Market Overview: Mass Personalization and On-Demand Printing Redefine Packaging Economics

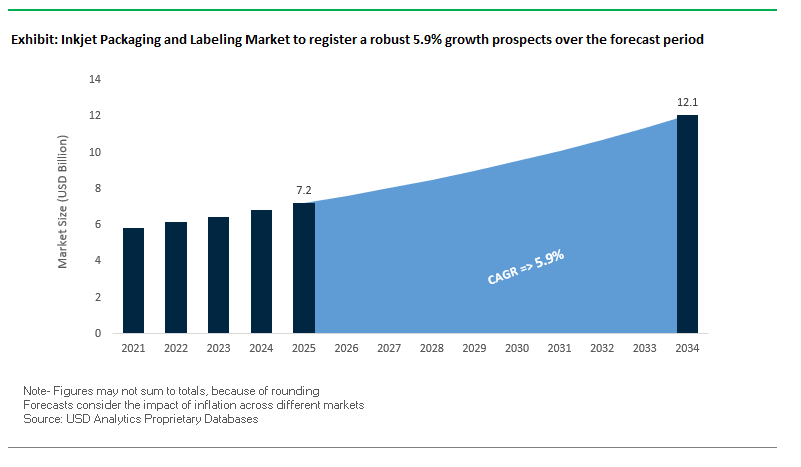

The Inkjet Packaging and Labeling Market is valued at USD 7.2 billion in 2025 and is projected to reach USD 12.1 billion by 2034, registering a CAGR of 5.9%. For industry buyers, the core question is how to deploy digital inkjet to unlock short runs, versioning, and variable data while meeting sustainability targets and strengthening traceability/brand protection. Inkjet eliminates plates, slashes makeready waste, and enables real-time, SKU-level customization across substrates from paperboard and corrugated to films and rigid containers. Its growing materials/ink portfolio (water-based and UV-curable) supports compliance and lower environmental impact, while inline serialization (QR, GS1 barcodes, RFID) enhances supply-chain visibility and anti-counterfeiting. The strategic shift from pre-printed stock to direct-to-pack on demand reduces inventory, accelerates launches, and improves total cost of ownership for converters and brands.

Key Insights for Industry Professionals:

- Growth vector: USD 7.2B (2025) → USD 12.1B (2034) at 5.9% CAGR driven by customization and speed-to-market.

- Economics: Short runs and frequent design changeovers favor digital over analog; lower waste, zero plates.

- Sustainability: Water-based/UV-curable sets curb VOCs and scrap; mono-material packs benefit from late-stage digital print.

- Traceability: Serialized barcodes, QR, RFID/NFC for authentication, recalls, and consumer engagement.

- Application breadth: Labels, flexible packaging, corrugated direct-print, and direct-to-shape containers.

Market Analysis: Smart Codes, M&A, and Film Innovations Accelerate Digital Adoption

Sector momentum is visible across press launches, materials, and consolidation. In September 2025, Domino Printing Sciences introduced the N410 digital LED inkjet label press, a compact, cost-effective gateway for converters entering digital. August 2025 brought Siegwerk’s acquisition of Allinova, strengthening sustainable coatings and ink chemistries, while All4Labels advanced a string of M&A in South America to scale label and packaging capacity for regional FMCG growth.

Consolidation at scale continued in July 2025, as Amcor and Berry Global completed their all-stock combination, creating a powerhouse across flexible/rigid platforms important for hybrid converting lines that marry substrates, films, and digital finishing. That same month (July 2025), a market study flagged surging uptake of smart packaging (QR, NFC, RFID) to boost item-level visibility and engagement. In June 2025, Mondi launched a mono-material, recyclable paper-based pouch for pet nutrition, aligning materials innovation with digital decoration. Parallel June 2025 merger talks between DS Smith and Mondi (proposed all-stock deal) underscored corrugated/paper integration that complements direct-to-board inkjet growth.

Platform expansion and specialty films rounded out the investment cycle. In April 2025, Inovar Packaging Group acquired ModTek to extend prime-label reach in the US, while in March 2025 Toppan acquired Irplast (high-performance BOPP films), reinforcing film supply for high-speed inkjet and recyclable structures. Collectively, these moves signal a market coalescing around digital-ready materials, smart codes, and regional capacity to support faster, cleaner, and more traceable packaging workflows.

Emerging Trends and Strategic Opportunities in the Inkjet Packaging and Labeling Market

Adoption of High-Speed Single-Pass Inkjet for Corrugated Packaging

The inkjet packaging and labeling market is witnessing a transformative shift as major corrugated packaging converters invest in high-speed single-pass inkjet presses. Unlike traditional multi-pass systems, single-pass technology utilizes a full-width fixed print bar to deliver line-speed printing directly onto corrugated board, eliminating the need for printing plates and significantly reducing setup waste. This is particularly advantageous for e-commerce and retail-ready packaging, where high-volume, variable data printing is essential.

Leading industry examples underscore this trend: In 2022, Modern Ambalaj in Turkey installed the EFI Nozomi C18000 Plus to expand production capacity from 600,000 to 800,000 tonnes annually. Similarly, Domino Printing Solutions’ X630i press prints up to 75 meters per minute and produces 4,500 sheets per hour, demonstrating efficiency and scalability for high-volume applications.

Environmental and operational benefits further enhance adoption. EFI’s Nozomi presses reduce ink and board waste, eliminate water usage, and are certified for OCC recyclability and repulpability. Companies like Box Genie note that digital inkjet cuts preparation stages, enabling rapid design changes and small-run printing without flexo tooling costs, offering a critical competitive advantage for brands.

Expansion of Water-Based Pigment Inks for Flexible Film Printing

A parallel trend in the market is the shift to water-based pigment inkjet inks for flexible packaging films. Driven by sustainability mandates, regulatory compliance, and food safety concerns, these inks reduce solvent emissions while ensuring low migration in food-contact applications.

Technological innovations, such as Sun Chemical’s water-based inks, enable adhesion on non-porous surfaces like polyolefins, addressing historical challenges. Compliance with EuPIA exclusion policies and evolving guidelines from the U.S. FDA and EFSA further reinforce industry adoption. Companies like Fujifilm are investing in production capacity expansion to meet the growing demand for food-safe, low-migration inks, underscoring capital commitment and market validation.

Integration of Smart and Connected Packaging Features

Digital inkjet provides a gateway to smart and interactive packaging, moving beyond barcodes to UV fluorescing codes, NFC/RFID antennas, and unique QR codes. These features enable brand protection, anti-counterfeiting measures, and supply chain visibility, while also fostering direct-to-consumer engagement.

For example, Scantrust leverages unique QR codes to authenticate products and connect with consumers. Printing RFID tags or conductive traces allows real-time package tracking, enhancing logistics and inventory management. Brands like Coca-Cola have successfully used variable data printing to create personalized experiences that boost loyalty. Advances in cost-effective conductive ink technology also allow embedding sensors to monitor temperature and humidity, ensuring product integrity for sensitive goods.

On-Demand Digital Labeling for Sustainable Personal Care and Chemicals

The growing market for personalized and regionally customized products is driving on-demand digital label printing, especially in cosmetics, industrial chemicals, and cleaning products. This approach enables short runs, regulatory compliance, and test marketing while minimizing waste.

Competitive Landscape: Hardware, Chemistry, and Workflow Orchestrate End-to-End Digital Packaging

A tightly coordinated value chain press OEMs, ink/coating specialists, and software/workflow providers now defines competitive advantage. Leaders are combining 1200-dpi class imaging, color/ICC automation, and inline finishing with eco-optimized inks to deliver shelf-ready, compliant packs at digital speeds.

HP Inc.: Digital presses scale mass personalization

Overview. HP anchors digital transformation with a broad portfolio spanning labels, flexibles, folding carton, and corrugated. The company reported >20% growth (2024) in flexible packaging adoption, led by the HP Indigo 200K for speed, gamut, and substrate agility; corrugated ink usage rose >30% (2024) as brands pivoted to digitally printed shipper experiences.

Focus. High-fidelity color, variable data at scale, and robust workflow (color management, job ganging) underpin short-run economics. HP’s strategy centers on mass customization, faster time-to-shelf, and sustainability via lower waste and plate-free changeovers.

Domino Printing Sciences: Accessible, industrial-grade digital for converters

Overview. Domino’s strength spans CIJ/TIJ coding to single-pass piezo and now digital label presses. In September 2025, it launched the N410 LED inkjet label press to lower barriers for converters; earlier (June 2024) it unveiled Gx-Series TIJ→TTO solutions for flexible lines.

Focus. Reliability, integration with existing finishing, and traceability printing (lot/expiry, barcodes) make Domino a go-to for food, beverage, pharma lines transitioning to hybrid digital workflows with less waste and higher OEE.

FUJIFILM Corporation: Printheads, inks, and stabilization for packaging

Overview. Fujifilm couples advanced printheads and ink sets with software that stabilizes substrates on the fly mitigating cockling and color drift that historically limited continuous inkjet on flexible webs. By July 2025, the company highlighted growth in labels, corrugated, and flexibles.

Focus. End-to-end solutions hardware, RIP/workflow, and chemistry drive color consistency and high uptime. Fujifilm’s roadmap targets shorter runs, rapid design cycles, and converters needing predictable, repeatable color across diverse substrates.

Durst Group: 1200-dpi hybrid platforms for label and board

Overview. Durst’s Tau RSC (labels) and P5 (packaging/board) families deliver 1200-dpi resolution and high productivity. August 2025 commentary emphasized hybrid architectures that combine inkjet + flexo, letting converters balance spot-color economics with variable content.

Focus. “Complete solutions” (press + workflow + analytics + color) shorten ramp-up times and ensure factory-level reliability. Durst positions on quality at speed, enabling converters to shift significant analog volumes to digital without sacrificing brand color targets.

DIC Corporation (Sun Chemical): Sustainable ink chemistries for digital growth

Overview. DIC/Sun Chemical supplies water-based, UV-curable, and specialty inkjet chemistries, reporting in August 2025 rising demand for direct-to-shape and metal decoration alongside packaging. DIC India (2024) reiterated a pipeline of eco-friendly inks and coatings.

Focus. Recyclability-ready sets, low-migration options, and functional inks (adhesion, special effects) enable converters to meet circularity and compliance targets while achieving premium shelf impact key to brand protection and consumer engagement.

Inkjet Packaging and Labeling Market Share Insights

Inks Drive Market Share by Component in Inkjet Packaging and Labeling

Inks command 50% of the inkjet packaging and labeling market in 2025, underscoring their central role as the recurring revenue engine in the industry. Inkjet’s business model is heavily consumables-driven, with inks tailored to different substrates and regulatory requirements ranging from pigment-based inks for durability, to UV-curable inks for versatility, and low-migration inks for food safety compliance. This high-margin segment benefits from continuous demand as companies rely on specialized formulations to maintain print quality, durability, and compliance. Printers, while representing significant capital investment, remain essential enablers of inkjet adoption, with innovation focused on speed, substrate compatibility, and integration into automated packaging lines. Consumables beyond inks, including printheads, maintenance kits, and cleaning fluids, ensure the longevity and efficiency of printing systems, making them indispensable despite a smaller revenue contribution. The overall segmentation reflects how inks dominate ongoing revenue, printers secure technology adoption, and consumables safeguard operational reliability.

Food and Beverages Sector Dominates Market Share by Application in Inkjet Packaging and Labeling

The food and beverages industry captures 35% of the inkjet packaging and labeling market in 2025, driven by the sector’s reliance on high-speed, variable data printing (VDP) for critical information such as expiry dates, lot codes, and barcodes. Beyond compliance, inkjet enables rapid design iteration for seasonal promotions, limited editions, and product personalization, aligning with consumer trends toward customization. Pharmaceuticals & healthcare follow as a high-value segment, where serialization, unique device identifiers (UDIs), and strict track-and-trace mandates demand high-resolution, smudge-resistant printing that complies with FDA and EU regulations. Industrial and logistics sectors utilize inkjet extensively for corrugated box printing, reducing costs tied to pre-printed inventory and providing agility in e-commerce and supply chain operations. Household and personal care applications highlight inkjet’s versatility, with brands leveraging it for promotional campaigns, regional versioning, and rapid SKU expansion. Together, these segments illustrate how F&B leads in volume, pharmaceuticals anchor value-driven compliance, and industrial/logistics optimize operational efficiency through inkjet.

United States Inkjet Packaging and Labeling Market Driven by EPR Regulations and Advanced Printing Technologies

The U.S. inkjet packaging and labeling market is heavily influenced by a fragmented regulatory landscape, including California’s SB-54 Extended Producer Responsibility (EPR) law, which mandates a 25% reduction in plastic usage by 2032. This has created strong demand for paper-based packaging compatible with digital printing. The Drug Supply Chain Security Act (DSCSA) also drives the adoption of variable data inkjet printing, requiring unique identifiers for pharmaceutical products.

Technological advancements are focusing on new barrier coatings for paper and films to ensure recyclability and compatibility with inkjet inks, supporting mono-material packaging. Corporate investments from companies like HP Inc. and Domino Printing Sciences highlight the commitment to sustainable, high-performance solutions. Key applications include e-commerce, food and beverage, and pharmaceutical sectors, where personalized packaging, traceability, and sustainability are critical. Eco-friendly inks, including UV-curable and water-based formulations, are increasingly adopted to reduce VOC emissions and enhance sustainability.

Germany Inkjet Packaging and Labeling Market Excels Through Industry 4.0 and Circular Economy Leadership

Germany’s inkjet packaging and labeling industry is shaped by stringent EU regulations, including the Packaging and Packaging Waste Regulation (PPWR) effective February 2025, requiring all packaging to be fully recyclable or reusable by 2030. This has accelerated the adoption of high-performance digital printing solutions.

The country’s strong Industry 4.0 initiatives are integrating smart manufacturing and digital technologies, enhancing productivity and precision. Germany’s Packaging Act (VerpackG) incentivizes recyclable packaging designs, favoring inkjet over traditional printing methods. Corporate collaborations, such as SÜDPACK and SN Maschinenbau developing digitally printed stand-up pouches, exemplify the focus on innovation and sustainability. These factors drive strong demand across food, beverage, and specialty packaging applications.

China Inkjet Packaging and Labeling Market Expands Through Green Policies and Technological Investments

China’s inkjet packaging and labeling market is propelled by governmental initiatives, including the “dual carbon” goal and the March 2024 Action Plan for Large-Scale Equipment Updates, promoting sustainable materials and recycling. The GB/T 31268 regulation, effective November 2024, restricts excessive packaging, directly influencing e-commerce and industrial packaging sectors.

Technological advancements, including automation, AI integration, and “5G plus industrial internet,” are optimizing production processes and enhancing flexible manufacturing capacity. Domestic production and substitution of imported technologies remain key trends, with local companies expanding their capacity to meet growing demand for high-quality, circular inkjet packaging solutions.

India Inkjet Packaging and Labeling Market Strengthened by Circular Economy Policies and GST Incentives

India’s inkjet packaging and labeling industry is experiencing growth due to government support for a circular economy and GST reduction on paper and biodegradable packaging to 5% in September 2025. This has increased adoption of sustainable printing solutions across food, beverage, and consumer goods sectors.

Technological adoption, including automated production lines and inkjet printing on paper, cardboard, and plastic packaging, supports regulatory compliance with FSSAI food safety standards. Corporate investments, such as Tetra Pak’s introduction of certified recycled polymer packaging, reflect the growing emphasis on sustainability and high-quality labeling solutions for domestic and export markets.

Japan Inkjet Packaging and Labeling Market Driven by Precision Manufacturing and Recycled Materials

Japan’s inkjet packaging and labeling market leverages advanced precision manufacturing and next-generation production technologies. Companies such as Toppan Inc., RM Tohcello, and Mitsui Chemicals Inc. have developed recycled BOPP films for mass production, enhancing sustainability and performance.

Regulatory guidance from the Plastic Resource Circulation Act (April 2022) promotes environmentally conscious packaging and reduces single-use plastics. Major players focus on high-performance products with durable, aesthetic, and functional properties. Innovations such as self-sealing and barrier-enhanced packaging address industry-specific needs across food, pharmaceutical, and industrial applications.

Brazil Inkjet Packaging and Labeling Market Strengthened by Sustainable Policies and Strategic Collaborations

Brazil’s inkjet packaging and labeling market benefits from sustainable waste management initiatives under the National Solid Waste Policy, which encourages domestic recycling. Upcoming government mandates are expected to require companies to recycle a substantial portion of products, further promoting sustainable packaging solutions.

Technological advancements include premium and specialized digital printing solutions for flexible packaging. Key applications are concentrated in the food, beverage, and e-commerce sectors. Corporate collaborations, such as SIG Group’s partnership with DPA Brazil to launch spouted pouches for Chamyto yogurt, reflect strategic moves to strengthen market presence and drive innovation in sustainable inkjet packaging.

Inkjet Packaging and Labeling Market Report Scope

Inkjet Packaging and Labeling Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.2 Billion

|

|

Market Size (2034)

|

$12.1 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Component (Printers, Inks, Consumables), By Substrate (Plastic, Paper & Paperboard, Metal, Glass, Others), By Packaging Type (Flexible Packaging, Corrugated Packaging, Folding Cartons, Labels), By Application (Food & Beverages, Pharmaceuticals & Healthcare, Household & Personal Care, Industrial & Logistics, Other End-Use Industries), By Ink Type (Aqueous, Solvent-based, UV-curable, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

HP Inc., Domino Printing Sciences plc, Konica Minolta, Inc., Durst Phototechnik AG, SCREEN Holdings Co., Ltd., EFI (Electronics for Imaging), FujiFilm Holdings Corporation, SATO Holdings Corporation, Linx Printing Technologies, Videojet Technologies, Markem-Imaje, Xaar plc, Xeikon (Flint Group), Canon Inc., Kodak

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Inkjet Packaging and Labeling Market Segmentation

By Component

- Printers

- Inks

- Consumables

By Substrate

- Plastic

- Paper & Paperboard

- Metal

- Glass

- Others

By Packaging Type

- Flexible Packaging

- Corrugated Packaging

- Folding Cartons

- Labels

By Application

- Food & Beverages

- Pharmaceuticals & Healthcare

- Household & Personal Care

- Industrial & Logistics

- Other End-Use Industries

By Ink Type

- Aqueous

- Solvent-based

- UV-curable

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Inkjet Packaging and Labeling Market

- HP Inc.

- Domino Printing Sciences plc

- Konica Minolta, Inc.

- Durst Phototechnik AG

- SCREEN Holdings Co., Ltd.

- EFI (Electronics for Imaging)

- FujiFilm Holdings Corporation

- SATO Holdings Corporation

- Linx Printing Technologies

- Videojet Technologies

- Markem-Imaje

- Xaar plc

- Xeikon (Flint Group)

- Canon Inc.

- Kodak

* List Not Exhaustive

Methodology

USDAnalytics employed a rigorous, multi-source methodology to analyze the Inkjet Packaging and Labeling Market, combining primary research from packaging engineers, brand managers, converters, and supply chain experts with secondary data from corporate reports, regulatory filings, trade journals, and verified industry databases. Market sizing, CAGR, and forecasts were calculated using a combination of bottom-up and top-down approaches, validated against historical adoption trends, substrate consumption, and equipment deployment data. The study emphasizes emerging digital printing technologies including high-speed single-pass inkjet, water-based and UV-curable inks, smart codes, and variable-data printing alongside sustainability trends, regulatory compliance (EPR, PPWR, DSCSA), and the evolving competitive landscape. Competitive strategies of leading players such as HP Inc., Domino Printing Sciences, Fujifilm, and Durst Group were analyzed to assess innovation, workflow integration, and eco-friendly packaging solutions. Regional dynamics across North America, Europe, Asia-Pacific, and Latin America were incorporated, providing actionable insights for industry professionals seeking to optimize print operations, reduce waste, and enable mass personalization across flexible, corrugated, and rigid packaging applications.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.