Market Overview: Sustainability, E-commerce Growth, and Branding Innovations

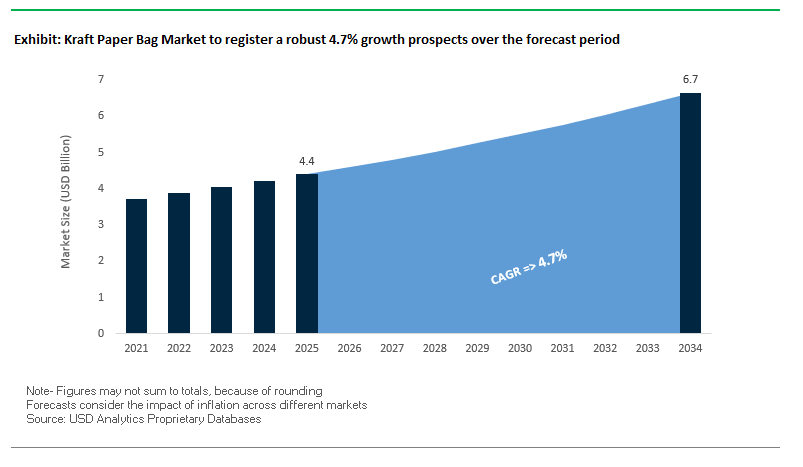

The Kraft Paper Bag Market is valued at USD 4.4 billion in 2025 and projected to reach USD 6.7 billion by 2034, registering a steady CAGR of 4.7%. The market is at the forefront of the global shift away from single-use plastics, driven by regulatory pressures, corporate sustainability goals, and strong consumer preference for recyclable and biodegradable solutions. Industry professionals and buyers are increasingly evaluating how Kraft paper bags can deliver cost efficiency, branding value, and compliance with circular economy targets.

Key Insights for Industry Professionals

- Consumer Priority: Over 60% of global consumers prefer sustainable packaging, positioning Kraft paper bags as a viable alternative to plastics.

- E-commerce Driver: The expansion of online retail and home delivery has increased demand for lightweight, durable, and recyclable Kraft paper bags.

- Branding Power: Boutique retailers and global brands are using tinted, custom-printed Kraft bags to elevate consumer experience and brand loyalty.

- Beyond Bags: Kraft paper is diversifying into flexible food packaging and coated solutions, extending its role across multiple industries.

- Circular Economy Alignment: Adoption of barrier-coated and heat-sealable Kraft grades ensures recyclability while replacing multi-layer plastics.

Market Analysis: Recent Developments Shaping the Kraft Paper Bag Industry

The Global Kraft Paper Bag Market has witnessed significant product innovation and corporate strategy realignments in the past two years. In August 2025, Mondi introduced Ad/Vantage Smooth Brown Semi Extensible Kraft paper, a high-performance paper designed for coating applications, balancing strength and printability. The same month, Graphic Packaging International unveiled child-resistant paperboard packaging for laundry pods, reflecting the broader “paperization” trend across multiple consumer goods categories.

M&A and brand-led sustainability initiatives are shaping market structure. In July 2025, International Paper divested five European corrugated plants to meet regulatory conditions following its DS Smith acquisition, reshaping its fiber-based portfolio. That same month, IKEA committed to replacing plastic fitting bags with paper alternatives, eliminating 1,400 tons of plastic annually. Earlier in March 2025, Billerud launched heat-sealable Kraft paper, a recyclable, fossil-free replacement for plastics without requiring equipment modifications underscoring the scalability of innovation.

Consumer-facing innovations continue to expand Kraft’s versatility. In November 2024, Primark introduced shopping bags that double as festive wrapping paper, promoting both sustainability and reuse. In October 2024, the Smurfit Kappa–WestRock merger formed Smurfit WestRock, consolidating leadership in fiber-based solutions and cementing Kraft paper’s role in global packaging strategies.

Strategic Trends and Opportunities Driving the Kraft Paper Bag Market

Strategic Corporate Investment in Domestic Recycled Content Production

The kraft paper bag market is witnessing a substantial shift toward vertically integrated, high-recycled-content production, driven by sustainability demands and regulatory pressures. Major players are investing in recycling infrastructure to de-ink and process post-consumer waste, securing a steady supply of high-quality recycled fiber for production lines and reducing dependence on volatile recycled paper markets. This domestic focus not only supports local economies but also minimizes carbon emissions associated with importing raw materials, enhancing the overall sustainability profile of kraft paper products. Advanced deinking and refining technologies are being deployed to improve feedstock quality, allowing a broader range of recycled materials to be used. The Indian Paper Manufacturers Association (IPMA) emphasizes the role of alternative raw materials such as bagasse, wheat straw, and recycled wastepaper in promoting a circular economy, highlighting a long-term industry commitment to keeping materials in use for as long as possible. These initiatives reflect a growing trend of sustainability-driven capital investment and supply chain resilience in the global kraft paper bag market.

Policy-Driven Demand from Plastic Bag Bans and Extended Producer Responsibility (EPR)

Government legislation and extended producer responsibility (EPR) frameworks are significant drivers for kraft paper bag adoption, replacing single-use plastic alternatives. Global plastic bag bans and the EU’s Packaging and Packaging Waste Regulation (PPWR) promote recyclable and compostable packaging, encouraging brands to shift toward paper-based solutions. In the U.S., states like California, Oregon, and Maine have implemented EPR laws, holding producers financially accountable for packaging end-of-life management. EPR regulations often include modulating fees that reward recyclable material usage and penalize difficult-to-recycle plastics, creating direct financial incentives for brands to adopt kraft paper packaging. Corporate alignment with these regulations also supports consumer expectations for eco-friendly products, reinforcing ESG strategies. As a result, the kraft paper bag market is increasingly shaped by regulatory mandates and policy-driven demand, accelerating the replacement of plastic bags across retail and packaging applications.

Expansion into E-commerce Fulfillment and Reverse Logistics

The rapid growth of e-commerce presents a significant opportunity for kraft paper bags, particularly as consumers demand sustainable alternatives to plastic mailers. Companies like WestRock offer high-strength kraft paper mailers, both unpadded and padded, that serve as eco-friendly substitutes for shipping apparel, accessories, and other items. Reverse logistics solutions are also emerging; Mondi Group’s “re/cycle MailerBAGs” feature resealable dual-adhesive strips, enabling consumers to return items easily while reducing the need for new packaging. Kraft paper also enhances branding opportunities, providing a premium tactile experience that supports high-quality printing and reinforces brand identity. Durability is a key factor, and manufacturers like Shitla Papers emphasize lightweight yet robust kraft paper mailers designed to protect products during transit while minimizing shipping costs. These developments position kraft paper as a versatile solution for sustainable, brandable e-commerce packaging.

Development of High-Performance, Functional Barrier Coatings

Innovations in bio-based barrier coatings are creating opportunities for kraft paper to match the functional properties of plastic while remaining fully recyclable. Renewable biopolymers such as polylactic acid (PLA), chitosan, and cellulose are being explored as moisture and grease-resistant coatings that do not compromise recyclability. H.B. Fuller’s water-based coatings exemplify designs that can be easily removed during recycling, maintaining the paper’s circularity. Application-specific solutions are emerging, tailored to meet the unique needs of different products moisture barriers for taco shells or grease barriers for pet food packaging. Research is also exploring active properties, integrating antimicrobial compounds into bio-based coatings to extend food shelf life and prevent microbial growth. These functional innovations represent a high-value opportunity for the food and consumer goods industries, allowing kraft paper bags to compete effectively with traditional plastic while supporting sustainability objectives.

Competitive Landscape: Leading Companies in Kraft Paper Bag Market

Mondi Group: Driving innovation in performance kraft papers

Mondi is a global leader in sustainable packaging with an extensive Kraft portfolio. In August 2025, it launched Ad/Vantage Smooth Brown Semi Extensible, combining puncture resistance and printability. Mondi’s strategy is anchored in its goal to make 100% of packaging reusable, recyclable, or compostable by 2025, with strong collaborations across e-commerce and FMCG. Its offerings range from sack Kraft papers to mono-material compostable packaging, reinforcing its leadership in replacing plastics with fiber-based alternatives.

Billerud: Advancing fossil-free and heat-sealable kraft papers

Billerud continues to invest in high-performance Kraft grades that align with low-carbon packaging. In April 2025, the company advanced investments in its Michigan mills under the Way Forward strategy, strengthening its North American presence. Its virgin fiber expertise ensures premium quality for industrial bags, food packaging, and medical applications. With its new heat-sealable Kraft paper launched in March 2025, Billerud provides a scalable plastic replacement, enabling customers to meet recyclability targets.

Smurfit WestRock: Global powerhouse in fiber-based packaging

Formed in October 2024 through the merger of Smurfit Kappa and WestRock, Smurfit WestRock has become a global giant in corrugated and Kraft-based solutions. In August 2025, it launched innovations for Bag-in-Box packaging to meet regulatory compliance. Its integrated business model, from paper collection to finished products, ensures strong supply chain control. Smurfit WestRock’s strategy is clear: develop recyclable, compostable, and reusable paper-based packaging across all consumer segments, leveraging its unmatched scale.

International Paper: Expanding global presence in fiber-based consumer packaging

International Paper remains one of the largest fiber-based packaging leaders. Following its DS Smith acquisition in late 2024, it restructured its European operations, divesting five corrugated plants in July 2025. Its Kraft paper bags are popular among retailers and grocers, backed by a supply chain of responsibly sourced renewable fiber. With ongoing work on mono-material laminates, International Paper is targeting solutions that deliver 100% recyclability without compromising performance.

Klabin S.A.: Leading kraft paper innovator in Latin America

Klabin is Brazil’s largest exporter of paper packaging solutions, with strong vertical integration from forestry to final products. In December 2024, it launched the Wicket Paper Bag for diaper packaging, a 100% recyclable solution, showcasing its focus on consumer applications. Its Kraft grades include sack kraft paper and special packaging papers, widely used in industrial and retail segments. Klabin’s strategy emphasizes continuous improvement, innovation, and sustainability, reinforcing its competitive edge in the Latin American market.

Kraft Paper Bag Market Share Insights

Pasted Valve Bags Dominate Market Share by Product Type in the Kraft Paper Bag Industry

Pasted valve bags account for the largest share of the kraft paper bag industry in 2025, capturing around 40% of the market. Their leadership stems from superior compatibility with automated, high-speed filling lines, which makes them indispensable for bulk industries such as cement, construction powders, and industrial chemicals. These bags ensure dust-free filling, automatic closure, and cost-effective handling, aligning perfectly with the operational efficiency and containment standards required in heavy-duty applications. Sewn open mouth bags maintain relevance for coarse and heavy materials like animal feed and minerals, highlighting their robustness and versatility. Flat bottom bags, although smaller in share, are rapidly gaining traction in retail and premium consumer goods packaging due to their upright stability, convenience, and sustainable appeal. Collectively, the segmentation underscores how industrial applications drive high-volume demand for pasted valve designs, while retail shifts toward flat bottom bags reflect branding and sustainability priorities.

Building & Construction Leads Market Share by Application in the Kraft Paper Bag Industry

Building & construction is the leading application segment for kraft paper bags, holding 35% of the market in 2025. This dominance is directly tied to the global cement and plaster sectors, where multi-wall pasted valve sacks provide unrivaled containment of fine dust and superior stackability for supply chain efficiency. Food & beverages represent another significant consumer, requiring kraft bags with food-grade liners for safe storage of flour, sugar, and grains, while retail & consumer goods leverage flat bottom kraft bags for premium appeal and eco-friendly positioning. The chemicals sector adds critical demand through products such as pigments, dyes, and fertilizers, where barrier-lined kraft bags ensure safe handling and moisture protection. Other applications, including agriculture and minerals, reinforce the material’s role as a durable, recyclable, and sustainable packaging format. This segmentation demonstrates how building materials secure volume leadership, while food, retail, and chemicals create diversification opportunities in high-value niches.

United States Kraft Paper Bag Market Grows Amid Single-Use Plastic Regulations and Sustainable Packaging Demand

The U.S. kraft paper bag market is being strongly influenced by state and municipal bans on single-use plastics, creating a favorable environment for paper-based alternatives. This regulatory push is accelerating the adoption of sustainable kraft paper bags across retail, foodservice, and e-commerce sectors. Companies like International Paper, Mondi, and WestRock are introducing innovative bags made from sustainably sourced kraft paper, bioplastics, and compostable coatings. Advancements in materials, including thinner, stronger kraft paper with moisture-resistant coatings, are enabling high-performance and eco-friendly packaging solutions.

Corporate investments are further shaping market growth, with companies expanding production capabilities to meet rising demand. Sealed Air’s acquisition of Liquibox, for instance, is expected to enhance its CRYOVAC portfolio with kraft paper solutions. Key applications driving demand include e-commerce packaging for clothing, books, and electronics, as well as takeout containers and delivery bags in the foodservice industry. Sustainability remains a major market driver, as businesses and consumers increasingly seek eco-friendly alternatives to meet corporate social responsibility and regulatory targets.

Germany Leads in Circular Economy and High-Performance Kraft Paper Packaging Solutions

Germany’s kraft paper bag market is guided by a stringent regulatory framework, notably the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, which mandates fully recyclable or reusable packaging by 2030. The Single-Use Plastics levy is further incentivizing the adoption of reusable and recyclable paper-based solutions, driving innovation in sustainable packaging.

Technological advancement and industry collaboration are central to market development. Mondi, in partnership with CMC Packaging Automation in July 2024, is focusing on innovative kraft paper solutions for high-performance packaging applications. Germany’s Packaging Act (VerpackG) encourages recyclable packaging designs through modulated fees, favoring paper-based over single-use plastics. Strategic corporate initiatives, such as IKEA Components’ 2025 commitment to replace plastic fitting bags with paper alternatives by 2028, highlight the country’s leadership in circular economy practices and sustainable packaging innovation.

China Kraft Paper Bag Market Strengthens with Government Initiatives and E-Commerce Demand

China’s kraft paper bag industry is being transformed by governmental green policies, including the “dual carbon” initiative promoting sustainable manufacturing. The March 2024 “Action Plan for Promoting Large-Scale Equipment Updates and Consumer Goods Replacement” encourages the adoption of recyclable and sustainable packaging. Regulatory reforms, such as GB/T 31268 and the 2025 amendment to Express Delivery Regulations, are prioritizing recyclable and biodegradable materials, driving a shift from film mailers to folding cartons and kraft paper bags.

Technological advancements in automation and AI are enhancing production efficiency, while QR codes and RFID inserts on shipping cartons improve inventory visibility and returns management. Domestic manufacturing is expanding, with companies like Chengde Technology Co., Ltd. and Bagitan Packaging scaling operations to meet rising demand for high-quality, circular packaging. The booming e-commerce sector remains a key driver, stimulating innovation and adoption of kraft paper solutions across logistics and retail channels.

India’s Kraft Paper Bag Market Expands with Circular Economy Policies and Plastic Bans

India’s kraft paper bag market has been catalyzed by the government’s push for a circular economy and the July 2022 ban on single-use plastics. This regulatory framework has accelerated the shift towards paper-based packaging in retail, foodservice, and e-commerce sectors. Advanced materials and specialized products, such as the White Kraft Liner (WKL) introduced by Silverton Pulp and Paper in collaboration with Worthwell Papers in January 2025, are meeting the demand for branded and export packaging solutions.

Corporate investments are increasing, with Sripathi Paper and Boards launching low-GSM coated White Kraft Liners in Tamil Nadu to support high-speed packaging operations. The country’s expanding e-commerce, retail, and food processing sectors, combined with rising exports of industrial products, are fueling demand for high-performance kraft paper bags that adhere to global quality and safety standards.

Japan Drives Kraft Paper Bag Innovation Through Advanced Materials and Regulatory Support

Japan’s kraft paper bag market is a hub of innovation, led by precision manufacturing and advanced paper technology. Companies such as Oji Holdings and Nippon Paper Industries are recognized for their expertise in forest product management and high-performance paper solutions. Regulatory policies, including the Plastic Resource Circulation Act (April 2022) and revised food contact material regulations (effective June 2026), are promoting sustainable design and reducing single-use plastics.

Market players are increasingly focusing on specialty and value-added products, producing kraft paper bags with superior durability, barrier properties, and self-sealing capabilities. This focus on high-performance and functional packaging meets the demands of diverse sectors, including food, retail, and industrial applications, supporting Japan’s leadership in sustainable and technologically advanced packaging solutions.

Brazil’s Kraft Paper Bag Market Advances with Sustainability and Innovative Packaging Solutions

Brazil’s kraft paper bag market is being shaped by the National Solid Waste Policy, amended in April 2022, which establishes long-term goals for sustainable waste management. The market is experiencing rapid technological innovation, with companies like Klabin launching 100% recyclable and repulpable solutions such as the Wicket Paper Bag for diapers and the Eukaliner kraftliner made of 100% eucalyptus.

Key applications are concentrated in the food and beverage, agricultural, and processed goods sectors, reflecting the growing demand for environmentally responsible packaging. Corporate investments, including Klabin’s plans for a new 450,000 tpy recycled paper unit, highlight both domestic and international interest in the market, reinforcing Brazil’s position as a key player in sustainable kraft paper bag production.

Kraft Paper Bag Market Report Scope

Kraft Paper Bag Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.4 Billion

|

|

Market Size (2034)

|

$6.7 Billion

|

|

Market Growth Rate

|

4.7%

|

|

Segments

|

By Product Type (Pasted Valve Bags, Sewn Open Mouth Bags, Flat Bottom Bags, Others), By Paper Type (Brown Kraft Paper, White Kraft Paper), By Application (Food & Beverages, Retail & Consumer Goods, Building & Construction, Chemicals, Other Applications), By End-Use (Commercial, Industrial, Household)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Mondi Group, International Paper Company, Smurfit Kappa Group, WestRock Company, Oji Holdings Corporation, Stora Enso Oyj, DS Smith Plc, Novolex, Billerud AB, Packaging Corporation of America (PCA), Segezha Group, Klabin S.A., Irani Papel e Embalagem S.A., Nordic Paper, Bagitan Packaging

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Kraft Paper Bag Market Segmentation

By Product Type

- Pasted Valve Bags

- Sewn Open Mouth Bags

- Flat Bottom Bags

- Others

By Paper Type

- Brown Kraft Paper

- White Kraft Paper

By Application

- Food & Beverages

- Retail & Consumer Goods

- Building & Construction

- Chemicals

- Other Applications

By End-Use

- Commercial

- Industrial

- Household

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Kraft Paper Bag Market

- Mondi Group

- International Paper Company

- Smurfit Kappa Group

- WestRock Company

- Oji Holdings Corporation

- Stora Enso Oyj

- DS Smith Plc

- Novolex

- Billerud AB

- Packaging Corporation of America (PCA)

- Segezha Group

- Klabin S.A.

- Irani Papel e Embalagem S.A.

- Nordic Paper

- Bagitan Packaging

* List Not Exhaustive

Methodology

The research methodology adopted by USDAnalytics for analyzing the Kraft Paper Bag Market integrates a combination of primary and secondary research to provide actionable insights for industry professionals. Primary research includes structured interviews with manufacturers, distributors, and end-users across retail, e-commerce, food & beverages, and building & construction sectors to validate demand trends, material innovations, and regulatory impact. Secondary research involves the analysis of company reports, government regulations, sustainability frameworks, and trade data to identify macro and microeconomic drivers shaping market growth. A bottom-up approach has been employed to assess product type, paper type, and end-use applications, while a top-down model has been applied to validate overall market estimates and forecasts. Advanced data analytics tools and comparative benchmarking were used to evaluate competitive strategies, recent innovations, and mergers & acquisitions. This rigorous methodology ensures that USDAnalytics delivers an accurate, fact-driven, and comprehensive market outlook, helping stakeholders navigate evolving sustainability mandates, consumer expectations, and circular economy objectives.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.