant feedstocks, reinforcing its positioning in the carbon-neutral surfactant segment. Lion’s MES formulations are engineered for biodegradability, breaking down into water and CO₂, meeting Japan’s stringent sustainability mandates for 2030. Its proprietary IPMP (Isopropyl Methylphenol) delivery systems demonstrate formulation synergy with MES in oral care and hygiene applications, particularly targeting biofilm penetration. Strategically, Lion’s “Localization with Global Brands” model enables tailored detergent formulations across more than eight Asian markets, accounting for regional variations in water hardness and consumer washing habits. Capacity expansion in plant-derived surfactants further strengthens its footprint in sustainable detergent chemistry.

Wilmar International Controls Feedstock Supply in the Global MES Value Chain

Wilmar International leverages its position as one of the world’s largest palm oil refiners to exert significant influence over the Fatty Methyl Ester Sulfonate raw material supply chain. Its WILFAMES product line, including C16 and C12–18 cuts, serves large-scale detergent manufacturers, with the PR-10 powder grade recognized for its free-flowing characteristics and consistent off-white anionic surfactant profile. Wilmar’s port-side manufacturing model enhances global export capabilities, enabling bulk shipments via ISO tanks and flexibags with reduced lead times. In June 2025, the move to acquire a 50% interest in PZ Wilmar in Nigeria strengthened its strategic foothold in African feedstock sourcing and downstream surfactant distribution. The company’s MES is widely used in household laundry powders, dishwashing liquids, and agricultural adjuvants, reinforcing its scale-driven dominance across emerging markets with high detergent consumption growth.

Stepan Company Targets Specialty and Low-VOC MES Applications in North America

Stepan Company operates as a premium-focused player in the North American Fatty Methyl Ester Sulfonate market, strategically transitioning from commodity surfactants toward high-value specialty applications. Under its “Safe and Sustainable by Design” framework, Stepan emphasizes low-VOC MES grades suitable for personal care formulations and agricultural chemicals. The commissioning of a new alkoxylation facility in Pasadena, Texas in early 2025 significantly enhanced its capability to manufacture complex MES blends and specialized liquid formulations. Stepan is concurrently investing in fermentation-based biosurfactants to complement its existing methyl ester sulfonate portfolio, aligning with tightening environmental compliance standards in the United States and Europe. With all European manufacturing sites achieving ISCC PLUS certification, the company strengthens its sustainable sourcing credentials while maintaining strong R&D capabilities that differentiate it in specialty detergent and performance surfactant applications.

Zanyu Technology Group Expands China’s Dominance in Industrial-Grade MES Production

Zanyu Technology Group dominates China’s domestic MES production landscape. The company specializes in high-volume, cost-competitive industrial-grade MES in powder and liquid forms, primarily serving the mass-market detergent sector. Benefiting from China’s substantial household detergent consumption and national “Green Chemistry” initiatives, Zanyu receives policy support aimed at replacing petroleum-based surfactants with bio-based alternatives such as palm-derived methyl ester sulfonates. Its strategic shift toward specialty transition focuses on resolving low-temperature stability challenges—an ongoing technical limitation for MES in liquid detergent systems. By investing in advanced formulation R&D, Zanyu aims to improve cold-water solubility and broaden adoption in concentrated liquid detergents. Simultaneously, expanded export capacity targeting Southeast Asia and the Middle East enables the company to leverage manufacturing scale while strengthening its footprint in high-growth emerging markets.

Malaysia: World-Scale Oleochemical Expansion and RSPO-Led FMES Leadership

Malaysia continues to anchor the global Fatty Methyl Ester Sulfonate market through scale, feedstock security, and sustainability-led differentiation. In mid-2025, KLK OLEO completed a major expansion of its oleochemical processing assets, lifting total annual output capacity to approximately 500,000 tons. This expansion directly strengthens the upstream availability of high-purity methyl esters required for FMES production, positioning Malaysia as a primary supply hub for detergent manufacturers across Asia Pacific and Europe. The scale advantage is particularly relevant as global formulators increasingly replace petroleum-based anionic surfactants with bio-based alternatives to meet biodegradability and carbon-reduction targets.

Sustainability credentials are reinforcing Malaysia’s competitive position. In July 2025, RAM Sustainability upgraded Kuala Lumpur Kepong Berhad’s sustainability rating to Gold1 (G1), reflecting strong traceability and RSPO-certified palm feedstock integration. This is critical for FMES buyers in Europe and Japan, where supply chain transparency has become a non-negotiable procurement criterion. Product innovation is also accelerating. At VietnamPlas 2025 and K 2025, Malaysian producers showcased Palmere fractionated methyl esters designed to deliver low-discoloration FMES with improved detergency and hard-water stability. These performance gains support the transition of FMES from cost-driven substitution to premium detergent formulations.

India: Policy-Driven Biomanufacturing and FMCG-Led FMES Adoption

India’s FMES market is being reshaped by coordinated policy support, domestic feedstock strategies, and downstream FMCG adoption. The approval of the BioE3 Policy has catalyzed India’s high-performance biomanufacturing ecosystem, explicitly favoring bio-based surfactants such as FMES. Government-backed BioEnablers and Biomanufacturing Hubs are enabling the scale-up of sulfonation and esterification technologies, reducing dependence on imported surfactant intermediates and supporting domestic value creation across the detergent supply chain.

Feedstock security is emerging as a decisive factor. Under the National Mission on Edible Oils – Oil Palm, domestic palm oil production targets have increased, and early progress in 2025 has encouraged Indian surfactant producers to pivot toward FMES as a strategic alternative to imported Linear Alkylbenzene Sulfonate. This structural shift is reinforced by downstream demand. Major Indian FMCG players integrated FMES into premium detergent launches in 2025, leveraging its cold-water solubility, skin mildness, and plant-based origin to appeal to urban consumers seeking clean-label and sustainability-aligned household products. As a result, FMES is transitioning from niche bio-surfactant status to a mainstream formulation component in India.

United States: Regulatory Preference and Strategic Refocusing Toward Biodegradable Anionics

In the United States, the FMES market is benefiting from a combination of regulatory tailwinds and strategic realignment by surfactant producers. Following the divestment of its specialty esters business in 2024, Stepan Company refocused its 2025–2026 capital allocation toward core surfactant operations. This includes optimization of production lines for biodegradable anionic surfactants such as FMES, particularly for oilfield chemicals and agricultural formulations where environmental scrutiny is intensifying.

Trade dynamics are also influencing sourcing behavior. In early 2025, anticipatory procurement ahead of potential tariff escalations drove a measurable increase in domestic surfactant sales volumes. This environment has incentivized U.S. detergent and industrial formulators to secure long-term supply agreements for domestically produced bio-surfactants. Regulatory alignment further strengthens FMES adoption. Under the evolving EPA SNAP framework for 2026, FMES is increasingly positioned as a Safer Choice ingredient, particularly in concentrated liquid laundry detergents where petroleum-derived surfactants face rising regulatory and reputational risk.

China: Oleochemical Localization and Carbon-Driven Surfactant Transition

China’s FMES market trajectory is closely tied to oleochemical localization and provincial decarbonization mandates. KLK OLEO expanded its processing footprint in Zhangjiagang during 2024–2025, creating a strategically located hub for supplying high-purity methyl esters to China’s detergent manufacturers. This localization reduces logistics intensity and supports just-in-time sulfonation for large-scale FMCG producers.

Policy pressure is accelerating substitution trends. Under the Ministry of Industry and Information Technology’s 2025–2026 Work Plan emphasizing green growth, detergent plants in Zhejiang and Jiangsu are actively transitioning away from LAS toward plant-based FMES to comply with regional carbon-neutrality targets. This shift is not only regulatory but also economic, as integrated oleochemical supply chains reduce exposure to volatile petrochemical pricing. FMES is therefore becoming a core component of China’s low-carbon household care manufacturing strategy.

Germany and the European Union: Compliance Economics and Net-Zero Product Alignment

Across Germany and the wider European Union, FMES adoption is being shaped by regulatory compliance economics and corporate net-zero commitments. In 2025, Evonik ramped up industrial-scale production of rhamnolipid biosurfactants at its Slovenská Ľupča site. While rhamnolipids represent a different surfactant class, their commercialization has created a halo effect that accelerates interest in bio-based anionic surfactants such as FMES across European formulation houses.

Process optimization is also improving FMES competitiveness. German manufacturers are implementing closed-loop water and effluent systems to comply with tightening EU chemical safety standards, with these upgrades projected to reduce FMES production costs by around 20% compared with 2024 baselines. At the brand level, companies such as Henkel have expanded carbon-neutral production across multiple sites, increasing demand for FMES as a key ingredient in net-zero detergent and home care product lines.

Strategic Snapshot: Fatty Methyl Ester Sulfonate Market by Country (2025–2026)

Fatty Methyl Ester Sulfonate Market County Level Snapshot

|

Country / Region

|

Core Strategic Driver

|

Key End-Use Pull

|

Market Implication

|

|

Malaysia

|

World-scale oleochemical capacity and RSPO compliance

|

Detergents, export markets

|

Global supply anchor for sustainable FMES

|

|

India

|

BioE3 policy and palm oil self-sufficiency

|

FMCG detergents

|

Rapid mainstreaming of FMES formulations

|

|

United States

|

Regulatory preference and domestic sourcing

|

Laundry, oilfield, agriculture

|

Stable growth for biodegradable anionics

|

|

China

|

Green growth mandates and oleochemical localization

|

Mass-market detergents

|

Structural shift from LAS to FMES

|

|

Germany / EU

|

REACH compliance and net-zero targets

|

Home care, industrial cleaners

|

Cost-optimized, carbon-aligned FMES demand

|

Fatty Methyl Ester Sulfonate Market Report Scope

Fatty Methyl Ester Sulfonate Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2 Billion

|

|

Market Size (2034)

|

$6.4 Billion

|

|

Market Growth Rate

|

13.7%

|

|

Segments

|

By Raw Material (Palm Oil, Coconut Oil, Tallow, Soy Oil), By Grade (Technical Grade, Food and Personal Care Grade), By Form (Powder, Granular, Liquid), By Application (Household Detergents, Personal Care, Industrial and Institutional Cleaning, Oilfield Chemicals, Agrochemicals, Leather and Textiles)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Lion Corporation, KLK Oleo, Wilmar International Ltd, Stepan Company, Zanyu Technology Group Co., Ltd., Huish Detergents Inc., Jinchang Chemicals, Chemithon Corporation, Emery Oleochemicals, Sinopec Jinling Petrochemical, Marathon Isotech, Jiangsu Haiqing Biotechnology, Ecogreen Oleochemicals, KPL International Ltd, Guangzhou Keyun Chemicals

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fatty Methyl Ester Sulfonate Market Segmentation

By Raw Material

- Palm Oil

- Coconut Oil

- Tallow

- Soy Oil

By Grade

- Technical Grade

- Food and Personal Care Grade

By Form

By Application

- Household Detergents

- Personal Care

- Industrial and Institutional Cleaning

- Oilfield Chemicals

- Agrochemicals

- Leather and Textiles

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Fatty Methyl Ester Sulfonate Industry

- Lion Corporation

- KLK Oleo

- Wilmar International Ltd

- Stepan Company

- Zanyu Technology Group Co., Ltd.

- Huish Detergents Inc.

- Jinchang Chemicals

- Chemithon Corporation

- Emery Oleochemicals

- Sinopec Jinling Petrochemical

- Marathon Isotech

- Jiangsu Haiqing Biotechnology

- Ecogreen Oleochemicals

- KPL International Ltd

- Guangzhou Keyun Chemicals

*- List not Exhaustive