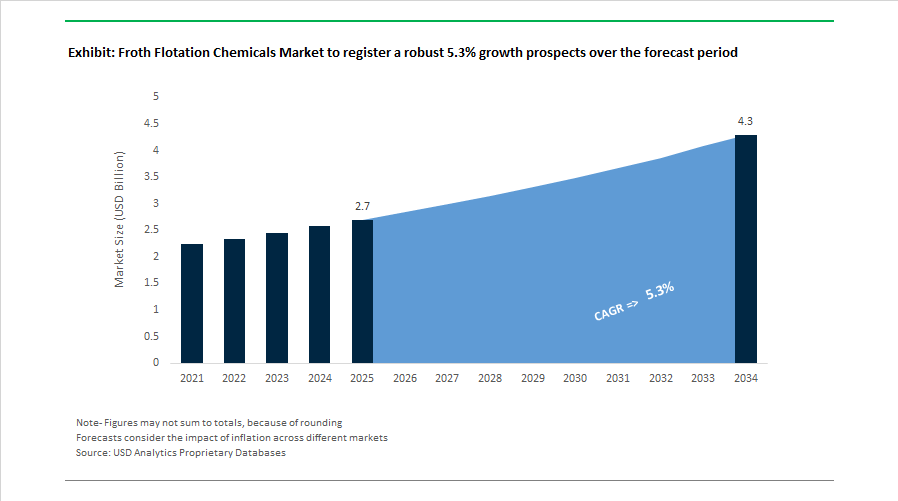

Froth Flotation Chemicals Market Size 2025–2034: $2.7 Billion to $4.3 Billion at 5.3% CAGR Shaped by Green Reagents and AI-Driven Optimization

The Froth Flotation Chemicals Market is projected to expand from $2.7 billion in 2025 to $4.3 billion by 2034, registering a CAGR of 5.3%. Growth is underpinned by sustained copper, gold, lithium, and coal beneficiation activity, alongside rising regulatory pressure on tailings toxicity and water discharge standards. Collectors, frothers, modifiers, depressants, and dispersants remain core reagent categories, while digital flotation control platforms and biodegradable chemistries are reshaping procurement strategies among global mining operators. Increasing treatment of low-grade ores and complex polymetallic deposits is intensifying the demand for highly selective, pH-neutral flotation collectors and performance-optimized frothing systems.

In December 2025, Syensqo reported that temporary closures of major copper mines impacted early 2025 mining chemical volumes, prompting a strategic pivot toward resilient supply chains and diversification into lithium and battery-metal flotation reagents. In August 2025, BASF launched a global line of bio-based flotation reagents, introducing biodegradable collectors and frothers engineered to reduce tailings pond toxicity while maintaining copper and gold recovery efficiency. In April 2025, Nalco Water introduced the Flotation 360™ digital optimization platform developed with Stone Three Digital, integrating in-situ pulp sensors and machine learning to dynamically adjust reagent dosages based on bubble formation and mineral loading parameters. During 2025, KGHM successfully piloted an AI-powered flotation automation system under the EU-backed MINE.IO initiative, targeting up to 10% reduction in chemical consumption through real-time dosing control.

Strategic portfolio realignments and capacity expansions intensified across 2024 and early 2025. Following its spin-off from Solvay, Syensqo completed divestment of its Oil & Gas business to SNF Group in 2024, reallocating R&D investment toward sustainable mining reagents within its Consumer & Resources pillar. In late 2024, Solenis finalized acquisition of BASF’s mining flocculants business, incorporating brands such as Magnafloc®, Rheomax®, and Alclar®, strengthening its position in post-flotation solid-liquid separation while BASF retained flotation collector and frother portfolios. In early 2024, Clariant reported 4% organic growth in its Mining Solutions unit and expanded technical service capabilities across the Americas to support copper mines transitioning toward more selective flotation chemistries. During 2024, Shaanxi Coal and Chemical Industry expanded production capacity for specialized collectors and frothers targeting low-grade iron and copper ore beneficiation in China. Cheminova introduced new coal flotation reagents optimized for high-ash feedstocks, enhancing selectivity in emerging market coal processing plants. The 2024 market also saw broader adoption of Metso Outotec’s Spider Crowder flotation equipment upgrade, which altered froth surface dynamics and required recalibration of frother-to-collector ratios in operational circuits. In July 2025, Arkema announced a $20 million investment in Singapore to expand high-purity specialty material intermediates that support advanced flotation reagent formulation.

Trends and Opportunities Reshaping the Global Froth Flotation Chemicals Market

High-Selectivity Chemistry for Complex and Polymetallic Ore Bodies

The depletion of easily accessible high-grade deposits is forcing operators to process polymetallic and refractory ores with tightly interlocked mineral phases. This shift has significantly raised the technical bar for collectors, frothers, and modifiers. In June 2025, optimized flotation circuits for copper–lead–zinc ores demonstrated that advanced selective reagent systems could lift copper recovery from 83.33% to more than 90.32% while reducing lead and zinc contamination in the copper concentrate by up to 55%. These gains directly translate into higher payable metal and lower downstream smelting penalties.

Molybdenum–copper separation has also seen notable progress. Industrial trials reported in December 2025 at the Aktogay deposit showed that modified apolar flotation agents, including diesel-based collectors treated with ultrasonic activation, increased molybdenum concentrate grade by 3.6% and overall recovery by 5.7% compared with conventional kerosene systems. This reflects a broader industry trend toward chemically and physically enhanced collectors that improve selectivity without increasing dosage.

Nanotechnology is emerging as a disruptive enabler. By 2025, engineered nanoparticles acting as collectors or surface modifiers have progressed from pilot trials into early commercial deployment. These nano-collectors enhance mineral selectivity at the molecular scale, allowing mining operations to reduce total reagent consumption by nearly 30% while improving recovery of ultra-fine particles that were historically lost to tailings.

Sustainability-Driven Reformulation and Cyanide Reduction Pressure

Environmental regulation and investor-led ESG frameworks are accelerating the shift away from toxic flotation reagents. By 2025, approximately 80% of mining companies in North America had initiated transitions toward biodegradable depressants and low-toxicity collectors. Suppliers such as AkzoNobel and Clariant have introduced eco-labeled flotation chemicals that report up to 30% lower environmental impact while maintaining or improving recovery rates by as much as 15%.

Gold flotation is a focal point of reformulation. Although cyanide remains central to leaching, flotation circuits are increasingly incorporating cyanide-free depressants for pyrite suppression. In late 2025, research activity intensified around organic sulfite systems and starch-derived bio-depressants to meet stricter limits on cyanide discharge in mine effluents. These alternatives reduce long-term environmental liabilities and simplify water treatment requirements.

However, innovation comes at a cost. Industry data from early 2025 indicates that developing a new biodegradable flotation reagent requires an average R&D investment of around USD 10 million per product. This high capital threshold favors large multinational chemical producers such as BASF and Solvay, reinforcing market consolidation while raising entry barriers for smaller formulators.

Recovery of Critical Battery Metals from Tailings and Secondary Waste

The global push for electrification has elevated tailings reprocessing from a sustainability initiative to a strategic necessity. Governments are increasingly backing secondary resource recovery. In December 2025, India approved the National Critical Mineral Mission with funding of approximately USD 4.1 billion, prioritizing the extraction of lithium, cobalt, and nickel from mine tailings and industrial residues using advanced flotation and hydrometallurgical routes.

High-purity graphite recovery illustrates the opportunity scale. Collaborative research announced in November 2025 demonstrated a proprietary froth flotation process capable of recovering more than 98% of graphite from battery black mass and tailings, achieving oxide purities of up to 96%. This creates strong demand for custom collectors and frothers tailored to battery materials and recycling streams.

Modern tailings reprocessing is also benefiting from digitalization. By 2025, AI-guided reagent dosing and online mineralogical analysis were delivering up to 16% higher metal recovery from fine-ground waste compared with 2020 benchmarks. These improvements reposition flotation chemicals as critical enablers of circular mining and domestic critical mineral supply chains.

Water-Efficient Flotation in Arid and High-Salinity Mining Regions

Water scarcity is reshaping flotation chemistry requirements, particularly in Chile, Australia, and the U.S. Southwest. Mines in these regions are increasingly operating with seawater or highly recycled process water. This has created strong demand for salt-tolerant collectors, frothers, and modifiers that maintain performance in high-ionic-strength environments.

Chemical suppliers such as Solvay and Nalco Water are commercializing flotation reagents designed specifically for seawater circuits, eliminating the need for energy-intensive desalination. These reagents are becoming standard in Chilean copper operations that rely entirely on raw seawater for flotation.

Closed-loop water circuits introduce additional complexity. Zero-discharge mining strategies require reagents that resist degradation, scaling, and accumulation in recycled water systems. This has opened a niche market for biodegradable dispersants and scale inhibitors that stabilize froth behavior even after multiple reuse cycles.

Digital optimization further strengthens this opportunity. By 2025, AI-driven systems such as SmartFloat were widely deployed to dynamically adjust reagent dosage based on real-time water chemistry and ore variability. These platforms are delivering metallurgical performance improvements of 12 to 18% while simultaneously reducing reagent waste, positioning intelligent flotation chemistry as a core competitive advantage for modern mining operations.

Froth Flotation Chemicals Market Share and Segmentation Insights

Collector Reagents Lead Froth Flotation Chemistry Through Critical Role in Mineral Separation

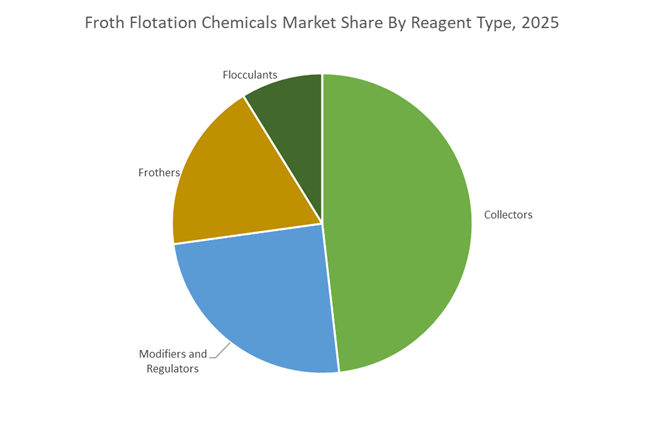

Collectors accounted for 48.20% of the Froth Flotation Chemicals Market share in 2025, making them the most essential reagent type used in mineral flotation processes. Collectors function by selectively adsorbing onto mineral surfaces and altering their surface properties to become hydrophobic, enabling valuable mineral particles to attach to air bubbles and rise to the froth layer for separation from unwanted gangue material. This mechanism forms the core principle of froth flotation technology, which is widely used in the beneficiation of sulfide ores, base metals, and complex polymetallic deposits. Common collector chemistries include xanthates, dithiophosphates, and thionocarbamates, each tailored to interact with specific mineral compositions. In 2025, collector development is increasingly focused on enhancing selectivity for complex ore bodies, as declining ore grades and challenging mineralogy create new processing difficulties for mining operators. Advanced collector formulations are designed to selectively separate valuable minerals from closely associated gangue, particularly in copper–molybdenum and copper–gold flotation circuits, where maintaining high concentrate grade while maximizing recovery is critical. These innovations are strengthening the role of collectors as the most strategically important reagent category in the global froth flotation chemicals market.

Mineral Processing Drives the Largest Demand for Froth Flotation Chemicals Worldwide

Mineral Processing represented 78.60% of the Froth Flotation Chemicals Market share in 2025, making it the dominant application segment across the flotation chemicals industry. Froth flotation is the primary beneficiation method used in large-scale mining operations, enabling the concentration of valuable minerals from low-grade ore bodies. The technique is widely applied in the processing of copper, zinc, lead, nickel, phosphate, and other industrial minerals, with global mining operations collectively processing billions of tons of ore annually. This massive processing volume generates consistent demand for flotation reagents including collectors, frothers, modifiers, and flocculants. In 2025, the mineral processing segment is increasingly influenced by the global energy transition and the rising demand for critical minerals used in battery and renewable energy technologies. Metals such as lithium, cobalt, rare earth elements, and graphite are becoming strategically important for electric vehicle batteries, energy storage systems, and renewable infrastructure. Many of these minerals require highly specialized flotation circuits and customized reagent systems, as their surface chemistry differs significantly from traditional base metal ores. This shift is driving ongoing innovation in collector and modifier chemistries, ensuring efficient recovery of critical minerals while maintaining concentrate purity in the evolving global froth flotation chemicals market.

Competitive Landscape in Froth Flotation Chemicals Market

Solvay Strengthens Copper and Gold Circuit Optimization with Frothpro® Deployment

Solvay S.A. remains a global leader in mining reagents, anchored in its Essential Chemistry portfolio for large-scale mineral processing. For full-year 2025, Solvay reported underlying net sales of €4.3 billion and, on February 24, 2026, projected EBITDA between €770 million and €850 million for 2026. Under its Reshaping for the Long Term strategy, the company is phasing out Transition Services Agreements following its corporate split, targeting €300 million in cumulative structural cost savings by end-2026. Scope 1 and 2 CO2 emissions declined 29% in 2025 compared to 2021 levels, nearly achieving its 2030 decarbonization target ahead of schedule. The Frothpro® series continues to gain traction in copper and gold flotation circuits across Latin America and North America, enhancing recovery rates and froth stability in high-throughput concentrators.

Clariant Expands Green Collectors and Digital Optimization via CLARITY™

Clariant AG is advancing biodegradable and bio-based flotation collectors aligned with green chemistry principles. In 2025, the company reported sales of CHF 3.9 billion and confirmed an EBITDA margin improvement to 17.8% in February 2026, marking its third consecutive year of margin expansion. Innovation sales accounted for 18.8% of total revenue in 2025, reflecting accelerated commercialization of new flotation reagents introduced within the past five years. The CLARITY™ digital service platform doubled utilization during 2025 to 2026, optimizing chemical dosing and performance across 220 plants in 38 countries. While projecting flat local currency sales for 2026, Clariant expects EBITDA margins to improve to approximately 18%, supported by completion of an CHF 80 million cost-productivity initiative. This combination of digital mining chemistry and sustainable collector chemistry reinforces its premium positioning.

BASF Enhances Low-Toxicity Frothers and Carbon Footprint Transparency

BASF SE leverages its integrated Verbund model to deliver tailored flotation solutions under the Lupromin®, Luprofroth®, and Luproset® brands. During late 2025 and early 2026, BASF accelerated global rollout of its next-generation frothers and modifiers designed with improved Globally Harmonized System safety classifications and lower toxicity profiles. For fiscal year 2026, BASF expects EBITDA before special items between $6.2 billion and $7.0 billion, supported by recovery in Chemicals and Nutrition & Care segments. Expansion of the Zhanjiang Verbund site strengthens BASF’s ability to serve Asia-Pacific, which represents approximately 48% of incremental growth in mining chemicals demand. Through verified Product Carbon Footprint transparency across its flotation portfolio, BASF enables mining clients to quantify Scope 3 emissions reductions, aligning reagent selection with corporate sustainability mandates.

Kemira Expands Water Solutions Integration for Flotation and Tailings Management

Kemira Oyj positions itself at the intersection of flotation chemistry and water-intensive mineral processing. In 2025, Kemira reported revenue of €2.75 billion and issued 2026 guidance between €2.6 billion and €3.0 billion. The Water Solutions segment contributes approximately 45% of total revenue, underscoring its importance to flotation, tailings thickening, and solid-liquid separation operations. Early 2026 acquisitions of AquaBlue, Inc. and SIDRA Wasserchemie expanded Kemira’s footprint in North America and Western Europe, strengthening its integrated water treatment portfolio. A multi-million Euro investment finalized in March 2025 to 2026 expanded Thailand production capacity to 100,000 tons annually, positioning Kemira to capture Asia-Pacific mineral processing growth. This integrated flotation and water treatment capability supports zero liquid discharge and tailings reuse strategies in water-scarce mining regions.

Arkema Advances Reverse Flotation and Safer Collector Alternatives

Arkema S.A. delivers specialized surfactants and collectors under the CustoFloat® and CustAmine® brands, particularly for reverse flotation processes in phosphate, silica, and calcium carbonate beneficiation. The company is promoting thioglycolic acid derivatives as safer and lower-dosage alternatives to sodium sulfhydrate in sulfide scavenger circuits, addressing environmental and worker safety concerns. Arkema’s global flotation laboratories are increasingly focused on rare earth mineral recovery flowsheets, reflecting rising demand linked to electrification and energy transition technologies. Through its integrated Methyl Isobutyl Carbinol production, Arkema maintains a strong position as a primary frother supplier for copper and zinc sulfide flotation. This specialization in reverse flotation and impurity removal supports high-purity mineral output for fertilizer, battery, and advanced materials markets.

China: Belt and Road Scale-Up and Green Chemistry Mandates Reshaping Reagent Demand

China continues to set the pace in the global froth flotation chemicals market through infrastructure-led demand expansion and regulatory pressure on formulation chemistry. By February 2024, Belt and Road Initiative mining investments reached a cumulative USD 1 trillion, creating integrated cross-border beneficiation corridors across Central Asia and Africa. By 2025, this infrastructure has enabled Chinese suppliers to embed proprietary collectors and frothers into overseas copper and iron ore operations, effectively extending domestic reagent standards and supply chains beyond China’s borders. This scale advantage is reinforcing China’s role as both a producer and system integrator of flotation reagents.

Regulatory mandates are simultaneously pushing chemical innovation. Under the 2025–2026 Work Plan issued by the Ministry of Industry and Information Technology, flotation reagent producers are required to cut VOC emissions by 15%, accelerating adoption of biodegradable fatty-acid-based collectors. On the supply side, Shaanxi Coal and Chemical Industry Co., Ltd. expanded capacity in 2024–2025 for high-selectivity frothers tailored to low-grade iron ore and complex sulfide deposits. Digitalization is reinforcing efficiency gains, with Shanghai-area plants piloting AI-driven dosing systems in late 2025 to reduce reagent waste by up to 10% through real-time sensor feedback.

Australia: Environmental Reformulation and Critical Minerals Driving Portfolio Shifts

Australia’s froth flotation chemicals market is being reshaped by environmental compliance and surging demand from critical minerals processing. From January 1, 2026, the Industrial Chemicals Environmental Management Standard will impose strict controls on mercury compounds and 1,2-dichloroethane, forcing rapid reformulation of legacy collectors that rely on restricted intermediates. This regulatory shift is accelerating the replacement of traditional xanthates and chlorinated chemistries with safer alternatives.

Trade and investment dynamics are amplifying this transition. The July 2024 interim free trade agreement between Australia and India targeting critical minerals processing has triggered 2025 investment into locally produced flotation reagents for lithium and rare earth separation. Innovation is also supplier-led. In 2025, Orica launched its Sustainable Ore initiative, introducing bio-based flotation reagents for gold and copper operations that align with institutional ESG requirements while maintaining recovery performance.

United States: Purity Scrutiny and Materials Science-Led Substitution

The United States froth flotation chemicals market is increasingly influenced by regulatory spillover effects and materials science innovation. Although MoCRA targets cosmetics, its enforcement has indirectly driven the U.S. Environmental Protection Agency to apply higher purity expectations to industrial reagents in 2026. This has implications for amine-based collectors used in phosphate and potash mining, where trace impurity control is becoming a procurement criterion.

State-level oversight is reinforcing transparency. The Minnesota Pollution Control Agency extended PFAS reporting deadlines to July 1, 2026, directly affecting manufacturers of fluorinated frothers that must now disclose precise PFAS content and functional roles. Innovation pathways are emerging in parallel. In January 2025, Super Copper Corporation launched a materials science division focused on chemical alternatives to conventional extraction reagents, targeting higher copper recovery yields in the Southwest while reducing environmental burden.

Brazil: Tailings Risk Reduction and Collaborative Reagent Design

Brazil’s froth flotation chemicals market is evolving around sustainability audits and collaborative reagent development. During 2024–2025, Clariant partnered with a major Brazilian mining group to co-develop customized flotation reagents for copper operations, prioritizing reduced effluent toxicity and improved biodegradability. This partnership model reflects growing preference for site-specific reagent design over standardized formulations.

Regulatory scrutiny of tailings management is further shaping demand. Following sustainability audits by the Brazilian National Mining Agency, iron ore producers have transitioned to low-dosage frothers to limit chemical volumes stored in tailings dams. This shift favors high-efficiency frothers that deliver recovery performance at lower concentrations, redefining purchasing criteria across Brazil’s bulk minerals sector.

South Africa: Energy Efficiency and Lithium-Linked Innovation

South Africa remains a critical innovation hub for advanced flotation technologies, driven by platinum group metals and emerging lithium opportunities. The 12th International Flotation Conference held in Cape Town in November 2025 marked a strategic inflection point, with Clariant unveiling its Decarbonization Minerals Program. New collectors for spodumene and safer sulfide depressants designed to replace sodium hydrosulfide were introduced, aligning flotation chemistry with decarbonization targets.

Operational efficiency is also advancing. South African PGM producers initiated pilots in 2026 for coarse particle flotation chemicals, enabling separation at larger grain sizes. This approach is projected to cut grinding energy consumption by around 20%, positioning reagent innovation as a lever for both cost reduction and emissions mitigation in deep-level mining.

Japan: Urban Mining and Battery Recycling Redefining Flotation Use Cases

Japan’s froth flotation chemicals market is defined by urban mining and secondary resource recovery rather than primary extraction. With limited domestic ore reserves, Japanese chemical firms are developing specialized collectors for rare earth recovery from electronic waste, particularly magnet scrap, using modified flotation techniques tailored to complex waste matrices.

Public-private collaboration is accelerating biodegradable solutions. In mid-2025, a government-funded academic-industry program successfully trialed biodegradable collectors for recovering cobalt and nickel from spent lithium-ion batteries. These pilots demonstrated improved recovery efficiency while reducing hazardous residues, positioning flotation chemistry as a core technology in Japan’s circular economy and battery recycling strategy.

Summary of Country-Level Strategic Drivers in the Froth Flotation Chemicals Market

Froth Flotation Chemicals Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Implications for Froth Flotation Chemicals

|

|

China

|

BRI mining scale and VOC mandates

|

Growth in biodegradable collectors and digital dosing

|

|

Australia

|

IChEMS standards and critical minerals

|

Rapid reformulation and bio-based reagents

|

|

United States

|

Purity scrutiny and PFAS disclosure

|

Shift toward high-purity, non-fluorinated frothers

|

|

Brazil

|

Tailings risk reduction

|

Demand for low-dosage, site-specific reagents

|

|

South Africa

|

Energy efficiency and lithium focus

|

Adoption of CPF chemicals and safer depressants

|

|

Japan

|

Urban mining and battery recycling

|

Specialized collectors for complex waste streams

|

Froth Flotation Chemicals Market Report Scope

Froth Flotation Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.7 Billion

|

|

Market Size (2034)

|

$4.3 Billion

|

|

Market Growth Rate

|

5.3%

|

|

Segments

|

By Reagent Type (Collectors, Frothers, Modifiers and Regulators, Flocculants), By Ore Type (Sulfide Ores, Oxide Ores, Non-Metallic Minerals, Rare Earth and Strategic Minerals), By Application (Mineral Processing, Wastewater Treatment, Pulp and Paper, Recycling and Secondary Recovery), By Form (Liquid, Powder and Solid)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Clariant AG, Solvay S.A., BASF SE, Orica Limited, Arkema S.A., Syensqo, Dow Inc., Huntsman Corporation, Nalco Water, Nouryon, Chevron Phillips Chemical Company, SNF Group, Shaanxi Coal and Chemical Industry Group, Kemcore, Air Products and Chemicals, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Froth Flotation Chemicals Market Segmentation

By Reagent Type

- Collectors

- Frothers

- Modifiers and Regulators

- Flocculants

By Ore Type

- Sulfide Ores

- Oxide Ores

- Non-Metallic Minerals

- Rare Earth and Strategic Minerals

By Application

- Mineral Processing

- Wastewater Treatment

- Pulp and Paper

- Recycling and Secondary Recovery

By Form

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Froth Flotation Chemicals Industry

- Clariant AG

- Solvay S.A.

- BASF SE

- Orica Limited

- Arkema S.A.

- Syensqo

- Dow Inc.

- Huntsman Corporation

- Nalco Water

- Nouryon

- Chevron Phillips Chemical Company

- SNF Group

- Shaanxi Coal and Chemical Industry Group

- Kemcore

- Air Products and Chemicals, Inc.

*- List not Exhaustive