Market Overview: Global Food Packaging Machinery Market to Reach $26.5 Billion by 2034

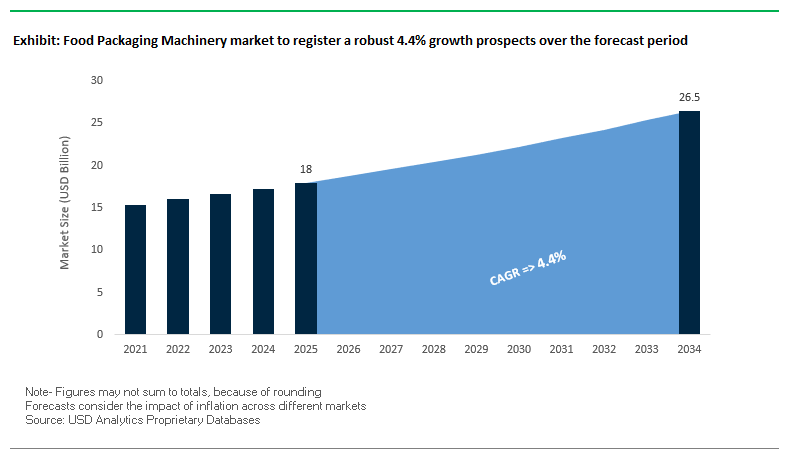

The global food packaging machinery market is valued at $18 billion in 2025 and is expected to expand to $26.5 billion by 2034, growing at a CAGR of 4.4%. This market plays a critical role in enabling food manufacturers to meet consumer expectations for safety, efficiency, and sustainability. For industry professionals and buyers, food packaging machinery provides the backbone for ensuring speed, precision, and operational flexibility in processing environments ranging from ready-to-eat meals to high-volume packaged goods.

The sector is being driven by automation, smart technologies, and the ability to handle sustainable packaging materials without compromising efficiency. The shift toward AI, IoT, and robotics integration has further accelerated innovation, enabling predictive maintenance and real-time defect detection that enhance food safety while reducing waste. At the same time, machinery capable of processing biodegradable plastics, recycled paperboard, and fiber-based packaging is addressing the rising global demand for eco-friendly solutions.

Key Insights for Industry Professionals:

- Automation as a Driver: Advanced packaging lines reduce labor costs and enhance throughput.

- Flexibility in Packaging Formats: Adaptability to pouches, trays, cartons, and rigid containers supports product diversification.

- Integration of Smart Technologies: AI-powered systems enable predictive maintenance and precision defect detection.

- Sustainable Packaging Compatibility: Machinery designed to process biodegradable and recycled materials is in high demand.

Market Analysis: Recent Developments Shaping the Food Packaging Machinery Industry

The food packaging machinery market is evolving rapidly with major product launches, capacity expansions, and strategic acquisitions aimed at strengthening global positions and aligning with sustainability goals.

In August 2025, Krones introduced its LinaFlex eSync pasteurizer with space-saving single-lane transport and the Lavasonic HI bottle washer utilizing ultrasound cleaning technology, highlighting its focus on efficiency and sustainability. Earlier, in April 2025, Krones completed the acquisition of Netstal Maschinen AG, enabling it to provide a complete closed-loop PET solution from preforms to recycling.

Tetra Pak significantly expanded its manufacturing footprint in July 2025 by inaugurating its second aseptic carton packaging line in Vietnam, investing €97 million to boost output beyond 30 billion packs annually, reinforcing its commitment to Southeast Asia. At the same time, MULTIVAC opened a Global Capability Center in India, enhancing its regional expertise, and in February 2025, partnered with Watttron to advance “Smart Heating” for recyclable thermoformed packaging.

On the technology front, IMA launched its AI LAB in June 2025 to accelerate the adoption of artificial intelligence in packaging equipment, focusing on advanced vision and barcode systems. Meanwhile, Syntegon hosted its Pharmatag 2025 in May, unveiling its SynTiso line for liquid filling, demonstrating leadership in regulated packaging environments.

Additionally, GEA secured one of its largest-ever contracts in April 2025 to build an integrated dairy facility in Algeria, a project that integrates large-scale processing and packaging machinery. Collectively, these developments underscore how the market is advancing toward automation, digitalization, and eco-material readiness, reshaping global competitiveness.

Trends and Opportunities Transforming the Food Packaging Machinery Market

Shift Towards High-Barrier Modified Atmosphere Packaging (MAP) for Shelf-Life Extension

The food packaging machinery market is increasingly shaped by the growing adoption of Modified Atmosphere Packaging (MAP) technologies, driven by the need to extend shelf life, reduce waste, and maintain product integrity across long distribution chains. MAP relies on high-barrier films and precision gas flushing systems to slow spoilage and preserve sensory qualities, making it a core technology in meat, dairy, bakery, and ready-to-eat categories.

Academic research underscores the effectiveness of MAP: in the Dutch fresh meat industry, MAP adoption significantly reduced losses in the supply chain, lowering both economic and environmental impacts. The choice of gas mixtures is crucial high-oxygen MAP is widely applied in red meat packaging to maintain oxymyoglobin, preserving the bright red appearance that consumers equate with freshness. However, studies caution that excessive CO₂ in high-moisture foods can impair quality, highlighting the importance of machinery that enables precise control over gas ratios.

Packaging machinery manufacturers are investing in advanced sealing and gas-flushing technologies capable of delivering tailored atmospheres for specific food types. This precision not only ensures food safety and extended shelf life but also helps retailers and brands reduce waste a critical driver as global food waste exceeds 1.3 billion tons annually. The demand for MAP-ready packaging machinery is expected to expand further as centralized processing and e-commerce-driven food logistics continue to grow.

Regulatory and Consumer Pressure for Recyclable and Reduced Plastic Formats

The second major trend is the dual impact of regulatory mandates and consumer demand for more sustainable packaging formats. With the European Union’s Packaging and Packaging Waste Regulation (PPWR) now in effect, all food packaging must be recyclable by 2030, with explicit bans on hard-to-recycle formats like PVC and polystyrene. These rules are transforming machinery requirements, as converters must adapt to handle mono-materials and paper-based trays while maintaining throughput and efficiency.

Corporate commitments are accelerating the shift. One packaging firm recently commercialized paperboard trays for chilled foods that reduce plastic content by up to 90%, showcasing how packaging innovation directly aligns with ESG goals. In addition, regulatory agencies highlight that PPWR will influence entire supply chains, from raw material sourcing to distribution, forcing manufacturers to upgrade equipment for compatibility with recyclable substrates.

Food packaging machinery companies are responding with new thermoforming and form-fill-seal machines designed to process PE- or PP-based mono-material films and hybrid fiber-based solutions. At the same time, consumer preference for visibly sustainable formats means equipment must integrate capabilities for handling emerging packaging materials while ensuring food safety, durability, and high-speed production.

Development of High-Performance Recyclable Mono-Material Films

The intersection of MAP performance requirements and sustainability regulations creates a clear opportunity for the development of recyclable mono-material films. Packaging machinery will play a pivotal role in processing these new films while delivering oxygen, CO₂, and moisture barriers equivalent to traditional multi-layer laminates.

Recent commercial launches highlight rapid progress. A packaging company introduced mono-PP high-barrier films for thermoforming, certified by a German institute as fully recyclable in existing streams an achievement that removes a key barrier for FMCG adoption. Similarly, new PE-based thermoformed barrier packages demonstrate oxygen barrier performance comparable to nylon, while maintaining recyclability.

The opportunity lies in machinery innovation that ensures these new materials can be processed at scale, with reliable sealing, thermoforming, and gas barrier performance. As demand for MAP-compatible mono-materials rises, companies that offer equipment solutions optimized for these films will be positioned at the forefront of the sustainability-driven packaging transition.

Integration of Smart Labels for Dynamic Freshness and Traceability Indicators

Another high-growth opportunity is the integration of smart packaging technologies such as time-temperature indicators (TTIs), freshness sensors, and QR-enabled smart labels. These innovations turn packaging into an active participant in food safety and consumer engagement, creating demand for machinery platforms capable of inline smart label application.

For consumers, smart labels enhance trust by providing a transparent signal of product freshness and traceability. Integrated with digital platforms, they allow brands to offer dynamic “digital passports” that track production, shipping, and storage conditions. Machinery providers that adapt their lines to seamlessly integrate these smart technologies will not only support compliance with stricter food safety standards but also unlock new consumer engagement opportunities in an increasingly connected packaging ecosystem.

Competitive Landscape: Leading Companies Driving Innovation and Sustainability

The food packaging machinery market is dominated by multinational corporations leveraging acquisitions, digital transformation, and sustainability-focused R&D to maintain competitive advantage.

Tetra Pak: Expanding in Southeast Asia with €97 Million Investment

Tetra Pak remains a global leader in processing and packaging for liquid foods. In July 2025, it expanded its Vietnam facility with a €97 million investment, doubling capacity to 30 billion packs annually. With specialized machinery for categories like coffee and iced tea, and its May 2025 Customer Innovation Centre in Thailand, Tetra Pak combines end-to-end sustainability and co-creation capabilities with strong regional expansion.

Krones AG: Driving PET Recycling and Efficiency Innovations

Krones strengthens its leadership in beverage and food packaging machinery through its April 2025 acquisition of Netstal, enabling a closed PET loop offering. Its August 2025 innovations, including the LinaFlex eSync pasteurizer and Lavasonic HI bottle washer, highlight advances in sustainability and footprint optimization. Krones excels as a total system supplier, integrating AI-powered predictive maintenance into complete line solutions.

MULTIVAC: Scaling Global Reach and Smart Heating Partnerships

MULTIVAC focuses on thermoforming machines, traysealers, and inspection systems. The company opened a Global Capability Center in India in July 2025 and continues to expand in Europe with its Bulgarian site. Strategic collaborations, including the Watttron Smart Heating initiative, reflect MULTIVAC’s pursuit of sustainable thermoformed packaging. Its portfolio emphasizes automation and flexibility for diverse batch sizes and materials.

Syntegon Technology: Leading in High-Precision and Regulated Packaging

Syntegon maintains strong positions in both food and pharmaceuticals with high-speed vertical and horizontal systems. Its record FY 2024 results highlight growing demand, and its SynTiso line unveiled at Pharmatag 2025 reinforced its role in liquid filling technologies. With validated SBTi climate targets, Syntegon is committed to sustainability while leveraging engineering excellence and lifecycle management for customer value.

IMA Group: Accelerating AI-Driven Packaging Innovation

IMA is pioneering digitalization through the launch of its IMA AI LAB in June 2025, designed to integrate robotics and vision systems into packaging lines. The acquisition of Sarong’s thermoform-fill-seal business in August 2024 broadened its expertise. With more than 3,000 patents and 53 facilities worldwide, IMA combines innovation scale with deep expertise in flexible packaging and end-of-line automation.

GEA Group: Securing Landmark Dairy Facility Contract in Algeria

GEA is one of the largest system suppliers for food and beverage, emphasizing sustainability through its “Engineering for a better world” approach. In April 2025, it won one of its biggest contracts to build a large-scale dairy facility in Algeria, integrating advanced processing and packaging lines. GEA’s global technology centers allow customers to trial new solutions, positioning it as a trusted partner for alternative proteins and sustainable production.

Food Packaging Machinery Market Share Insights

Form-Fill-Seal Machines Lead Market Share by Machine Type in Food Packaging Machinery

In 2025, form-fill-seal (FFS) machines account for 25% of the food packaging machinery market, making them the backbone of flexible packaging’s global expansion. These machines dominate due to their unmatched ability to streamline operations by forming, filling, and sealing in a continuous process, drastically reducing labor costs, material waste, and production time. Their versatility in handling powders, liquids, and solids positions them as the go-to technology for snack foods, beverages, and ready meals. Filling and dosing machines, at 20%, hold the next largest share, reflecting the universal requirement for precision and speed across every food segment. Meanwhile, labeling and coding machines secure essential demand as traceability and regulatory compliance intensify under frameworks such as FSMA and EU food labeling directives. End-of-line automation via cartoning and palletizing further boosts efficiency, while cleaning and sterilizing systems serve aseptic niches like dairy and baby food, where hygiene assurance is non-negotiable. Overall, machine type segmentation highlights how FFS systems dominate flexible packaging production, filling and dosing ensure accuracy, and coding machinery enforces compliance in an increasingly automated landscape.

Beverages Command Market Share by Application in Food Packaging Machinery

By application, the beverage sector leads the food packaging machinery market with a 25% share in 2025, reflecting its reliance on ultra-high-speed filling, capping, and labeling lines capable of producing tens of thousands of bottles per hour. This segment drives continuous innovation in aseptic filling technology, carbonated product handling, and palletizing automation to support the scale of global soft drink, bottled water, and juice production. Convenience foods follow at 20%, where machinery flexibility is paramount to accommodate multiple SKUs, portion sizes, and packaging formats within the same production facility. Dairy products remain critical investors in CIP/SIP sterilizing systems and precision dosing, while bakery and confectionery machinery focuses on gentle handling solutions to preserve product integrity. Meat, poultry, and seafood applications depend heavily on MAP-enabled tray sealing machines, ensuring freshness and extending shelf life. Meanwhile, fruits and vegetables increasingly adopt automated weigh-price labelers and FFS solutions to meet the growing demand for fresh-cut and packaged produce. Collectively, this application breakdown illustrates how beverages drive machinery scale and innovation, convenience foods push for format agility, and proteins demand safety-driven MAP solutions.

United States: Automation and E-Commerce Driving Food Packaging Machinery Innovation

The U.S. food packaging machinery market is undergoing a significant transformation driven by automation, robotics, and e-commerce demand. Companies are heavily investing in automation-ready secondary packaging lines, with some firms reporting labor reductions of up to 85% while maintaining high output, addressing workforce shortages and boosting operational efficiency. The booming e-commerce sector is fueling demand for machinery capable of handling diverse package formats, including small parcels and subscription boxes, which is critical for online retail logistics. Technological advancements, particularly AI-enabled vision systems, are enabling predictive maintenance for case packers, palletizers, and robotics, reducing downtime and material waste a key application of Industry 4.0 principles. Moreover, the regulatory shift towards PFAS-free materials is driving demand for machinery that can process alternative packaging substrates. Premiumization trends in food and beverage, particularly high-barrier flexible packaging, are further stimulating the development of machinery that accommodates multilayer films, supporting clean-label and shelf-life extension requirements.

Germany: Leading in Circular Economy and Hygienic Packaging Machinery

Germany’s food packaging machinery market is defined by its stringent regulatory framework, including the Packaging Act (VerpackG) and EU directives promoting circular economy practices. The mandatory reusable packaging obligation for catering businesses, implemented in January 2023, has created a new market for machinery capable of washing, sorting, and refilling reusable containers. Germany is also a pioneer in machinery with advanced hygienic designs, ensuring easy cleaning, minimal human contact, and compliance with food safety regulations, especially in meat and dairy sectors. Additionally, German trade organizations actively promote machinery technologies abroad, with delegations highlighting innovations to strengthen international partnerships and expand exports, reinforcing the country's leadership in global food packaging machinery.

China: Intelligent Automation and End-to-End Packaging Solutions Accelerating Market Expansion

China’s food packaging machinery market is experiencing rapid advancements in intelligent, multifunctional, and highly automated equipment. The adoption of IoT, AI quality inspection, and 5G remote monitoring has significantly enhanced production efficiency, equipment stability, and operational reliability. Chinese manufacturers are recognized globally for providing cost-effective yet high-quality machinery compliant with CE and ISO standards. There is a growing trend toward integrated, end-to-end packaging lines capable of handling filling, sealing, palletizing, and logistics, which is essential for large-scale food and beverage operations. Robotics is a key driver, with fully automatic palletizing systems processing up to 1,200 boxes per hour, reducing labor costs and optimizing warehouse operations, making China a global hub for efficient and scalable packaging machinery solutions.

India: Government Incentives and Automation Fueling Packaging Machinery Growth

India’s food packaging machinery market is being propelled by governmental initiatives such as the Production Linked Incentive (PLI) Scheme, supporting capital investment in automated food and packaging lines. The rapid adoption of automation, robotics, and smart technologies is enhancing operational efficiency, reducing labor costs, and improving product quality standards. The e-commerce boom and growth of convenience foods are increasing demand for machinery capable of handling various product sizes and customized packaging formats. Sustainability is also a key trend, with the Food Safety and Standards Authority of India (FSSAI) approving recycled PET for food-contact applications, which drives the demand for machinery that can process recycled materials and support circular economy practices.

Brazil: Technological Investment and Sustainable Packaging Machinery Expanding Market Potential

Brazil’s food packaging machinery market is seeing substantial technological investment to meet growing domestic demand for packaged foods. Automation for both rigid and flexible packaging lines is a key trend, enabling efficiency and consistency in production. Regulatory compliance is driving machinery development, with the Brazilian Health Regulatory Agency (Anvisa) providing clear guidelines for food contact materials and equipment to ensure consumer safety. Companies are also focusing on sustainable solutions, developing automated equipment capable of handling recycled and bio-based materials to reduce reliance on fossil fuels, reflecting Brazil’s commitment to eco-friendly packaging practices while supporting industry growth.

Japan: Precision, Hygiene, and Automation Addressing Labor Shortages and Market Needs

Japan’s aging workforce is driving demand for highly automated food packaging machinery to maintain productivity and reduce labor dependency. The market is responding with machinery optimized for small-format packaging, catering to the growing single-person household trend, and providing customizable solutions for compact packaging requirements. Strict hygiene regulations under the Japanese Sanitation Act have led to the development of machinery with advanced hygienic features to minimize contamination and ensure product safety. Japanese manufacturers also lead in precision-sensitive applications; for example, seafood processing machinery has achieved a 15% waste reduction and a 10% yield improvement for clients. These innovations highlight Japan’s focus on high-precision, safe, and efficient food packaging machinery.

Food Packaging Machinery Market Report Scope

Food Packaging Machinery market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$18 Billion

|

|

Market Size (2034)

|

$26.5 Billion

|

|

Market Growth Rate

|

4.4%

|

|

Segments

|

By Machine Type (Form-Fill-Seal Machines, Filling & Dosing Machines, Wrapping Machines, Labeling & Coding Machines, Cartoning Machines, Palletizing Machines, Cleaning & Sterilizing Machines, Other Machines), By Application (Bakery & Confectionery, Meat, Poultry & Seafood, Dairy Products, Fruits & Vegetables, Beverages, Convenience Foods, Other Applications), By End-Use (Food Manufacturers, Food Service Providers, Contract Packagers), By Technology (General Packaging, Modified Atmosphere Packaging, Vacuum Packaging, Aseptic Packaging)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Krones AG, Tetra Pak International S.A., MULTIVAC, IMA S.p.A., Syntegon Technology GmbH, Ishida Co., Ltd., GEA Group Aktiengesellschaft, ProMach Inc., Coesia S.p.A., OPTIMA Packaging Group GmbH, Pactiv Evergreen Inc., Fuji Machinery Co., Ltd., Duravant LLC, Harada Corporation, Yanagiya Machinery Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Food Packaging Machinery Market Segmentation

By Machine Type

- Form-Fill-Seal Machines

- Filling & Dosing Machines

- Wrapping Machines

- Labeling & Coding Machines

- Cartoning Machines

- Palletizing Machines

- Cleaning & Sterilizing Machines

- Other Machines

By Application

- Bakery & Confectionery

- Meat

- Poultry & Seafood

- Dairy Products

- Fruits & Vegetables

- Beverages

- Convenience Foods

- Other Applications

By End-Use

- Food Manufacturers

- Food Service Providers

- Contract Packagers

By Technology

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Food Packaging Machinery Market

- Krones AG

- Tetra Pak International S.A.

- MULTIVAC

- IMA S.p.A.

- Syntegon Technology GmbH

- Ishida Co., Ltd.

- GEA Group Aktiengesellschaft

- ProMach Inc.

- Coesia S.p.A.

- OPTIMA Packaging Group GmbH

- Pactiv Evergreen Inc.

- Fuji Machinery Co., Ltd.

- Duravant LLC

- Harada Corporation

- Yanagiya Machinery Co., Ltd.

*List not Exhaustive

Research Coverage

This report by USDAnalytics investigates the global food packaging machinery market, offering a comprehensive analysis of recent breakthroughs, technological advancements, and strategic developments shaping the sector. The study reviews historical data from 2021 to 2024 and provides robust forecasts from 2025 to 2034, highlighting opportunities for automation, smart machinery integration, and sustainable packaging solutions. The report highlights key trends, including Modified Atmosphere Packaging (MAP), recyclable and mono-material handling capabilities, AI-driven predictive quality control, and end-of-line automation. It further examines the competitive landscape, spotlighting strategic investments, acquisitions, and global expansions by leading manufacturers, underscoring how innovation and sustainability initiatives are redefining market dynamics. For industry professionals, this report is an essential resource for identifying investment opportunities, understanding technological trajectories, optimizing production processes, and staying ahead of regulatory shifts. USDAnalytics provides critical insights that equip decision-makers to enhance operational efficiency, reduce waste, and adopt agile packaging machinery capable of supporting diverse applications across food and beverage sectors.

Scope Highlights:

- Segmentation: By Machine Type (Form-Fill-Seal Machines, Filling & Dosing Machines, Wrapping Machines, Labeling & Coding Machines, Cartoning Machines, Palletizing Machines, Cleaning & Sterilizing Machines, Other Machines), By Application (Bakery & Confectionery, Meat, Poultry & Seafood, Dairy Products, Fruits & Vegetables, Beverages, Convenience Foods, Other Applications), By End-Use (Food Manufacturers, Food Service Providers, Contract Packagers), By Technology (General Packaging, Modified Atmosphere Packaging, Vacuum Packaging, Aseptic Packaging)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Historical & Forecast Data: Historical insights from 2021–2024 and projections from 2025–2034

- Companies: In-depth analysis and profiles of 15+ key industry players including Krones AG, Tetra Pak, MULTIVAC, IMA, Syntegon Technology, GEA, and others

Methodology

This report employs a rigorous and multi-faceted research methodology designed to deliver actionable insights for industry professionals. Primary research included direct interviews with executives, engineers, and decision-makers at leading food packaging machinery manufacturers, distributors, and end-users. Secondary research involved a detailed review of company reports, press releases, regulatory filings, and trade publications to identify recent trends, technological innovations, and market dynamics. Quantitative data was triangulated using multiple sources to ensure accuracy, covering production volumes, revenue, and machinery adoption rates across various regions and applications. Forecasting was conducted using advanced statistical models incorporating CAGR, market penetration, and technology adoption rates, ensuring reliable projections from 2025 to 2034. USDAnalytics also applied competitive benchmarking and SWOT analyses to evaluate strategic positioning, innovation capabilities, and sustainability initiatives, providing a holistic understanding of the global market landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.