Market Overview: Flexible Paper Packaging Market to Reach $116.5 Billion by 2034 at 4.5% CAGR

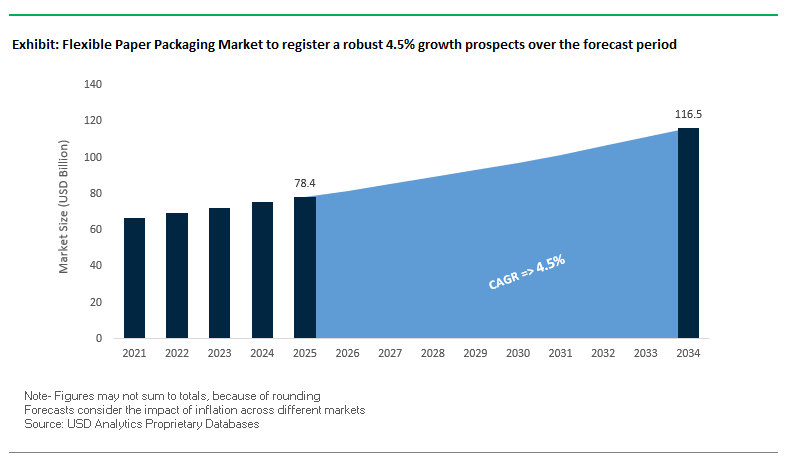

The global flexible paper packaging market is projected to expand from $78.4 billion in 2025 to $116.5 billion by 2034, growing at a steady CAGR of 4.5%. The market is defined by its printability, lightweighting, recyclability, and barrier performance, making it a preferred choice for industries seeking sustainable alternatives to plastics. Its importance has accelerated in e-commerce, food service, fast-moving consumer goods (FMCG), and retail, where cost, sustainability, and consumer perception play a pivotal role.

For buyers and industry professionals, the market answers key questions on sustainability, operational efficiency, and innovation readiness, positioning flexible paper packaging as both a cost-effective and environmentally responsible solution.

Key Insights for Industry Stakeholders:

- E-commerce Catalyst: Online retail growth is driving demand for lightweight recyclable mailers and void-fill paper packaging.

- Barrier Innovations: Bio-based and PFAS-free coatings are extending paper packaging use into moisture- and grease-sensitive categories.

- Circularity Commitment: Major players are pledging 100% recycled or responsibly sourced fibers, aligning with global ESG goals.

- Production Efficiency: Technologies like PulPac dry molded fiber deliver cycle times as fast as 3.76 seconds, producing 23,000 fiber lids/hour, reducing energy and CO₂ emissions.

Market Analysis: Strategic Expansions, Material Innovation, and E-commerce Growth

The flexible paper packaging industry has witnessed significant corporate moves and product launches that highlight its rapid transformation.

In August 2025, Mondi introduced its Ad/Vantage Smooth Brown Semi Extensible paper for industrial use and simultaneously ramped up production of its FunctionalBarrier Paper Ultimate, addressing rising demand for sustainable high-barrier packaging. In the same month, Ranpak secured its second major e-commerce deal in 2025, strengthening its position as a key supplier of void-fill and paper mailer solutions to global online retailers.

The consolidation trend is reshaping the market landscape. In July 2025, International Paper completed a $9.9 billion acquisition of DS Smith, expanding its European footprint and reinforcing its corrugated and fiber packaging dominance. A month earlier, Mondi collaborated with Saga Nutrition (June 2025) to launch a sustainable pet food solution, while Ahlstrom (May 2025) expanded its specialty materials portfolio by acquiring the Stevens Point operation in the U.S., adding expertise in life sciences and high-performance applications.

Innovation remains a cornerstone. In April 2025, Billerud launched a formable fiber-based material to replace plastics in select applications, while DS Smith (March 2025) opened a new R&D and innovation center in Birmingham, UK, designed to accelerate “radically new” packaging solutions. These moves confirm the industry’s dual focus on technological development and circularity, making flexible paper packaging central to the global transition away from plastics.

Emerging Trends and Growth Opportunities in the Flexible Paper Packaging Market

Advanced Coating and Barrier Technology Development for Plastic Replacement

One of the most significant trends shaping the flexible paper packaging market is the rapid development and commercialization of high-performance barrier coatings that allow paper to effectively replace multi-layer plastics. With global regulations tightening around single-use plastics and PFAS “forever chemicals,” brand owners are investing in scalable paper-based solutions that can deliver moisture, grease, and oxygen resistance without contaminating recycling streams.

Companies like Solenis are leading this transformation through innovations such as TopScreen™ and EarthGuard™ water-based coatings, which provide oil, grease, and water resistance while being recyclable, repulpable, and compostable. These coatings function as drop-in solutions, enabling converters to transition away from plastic films without significant retooling costs. Academic research is reinforcing these advancements by demonstrating how cellulose nanocrystals and chitosan-based coatings can enhance oxygen and water vapor resistance, making paper suitable for sensitive food products. In parallel, packaging majors like Toppan are commercializing hybrid solutions that merge proprietary GL Barrier film technology with paper substrates, setting a benchmark for functional yet sustainable packaging. This shift illustrates how paper is evolving from a structural medium into a high-performance substrate capable of replacing traditional plastics in demanding applications.

Integration of Digital Watermarks for Automated Sorting and Recycling

Another transformative trend is the integration of digital watermarks into flexible paper packaging to enable next-generation recycling efficiency. The HolyGrail 2.0 initiative, a pan-industry collaboration, has proven that nearly invisible codes embedded in packaging can be detected by high-resolution cameras at recycling facilities. Industrial trials consistently achieved detection rates above 90% and high purity in sorted streams, showcasing the potential to elevate recycling outcomes for fiber-based composites.

Unlike traditional near-infrared (NIR) sorting, digital watermarks carry a “digital passport” for each package, embedding data such as material type, food vs. non-food grade classification, and adhesive or coating content. This granularity allows recyclers to create high-quality fiber streams suitable even for food-grade applications, directly supporting EU PPWR mandates and corporate recycled-content goals. Major packaging converters such as Wipak and Greiner Packaging are actively piloting this technology, demonstrating a clear trajectory toward industry-wide adoption. Beyond recycling, digital watermarks also offer consumer-facing benefits, enabling traceability and brand transparency while enhancing end-of-life value streams.

Development of Functional Paper-Based Pouches for Liquid and Viscous Products

A significant white space exists in the replacement of plastic laminate pouches for liquids, sauces, and viscous goods with paper-based alternatives. Historically, pouches for condiments, beverage refills, and detergents have relied on multi-layer plastic laminates to achieve leak resistance and barrier performance, but new innovations in kraft-paper-based and bio-coated pouches are bridging this gap.

Some companies are now commercializing heat-sealable, spout-compatible paper pouches that maintain structural integrity and leak resistance, making them suitable for beverages, soups, or personal care liquids. This development could substantially reduce the plastic footprint of one of the highest-volume categories in flexible packaging. Research is also progressing in the formulation of bio-based coatings and thin-film technologies to enhance durability during transportation without compromising recyclability. Successful deployment of these products could transform packaging for everyday items, cutting millions of tonnes of plastic waste annually while giving brands a strong sustainability-driven differentiation in crowded markets.

Establishment of Closed-Loop Collection and Recycling Infrastructure for Paper-Based Composites

While demand for fiber-based flexible packaging is accelerating, the recycling infrastructure often lags behind, especially for coated or composite paper packaging. This creates a critical opportunity for the industry to establish dedicated take-back systems, advanced mechanical sorting, or chemical recycling processes tailored to paper composites.

Mechanical recycling often weakens fibers, limiting reuse potential. Advanced processes such as solvent-based separation and fiber recovery can recapture high-quality fiber suitable for remanufacturing. Pilot projects led by packaging coalitions and recyclers are already demonstrating the economic viability of such systems. Building a closed-loop infrastructure for coated paper packaging ensures that the material delivers on its sustainability promise, turning what would otherwise be a landfill-bound waste stream into a valuable secondary raw material. For brands, investing in or partnering with such initiatives strengthens compliance with EPR mandates while securing future-ready, sustainable packaging supply chains.

Competitive Landscape: Sustainability and Innovation Driving Competitive Advantage

The flexible paper packaging market is moderately consolidated, with global leaders differentiating through innovation, strategic mergers, and sustainability-driven roadmaps.

Mondi plc Leading Innovation in High-Barrier Flexible Papers

Mondi is a global packaging leader with a broad portfolio of kraft paper, functional papers, and industrial bags. Recent launches include Ad/Vantage Smooth Brown Semi Extensible and the FunctionalBarrier Paper Ultimate, positioned as recyclable alternatives to plastics. Its MAP2030 sustainability strategy drives “sustainable by design” innovations. Mondi’s vertically integrated network from forestry to finished packaging ensures consistent supply chain reliability and quality control.

Smurfit Kappa Group Expanding Global Reach Through WestRock Merger

Smurfit Kappa is a global pioneer in corrugated and paper-based packaging, with growing penetration into flexible paper applications. The company is completing a merger with WestRock, creating a global leader in sustainable packaging. Known for innovation, Smurfit Kappa has introduced recyclable void-fill packing papers, offering an alternative to bubble wrap. Its Experience Centres strengthen customer collaboration by simulating supply chain impact.

Billerud Innovating Formable Fiber Materials as Plastic Alternatives

Billerud provides high-performance kraft papers and specialty materials for flexible packaging, including heat-sealable papers. The company’s innovation focus is evident in its new formable fiber-based material (April 2025), designed to directly replace certain plastic applications. Its sustainability-first strategy includes using 100% primary fibers for durability and food safety, while expanding offerings for barrier-coated and metallizable paper packaging.

International Paper Strengthening European Presence Through DS Smith Acquisition

International Paper, a U.S.-based multinational, has consolidated its leadership by acquiring DS Smith for $9.9 billion (July 2025). This move enhances its European operations and strengthens its corrugated and paperboard portfolio. The company also invested $250 million in converting its Riverdale mill to containerboard production to meet e-commerce demand. International Paper continues to emphasize high-performance sustainable packaging while exiting non-core cellulose fibers to focus on higher-margin fiber packaging solutions.

WestRock Company Driving Innovation and Facility Expansion

WestRock offers a wide range of corrugated, consumer packaging, and paperboard solutions. The company is in the process of merging with Smurfit Kappa, which will create an unrivaled global footprint. Recent investments include a $47 million expansion at its North Carolina facility, increasing capacity for sustainable paper packaging. WestRock is recognized for innovations such as CanCollar®, a recyclable paper-based multipack solution, and Meta® Systems, enhancing equipment flexibility and packaging strength.

Flexible Paper Packaging Market Share Insights

Pouches Lead Market Share by Packaging Type in Flexible Paper Packaging

In flexible paper packaging, pouches hold the top share at 35% in 2025, spearheading plastic replacement with paper-led laminates and bio-barrier innovations that preserve shelf life for snacks, coffee, and pet food while unlocking superior shelf appeal and lightweight logistics. Bags & sacks at 30% scale on the back of plastic-bag bans and upgraded wet-strength handles for retail carry-out and industrial multi-wall applications. Wraps expand as fresh-food protectors where breathability reduces condensation and supports natural aesthetics, while roll stock represents the manufacturing backbone feeding FFS lines at FMCG majors and accelerating at-source sustainability shifts. Liners retain a smaller, performance-critical niche grease/moisture barriers inside boxes and crates for frozen and prepared foods. Overall, packaging-type share tracks material-efficiency gains, barrier-coating advances, and policy-driven plastic substitution.

Food & Beverages Drive Market Share by End-Use Industry in Flexible Paper Packaging

End-use demand is overwhelmingly led by food & beverages at 60% share in 2025, where brands pursue circular-economy goals via recyclable paper structures, PFAS-free/repulpable barriers, and downgauged formats without compromising product integrity. Retail & e-commerce at 25% act as the visibility engine paper shopping bags, curbside-recyclable mailers, paper wraps, and void-fill make sustainability tangible for consumers and drive large-scale roll-outs. Personal care & cosmetics leverage paper pouches and wraps for premium, natural positioning, while healthcare & pharma adopt cautiously due to stringent moisture/sterility barriers remaining a frontier for next-gen coatings. This end-use split highlights how regulation, retailer mandates, and brand decarbonization targets consolidate share around F&B and retail logistics, channeling capex into high-speed paper converting and advanced functional coatings.

United States: Accelerating Shift Toward Sustainable Paper-Based Packaging

The U.S. flexible paper packaging market is undergoing a significant transformation as brands respond to consumer demand for sustainable, plastic-free solutions. Companies are increasingly transitioning from multi-material plastic laminates to paper-based alternatives for snacks, cereals, and dry goods, enhancing recyclability and appealing to eco-conscious consumers. Technological advancements are enabling manufacturers to produce high-barrier, flexible paper packaging with improved moisture and oxygen resistance, thereby extending the shelf life of food products.

Strategic acquisitions are strengthening supply chains, exemplified by Novolex’s acquisition of a paper handle manufacturer, enhancing capabilities in the paper bag and sack segment. Furthermore, the rapid expansion of e-commerce is driving demand for durable, lightweight, and protective paper-based mailers, pouches, and wraps, providing safe shipping solutions while supporting sustainability initiatives.

Germany: Driving Europe’s Circular Economy with Innovative Paper Solutions

Germany’s flexible paper packaging industry is a pivotal player in Europe’s circular economy, shaped by stringent regulations under the VerpackG (Packaging Act) that enforce high recycling targets. Companies are focusing on developing paper-based packaging with advanced barrier properties capable of replacing multi-material plastic films. Technologies such as Dry Fiber systems are enabling deep-drawn trays and containers for food applications, reducing plastic use while saving energy and water compared to traditional wet-molded pulp processes.

Strategic investments are fueling capacity expansion and innovation. For example, DS Smith invested over $52.91 million in its packaging facilities in Portugal, reflecting the company’s efforts to meet growing European demand for sustainable fiber-based packaging. Germany’s market leadership is strengthened by combining regulatory compliance, material innovation, and investment in high-performance paper solutions.

China: Leveraging E-commerce and Policy Initiatives to Expand Paper Packaging

China is a global hub for flexible paper packaging, driven by its massive e-commerce sector and manufacturing capacity. The need for lightweight, protective, and sustainable packaging for online retail is a major growth driver. Chinese companies are investing in digital printing and automated production lines to deliver customized packaging efficiently, meeting the high-volume demands of both domestic and international markets.

Government policies targeting plastic pollution control and environmental compliance are accelerating the adoption of sustainable paper-based alternatives. These measures are pushing businesses to transition from conventional plastic packaging to eco-friendly flexible paper solutions, enhancing recyclability and sustainability.

India: Rapid Market Expansion Fueled by “Make in India” and Sustainability Regulations

The Indian flexible paper packaging market is experiencing rapid growth due to the Make in India initiative and the expansion of e-commerce. Rising consumer demand for packaged goods and the expanding middle class are key drivers. Regulatory mandates, such as EPR and plastic waste management rules, are compelling companies to integrate paper-based solutions and use a minimum of 10% post-consumer recycled (PCR) content in flexible packaging by 2025.

Strategic investments in local manufacturing are enabling companies to meet rising demand. For instance, leading printing ink firms are expanding innovation hubs and production facilities to support the growing market for sustainable flexible paper packaging, reinforcing India’s position as a key player in environmentally responsible packaging solutions.

Brazil: Harnessing Forest Resources and Innovation for Sustainable Paper Packaging

Brazil’s flexible paper packaging industry benefits from its robust forest-based resources, providing a sustainable raw material base for paper and paperboard production. Companies are innovating to produce high-performance paper alternatives, such as Klabin’s first flexible packaging paper, which replaces traditional plastics across multiple industries, including food.

Compliance with environmental regulations is driving the development of recyclable and repulpable paper packaging solutions, aligning with both domestic and international sustainability standards. Brazil’s industry is increasingly focused on eco-friendly innovation, regulatory adherence, and leveraging local raw materials to meet growing consumer and industrial demand for sustainable packaging.

Japan: Pioneering High-Performance and Biodegradable Paper Packaging Solutions

Japan’s flexible paper packaging market is characterized by high-quality, high-performance paper materials. Innovations like Nippon Paper Industries’ SHIELDPLUS offer barrier properties comparable to plastic films, making them suitable for food and pharmaceutical applications. The industry is increasingly adopting biodegradable and recyclable solutions, such as cellulose nanofiber (CNF) films, to reduce reliance on plastics.

Strategic collaborations, including partnerships with Mitsubishi Chemical Corporation, are accelerating the development of recyclable and sustainable paper packaging materials. Japanese companies are leading the global push to reduce plastic waste by combining advanced materials, high barrier properties, and innovative production methods to deliver sustainable packaging solutions for both domestic and international markets.

Flexible Paper Packaging Market Report Scope

Flexible Paper Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$78.4 Billion

|

|

Market Size (2034)

|

$116.5 Billion

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Paper Grade (Kraft Paper, Coated Paper, Greaseproof Paper, Parchment Paper, Other Grades), By Packaging Type (Pouches, Bags & Sacks, Wraps, Liners, Roll Stock), By End-Use Industry (Food & Beverages, Retail & E-commerce, Personal Care & Cosmetics, Healthcare & Pharmaceuticals, Other Industries), By Printing Technology (Flexography, Rotogravure, Digital Printing, Other Printing Technologies)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

International Paper Company, Mondi Group, WestRock Company, DS Smith Plc, Smurfit Kappa Group plc, Huhtamaki Oyj, Klabin S.A., Graphic Packaging Holding Company, Rengo Co., Ltd., ProAmpac LLC, Sonoco Products Company, TC Transcontinental Inc., BillerudKorsnäs AB, Novolex Holdings, LLC, Greif, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Flexible Paper Packaging Market Segmentation

By Paper Grade

- Kraft Paper

- Coated Paper

- Greaseproof Paper

- Parchment Paper

- Other Grades

By Packaging Type

- Pouches

- Bags & Sacks

- Wraps

- Liners

- Roll Stock

By End-Use Industry

- Food & Beverages

- Retail & E-commerce

- Personal Care & Cosmetics

- Healthcare & Pharmaceuticals

- Other Industries

By Printing Technology

- Flexography

- Rotogravure

- Digital Printing

- Other Printing Technologies

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Flexible Paper Packaging Market

- International Paper Company

- Mondi Group

- WestRock Company

- DS Smith Plc

- Smurfit Kappa Group plc

- Huhtamaki Oyj

- Klabin S.A.

- Graphic Packaging Holding Company

- Rengo Co., Ltd.

- ProAmpac LLC

- Sonoco Products Company

- TC Transcontinental Inc.

- BillerudKorsnäs AB

- Novolex Holdings, LLC

- Greif, Inc.

*List not Exhaustive

Research Coverage

This USDAnalytics report investigates the evolving dynamics, technological breakthroughs, and strategic developments in the global Flexible Paper Packaging market. The analysis reviews innovations in high-performance barrier coatings, digital watermarking for enhanced recyclability, formable fiber-based pouches, and closed-loop recycling infrastructure, while highlighting corporate acquisitions, R&D expansions, and partnerships shaping competitive landscapes. This report is an essential resource for packaging engineers, sustainability managers, brand owners, and investors seeking actionable insights into market growth, regulatory compliance, and product innovation. Breakthroughs in PFAS-free, bio-based coatings and scalable paper alternatives to plastics underscore the market’s role in supporting circular economy initiatives and sustainability mandates. Additionally, the report evaluates historical trends from 2021 to 2024 and provides detailed forecasts through 2034, encompassing technological, operational, and commercial drivers, enabling stakeholders to make informed strategic, procurement, and investment decisions across global markets.

Scope Highlights:

- Segmentation: By Paper Grade (Kraft, Coated, Greaseproof, Parchment, Other), By Packaging Type (Pouches, Bags & Sacks, Wraps, Liners, Roll Stock), By End-Use Industry (Food & Beverages, Retail & E-commerce, Personal Care & Cosmetics, Healthcare & Pharmaceuticals, Other Industries), By Printing Technology (Flexography, Rotogravure, Digital Printing, Other Printing Technologies).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Timeframe: Historical data from 2021 to 2024; forecast data from 2025 to 2034.

- Companies: Profiles and analysis of 15+ leading manufacturers, including International Paper, Mondi, WestRock, DS Smith, Smurfit Kappa, Huhtamaki, Klabin, BillerudKorsnäs, and Novolex Holdings.

Methodology

This study employs a multi-layered research methodology combining primary interviews with industry stakeholders and secondary data from corporate reports, trade publications, government databases, and market intelligence platforms. USDAnalytics analyzed technological, operational, and regulatory trends to quantify historical market performance and forecast future growth. A hybrid approach of top-down and bottom-up modeling was applied to assess segmental performance across paper grades, packaging types, end-use industries, and printing technologies. Market sizing, share analysis, and competitive benchmarking were validated through expert consultations and statistical modeling, integrating macroeconomic indicators, production capacity, sustainability adoption rates, and e-commerce growth. Scenario analysis accounts for regulatory shifts, innovations in barrier coatings, digital watermark adoption, and closed-loop recycling initiatives, enabling actionable insights for supply chain optimization, product innovation, and strategic investment in the flexible paper packaging sector.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.