Market Overview: Regulatory-Grade, Traceable, and Sustainable IVD Packaging Scales With Decentralized Testing

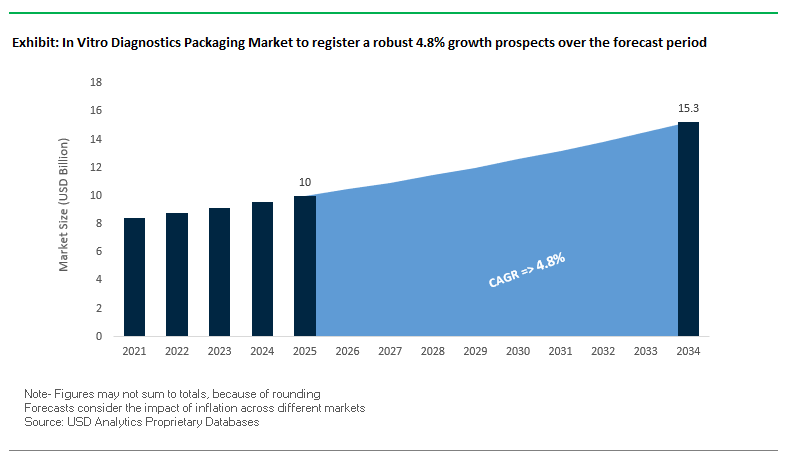

The In Vitro Diagnostics (IVD) Packaging Market is valued at USD 10.0 billion in 2025 and is projected to reach USD 15.2 billion by 2034, registering a CAGR of 4.8%. For industry buyers, the core question is how to secure sterility, stability, and end-to-end traceability while accelerating launches of point-of-care (PoC) and self-testing kits. The market is defined by compliance-first design (e.g., IVDR documentation and UDI/serialization), digital traceability (RFID/NFC smart labels for condition monitoring), and materials engineering that preserves reagent efficacy across global cold chains. Packaging must also enable single-use, pre-filled, tamper-evident formats that work reliably outside clinical settings, and increasingly align with sustainability goals through recycle-ready laminates and responsible material choices. Multi-stakeholder expectations from regulators to hospital systems, retail pharmacies, and e-commerce are pushing suppliers to deliver high-performance primary containers, sterile barrier systems, and data-rich secondary packs that protect product integrity and brand trust.

Key Insights for Industry Professionals:

- Growth vector: USD 10.0B (2025) → 15.2B (2034) at 4.8% CAGR, led by PoC and self-testing adoption.

- Compliance pressure: IVDR-level documentation, UDI/serialization, and robust technical files are now baseline.

- PoC packaging shift: Demand rises for single-use, pre-filled, tamper-evident kits suited to non-clinical environments.

- Smart packaging: RFID/NFC labels for real-time temperature/humidity/location monitoring to protect reagent efficacy.

- Sustainability: Recycled content and recycle-ready mono-material solutions gain traction without compromising barrier.

Market Analysis: Digitally Traceable, PoC-Ready, and Regulation-Driven IVD Packaging

Recent developments show the sector converging on localization, digitalization, and sustainable materials. In August 2025, Schott initiated local production of syringe and cartridge glass tubing in India to support “Make in India” and rising biologics demand, while DNP used August 2025 to introduce mono-material, recyclable sterile barrier concepts at Medical Fair Thailand signaling a regionalization of supply with circular design built in. Also in August 2025, a market report underscored accelerating adoption of QR, NFC, and RFID for item-level verification and chain-of-custody visibility, reflecting buyers’ expectations for authenticated, condition-monitored diagnostics.

Regulatory infrastructure continues to tighten and professionalize. June 2025 saw India’s CDSCO update the approved labs roster for IVD reagent performance evaluations, enhancing quality oversight. Upstream digital enablers are expanding as well: May 2025 brought Avery Dennison’s RFID-enabled in-mold labels (IMLs) for reusable plastic packs, enabling accurate item-level scanning and supporting circular systems. Capacity commitments remain strong April 2025, Gerresheimer announced about USD 180 million to expand medical systems (inhalers/auto-injectors) in the US, complementing growing demand for precision primary packaging. The demand-side trend line is reinforced by February 2025 reporting rapid growth in self-testing, elevating requirements for consumer-safe, instruction-clear, and contamination-resistant kit packaging. January 2025 saw Wiliot launch an IoT packaging technology for end-to-end visibility, while December 2024 highlighted Unilever’s increased R&D in “Future Flexibles” a reminder that healthcare packaging is absorbing learnings from adjacent high-volume CPG sustainability programs.

Strategic Trends and Emerging Opportunities Shaping the In Vitro Diagnostics Packaging Market

Adoption of High-Barrier Polymer Pouches to Replace Glass Vials

The IVD packaging market is witnessing a rapid shift from traditional glass vials to high-barrier, multi-layer polymer pouches, driven by the need to reduce breakage, lower shipping weight, and enhance laboratory safety. These flexible pouches are engineered to provide superior oxygen and moisture barrier properties, critical for protecting sensitive liquid and lyophilized reagents.

Advancements in polymer science, particularly with cyclic olefin copolymers (COP), enable compatibility with lab-on-a-chip systems, offering compact, reagent-efficient, and fast diagnostic solutions. Companies like Dow Packaging, in collaboration with Syntegon and Ticinoplast, have developed PE-based high-barrier pouches that are predominantly mono-material, supporting recyclability and circular economy initiatives. Innovations by SML and Saica Flex, including MDO-PE films and metallized PE triplex pouches, demonstrate the industry’s capacity to deliver high-performance, transparent, and mechanically robust polymer solutions at commercial scale.

This strategic shift not only enhances operational efficiency and supply chain safety but also aligns with the sustainability goals of major IVD manufacturers, establishing polymer pouches as a future-proof alternative to glass in laboratory and diagnostic applications.

Integration of Smart and Connected Packaging for Chain of Custody

The rise of smart packaging solutions in IVD is revolutionizing traceability, chain of custody, and sample integrity. Features such as temperature and tilt indicators, RFID tags, and NFC-enabled tracking ensure that diagnostic samples remain secure and compliant throughout the supply chain. According to CCL Healthcare, these technologies enhance medication safety, improve operational efficiency, and provide real-time supply chain visibility.

RFID-enabled IVD packaging also ensures compliance with regulatory frameworks such as the U.S. FDA Unique Device Identification (UDI) system, while consumer-facing QR codes and NFC tags offer intuitive guidance and engagement for patients. Providers like ParkourSC highlight that smart packaging supports predictive planning and quality assurance, allowing companies to optimize transport routes and packaging methods while maintaining product integrity.

Development of Sustainable, PCR-Integrated Packaging without Compromising Performance

Sustainability in IVD packaging presents a major growth opportunity, particularly through high-performance materials incorporating post-consumer recycled (PCR) content. Innovations aim to reduce environmental footprint while preserving the chemical and biological integrity of diagnostic assays.

Companies such as Illumina are achieving dramatic reductions in packaging material and dry ice use, while Medix Biochemica is implementing recycled plastic and cardboard solutions for small reagent shipments, resulting in up to 98% less packaging waste. Origin focuses on holistic circular economy approaches, including onshoring and nearshoring production, to minimize transport-related emissions. Global regulatory initiatives like the EU Green Deal further drive the adoption of PCR-integrated, recyclable materials, creating a market pull for sustainable yet high-performance IVD packaging.

Packaging Designed for At-Home and Point-of-Care Diagnostic Collection Kits

The surge in at-home and point-of-care diagnostics necessitates user-centric, safe, and stable packaging solutions. Kits must ensure sample integrity, be intuitive for untrained consumers, and comply with postal and hazardous material regulations.

Competitive Landscape: High-Performance Primary Containers, Smart Labels, and Recycle-Ready Barriers

A concentrated group of materials science leaders and medical-grade converters is shaping IVD packaging through cleanroom manufacturing, tight-tolerance glass/plastic forming, and smart-label integration. The winners combine regulatory fluency (IVDR/UDI), validated sterile barrier systems, and scalable sustainability across global networks.

Gerresheimer AG focuses on regulated primary packaging

Gerresheimer brings deep expertise in glass and engineered plastics, supported by cleanroom production and strong documentation practices vital for IVDR submissions. In April 2025, it committed roughly USD 180 million to expand US medical systems capacity (e.g., inhalers, auto-injectors), underscoring precision molding and assembly capabilities. Its IVD portfolio spans glass vials for reagents, plastic bottles, and molded components for diagnostic kits. Strategically, Gerresheimer targets end-to-end pharma partnerships, couples packaging with drug delivery platforms, and advances sustainability (e.g., 100% renewable electricity by 2030, 50% CO₂ cut) without compromising barrier or sterility.

Schott AG localizes glass tubing for resilient supply

Schott’s strength is Type I borosilicate excellence (e.g., FIOLAX®), delivering consistent geometry for prefillable syringes/cartridges critical to dose accuracy and plunger performance. In August 2025, Schott launched local syringe and cartridge glass tubing production in India, the largest in Asia, transferring technology from Germany to support biologics (including high-growth molecules like semaglutide). Schott’s strategy centers on regional capacity, tight tolerances, and secure supply chains aligned with national manufacturing initiatives and global demand for sterile, high-integrity primary containers.

DWK Life Sciences LLC extends precision labware into IVD

DWK Life Sciences leverages the KIMBLE® and WHEATON® brands to supply glass vials, tubes, and bottles alongside custom plastic components for diagnostic kits. Its reputation rests on sterility, dimensional consistency, and cleanliness, key to reagent stability and analytical accuracy. Strategically, DWK blends standard catalog breadth with custom engineering, investing in processes that improve particle control, closure compatibility, and line efficiency for IVD fillers operating under stringent QA/QR frameworks.

Amcor plc advances recycle-ready medical barriers

Amcor combines a global converting footprint with medical-grade sterile barrier systems (pouches, laminates, films) for diagnostic test kits. Following its July 2025 combination with Berry Global, Amcor broadened access to rigid/flexible platforms and accelerated sustainable high-barrier development. Offerings include AmLite Recyclable (metal-free, high-barrier) and mono-material films that maintain performance while enabling polyolefin-stream recyclability. Strategy: meet IVDR-level requirements, de-risk sterilization pathways, and help OEMs hit 2025 circularity commitments without compromising seal integrity or shelf life.

AptarGroup, Inc. secures integrity with active and dispensing systems

AptarGroup specializes in closures, dosing, and active material science, providing secure seals and accurate dispensing for diagnostic vials and bottles. Its Activ-Blister™ platform protects moisture-sensitive contents vital for lateral-flow and tablet-based IVD formats. With a focus on user safety, tamper evidence, and contamination prevention, Aptar aligns dispensing design with ease-of-use requirements in PoC and self-testing. Strategically, the company advances active packaging and sustainability in tandem, enabling longer reagent stability windows and reduced product waste

In Vitro Diagnostics Packaging Market Share Insights

Blood Collection Tubes Anchor Market Share by Product Type in In Vitro Diagnostics Packaging

Blood collection tubes account for 25% of the in vitro diagnostics (IVD) packaging market in 2025, making them the single most critical product type. Their dominance reflects the indispensable role of tubes as primary sample collection devices in virtually every diagnostic workflow. Designed with anticoagulants, preservatives, or clot activators, these tubes ensure sample integrity for millions of daily blood tests worldwide, from routine health screenings to advanced molecular diagnostics. Microplates also hold a significant share, driven by high-throughput screening in laboratories, enabling simultaneous processing of hundreds of samples in infectious disease, oncology, and genetic testing. Reagent bottles, vials, and ampoules form another cornerstone segment, providing secure, sterile storage for reagents, calibrators, and controls that power diagnostic assays. Complementary formats such as folding cartons, trays, labels, and inserts support organization, compliance, and traceability, which are non-negotiable in regulated environments. The product segmentation highlights how blood collection tubes and microplates drive testing volume, while reagent containers and compliance-oriented packaging ensure reliable, large-scale diagnostic performance.

Infectious Disease Diagnostics Drive Market Share by Application in In Vitro Diagnostics Packaging

Infectious disease diagnostics hold 30% of the IVD packaging market share in 2025, cementing their role as the primary driver of demand. This dominance has been amplified by the COVID-19 pandemic and the sustained global need for testing of HIV, hepatitis, influenza, and emerging pathogens. The enormous testing volume requires a full ecosystem of packaging solutions, from tubes and microplates to reagent storage bottles, creating consistent demand across multiple product types. Cancer diagnostics, with a 20% share, represents the fastest-growing segment, supported by the expansion of precision medicine, liquid biopsy innovations, and companion diagnostics that require specialized packaging for sensitive samples. Diabetes testing adds long-term, high-volume demand through billions of blood glucose strips and lancets, while cardiology and nephrology diagnostics contribute steady, application-specific growth tied to chronic disease monitoring in aging populations. The “Others” category, including immunology, endocrinology, toxicology, and genetic testing, reflects the expansion of personalized medicine and wellness diagnostics. Collectively, this segmentation shows how infectious disease testing underpins volume demand, while cancer, chronic disease, and emerging fields add high-value growth opportunities for IVD packaging.

United States IVD Packaging Market Driven by FDA Regulations and Sustainable Innovation

The U.S. in vitro diagnostics (IVD) packaging market is strongly influenced by stringent FDA regulations aimed at ensuring product sterility, integrity, and extended shelf life. State-level sustainability mandates and consumer demand for traceable, eco-friendly packaging are driving brand owners toward innovative materials and designs. Technological advancements are centered on user-friendly, tamper-evident, and temperature-controlled solutions, especially for point-of-care diagnostics and home-testing kits. Integration of smart packaging features, including QR codes, is enhancing supply chain management and consumer engagement.

Corporate investments, such as Amcor’s planned acquisition of Berry Global Group, are expected to accelerate R&D in medical device and diagnostic packaging. Key applications include infectious disease testing, cancer diagnostics, and diabetes management, where secure, reliable, and high-performance packaging is critical for both professional laboratories and at-home use. Sustainability remains a central focus, with companies developing biodegradable materials and packaging solutions designed to reduce waste and carbon footprints.

Germany IVD Packaging Market Advances Through IVDR Compliance and Circular Economy Leadership

Germany’s IVD packaging sector operates under the EU In Vitro Diagnostic Regulation (IVDR), fully effective since May 2022, which imposes rigorous requirements for notified body involvement and post-market surveillance. This regulatory landscape is accelerating the adoption of advanced packaging solutions capable of protecting molecular diagnostics and personalized medicine products.

Technological innovation in Germany focuses on high-performance, recyclable packaging, addressing both regulatory and environmental demands. The country’s robust circular economy infrastructure incentivizes manufacturers to design protective packaging that can be efficiently recycled. Governmental R&D investment and healthcare reforms further stimulate the market, creating opportunities for packaging solutions that meet the needs of an aging population and the rising burden of chronic diseases.

China IVD Packaging Market Expands with Domestic Innovation and Green Transformation

China’s IVD packaging industry is influenced by the “Healthy China 2030” initiative and the national dual carbon targets, which promote sustainable production and materials adoption. Regulatory reforms, including the new IVD Classification Catalog implemented by NMPA in early 2025, enhance transparency and streamline the classification of complex diagnostic products.

Technological advancements are centered on automation, AI integration, and advanced production methods, improving efficiency and production flexibility for diagnostic kits and reagents. Corporate partnerships between domestic biotech firms and global diagnostic companies are fostering the development of customized solutions, creating demand for high-quality, specialized IVD packaging. The push for domestic production reduces dependency on imports while supporting the growing local market for innovative and recyclable packaging.

Japan IVD Packaging Market Leveraging Precision Manufacturing and High-Performance Solutions

Japan’s IVD packaging market benefits from advanced precision manufacturing capabilities and the strict regulatory oversight of the Pharmaceuticals and Medical Devices Agency (PMDA). Companies like Sysmex are introducing state-of-the-art clinical flow cytometry systems and other advanced diagnostics that require high-performance, protective packaging.

Innovation in packaging focuses on barrier properties, IoT-enabled temperature tracking, and high durability to ensure reagent integrity. High-performance, value-added solutions are in demand due to an aging population and the increasing prevalence of chronic and age-related diseases. Packaging for consumables and kits must be secure, reliable, and compatible with both hospital and at-home testing environments, driving continuous technological innovation in the Japanese market.

Brazil IVD Packaging Market Strengthened by Regulatory Reforms and Local Manufacturing Growth

Brazil’s IVD packaging industry is experiencing dynamic growth supported by sustainable waste management initiatives, including amendments to the National Solid Waste Policy, which encourage domestic recycling. Regulatory measures, such as ANVISA’s Siud unique-device-identification system implemented in June 2025, enhance traceability of medical devices nationwide.

Technological advancement in Brazil includes increased automation, miniaturization, and multiplexing capabilities, requiring compact and efficient packaging. Corporate investments are rising to mitigate currency risks, with AI integration into diagnostic workflows. The market has seen activity from companies like Todos Medical Ltd., which received ANVISA approval for COVID-19 qPCR test kits, demonstrating strong local manufacturing and packaging innovation.

United Kingdom IVD Packaging Market Shaped by MHRA Reforms and Sustainable Healthcare Initiatives

The UK IVD packaging market is guided by MHRA’s new international reliance framework, enabling regulatory reliance on approvals from countries such as the USA, Canada, and Australia. This regulatory alignment is facilitating faster adoption of innovative IVD products. Technological innovations are focused on user-friendly, compact, and protective packaging for point-of-care testing in primary and community care settings.

Government initiatives, including the NHS 10-Year Plan, are driving demand for diagnostics and encouraging investment in advanced packaging solutions. Sustainability is an emerging focus, with the development of eco-friendly packaging that maintains safety and performance while reducing environmental impact. The UK market is positioned for growth in both commercial and home-use diagnostic kits, reflecting a broader shift toward sustainable, high-performance IVD packaging solutions.

In Vitro Diagnostics Packaging Market Report Scope

In Vitro Diagnostics Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$10 Billion

|

|

Market Size (2034)

|

$15.2 Billion

|

|

Market Growth Rate

|

4.8%

|

|

Segments

|

By Product Type (Reagent & Solution Bottles, Blood Collection Tubes, Sample & Transport Tubes, Vials & Ampoules, Culture & Media Bottles, Microplates & Dishes, Pouches & Bags, Folding Cartons & Trays, Labels & Package Inserts), By Material (Plastic, Glass, Paper & Paperboard), By End-User (Hospitals, Clinical Laboratories, Academic & Research Institutes, Point-of-Care Testing Facilities), By Application (Infectious Disease Diagnostics, Cancer Diagnostics, Diabetes Diagnostics, Cardiology Diagnostics, Nephrology Diagnostics, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Gerresheimer AG, AptarGroup, Inc., SCHOTT AG, DWK Life Sciences LLC, Thermo Fisher Scientific Inc., Corning Incorporated, Greiner Bio-One GmbH, Tekni-Plex, Inc., Comar, LLC, Becton, Dickinson and Company, West Pharmaceutical Services, Inc., Placon Corporation, Sealed Air Corporation, Nelipak Healthcare Packaging

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

In Vitro Diagnostics Packaging Market Segmentation

By Product Type

- Reagent & Solution Bottles

- Blood Collection Tubes

- Sample & Transport Tubes

- Vials & Ampoules

- Culture & Media Bottles

- Microplates & Dishes

- Pouches & Bags

- Folding Cartons & Trays

- Labels & Package Inserts

By Material

- Plastic

- Glass

- Paper & Paperboard

By End-User

- Hospitals

- Clinical Laboratories

- Academic & Research Institutes

- Point-of-Care Testing Facilities

By Application

- Infectious Disease Diagnostics

- Cancer Diagnostics

- Diabetes Diagnostics

- Cardiology Diagnostics

- Nephrology Diagnostics

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in In Vitro Diagnostics Packaging Market

- Amcor plc

- Gerresheimer AG

- AptarGroup, Inc.

- SCHOTT AG

- DWK Life Sciences LLC

- Thermo Fisher Scientific Inc.

- Corning Incorporated

- Greiner Bio-One GmbH

- Tekni-Plex, Inc.

- Comar, LLC

- Becton, Dickinson and Company

- West Pharmaceutical Services, Inc.

- Placon Corporation

- Sealed Air Corporation

- Nelipak Healthcare Packaging

* List Not Exhaustive

Methodology

USDAnalytics has prepared the In Vitro Diagnostics (IVD) Packaging Market analysis through a rigorous methodology combining primary interviews with packaging engineers, regulatory experts, laboratory managers, and supply chain professionals across key regions, alongside secondary research using company reports, regulatory filings, trade journals, and verified industry publications. Market sizing, CAGR, and trend forecasts were derived using a mix of top-down and bottom-up approaches, cross-validated through triangulation with historical shipment data, technology adoption rates, and materials cost indices. The methodology also incorporates regulatory frameworks such as IVDR, UDI/serialization, and national IVD classification catalogs, as well as technological innovations in high-barrier polymers, smart labels (RFID/NFC), and PCR-integrated recyclable packaging. USDAnalytics further analyzed competitive strategies, regional infrastructure, point-of-care adoption, and sustainability initiatives to provide actionable insights on product types, applications, end-users, and material trends, ensuring a robust, industry-focused outlook for decision-makers in IVD packaging.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.