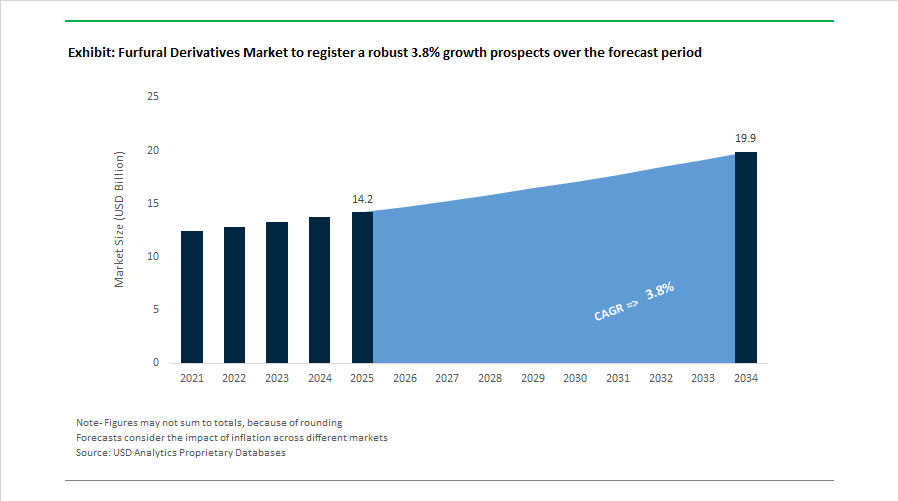

Furfural Derivatives Market to Reach $19.9 Billion by 2034 at 3.8% CAGR Driven by Biorefinery Expansion and Bio-Polymer Commercialization

The Furfural Derivatives Market is projected to grow from $14.2 billion in 2025 to $19.9 billion by 2034, registering a CAGR of 3.8% over the forecast period. Market expansion is anchored in the rising adoption of furfuryl alcohol, tetrahydrofurfuryl alcohol (THFA), 2-methylfuran, and FDCA as renewable chemical intermediates across foundry binders, bio-based polymers, lubricants, agrochemicals, and specialty solvents. Increasing regulatory scrutiny on fossil-derived chemicals and the acceleration of biomass valorization technologies are positioning furfural derivatives as strategic bio-based platform chemicals within the global circular economy.

In January 2025, Central Romana Corporation expanded its furfural production capacity to 90 million pounds annually in the Dominican Republic, responding to strong downstream demand from furan resin manufacturers and lubricant formulators. In February 2025, Sappi Limited announced a $60 million investment to construct a new furfural plant at its Saiccor Mill, targeting 25,000 tonnes per annum through valorization of hemicellulose streams. This integration of pulp by-products into high-value chemical intermediates reflects a growing trend of forestry-based biorefineries entering the furfural derivatives value chain. In July 2024, Hongye Holding Group disclosed a major expansion of its furfural and furfuryl alcohol capacity to serve global foundry and adhesive markets, reinforcing China’s position as a dominant production hub.

Polymer innovation is reshaping long-term demand fundamentals. In November 2024, Avantium N.V. initiated operations at the first section of its flagship FDCA plant in the Netherlands. FDCA is a critical derivative used to produce polyethylene furanoate (PEF), a fully bio-based and recyclable alternative to PET. Commercialization of FDCA and PEF represents a structural shift toward furan-based polymers in packaging, fibers, and barrier materials. In September 2025, Numaligarh Refinery Limited advanced its $4.4 billion downstream expansion, including a bamboo-based biorefinery processing 300,000 tonnes annually to produce bio-ethanol and furfural-derived chemicals. This large-scale bamboo-to-chemical platform signals diversification of feedstocks beyond agricultural residues into dedicated biomass supply chains.

Environmental compliance and emission controls are accelerating reformulation activity. In early 2025, implementation of the EU Industrial Emissions Directive stimulated more than $85 million in R&D investments to reduce formaldehyde content in furan resin systems, prompting development of ultra-low emission furfuryl alcohol derivatives for European foundries. In mid-2024, DynaChem South Africa introduced furfuryl alcohol-based binders for automotive castings designed to replace petrochemical resins with lower-emission alternatives. In January 2025, Shandong Yino Biologic Materials Co. completed modernization of its production base, incorporating advanced waste treatment and high-purity distillation systems to supply pharmaceutical and agrochemical-grade furfural.

Technological breakthroughs are enhancing yield economics and expanding derivative portfolios. In July 2025, researchers at the University of Twente demonstrated a catalytic process using boronate esters to significantly improve furfural selectivity and yield from biomass, with implications for cost reduction in 2-methylfuran and THFA production. In March 2025, International Flavors & Fragrances Inc. and dsm-firmenich reported a strategic pivot toward furan-based aroma chemicals to develop carbon-neutral fragrance platforms. In February 2026, DalinYebo marked over a century of furfural commercialization while outlining 2026 initiatives aimed at lowering production costs of furfural-derived intermediates for bioplastics applications.

The Furfural Derivatives Market trajectory reflects expansion of integrated biorefineries, polymer-grade FDCA commercialization, emission-compliant binder reformulations, and catalytic process intensification. Competitive positioning is increasingly influenced by feedstock diversification, biomass conversion efficiency, regulatory alignment in Europe, and downstream integration into bio-based plastics, lubricants, and specialty chemical segments.

Trends and Opportunities in the Global Furfural Derivatives Market

High-Purity Green Solvents for Semiconductors and Electronics Manufacturing

Electronics and semiconductor manufacturers are actively phasing out high-risk solvents such as N-Methyl-2-pyrrolidone under tightening occupational safety and environmental regulations. This shift has accelerated the adoption of bio-based furfural derivatives, particularly tetrahydrofurfuryl alcohol and 2-methylfuran, in precision cleaning, photoresist stripping, and electronic chemical formulations.

By 2025, qualification requirements for electronic-grade solvents have tightened significantly, with leading fabs demanding metallic impurity thresholds below 10 parts per billion. Tetrahydrofurfuryl alcohol is gaining preference due to its strong solvency, low volatility profile, and compatibility with sensitive substrates, allowing manufacturers to maintain yield stability while reducing toxic exposure risks. Industry validation trials reported in late 2025 indicate that furfural-derived solvents can achieve up to 98% efficiency in precision stripping applications, matching petroleum-based incumbents while delivering an estimated 30% reduction in lifecycle carbon footprint per liter. This performance parity, combined with regulatory resilience, is making furfural derivatives a long-term solvent strategy rather than a transitional substitute.

Scaling FDCA as a Core Bio-Based Platform for Sustainable Polyesters

2,5-Furandicarboxylic acid has emerged as one of the most commercially significant furfural derivatives, acting as a renewable replacement for purified terephthalic acid in advanced polyesters. FDCA-based polymers such as polyethylene furanoate are gaining traction due to superior barrier properties, offering up to six times better oxygen resistance and three times better water vapor resistance compared with conventional PET. These advantages directly support lightweight packaging, extended shelf life, and recyclability targets across food and beverage value chains.

Commercial-scale progress accelerated in 2025, with the FDCA segment projected to approach a valuation of nearly 800 million dollars by 2030. Feedstock security has become a central theme, prompting large-scale biorefinery investments. In September 2025, Engineers India Limited announced the completion of the Assam Bio Ethanol biorefinery, designed to produce 19,000 tons per annum of furfural from lignocellulosic biomass. This capacity provides a critical upstream supply base for FDCA and downstream polyester production in South Asia. Similarly, in February 2025, Sappi confirmed plans for commercial-scale furfural manufacturing at its Saiccor Mill, reinforcing Africa’s role as a strategic supplier of renewable chemical building blocks.

High-Value Pharmaceutical Intermediates and API Scaffolds

The furan ring structure is increasingly recognized as a versatile and efficient scaffold in pharmaceutical synthesis, particularly for antiviral, anti-inflammatory, and cardiovascular drug development. Furfural derivatives such as furfuryl alcohol, furfurylamine, and furoic acid are being integrated into multi-step synthesis routes due to their reactivity, chiral flexibility, and bio-based origin.

In May 2025, a low-cost antiviral synthesis pathway using furfuryl alcohol as a core building block gained global recognition, underscoring the growing relevance of furfural chemistry in drug manufacturing. Pharmaceutical-grade derivatives with purity levels of 99.9% or higher are now in strong demand, driven by both regulatory requirements and corporate sustainability commitments. Industry analysis indicates that leading pharmaceutical companies are allocating 15 to 20% of R&D budgets toward bio-based intermediates that can simultaneously support clinical performance and ESG reporting. This creates a high-margin opportunity for producers capable of delivering GMP-compliant, traceable furfural derivatives at scale.

Next-Generation Low-Emission Foundry Binder and Construction Systems

Although foundry binders remain the largest volume application for furfural derivatives, the opportunity lies in upgrading this demand toward low-emission, regulation-compliant systems. New public procurement policies introduced across parts of the Asia-Pacific region in September 2025 now mandate the use of eco-friendly binders in infrastructure projects. This is accelerating the transition toward furan-based binders with near-zero free formaldehyde and reduced volatile emissions.

Currently, furan resins account for approximately 70% of foundry binder usage, but tightening air quality and worker safety standards are driving continuous reformulation toward lower toxicity profiles. Beyond foundries, a high-value niche is emerging in construction and water systems through the use of furoic acid salts as non-toxic corrosion inhibitors. These derivatives offer a viable bio-based alternative to restricted chromates in concrete additives and cooling water treatment, aligning with global restrictions on heavy metals and carcinogenic inhibitors. As sustainability requirements become embedded in infrastructure spending, furfural derivatives are positioned to capture incremental demand across both traditional and adjacent industrial markets.

Furfural Derivatives Market Share and Segmentation Insights

Furfuryl Alcohol Leads Bio-Based Chemical Derivatives Through Dominance in Foundry Resin Applications

Furfuryl Alcohol accounted for 52.80% of the Furfural Derivatives Market share in 2025, making it the most significant derivative produced from furfural globally. Furfuryl alcohol is widely used as the primary raw material for manufacturing furan resins, which serve as essential binders in foundry sand molds and cores used for metal casting operations. These resins provide critical performance characteristics including high thermal resistance, dimensional stability, strong bonding strength, and controlled collapsibility after metal casting, making them indispensable in industrial casting applications. Because of this strong functional role, furfuryl alcohol consumes the majority of global furfural production. In 2025, market dynamics for furfuryl alcohol are influenced by evolving trends in the automotive and industrial manufacturing sectors, particularly as lightweight vehicle design and electrification influence casting demand. Despite these structural changes, demand for furfuryl alcohol remains stable because complex cast metal components used in engines, machinery housings, and industrial equipment continue to require high-performance foundry binder systems. Foundries are increasingly optimizing resin formulations to reduce furfuryl alcohol consumption per ton of casting while maintaining mold strength and thermal stability, ensuring efficient resource use while preserving the critical role of furfuryl alcohol within the global furfural derivatives market.

Foundry and Metal Casting Industry Drives the Largest Consumption of Furfural Derivatives

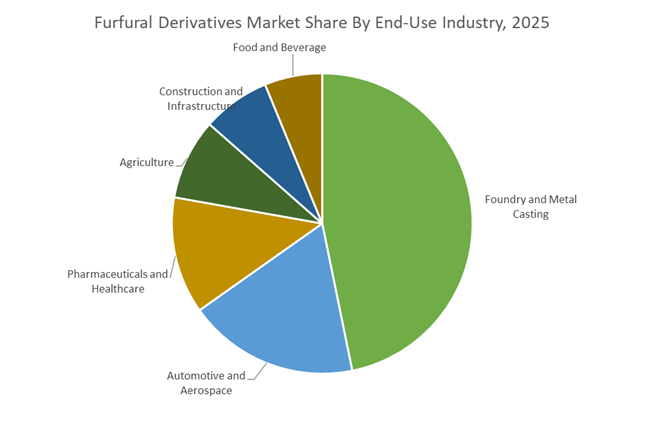

Foundry and Metal Casting represented 46.80% of the Furfural Derivatives Market share in 2025, establishing it as the leading end-use industry for furfural-based chemicals. Furfural derivatives—particularly furfuryl alcohol and furan resin binders—are essential in the production of sand molds and cores used to manufacture complex metal castings. These castings are widely used in industries such as automotive manufacturing, heavy equipment production, industrial machinery, and infrastructure components, where metal parts must withstand extreme mechanical and thermal stress. Furan-based binder systems are highly valued in foundry operations because they offer excellent mold strength, dimensional precision, and high-temperature resistance during molten metal pouring, enabling the production of complex geometries and high-quality cast components. In 2025, the foundry sector is also experiencing technological transformation driven by the growing adoption of additive manufacturing techniques for mold and core production. Binder jetting technology allows manufacturers to 3D print sand molds and cores using furan resin binder systems, enabling rapid prototyping and the production of highly complex internal geometries that are difficult or impossible to achieve with conventional pattern-based casting methods.

Competitive Landscape in Furfural Derivatives Market

Central Romana Dominates Global Furfural Capacity Through Bagasse Integration

Central Romana Corporation operates the largest single-site furfural production facility globally, with an annual capacity of approximately 90 million pounds, equivalent to 40,800 metric tons as of 2026. The company’s vertically integrated model leverages sugarcane bagasse from its own milling operations, creating a low-carbon, waste-valorized supply chain that reduces exposure to external biomass volatility. Its high-purity furfural serves primarily as a selective solvent in petroleum refining and as a critical feedstock for furfuryl alcohol manufacturing. In late 2025, Central Romana expanded its biorefinery efficiency, improving furfural yield per ton of processed bagasse to stabilize output amid global supply fluctuations. This scale advantage reinforces its leadership in the global bio-based furfural and derivative value chain.

Lenzing Integrates Furfural into European Biorefinery and Fiber Strategy

Lenzing AG is Europe’s largest producer of bio-based furfural, integrating chemical co-products within its wood-based dissolving pulp biorefinery model. Its LENZING™ Furfural Biobased grade is double-distilled for high purity and targets pharmaceutical intermediates and specialty resin applications in the EU market. In February 2026, Lenzing announced majority ownership of TreeToTextile AB, accelerating commercialization of next-generation bio-based fibers incorporating furan-derived chemistry. The company’s premiumization strategy emphasizes high-value co-products and alignment with its net-zero greenhouse gas emissions target by 2050. Operating biorefineries in Austria, Czechia, and Brazil, Lenzing has localized furfural supply to reduce logistics emissions and strengthen supply resilience for European specialty chemical customers.

Pennakem Expands Advanced Furan Solvent Technologies in North America

Pennakem, a subsidiary of the Minakem and Biolandes Group, is the leading North American specialist in furan-based green chemistry building blocks. During 2025 and early 2026, the company expanded production capacity for 2-methyltetrahydrofuran and tetrahydrofurfuryl alcohol, both positioned as sustainable alternatives to petroleum-derived tetrahydrofuran. A patent published in early 2026 outlines a single-step catalytic process converting furfuryl alcohol directly into 2-methyltetrahydrofuran, reducing energy consumption and process waste. Pennakem’s product portfolio includes eco-friendly binders and pharmaceutical-grade solvents aligned with Safe and Sustainable by Design principles. With approximately 175 employees in Pennsylvania, the company focuses on supplying high-purity, bio-based furfural derivatives to the North American pharmaceutical, coatings, and advanced materials sectors.

Hongye Strengthens Asia-Pacific Leadership in Furfuryl Alcohol and Resins

Hongye Holding Group remains a major vertically integrated producer in Asia-Pacific, a region accounting for more than 70% of global furfural demand. The company holds a substantial share of the furfuryl alcohol market, the largest derivative segment representing over 80% of total furfural consumption in 2026. Its portfolio spans furan resins, furfuryl ketone resins, and bio-based additives for paper-making and industrial applications. In January 2026, Hongye updated specifications for its 98.5% purity furfural to meet stringent requirements in lube oil refining and pesticide active ingredient production. Investments in closed-loop manufacturing systems support compliance with China’s 2026 VOC emission standards, reinforcing its environmental-chemical integration strategy.

Illovo Advances Biorefinery Evolution in African Furfural Supply

Illovo Sugar Africa is the continent’s largest sugar producer and a significant global supplier of furfural derived from sugarcane bagasse. During the 2025 and 2026 cycle, Illovo intensified its biorefinery evolution strategy, maximizing value extraction from bagasse through furfural and ethanol production. In early 2026, the company reported converting more than 95% of bagasse into energy or chemical feedstock, significantly reducing mill waste. Illovo supplies furfural to European and Asian foundry sectors for the production of furan resins used in metal casting. Its geographic position in South Africa enables efficient export access to both European green chemistry markets and rapidly industrializing Asian manufacturing hubs, strengthening its role in the global furfural derivatives supply chain.

India: Biorefinery Scale-Up and Solvent Substitution

India is rapidly repositioning itself in the furfural derivatives market through large-scale biorefinery investments and regulatory support. In August 2025, Japan approved 60 billion yen in financing for the Assam bamboo-based biorefinery, designed to process 5 million metric tons of biomass annually and produce 19,000 metric tons of furfural and downstream derivatives. This project materially reduces India’s import dependence for foundry resins and specialty chemicals.

Policy alignment is accelerating adoption. Under the MNRE biomass program, FY 2025–26 incentives prioritized advanced continuous distillation systems, improving furfural-to-alcohol conversion efficiency by 33%. The Numaligarh biorefinery, nearing commissioning in late 2025, targets furfuryl alcohol for domestic foundry and aerospace uses. Concurrently, 2025 chemical safety guidelines promoting green solvents have driven a marked shift toward furan-based solvents across pharmaceuticals and industrial cleaning.

China: Export Scale and Battery-Linked Derivatives

China retains its dominance in furfural derivatives through scale, automation, and downstream battery integration. MIIT’s September 2025 directive elevated high-purity electronic-grade furfural derivatives as strategic materials for semiconductor encapsulation and lithium-ion gel electrolytes. Large producers in Hebei and Shandong integrated AI-driven process controls, cutting energy intensity by roughly 15% per ton of furfuryl alcohol.

Innovation is extending into energy storage. Mid-2025 commissioning of a 1,000-ton-per-year porous carbon line derived from furan precursors positions China at the forefront of sodium-ion battery anode materials ahead of 2026 commercialization, expanding furfural’s role beyond traditional resins.

United States: Bio-Monomer Substitution and Feedstock Innovation

In the United States, furfural derivatives are gaining traction as renewable substitutes for petrochemical monomers. Expanded eligibility under the Renewable Fuel Standard in 2025 encouraged investment in tetrahydrofuran derived from furfural, supporting high-performance polymer production. Companies such as Ingevity and Pennakem advanced furan-based coatings for corrosion protection in EV battery housings.

Feedstock innovation is progressing in parallel. USDA-backed pilot projects in the Midwest demonstrated corncob-to-furfural yields exceeding traditional benchmarks, targeting 2026 commercial deployment for sustainable resin binders.

Japan: Regulatory Substitution and Automotive Composites

Japan’s furfural derivatives market is being reshaped by regulatory substitution and green partnerships. With Class I chemical prohibitions effective June 17, 2026, the Ministry of Economy, Trade and Industry is driving rapid adoption of furfural-based surface treatment agents in electronics. Strategic collaborations following Japan’s investment in India are also advancing bio-based furan resin matrices for lightweight automotive composites, targeting measurable weight reduction in next-generation hybrid vehicles.

South Africa and European Union: Biomass Valorization and Circular Materials

South Africa is reinforcing its role as a sustainable furfural supplier through biomass valorization. Sappi expanded its furfural pilot plant in early 2025 and is evaluating commercial integration with cellulose mills, while Illovo Sugar optimized bagasse-based extraction to supply European foundries.

Within the European Union, Horizon Europe funding launched new flagship biorefineries in 2025 focused on FDCA production for polyethylene furanoate, positioning furfural derivatives at the center of the next sustainable packaging cycle. Lenzing AG further advanced circularity by supplying high-purity furfural by-products to the fragrance and flavor industry.

Summary: Furfural Derivatives Market Country Drivers

Furfural Derivatives Market County Level Snapshot

|

Region

|

Strategic Focus

|

Market Implication

|

|

India

|

Biorefineries and green solvents

|

Import substitution and capacity growth

|

|

China

|

Scale and battery integration

|

Leadership in electronic-grade derivatives

|

|

United States

|

Renewable monomers

|

Expansion in polymers and EV coatings

|

|

Japan

|

Regulatory substitution

|

Shift to bio-based surface treatments

|

|

EU & South Africa

|

Circular bio-refining

|

FDCA, PEF, and specialty derivatives

|

Furfural Derivatives Market Report Scope

Furfural Derivatives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$14.2 Billion

|

|

Market Size (2034)

|

$19.9 Billion

|

|

Market Growth Rate

|

3.8%

|

|

Segments

|

By Derivative Type (Furfuryl Alcohol, Tetrahydrofurfuryl Alcohol, Furoic Acid, Bio-based Tetrahydrofuran, 2,5-Furandicarboxylic Acid, Methyl Tetrahydrofuran, Furfurylamine), By Raw Material (Corn Cobs, Sugarcane Bagasse, Rice Husks, Bamboo and Wood Residues, Cotton and Oat Hulls), By Application (Resins and Binders, Solvents, Chemical Intermediates, Fuel Additives, Corrosion Inhibitors), By End-Use Industry (Foundry and Metal Casting, Automotive and Aerospace, Pharmaceuticals and Healthcare, Agriculture, Food and Beverage, Construction and Infrastructure)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Lenzing AG, Pennakem, LLC, Jinan Shengquan Group, Hongye Holding Group Corporation Ltd., Illovo Sugar Africa (Pty) Ltd., Central Romana Corporation, Ingevity Corporation, BASF SE, TransFurans Chemicals bvba, Silvateam S.p.A., KRBL Limited, Arcoy Biorefinery Pvt. Ltd., Nova Molecular Technologies, Avantium N.V., Xingtai Chunlei Furfuryl Alcohol Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Furfural Derivatives Market Segmentation

By Derivative Type

- Furfuryl Alcohol

- Tetrahydrofurfuryl Alcohol

- Furoic Acid

- Bio-based Tetrahydrofuran

- 2,5-Furandicarboxylic Acid

- Methyl Tetrahydrofuran

- Furfurylamine

By Raw Material

- Corn Cobs

- Sugarcane Bagasse

- Rice Husks

- Bamboo and Wood Residues

- Cotton and Oat Hulls

By Application

- Resins and Binders

- Solvents

- Chemical Intermediates

- Fuel Additives

- Corrosion Inhibitors

By End-Use Industry

- Foundry and Metal Casting

- Automotive and Aerospace

- Pharmaceuticals and Healthcare

- Agriculture

- Food and Beverage

- Construction and Infrastructure

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Furfural Derivatives Industry

- Lenzing AG

- Pennakem, LLC

- Jinan Shengquan Group

- Hongye Holding Group Corporation Ltd.

- Illovo Sugar Africa (Pty) Ltd.

- Central Romana Corporation

- Ingevity Corporation

- BASF SE

- TransFurans Chemicals bvba

- Silvateam S.p.A.

- KRBL Limited

- Arcoy Biorefinery Pvt. Ltd.

- Nova Molecular Technologies

- Avantium N.V.

- Xingtai Chunlei Furfuryl Alcohol Co., Ltd.

*- List not Exhaustive