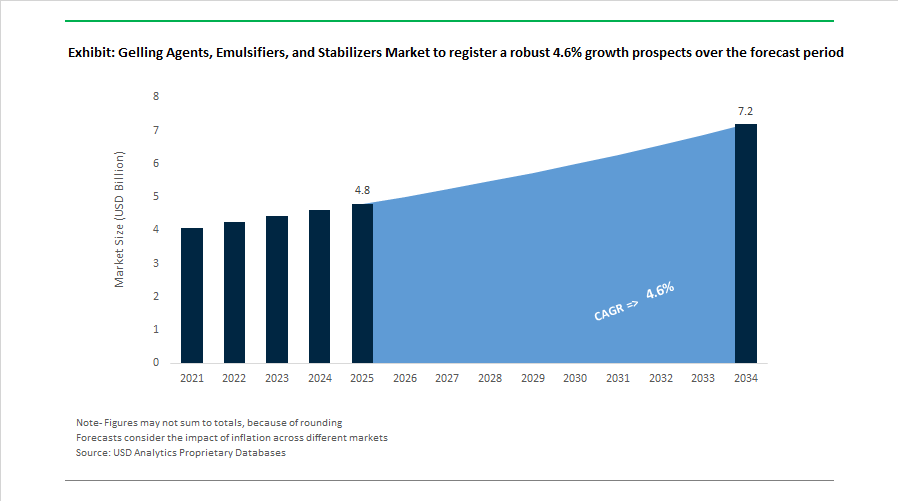

Gelling Agents, Emulsifiers, and Stabilizers Market to Reach $7.2 Billion by 2034 at 4.6% CAGR Driven by Hydrocolloid Consolidation and Clean-Label Reformulation

The Gelling Agents, Emulsifiers, and Stabilizers Market is projected to grow from $4.8 billion in 2025 to $7.2 billion by 2034, registering a CAGR of 4.6%. Market expansion is fueled by rising demand for hydrocolloids, enzyme-based texturants, lecithin emulsifiers, modified starch stabilizers, and plant-based protein systems across bakery, dairy, confectionery, sauces, and alternative protein applications. Structural shifts toward clean-label formulations, allergen-free emulsifiers, fermentation-derived stabilizers, and plant-based dairy analogues are reshaping ingredient portfolios across global food and beverage manufacturing.

In September 2024, Cargill Incorporated inaugurated a new sunflower lecithin facility targeting non-GMO and allergen-free emulsifier demand in confectionery, bakery, and dairy systems. In November 2024, Tate & Lyle PLC finalized its $1.8 billion acquisition of CP Kelco, consolidating pectin, carrageenan, xanthan gum, and gellan gum capabilities with sweetener and fortification technologies. The transaction creates a vertically integrated platform for advanced texture, mouthfeel optimization, and shelf-life stabilization across processed foods. In November 2024, Kerry Group introduced an enzyme-emulsifier blend designed to replace synthetic mono- and diglycerides in industrial bread production, enabling manufacturers to remove chemical emulsifiers while maintaining volume, softness, and crumb structure.

Capacity expansion and portfolio realignment intensified in 2025. In February 2025, Ingredion Incorporated announced a $100 million modernization of its Indianapolis facility, scheduled for completion in late 2026, focused on advanced starch-based texturants and gelling agents with improved production efficiency and lower greenhouse gas emissions. The company also commercialized VITESSENCE® Pulse 1853 pea protein isolate during 2024–2025, a dual-functional ingredient offering protein fortification and stabilizing performance in plant-based dairy applications. In February 2025, Corbion N.V. launched a clean-label emulsification solution for refrigerated sauces and dressings, replacing titanium dioxide and certain modified starches while improving viscosity stability and surface cling. In 2024, Palsgaard A/S expanded its PGPR production capacity in the Netherlands to 11,500 metric tons annually, addressing rising demand in chocolate and vegan spreads.

Strategic divestments and vertical integration reshaped competitive positioning between 2024 and 2026. In 2024, Kingswood Capital Management acquired Corbion’s emulsifier business for $362 million, establishing a focused emulsifier platform in North America. In February 2025, Novonesis agreed to acquire dsm-firmenich’s share of the Feed Enzyme Alliance for €1.5 billion, integrating specialty enzymes used as functional stabilizers in animal nutrition. In May 2025, dsm-firmenich acquired a European biotech startup specializing in enzymatic emulsification, reinforcing fermentation-based stabilizer development for dairy and bakery systems. In February 2026, dsm-firmenich divested its Animal Nutrition & Health division to CVC Capital Partners for €2.2 billion, finalizing its strategic pivot toward human nutrition and consumer-grade gelling and stabilizing solutions.

The Gelling Agents, Emulsifiers, and Stabilizers Market outlook reflects hydrocolloid consolidation, enzyme-driven clean-label reformulation, sunflower lecithin expansion, PGPR capacity scaling, fermentation-derived emulsifier innovation, and plant-based dairy stabilization technologies. Competitive differentiation increasingly centers on mouthfeel optimization, allergen-free ingredient sourcing, vertical enzyme integration, sustainability-linked manufacturing upgrades, and regulatory-compliant label simplification across global food processing value chains.

Gelling Agents, Emulsifiers, and Stabilizers (GES) Market Trends and Strategic Growth Opportunities

Clean-Label Engineering Redefines Starch and Cellulose-Based Texturants

The global gelling agents, emulsifiers, and stabilizers market is experiencing a decisive shift toward clean-label ingredient engineering as food manufacturers respond to tightening regulatory scrutiny and evolving consumer expectations for transparency. Chemically modified starches are increasingly being replaced by enzymatic and physical modification techniques that deliver comparable functionality while enabling simplified ingredient declarations. In 2024, Ingredion launched NOVATION Indulge 2920, a functional native corn starch designed to replicate the fat-mimetic and viscosity-building properties of modified starches while retaining a simple “starch” or “cornflour” label. This innovation is particularly relevant in Europe, where reformulation pressure has intensified under nutritional profiling guidelines, enabling food manufacturers to achieve fat and oil reductions exceeding 30% in sauces and dairy desserts without compromising texture.

Enzymatic modification is emerging as the fastest-growing technological pathway within clean-label texturants. By mid-2025, enzymatically modified starches had outpaced traditional chemical cross-linking due to their ability to deliver acid stability, freeze-thaw resistance, and shear tolerance required for ultra-high temperature processing. Capacity expansion is reinforcing this trend. In June 2025, Ingredion secured final regulatory approval for its joint venture with AGRANA in Romania, significantly strengthening supply of clean-label potato and corn starches to Eastern Europe and fast-growing Asian processed food markets. These developments indicate that clean-label functionality is no longer a premium niche but a structural requirement across mainstream food categories.

Fermentation-Derived and Seaweed Polysaccharides Gain Commercial Dominance

Innovation in microbial and marine polysaccharides is reshaping the stabilizer segment of the GES market, driven by the need for high performance at ultra-low inclusion rates. High-acyl gellan gum has emerged as a preferred solution for suspension challenges in fortified beverages, particularly plant-based milks. In early 2025, CP Kelco, now part of Tate & Lyle, expanded its gellan gum portfolio to support calcium and protein suspension at concentrations as low as 0.03 to 0.035%. This performance enables manufacturers to replace costlier or label-sensitive stabilizers while maintaining clean mouthfeel and visual appeal.

The strategic integration of Tate & Lyle and CP Kelco, completed in November 2024, has created a global leader in specialty hydrocolloids. The combined capabilities are accelerating development of multi-hydrocolloid systems that deliver synergistic stability in acidic and high-protein formulations. Parallel to fermentation advances, seaweed-derived stabilizers are benefiting from circular economy investments. By June 2025, the global seaweed by-products market had reached an estimated value of 5 billion dollars, supported by sourcing initiatives from players such as Cargill focused on traceable red and brown algae for pharmaceutical and cosmetic-grade gelling applications.

Advanced GES Systems Enable Next-Generation Plant-Based and Cultivated Foods

The rapid evolution of plant-based and cultivated foods is creating strong demand for advanced, multi-component gelling and emulsifying systems capable of replicating the sensory complexity of animal-derived products. Achieving realistic fibrous texture, fat distribution, and heat stability requires coordinated functionality across stabilizers, emulsifiers, and gelling agents. In January 2024, Unilever, IFF, and Wageningen University launched a four-year collaborative program focused on managing flavor-protein interactions in plant-based meats. The initiative highlights the critical role of GES systems in masking off-notes while delivering the fibrous bite expected by flexitarian consumers.

In animal-free dairy, precision fermentation is opening new commercial pathways. During 2024 and 2025, ADM partnered with New Culture to accelerate animal-free mozzarella production using fermented casein. These formulations rely on highly specialized stabilizer and emulsifier systems to replicate melt and stretch performance. At IFFA 2025, Hydrosol and Planteneers introduced PLUSmulson stabilizing systems for hybrid meat-vegetable products, enabling reduced meat content while maintaining authentic texture and fat stability under high-heat cooking.

Heat-Stable GES Solutions for Retort and Shelf-Stable Ready Meals

Growth in shelf-stable ready-to-eat and ready-to-cook meals is creating a significant opportunity for GES systems that can withstand retort sterilization at temperatures reaching 121 degrees Celsius. Late 2024 technical evaluations indicate that starch-pectin and high-acyl gellan gum blends are becoming the industry benchmark for preventing syneresis in sauces stored for up to 24 months. These systems maintain homogeneity through extreme thermal cycling, preserving consumer appeal in long-life products.

High-protein ready-to-cook snacks are further expanding demand for robust, clean-label binding systems. In May 2025, Hydrosol presented its HydroTOP High Gel range, formulated to deliver consistent texture and juiciness in low-meat and low-fish recipes subjected to severe heat processing and ambient storage. As global meal-kit and convenience food consumption rises, heat-stable, E-number-free gelling and stabilizing solutions are positioned to become a core growth engine within the global GES market.

Gelling Agents, Emulsifiers, and Stabilizers Market Share and Segmentation Insights

Emulsifiers Lead Functional Ingredient Demand in the Gelling Agents, Emulsifiers, and Stabilizers Market

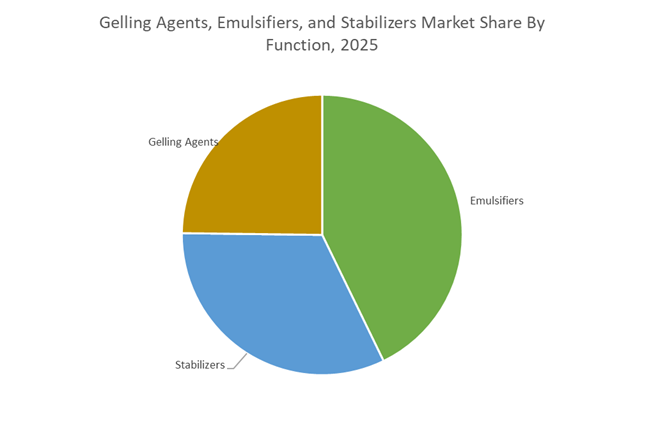

Emulsifiers accounted for 42.80% of the Gelling Agents, Emulsifiers, and Stabilizers Market share in 2025, making them the dominant functional category across multiple formulation-intensive industries. Emulsifiers such as mono- and diglycerides, lecithin, polysorbates, diacetyl tartaric acid esters of monoglycerides (DATEM), and sucrose esters are critical for creating and maintaining stable oil-in-water and water-in-oil emulsions used extensively in food processing, cosmetics, and pharmaceutical formulations. These ingredients play a central role in improving texture, product stability, shelf life, and sensory consistency in products such as bakery goods, dairy beverages, sauces, creams, and lotions. In 2025, the emulsifier segment is undergoing rapid reformulation driven by the clean label movement within food and personal care industries. Manufacturers are increasingly replacing traditional synthetic emulsifiers with plant-derived alternatives such as sunflower lecithin, quillaja saponin extracts, and plant protein emulsifier systems. These natural emulsifiers allow brands to maintain functional performance while aligning with consumer demand for recognizable, minimally processed ingredients, accelerating innovation across the global gelling agents, emulsifiers, and stabilizers market.

Food and Beverage Industry Drives the Largest Demand for Gelling Agents, Emulsifiers, and Stabilizers

Food and Beverage represented 58.70% of the Gelling Agents, Emulsifiers, and Stabilizers Market share in 2025, establishing it as the largest application segment for these functional food ingredients. Food manufacturers rely heavily on hydrocolloids and functional additives to control texture, stability, viscosity, and mouthfeel, all of which are essential attributes influencing consumer acceptance of processed foods. Gelling agents provide structural integrity in products such as confectionery, desserts, and jellies, while emulsifiers stabilize sauces, dressings, and dairy emulsions, and stabilizers prevent ice crystal formation in frozen desserts and maintain suspension in beverages. In 2025, the food sector is experiencing transformative growth driven by the rapid expansion of plant-based dairy alternatives and meat analog products. Replicating the texture, creaminess, and structural properties of traditional animal-based foods requires advanced hydrocolloid and emulsifier systems, including specialized blends of carrageenan, pectin, xanthan gum, and plant protein emulsifiers. These ingredient systems are specifically engineered to mimic the melting behavior of cheese, the creaminess of yogurt, and the fibrous texture of meat alternatives, driving strong demand across the food ingredient market.

Competitive Landscape in Gelling Agents, Emulsifiers, and Stabilizers Market

Tate and Lyle Strengthens Global Leadership Through CP Kelco Integration

Following completion of the CP Kelco acquisition in late 2024, Tate and Lyle has established the industry’s most comprehensive mouthfeel solutions portfolio, spanning pectins, xanthan gum, gellan gum, and specialty starches. The integration positions the company as a leader in texture systems for yogurt stabilizers, plant-based dairy emulsification, and indulgent dessert formulations. In September 2025, the launch of Tate and Lyle Sensation™ in Asia-Pacific introduced a precision sensory mapping platform that links consumer mouthfeel preferences to ingredient functionality. For 2026, the company is aligning innovation with GLP-1 influenced dietary trends, researching fiber-rich stabilizers that enhance satiety while maintaining palatability. Expansion across China and Southeast Asia supports growth in high-protein dairy alternatives and spoonable fermented products.

Cargill Expands Cost-Optimized and Digital Texture Platforms

Cargill maintains a diversified hydrocolloid and emulsifier portfolio that includes lecithin, carrageenan, seaweed-derived stabilizers, and pectin replacers. In March 2025 and 2026, the company introduced cost-optimized pectin alternatives aimed at mitigating price volatility in beverage and bakery applications. Natural gelling agents now represent 55.5% of value demand, prompting Cargill to expand plant-based dairy stabilizer systems with label-friendly positioning. Its Digitalization of Texture strategy incorporates AI-controlled viscosity monitoring to reduce production variability and material waste. With a strong footprint in global food additives and ingredient distribution, Cargill remains positioned to capitalize on functional beverage stabilization and clean-label reformulation trends.

ADM Leverages Field to Market Integration in Plant-Based Emulsifiers

Archer Daniels Midland Company holds approximately 11% of the global food additive market and continues to expand its plant-based emulsifier and stabilizer offerings. In August 2025, ADM introduced new emulsifier systems tailored for oat and almond milk, enhancing suspension stability and improving shelf life in dairy alternatives. The company remains a dominant lecithin producer, sourcing from soy, canola, and sunflower through a vertically integrated grower network that ensures non-GMO and sustainably certified supply. ADM’s legacy in emulsifier science supports applications across bakery improvers, confectionery dispersion systems, and industrial coatings. Its field-to-market supply chain resilience provides pricing stability amid agricultural commodity fluctuations.

IFF Advances Functional Emulsifiers and Heat-Stable Hydrocolloids

IFF’s Nourish division, strengthened by the integration of DuPont Nutrition and Biosciences, markets established brands such as DIMODAN® and PANODAN® for bakery and confectionery structure optimization. These emulsifiers regulate starch interaction, improve crumb softness, and enhance fat crystallization control in industrial-scale baking. IFF formulations also increase extrusion efficiency in pet food manufacturing and reduce processing time in high-throughput bakeries. In July 2025, the company expanded gellan gum systems in Japan for ready-to-drink beverages requiring superior heat stability and suspension performance. All emulsifiers are derived from vegetable oils with RSPO and RTRS traceability, reinforcing sustainability leadership in global food ingredient markets.

Ingredion Focuses on Clean-Label Texture and Functional Starch Innovation

Ingredion continues to expand its clean-label starches, carrageenan blends, and non-GMO thickening systems across food and pharmaceutical applications. In July 2025, the company broadened its functional texturizer portfolio to improve processing efficiency in ultra-processed foods while maintaining ingredient transparency. In August 2025, it launched a sustainably sourced carrageenan blend for pharmaceutical capsules, aligned with FDA clean-label standards for advanced drug delivery. Ingredion emphasizes texture as a differentiator, developing immersive formats such as aerated snacks and layered mochi-style products to meet evolving Gen Z and Millennial preferences. Its presence in the United States gelling and thickening segment supports strong positioning in bakery, dairy, confectionery, and nutraceutical stabilization systems.

United States: Precision Fermentation, GRAS Tightening, and Texture Science Investments

The United States remains a global innovation nucleus for gelling agents, emulsifiers, and stabilizers, driven by capital-intensive modernization and regulatory recalibration. In February 2025, Ingredion Incorporated announced a USD 100 million modernization program at its Indianapolis facility, complemented by a USD 50 million expansion at Cedar Rapids focused on specialty industrial starches. These investments are strategically aligned with demand for advanced texture systems in food packaging, papermaking, and clean-label food formulations, reinforcing the U.S. leadership in multifunctional hydrocolloids and modified starch-based stabilizers.

Regulatory and technological shifts are reshaping product development pathways. In March 2025, the U.S. FDA initiated reforms to the GRAS framework, significantly narrowing the approval funnel for novel bio-active emulsifiers and stabilizers. By Q3 2025, only 50 of 82 submissions received “no questions” letters, raising the compliance threshold for innovation. Against this backdrop, Ingredion’s May 2025 move to secure exclusive access to fermented Reb M technology following the RealSweet wind-down underscores a broader pivot toward precision fermentation as a scalable route to high-intensity stabilizers and sweeteners. Parallel innovation was visible in AgriFiber Solutions’ successful closure of GRN 998 for corn bran arabinoxylan, validated as a multifunctional gelling and binding agent in high-fiber dairy beverages. Additionally, Moolec Science’s 2025–2026 commercial deliveries of GLASO™, a high-GLA safflower oil, introduced a differentiated lipid-based emulsifier tailored for premium CPG formulations.

European Union: Regulatory Enablement and Plant-Based Texturizer Scale-Up

The European Union’s gelling agents and emulsifiers landscape is being reshaped by regulatory enablement aligned with sustainability and food waste reduction goals. Regulation (EU) 2025/651, effective April 2025, amended the core food additives framework to authorize mono- and diglycerides (E 471) and lecithins (E 322) as glazing agents and carriers for fresh produce such as cassava, kiwi, and passion fruit. This regulatory change has expanded the functional use of emulsifiers beyond processed foods, opening new application corridors in fresh produce preservation.

Scientific guidance updates from the European Food Safety Authority in mid-2025 further reinforced clean-label momentum. EFSA’s re-evaluation focus on fermentation-derived steviol glycosides (E 960b) and buffered vinegar (E 267) is accelerating the substitution of synthetic stabilizers with bio-based and fermentation-enabled alternatives. On the supply side, regulatory approval in June 2025 for the Agrana–Ingredion joint venture in Romania established a strategic production hub for specialty starch texturizers engineered to meet European Green Deal benchmarks. At the ingredient innovation level, Alland & Robert scaled SYNDEO GELLING, a gum acacia-based hydrocolloid blend, positioning it as a direct plant-based replacement for gelatin in confectionery and reinforcing Europe’s leadership in vegan gelling systems.

China: Bio-Based Hydrocolloids and Seaweed Supply Chain Dominance

China’s gelling agents and emulsifiers industry is being actively steered by industrial policy and raw material scale advantages. Under the MIIT Green Chemistry Action Plan for 2025–2026, the Ministry of Industry and Information Technology mandated a 12% increase in the adoption of bio-based emulsifiers, catalyzing large-scale investments in seaweed-derived hydrocolloids across Shandong and Fujian. This policy intervention is directly strengthening China’s domestic supply of carrageenan and agar, which are critical for pharmaceutical excipients, dairy stabilization, and functional beverage applications.

Supply chain dominance remains a defining feature. In 2025, China consolidated its position as the world’s largest producer of red seaweed, with new aquaculture infrastructure designed to stabilize carrageenan availability amid rising domestic demand. At the branded ingredient level, Yihai Kerry leveraged its vertically integrated rice bran ecosystem to launch high-oryzanol emulsifying oils into international markets in March 2025. These oils are increasingly positioned for functional bakery and nutrition applications, signaling China’s shift from volume-driven hydrocolloid exports toward value-added emulsifier systems.

India: PLI-Backed Capacity Build-Out and Natural Emulsifier Exports

India’s gelling agents and stabilizers sector is undergoing rapid capacity expansion supported by fiscal incentives and corporate consolidation. Following the acquisition of the Heubach Group, Sudarshan Chemical Industries integrated high-performance fatty acid derivatives into its portfolio, strengthening India’s role as a cost-competitive exporter of industrial-grade emulsifiers with consistent purity profiles. This consolidation has enhanced India’s ability to serve global coatings, plastics, and food processing markets.

Policy support has been equally decisive. The 2025–26 Union Budget extended Production Linked Incentives to specialty food chemicals, triggering an estimated ₹500 crore surge in private investment for guar gum and plant-based stabilizer refineries. Concurrently, Ricela Health Foods Limited announced significant capital expenditure to expand gamma oryzanol extraction, targeting 17% revenue growth in FY 2026 by supplying antioxidant-rich emulsifiers to global wellness and functional food brands. Together, these developments position India as a scalable source of natural, plant-derived gelling and emulsifying systems.

South Africa: Bio-Circular Stabilizers and Industrial Dispersant Innovation

South Africa is emerging as a niche innovator in bio-circular stabilizers derived from forestry and sugar value chains. In 2025, Sappi completed the commercial scale-up of its Saiccor biorefinery pilot, converting hemicellulose side-streams into lignin-based stabilizers and dispersants for construction materials and industrial coatings. This approach reduces reliance on petrochemical stabilizers while embedding circular economy principles into heavy-industry applications.

Complementing this, Illovo Sugar Africa optimized its bagasse-to-furfural pipeline throughout 2025, supplying key intermediates for furan-based emulsifiers used in regional agrochemicals. These initiatives underscore South Africa’s role as a supplier of bio-derived functional additives rather than conventional food hydrocolloids, with growing relevance in industrial and agricultural formulations.

Comparative Snapshot: Gelling Agents, Emulsifiers, and Stabilizers by Region

Gelling Agents, Emulsifiers, and Stabilizers Market County Level Snapshot

|

Region

|

Strategic Focus

|

Industry Implication

|

|

United States

|

Precision fermentation and GRAS tightening

|

Higher compliance thresholds, premium texture solutions

|

|

European Union

|

Regulatory enablement and vegan hydrocolloids

|

Expansion of plant-based and clean-label applications

|

|

China

|

Seaweed-based hydrocolloids and policy-driven bio-emulsifiers

|

Scaled supply with rising value-added exports

|

|

India

|

PLI-backed capacity expansion

|

Cost-efficient natural emulsifier production

|

|

South Africa

|

Bio-circular industrial stabilizers

|

Niche leadership in sustainable dispersants

|

Gelling Agents, Emulsifiers, and Stabilizers Market Report Scope

Gelling Agents, Emulsifiers, and Stabilizers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.8 Billion

|

|

Market Size (2034)

|

$7.2 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Function (Gelling Agents, Emulsifiers, Stabilizers), By Source (Plant-Based, Seaweed-Based, Microbial and Fermentation-Based, Animal-Derived, Synthetic and Semi-Synthetic), By Application (Food and Beverage, Pharmaceuticals, Cosmetics and Personal Care, Industrial and Technical), By Form (Powdered and Granular, Liquid and Paste, Flakes)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ingredion Incorporated, Archer Daniels Midland Company, Cargill, Incorporated, Kerry Group plc, CP Kelco, Tate and Lyle PLC, BASF SE, DSM-Firmenich, International Flavors and Fragrances Inc., Corbion N.V., Palsgaard A/S, Ashland Inc., Alland and Robert, Jinan Shengquan Group, Sudarshan Chemical Industries Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Gelling Agents, Emulsifiers, and Stabilizers Market Segmentation

By Function

- Gelling Agents

- Emulsifiers

- Stabilizers

By Source

- Plant-Based

- Pectin

- Guar Gum

- Gum Arabic

- Starch

- Lecithin

- Seaweed-Based

- Carrageenan

- Agar

- Alginates

- Microbial and Fermentation-Based

- Animal-Derived

- Synthetic and Semi-Synthetic

- Carboxymethyl Cellulose

- Mono- and Diglycerides

- Polysorbates

By Application

- Food and Beverage

- Pharmaceuticals

- Cosmetics and Personal Care

- Industrial and Technical

By Form

- Powdered and Granular

- Liquid and Paste

- Flakes

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Gelling Agents, Emulsifiers, and Stabilizers Industry

- Ingredion Incorporated

- Archer Daniels Midland Company

- Cargill, Incorporated

- Kerry Group plc

- CP Kelco

- Tate and Lyle PLC

- BASF SE

- DSM-Firmenich

- International Flavors and Fragrances Inc.

- Corbion N.V.

- Palsgaard A/S

- Ashland Inc.

- Alland and Robert

- Jinan Shengquan Group

- Sudarshan Chemical Industries Limited

*- List not Exhaustive