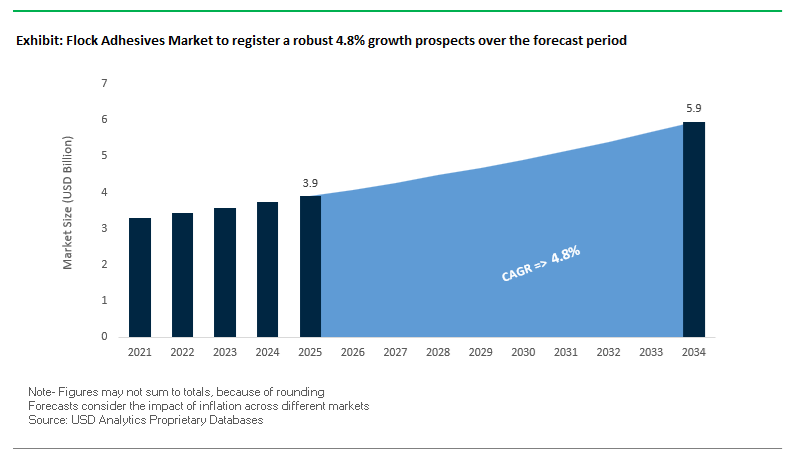

The Global Flock Adhesives Market is projected to expand from USD 3.9 billion in 2025 to USD 5.9 billion by 2034, advancing at a CAGR of 4.8%, as flocking evolves from a decorative finishing step into a functional surface-engineering process. Growth is structurally driven by automotive interior redesign, tighter emission regulations, and increasing automation of electrostatic flocking lines. OEMs are specifying flock adhesives not only for aesthetics, but for noise attenuation, abrasion resistance, and tactile performance, particularly in vehicle cabins, consumer products, and technical textiles. This shift is accelerating the transition away from solvent-based chemistries toward water-based and UV-curable polyurethane (PUR) and acrylic systems, which offer compliance with REACH and OEM cabin air quality standards while remaining compatible with high-speed, digitally controlled flocking equipment.

From a materials and OEM procurement standpoint, flock adhesives are evaluated against durability under cyclic stress, thermal stability, and long-term NVH performance, rather than initial bond strength alone. High-performance polyurethane flock adhesives specified in automotive interiors routinely deliver service lifetimes exceeding 10 years under repeated flexing, temperature cycling, and abrasion, supporting applications such as door seals, glove boxes, storage compartments, and soft-touch trims. In electric vehicles, where powertrain noise is largely eliminated, flocked surfaces bonded with acoustically optimized adhesives play a critical role in managing secondary noise and vibration paths, making flocking a functional NVH control layer rather than a cosmetic add-on. These performance requirements are driving material substitution, with flocked thermoplastic components increasingly replacing foamed plastics and mechanically fastened assemblies to reduce part count, weight, and assembly complexity.

Beyond automotive interiors, demand is broadening across technical textiles, filtration media, upholstery, and industrial workwear, where controlled fiber anchoring and wash or wear resistance are essential. Two-component epoxy-based flock adhesives, curing in the 80°C to 135°C range, are being adopted where rapid curing and high peel and shear strength are required for engineered fabrics. Overlaying these application trends is a clear sustainability pivot: Tier 1 suppliers and adhesive manufacturers are scaling bio-based polyurethane systems derived from plant-based polyols and acrylic backbones, alongside UV-curable flock adhesives that reduce energy consumption and line dwell time.

The past twelve months have marked a transformative period for the flock adhesives market, characterized by significant R&D breakthroughs, capacity expansions, and sustainability-driven policy changes that are reshaping material sourcing and production strategies.

In October 2024, H.B. Fuller Company announced an expansion of its Asia-Pacific water-based adhesive capacity, targeting growing demand in automotive textiles and consumer electronics. The move strategically positions Fuller to capture emerging market opportunities as OEMs accelerate the adoption of low-VOC and REACH-compliant flock adhesives. In December 2024, the European Union’s REACH authority reinforced these trends by issuing updated guidance on solvent restrictions in industrial adhesives, effectively mandating the phase-out of high-VOC solvent-based flocking systems across the EU. This regulatory milestone has fast-tracked the transition to UV-curable and aqueous polyurethane systems.

Entering 2025, BASF SE introduced a UV- and wash-resistant acrylic flock adhesive series (January 2025) designed for outdoor textiles and apparel, signaling a stronger focus on functional and durable textile coatings. Shortly after, the U.S. EPA (March 2025) announced its new emission reduction framework, tightening permissible VOC levels in coating and bonding operations — a development expected to further boost waterborne adhesive adoption in North America.

In May 2025, Henkel AG & Co. KGaA unveiled its breakthrough in UV-curable flock adhesive technology, capable of instantaneous curing under LED lamps while reducing energy consumption by up to 50% compared to conventional thermal curing. This innovation is particularly relevant for high-speed textile and packaging lines, where energy efficiency and throughput are critical.

By July 2025, Italian manufacturer CIM-JET S.r.l. expanded its global footprint through a partnership with a South American textile distributor, enhancing access to flocking machinery and adhesive dosing systems. This collaboration underlines a broader trend — the integration of chemistry and machinery to optimize fiber adhesion, adhesive uniformity, and sustainability.

Meanwhile, an emerging biomaterials firm (August 2025) announced a successful pilot of a plant-derived bio-based flock adhesive exhibiting superior abrasion resistance and flexibility, aligning with circular economy frameworks. Finally, in September 2025, a major European automotive OEM and a Tier 1 interior supplier entered into a landmark agreement to standardize a low-VOC, two-component PUR adhesive across all EV interior platforms — representing a pivotal shift toward sustainable and acoustically optimized flocking standards.

Evolving Sustainable Formulations and High-Performance Automotive Applications

Trend 1: Accelerated Shift Toward Water-Based and Solvent-Free Flock Adhesives Under Global VOC Regulations

The flock adhesives sector is undergoing a decisive transition toward water-based and solvent-free systems, driven by aggressive environmental regulations across Europe and North America that restrict VOC emissions and hazardous solvents like toluene. These policies not only target improved air quality but also eliminate the need for explosion-proof storage, solvent recovery units, and other safety infrastructure tied to solvent-borne adhesives. Technological advancements enable water-based acrylic adhesives to deliver bonding strength, abrasion resistance, and chemical durability comparable to high-performance solvent-based systems, making them viable for demanding applications such as textile flocking and automotive interior components. Leading suppliers such as Sika are supporting this shift by offering BTX-free formulations and hot-melt adhesives designed explicitly to meet OEM requirements for ultra-low interior emissions, fogging performance, and cabin air-quality compliance—critical considerations as automakers push for environmentally responsible, consumer-safe interiors.

Trend 2: Engineered Multi-Substrate Adhesives Enabling Next-Generation Automotive Interiors

As automotive designs evolve toward lightweight, soft-touch, and acoustically optimized interiors, flock adhesives must deliver high-performance bonds across complex, low-surface-energy materials including TPEs, TPVs, and PVC blends used in window channels, door seals, and interior trims. Research in polyurethane dispersions and water-dispersed polymer compositions demonstrates that properly engineered adhesion promoters can overcome the bonding challenges posed by these elastomeric substrates. Durability is also a defining requirement, as adhesives must withstand plasticizer migration—one of the primary causes of premature bond failure. High-resilience polyurethane systems, such as FA-808-type chemistries, are specifically designed to resist plasticizer attack and ensure adhesion stability over 10-year automotive lifecycles. In parallel, the adhesive’s ability to control flock thickness and uniformity plays a vital role in NVH performance, helping manufacturers reduce Buzz, Squeak & Rattle (BSR) and deliver the premium acoustic comfort expected in modern and electric vehicles.

Emerging Sustainability and Electrification-Driven Opportunities

Opportunity 1: Adhesives Compatible With Recycled and Bio-Based Flock Fibers and Substrates

The global shift toward circular manufacturing is opening new demand for flock adhesives engineered to bond effectively with recycled and bio-derived materials such as rPET flock fibers, recycled paperboard, and sustainable textile substrates. Manufacturers are increasingly integrating bio-based components—such as starch-derived or soy-derived polyols—into polyurethane flock adhesive formulations to increase renewable content and support aggressive corporate decarbonization goals across automotive and apparel supply chains. Industries like packaging, fashion, and nonwoven textiles are actively testing flock adhesives that can maintain bond integrity, abrasion resistance, washability, and colorfastness even when applied to substrates with high recycled content. This compatibility is essential for brands pursuing eco-certifications and aligns with broader sustainability mandates across consumer goods and transportation markets.

Opportunity 2: High-Performance Flock Adhesives Tailored for EV Thermal, Electrical & Environmental Demands

Electrification is creating a new category of high-performance flock adhesives designed for harsh thermal, electrical, and environmental conditions within EV platforms. Flocked insulation materials are increasingly deployed around EV battery packs, electrical harnesses, and power modules to provide lightweight thermal barriers and dielectric protection. As a result, adhesive systems must combine inherent flame retardancy, high dielectric strength, and exceptional chemical resistance to prevent thermal propagation and electrical failure. These adhesives must also endure severe temperature cycling—from –40°C to +80°C and beyond—without softening, delaminating, or losing mechanical strength, given the extreme heating and cooling cycles associated with fast charging and high-power operation. This creates a lucrative opportunity for suppliers capable of engineering durable, flame-retardant, thermally stable flock adhesive systems purpose-built for next-generation EV architectures.

The global flock adhesives market is shaped by a mix of chemical innovators, machinery integrators, and automotive adhesive suppliers that are advancing the performance and sustainability standards of flocking applications.

H.B. Fuller remains a global leader in automotive adhesives and textile bonding technologies, known for its low-emission polyurethane systems that reduce NVH levels in EV interiors. Its Swift® and Rakoll® product lines include high-flexibility, moisture-cure, and hot-melt solutions with proven durability under repetitive mechanical stress. Fuller’s current R&D focuses on renewable feedstock adhesives as substitutes for traditional petrochemical formulations. Additionally, its integrated flocking process solutions — including equipment recommendations and dispensing system alignment — enhance automation efficiency across production lines.

Henkel continues to lead with energy-efficient, UV-curable adhesive technologies under its LOCTITE and TECHNOMELT brands, offering instant curing times and reduced environmental impact. Its low-VOC water-based polyurethane and acrylic systems are designed for automotive, apparel, and packaging flocking, fully aligned with European and U.S. emission standards. Henkel’s R&D focus on substrate adhesion optimization ensures superior fiber anchoring even on metal, rubber, and composite surfaces. The company is deeply embedded in footwear and apparel applications, where adhesives must endure repeated washing and mechanical flexing.

Covestro AG serves as a critical upstream material supplier, producing polyurethane raw materials such as Desmodur® and Desmolac® dispersions essential for flock adhesive formulations. Its strategy centers on bio-based and mass-balanced PU dispersions, enabling adhesive manufacturers to reduce carbon footprints without compromising performance. Ongoing R&D initiatives aim to improve thermal stability and chemical resistance in flock adhesives used in engine compartment seals, exterior automotive trims, and heavy-duty textiles. Covestro’s materials allow fine-tuning of cure time, pot life, and mechanical strength, offering adhesive converters flexibility to meet diverse industry needs.

Huntsman leverages its Advanced Materials division to deliver epoxy and polyurethane-based flock adhesives with exceptional chemical resistance and adhesion to multi-layered substrates. Its products are widely utilized in industrial and technical textiles, including filtration, wall coverings, and heavy-duty coatings. Huntsman’s expertise in formulating variable-viscosity, two-component systems supports manufacturers requiring extended open times and high initial tack for large-format or complex flocking operations. The company’s integration of composite materials technology also positions it to support lightweight aerospace and automotive interiors requiring advanced flock adhesion.

Kiian Digital, part of INX International, stands out for its innovation in digital textile printing and adhesive deposition technologies. The company’s precision-applied flock adhesives are engineered to work seamlessly with digital printheads, enabling on-demand flocking patterns for high-end apparel, promotional textiles, and home décor. Its formulations are REACH-compliant and meet global apparel safety standards, making them ideal for sustainable fashion production. Kiian’s strategic focus on hybrid sublimation and pigment-based adhesives has opened new pathways for color-adhesive integration, enhancing design flexibility for textile decorators.

CIM-JET S.r.l. represents the intersection of machinery engineering and adhesive application, manufacturing state-of-the-art electrostatic flocking lines integrated with precision adhesive coating and dosing systems. Its technology ensures uniform adhesive layer thickness, optimized drying, and minimal waste generation — essential for achieving consistent flock density and adhesion strength. With its recent expansion into South America (July 2025), CIM-JET is supporting automotive and textile manufacturers seeking advanced flocking automation systems. The company’s systems are particularly favored in glove box interiors, dashboard trims, and sealing profiles, where dimensional accuracy and surface aesthetics are critical.

Germany remains at the forefront of the global flock adhesives market, driven by its robust industrial ecosystem, environmental regulations, and leadership in sustainable adhesion technologies. German specialty chemical companies, such as CHT Germany GmbH, continue to advance the industry with their TUBICOLL product line, emphasizing water-based polyurethane flock adhesives tailored for textile, automotive, and interior applications. The high-performance adhesives deliver exceptional durability, adhesion to synthetic fibers, and low environmental impact—meeting the growing demand for VOC-compliant materials under EU environmental standards.

The automotive sector remains Germany’s largest application base, with Tier 1 suppliers increasingly using flock adhesives in interior trims, seals, glove box assemblies, and pillar components. The adhesives enhance noise and vibration reduction (NVH control), providing superior tactile finishes that meet the country’s strict quality and performance standards. Moreover, the Industrieverband Klebstoffe (IVK) continues to promote the role of adhesives as “enablers of the circular economy”, encouraging the formulation of recyclable and repairable adhesive systems. Major players like Henkel AG & Co. KGaA are spearheading R&D initiatives focused on low-emission, high-durability adhesion systems, while manufacturers such as PFT Flock-Technik GmbH leverage German R&D strength to expand globally, including into Eastern Europe. Supported by initiatives like DIN/TS 54405 for design-for-disassembly, Germany is setting global benchmarks for eco-efficient flock adhesive formulations aligned with circular production practices.

China dominates the flock adhesives market as the world’s largest textile and apparel producer, underpinned by government policies promoting green manufacturing and industrial modernization. The 14th Five-Year Plan (2021–2025) prioritizes sustainability in industrial production, leading to a transition from solvent-based to water-borne and high-solid flock adhesives. The shift is accelerated by the tightening of emission standards and environmental audits targeting textile and coating facilities across the country.

According to the China National Textile and Apparel Council, fixed asset investment in textile, apparel, and chemical fiber industries saw strong year-on-year growth through 2024, confirming the expanding domestic base for industrial adhesive applications. The ongoing trend of high-end, intelligent, and green textile equipment development—supported by automation and robotics—demands fast-curing, consistent-performance flock adhesives suitable for precision flocking lines. Furthermore, the technical textile sector, including medical textiles, filtration materials, and functional apparel, is diversifying demand for specialty polyurethane (PU) and acrylic-based flock adhesives with enhanced heat resistance, flexibility, and antimicrobial compatibility.

China’s domestic chemical manufacturers are scaling up production of advanced PU resins and acrylic dispersions, reducing reliance on imported adhesive raw materials and fortifying local supply chains. Combined with the ongoing expansion in home textiles, apparel, and automotive interiors, China remains the largest consumption hub for flock adhesives globally, while simultaneously evolving toward green, compliant, and export-ready adhesive technologies.

The United States flock adhesives market is experiencing strong growth, driven by environmental policy alignment, sustainability innovation, and the premiumization of packaging and interior applications. Market leaders are focusing on low-VOC and bio-based adhesive systems to meet EPA and state-level clean air regulations, particularly across automotive, packaging, and decorative sectors. The transition from solvent-based to water-borne formulations is reshaping product portfolios, with polyurethane and acrylic dispersions emerging as dominant chemistries for eco-compliant flocking applications.

A key trend is the rise of bio-content innovation, with companies like H.B. Fuller Company validating sugar-cane-derived tackifiers under ISCC PLUS certification, paving the way for renewable-sourced flock adhesives that lower Scope 3 emissions in production. The automotive sector, bolstered by the EV transition and lightweighting efforts, is driving demand for high-performance PU flock adhesives that bond to complex composite and thermoplastic substrates. The adhesives are crucial for acoustic insulation, energy absorption, and surface finish durability. Additionally, the luxury packaging segment—including cosmetics, jewelry, and specialty boxes—is increasingly using flocking for aesthetic texture and tactile enhancement, fueling demand for non-migrating, high-clarity, and durable adhesive grades. With consumer and regulatory pressure converging, the U.S. market is emerging as a pioneer in green chemistry-based, high-durability flock adhesives for industrial and consumer applications alike.

India’s flock adhesives market is expanding rapidly, powered by its Make in India initiative, technical textiles expansion, and infrastructure development programs. The 2024–2025 national budget substantially increased allocations for the textile and technical textile sectors, with additional funding directed toward the Production Linked Incentive (PLI) and PM MITRA schemes—initiatives that directly enhance domestic production capacity for industrial adhesives and textile finishing solutions.

Under the National Technical Textiles Mission, government funding has more than doubled year-on-year, catalyzing growth in specialized end-use areas such as medical textiles, automotive interiors, and high-performance fabrics—all of which utilize flock adhesives for surface bonding and reinforcement. Furthermore, infrastructure-led growth in residential, commercial, and transport construction drives indirect demand for adhesive bonding solutions, particularly in furniture, insulation, and decorative components. The localization push in defense, aerospace, and electronics manufacturing further incentivizes the domestic production of certified, high-specification adhesive systems, reducing dependency on imports.

India’s strong domestic growth in furniture, modular interiors, and e-commerce packaging sectors is also spurring demand for decorative flock adhesives in protective and aesthetic coatings. With its expanding industrial base, government-backed manufacturing incentives, and growing export orientation, India stands as one of the fastest-growing markets for flock adhesives in Asia, particularly in PU and water-borne adhesive formulations for technical and decorative textile applications.

Flock Adhesives Market Report Scope

Flock Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.9 Billion

|

|

Market Size (2034)

|

$5.9 Billion

|

|

Market Growth Rate

|

4.8%

|

|

Segments

|

By Resin Type (Acrylic, Polyurethane, Epoxy Resin, Vinyl, Others), By Technology (Water-Based Adhesives, Solvent-Based Adhesives, Hot-Melt Adhesives, Reactive Adhesives), By End-User (Automotive, Textile & Apparel, Paper & Packaging, Consumer Goods, Industrial, Footwear & Leather, Construction / Upholstery), By Flock Material Type (Nylon Flock, Rayon Flock, Polyester Flock, Cotton Flock, Others), By Application Method (Spray Coating, Screen Printing / Rotary Printing, Brush Coating, Roll Coating, Dipping

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, Sika AG, Dow Chemical Company, Kissel + Wolf GmbH, CHT Germany GmbH, Stahl Holdings B.V., Bostik SA, 3M Company, Lord Corporation, Covestro AG, DELO Industrial Adhesives, Franklin International, Avient Corporation, Wacker Chemie AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type / Chemistry

- Acrylic

- Polyurethane

- Epoxy Resin

- Vinyl

- Others

By Technology / Formulation

- Water-Based Adhesives

- Solvent-Based Adhesives

- Hot-Melt Adhesives

- Reactive Adhesives

By End-Use Industry

- Automotive

- Textile & Apparel

- Paper & Packaging

- Consumer Goods

- Industrial

- Footwear & Leather

- Construction / Upholstery

By Flock Material Type

- Nylon Flock

- Rayon Flock

- Polyester Flock

- Cotton Flock

- Others

By Application Method

- Spray Coating

- Screen Printing / Rotary Printing

- Brush Coating

- Roll Coating

- Dipping

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Sika AG

- Dow Chemical Company

- Kissel + Wolf GmbH

- CHT Germany GmbH

- Stahl Holdings B.V.

- Bostik SA

- 3M Company

- Lord Corporation

- Covestro AG

- DELO Industrial Adhesives

- Franklin International

- Avient Corporation

- Wacker Chemie AG

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Global Flock Adhesives Market through decision-grade analytics that connect chemistry, process parameters, and end-use outcomes. It delivers analysis reviews of demand drivers across automotive NVH interiors, technical textiles, premium packaging, and consumer goods; highlights breakthroughs in low-VOC water-based PU dispersions, UV-curable acrylics, bio-based platforms, and high-durability two-component systems; and maps regulatory inflection points (REACH, cabin air quality, EPA VOC) to procurement and specification strategy. With granular sizing, price corridors, and install-throughput benchmarks aligned to modern flocking methods (spray, screen/rotary, roll, dipping), this report is an essential resource for OEMs, Tier-1s, textile converters, and sourcing leaders seeking sustainable, high-adhesion, soft-touch, and abrasion-resistant solutions that scale on automated production lines.

Scope Highlights

Segmentation:

- By Resin Type/Chemistry: Acrylic; Polyurethane; Epoxy Resin; Vinyl; Others.

- By Technology/Formulation: Water-Based Adhesives; Solvent-Based Adhesives; Hot-Melt Adhesives; Reactive Adhesives.

- By End-Use Industry: Automotive; Textile & Apparel; Paper & Packaging; Consumer Goods; Industrial; Footwear & Leather; Construction/Upholstery.

- By Flock Material Type: Nylon Flock; Rayon Flock; Polyester Flock; Cotton Flock; Others.

- By Application Method: Spray Coating; Screen Printing/Rotary Printing; Brush Coating; Roll Coating; Dipping.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Frame: Historic data 2021–2024 and forecast data 2025–2034.

Companies: Analysis/profiles of 15+ companies (strategy, portfolio, sustainability, partnerships, and recent moves).

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.