Liquid Packaging Carton Market Overview: Growth Outlook and Industry Statistics

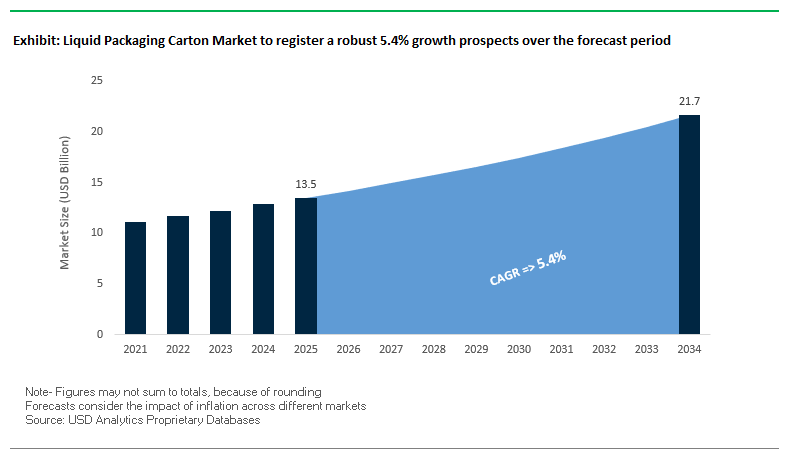

The global liquid packaging carton market is projected to grow from $13.5 billion in 2025 to $21.7 billion by 2034, expanding at a CAGR of 5.4%. This growth reflects the industry’s strong alignment with the circular economy, shifting consumer trends toward plant-based beverages, and rising demand for lightweight, recyclable, and durable packaging solutions across food and beverage supply chains. Unlike conventional plastic and glass containers, liquid cartons are derived primarily from renewable wood fibers sourced from responsibly managed forests, making them a frontrunner in sustainable packaging innovation.

Aseptic technology remains the backbone of the industry, accounting for over 60% of total market volume. These multi-layered cartons significantly extend the shelf life of UHT milk, juices, and functional beverages for up to 18 months without refrigeration, making them indispensable for global food logistics and reducing food waste. Moreover, the e-commerce boom is reinforcing the relevance of cartons as their rectangular design optimizes stacking, lowers freight costs, and reduces breakage compared to bottles.

The rising global appetite for plant-based beverages is another transformative factor. With over 59% of brands adopting cartons for almond, soy, oat, and functional beverages, manufacturers are capitalizing on this trend to strengthen their market presence. For industry professionals and buyers, these shifts highlight why cartons are not only sustainable but also strategically aligned with evolving consumer and retail dynamics.

Key Insights at a Glance

- Market size expected to reach $21.7 billion by 2034 at a 5.4% CAGR.

- Aseptic packaging dominates with 60%+ share, ensuring longer shelf life and reduced food waste.

- E-commerce logistics tailwinds driving adoption due to cost-efficiency in transport and storage.

- Plant-based beverage growth creating opportunities, with nearly 6 in 10 brands using cartons.

- Strong industry alignment with circular economy and renewable material sourcing.

Market Analysis: Recent Industry Developments

The liquid packaging carton industry is witnessing rapid innovation, investment, and expansion across multiple geographies. In September 2025, Mondi Group launched its FunctionalBarrier Paper Ultimate at Fachpack 2025, a breakthrough recyclable paper material with ultra-high barrier protection against oxygen and water vapor. This innovation addresses industry challenges in replacing plastic and aluminum layers, supporting the global shift toward 100% recyclable solutions.

Strategic investments are reshaping the supply base. In July 2025, SIG committed an additional $35 million to expand its Querétaro, Mexico plant, boosting output by 50% to meet growing North American demand. Similarly, Elopak reinforced its North American footprint in May 2025 with the opening of its first U.S. carton converting plant in Little Rock, Arkansas, catering to the surge in sustainable packaging demand from retailers and beverage brands.

Sustainability-driven partnerships are also transforming the value chain. In June 2025, Tetra Pak partnered with Fiat to repurpose recycled carton materials into automotive components, showcasing the rise of high-value secondary markets for carton recycling. The same month, Mondi announced plans to achieve 90% energy self-sufficiency at its Slovakian pulp and paper mill by deploying a new biomass power plant, reinforcing its climate commitments. Furthermore, in February 2025, SIG opened its first aseptic carton plant in India, cementing its presence in one of the fastest-growing markets for packaged beverages.

Innovation in formats is accelerating. In April 2025, Tetra Pak partnered with a European juice brand to launch the Tetra Prisma® Aseptic 300 Edge carton, featuring a tethered cap designed to reduce litter and maximize renewable material content. Meanwhile, Billerud launched ConFlex® HeatSeal in March 2025, a recyclable, heat-sealable paper offering sustainable alternatives to multi-layer plastic.

Key Trends and Strategic Opportunities Shaping the Liquid Packaging Carton Market

Strategic Shift to Plant-Based Polymers and Reduced Plastic Content

The liquid packaging carton (LPC) market is witnessing a decisive move toward plant-based polymers and reduced fossil-fuel content. Leading manufacturers are adopting bio-based polymers derived from sugarcane and other renewable resources for plastic layers and closures, targeting a significant reduction in lifecycle carbon footprint. Tetra Pak’s new paper-based barrier, when combined with plant-based polymers, cuts carbon emissions from base materials by up to 33%, illustrating the strong environmental impact of this transition. Increased renewable content is evident in Elopak’s Natural Brown Board cartons, which contributed to over 2,200 tonnes of CO₂ savings in 2024, with renewable content reaching 90% when combined with bio-based plastics. Strategic capital investments support this trend; Elopak deployed part of a NOK 2.7 billion ($232 million) green bond in 2024 to scale production of sustainable paper-based cartons in North America. Circular economy initiatives further bolster this movement—Tetra Pak launched packaging in India containing 5% certified recycled polymers in 2025, fully complying with the country’s Plastic Waste Management rules, demonstrating how recycled and plant-based materials can coexist to meet sustainability targets.

Integration of Digital Watermarking for Enhanced Recycling and Traceability

Digital watermarking technology is becoming a game-changer in the LPC market, enhancing recycling efficiency and supply chain traceability. Through initiatives like HolyGrail 2.0, manufacturers embed imperceptible codes in packaging to facilitate high-speed sorting at recycling facilities. Industrial trials in France achieved 95.1% sorting efficiency with two-pass detection, marking a substantial improvement over conventional optical systems. Beyond sorting, watermarks enable new capabilities, including differentiation between food-grade and non-food-grade materials, and even specific polymer types, supporting purer recycled streams and high-value applications. Extensive collaboration under HolyGrail 2.0, involving over 130 organizations across the packaging value chain, highlights industry-wide commitment to advancing circularity. Additionally, digital watermarks provide traceability across the supply chain, offering brands actionable insights and compliance with evolving regulations like the EU Packaging and Packaging Waste Regulation (PPWR), enhancing transparency and consumer trust.

Development of High-Barrier, All-Polymer Cartons for Aseptic Applications

A major growth opportunity lies in creating fully recyclable all-polymer aseptic cartons, eliminating aluminum foil while maintaining shelf-stable protection. Traditional aluminum layers hinder recyclability in standard paper streams, but companies like SIG are pioneering high-barrier, alu-layer-free cartons. In September 2025, Berglandmilch, Austria’s leading dairy brand, adopted SIG’s solution, exemplifying real-world adoption of fully recyclable structures. These all-polymer cartons provide uncompromised protection against oxygen and light, ensuring product shelf life without refrigeration. Importantly, these solutions are compatible with existing polyolefin recycling streams, enabling seamless integration into circular systems and offering brand owners a sustainable packaging option aligned with global environmental commitments.

Expansion into New Product Categories with Enhanced Functional Packaging

The liquid carton format offers significant potential for expansion into emerging product categories such as wine, plant-based beverages, liquid eggs, and meal kits. Functional beverage demand is driving this growth, with plant-based milks and ready-to-drink coffee benefiting from cartons’ sustainability, convenience, and long shelf-stable life without preservatives. Advanced barrier technologies have enabled packaging of sensitive products like wine, protecting contents from oxygen and light while reducing transport weight. New carton designs, such as SIG’s DomeMini, and innovative dispensing features, including tamper-protected taps, enhance convenience, versatility, and consumer appeal. This functional packaging evolution positions liquid cartons as a competitive, sustainable alternative to traditional glass and plastic containers across diverse beverage and liquid food segments.

Competitive Landscape: Leading Companies in the Liquid Packaging Carton Market

The global liquid packaging carton market is moderately consolidated, with a few major players shaping innovation, capacity expansion, and sustainability initiatives. Companies like Tetra Pak, SIG, Elopak, Billerud, and Mondi Group are spearheading product developments, recycling programs, and global plant expansions to capture share in this growing market.

Tetra Pak: Driving Circular Economy Leadership

Tetra Pak is the industry’s largest player with an extensive portfolio of aseptic and non-aseptic cartons. In June 2025, it partnered with Fiat to reuse recycled cartons in automotive parts, signaling its commitment to creating circular value chains. Its sustainability report highlights a 54% reduction in operational GHG emissions since 2019, with strong investment in renewable packaging like Tetra Rex Plant-based and Tetra Prisma Aseptic. By integrating digital solutions for track-and-trace and consumer engagement, Tetra Pak solidifies its leadership in sustainable and smart packaging.

SIG Combibloc: Expansion into Growth Markets

SIG Combibloc is aggressively scaling operations across North America and Asia. Its $35 million expansion in Mexico (July 2025) and the inauguration of an aseptic carton plant in India (February 2025) highlight its focus on capturing growth in emerging beverage markets. Known for its combibloc EcoPlus and combibloc NNP products, SIG leverages smart factory solutions and flexible filling technologies to help customers adapt to changing consumer preferences. Its end-to-end solutions for sustainability, convenience, and rapid changeover remain core to its strategy.

Elopak: Strengthening North American Presence

Elopak has sharpened its focus on North America with the opening of its Little Rock, Arkansas plant in May 2025, a move that aligns with its “Repackaging Tomorrow” strategy. Its Pure-Fill platform enables greater flexibility in customer operations, while its gable-top cartons remain a preferred choice for fresh milk and juices. With 2.4% YoY revenue growth in Q2 2025, Elopak is leveraging rising demand for fiber-based packaging and positioning itself as a leading alternative to plastic.

Billerud: Innovating Sustainable Paper Materials

Billerud plays a vital role as a supplier of high-performance paperboard for liquid packaging cartons. Its launch of ConFlex® HeatSeal (March 2025) provides a heat-sealable, recyclable paper that addresses customer demand for sustainable alternatives to plastic-based multilayers. The company’s Way Forward strategy underlines its focus on investments in U.S. mills to expand production capabilities while advancing sustainability. Recognized with an EcoVadis gold rating, Billerud is among the top 5% of global firms for sustainability.

Mondi Group: Advancing Barrier Paper Innovations

Mondi is a frontrunner in high-barrier packaging innovations. The FunctionalBarrier Paper Ultimate launched in September 2025 offers a recyclable solution with ultra-high protection against oxygen and moisture, addressing key technical challenges in liquid packaging. Its MAP2030 strategy commits to making all packaging reusable, recyclable, or compostable by 2025. With a vertically integrated model spanning forestry to finished products, Mondi ensures full supply chain control and delivers sustainable, high-performance packaging solutions for global customers.

Liquid Packaging Carton Market Share Insights

Brick Cartons Hold Market Share Leadership by Type in the Liquid Packaging Carton Industry

Brick cartons dominate the liquid packaging carton industry with a commanding 62% share, driven by their role as the global standard for aseptic, long-life packaging. Their lightweight, stackable format delivers unrivaled logistics efficiency and cost savings, making them the preferred solution for high-volume products like UHT milk, fruit juices, and plant-based dairy alternatives. Gable-top cartons maintain a strong second position, associated with fresh, refrigerated products in markets like North America and Europe where consumers equate this format with quality and freshness. Shaped cartons, while representing a smaller niche, serve as a powerful brand differentiation tool in premium categories such as wines, spirits, and high-end juices, where distinctive aesthetics justify higher costs. Collectively, these dynamics illustrate how brick cartons anchor high-volume aseptic markets, gable tops maintain relevance in fresh dairy, and shaped cartons capture premium brand-driven applications.

Dairy Products Dominate Market Share by Application in the Liquid Packaging Carton Industry

Dairy products hold the largest 40% application share of the liquid packaging carton market, underscoring their central role in both aseptic and fresh formats. UHT milk and cream drive high-volume demand for brick cartons, while fresh milk and refrigerated dairy drinks sustain strong adoption of gable-top formats. A notable driver of recent growth is the surging plant-based dairy sector, where oat, soy, and almond milk are overwhelmingly packaged in cartons to align with consumer expectations for sustainability and naturalness. Juices and beverages remain the core aseptic segment, nearly rivaling dairy in share, supported by cartons’ proven ability to protect sensitive nutrients and flavors in juice and still drinks. Wine and spirits continue to expand rapidly, leveraging cartons’ sustainability, lighter weight, and extended preservation capabilities to disrupt traditional glass packaging. Soups, sauces, and emerging applications such as liquid eggs and supplements reinforce the versatility of cartons in extending shelf-life across diverse liquid categories. This distribution highlights how dairy leads in volume, juices anchor aseptic credibility, and premium alcohol drives high-value growth opportunities.

United States Liquid Packaging Carton Market Expands Through Sustainable Fiber-Based Solutions

The U.S. liquid packaging carton (LPC) market is heavily influenced by a fragmented regulatory environment, with FDA regulations ensuring food and beverage safety and state-level Extended Producer Responsibility (EPR) laws driving the adoption of renewable and recyclable fiber-based packaging. This regulatory push encourages brands to move away from single-use plastics toward more sustainable liquid packaging cartons, fostering growth in eco-friendly packaging alternatives.

Technological advancements are reshaping the industry, with investments exceeding $10 million by leading U.S. carton producers in 2024 to expand production, improve printing and sealing technologies, and develop cartons for non-traditional applications, including soaps, cleansers, and lubricants. Corporate activities, such as Suzano’s acquisition of Pactiv Evergreen mills, are strengthening North American capabilities and expanding product portfolios. Demand remains robust in dairy, juice, plant-based beverages, and direct-to-consumer e-commerce channels, where high-barrier cartons are essential for product freshness and durability. Sustainability trends, including mono-polymer coatings and reduced foil loading, are further driving market adoption and aligning with recyclable paper packaging initiatives promoted by the AF&PA.

Germany Drives Liquid Packaging Carton Innovation Through Circular Economy Leadership

Germany’s liquid packaging carton market benefits from stringent regulations such as the Packaging Act (VerpackG) and the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, mandating full recyclability or reusability by 2030. This legislation accelerates the adoption of sustainable paper-based packaging and incentivizes innovation in high-performance aseptic cartons, such as Elopak’s Pure-Pak® eSense, the first aseptic carton without aluminum layers, simplifying recyclability while maintaining shelf life.

Germany’s focus on the circular economy and robust recycling infrastructure encourages companies to design packaging optimized for recovery and reuse. Corporate investments are aimed at enhancing production capabilities and launching eco-friendly liquid packaging solutions to meet growing regulatory and consumer demand. This combination of regulatory stringency, technological innovation, and sustainability leadership positions Germany as a global benchmark for renewable and recyclable liquid packaging cartons.

China’s Liquid Packaging Carton Market Grows With Domestic Manufacturing and Automation

China’s liquid packaging carton industry is guided by governmental initiatives under the dual carbon goal and the Action Plan for Large-Scale Equipment Updates, encouraging sustainable material adoption, including LPB. Regulatory reforms, notably GB/T 31268, target excessive packaging in e-commerce, which is a primary channel for liquid packaging cartons.

Technological advancements include automation, AI integration, and investment in aseptic liquid packaging board production, highlighted by Shandong Bohui Paper Industry’s RMB 40 million facility upgrade. Domestic manufacturing is emphasized to reduce reliance on imports while meeting growing demand in food and beverage, electronics, and e-commerce sectors. These trends are positioning China as a leader in high-quality, circular liquid packaging carton production.

India’s Liquid Packaging Carton Market Accelerates With Make in India and Food Processing Growth

India’s LPC market is supported by the Make in India initiative and incentives from the Ministry of Food Processing Industries (MoFPI), which enhance domestic manufacturing and cold-chain efficiency. Technological adoption is increasing, exemplified by UFlex commissioning India’s first U-shaped paper straw line and producing 10 billion aseptic liquid packs annually, aligning with sustainability goals and modern packaging standards.

Key applications include dairy, beverages, and pharmaceuticals, driven by rising exports and the need for high-performance, internationally compliant cartons. Investments in production facilities and adoption of advanced materials highlight India’s growth potential in eco-friendly liquid packaging cartons, supporting both domestic and global market expansion.

Japan’s Liquid Packaging Carton Market Focuses on Specialty Coatings and Regulatory Compliance

Japan’s liquid packaging carton industry is a hub of precision manufacturing and advanced material innovation, led by players like Nippon Paper Industries, which emphasizes expanding its packaging business foundation under its 2025 Medium-Term Business Plan. Regulatory updates effective June 2025, including a “positive list” for synthetic materials in food containers, are driving safer, compliant coatings for liquid packaging cartons.

The Japanese market is pivoting toward specialty and value-added LPB products, including self-sealing cartons and high-barrier options, catering to food, beverage, and pharmaceutical sectors. Strategies such as differentiation through total system integration and global collaboration are enabling companies to innovate rapidly, enhancing functionality, compliance, and sustainability in liquid packaging cartons.

Brazil’s Liquid Packaging Carton Market Expands Through Sustainable Investments and Bio-Based Innovations

Brazil’s liquid packaging carton market is strongly influenced by the National Solid Waste Policy, promoting sustainable packaging and waste reduction. Technological advancements include biodegradable, recyclable, and compostable LPB formats, with suppliers introducing bio-based polyethylene derived from sugarcane to reduce fossil fuel dependency and support carbon neutrality.

Corporate investments, such as Forest Paper Group’s R$60 million modernization project, are increasing production capacity by 25% for recycled linerboard, meeting the growing demand in food, beverage, and agricultural sectors. Rising urbanization, health awareness, and sustainability initiatives are shifting demand toward reusable and recyclable liquid packaging cartons, attracting both domestic and international players.

Liquid Packaging Carton Market Report Scope

Liquid Packaging Carton Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$13.5 Billion

|

|

Market Size (2034)

|

$21.7 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Material (Paperboard, PE, Aluminum), By Carton Type (Gable Top, Brick, Shaped), By Application (Dairy Products, Juices & Beverages, Wine & Spirits, Soups & Sauces, Other Applications), By Technology (Aseptic Packaging, Non-Aseptic Packaging)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Tetra Pak International S.A., SIG Group AG, Elopak ASA, Smurfit Kappa Group, Mondi Group, Nippon Paper Industries Co., Ltd., DS Smith Plc, International Paper, Uflex Ltd., WestRock Company, BillerudKorsnäs AB, Greatview Aseptic Packaging Co., Ltd., AR Packaging Group AB, Evergreen Packaging, Lami Packaging (Kunshan) Co. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Liquid Packaging Carton Market Segmentation

By Material

By Carton Type

By Application

- Dairy Products

- Juices & Beverages

- Wine & Spirits

- Soups & Sauces

- Other Applications

By Technology

- Aseptic Packaging

- Non-Aseptic Packaging

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Liquid Packaging Carton Market

- Tetra Pak International S.A.

- SIG Group AG

- Elopak ASA

- Smurfit Kappa Group

- Mondi Group

- Nippon Paper Industries Co., Ltd.

- DS Smith Plc

- International Paper

- Uflex Ltd.

- WestRock Company

- BillerudKorsnäs AB

- Greatview Aseptic Packaging Co., Ltd.

- AR Packaging Group AB

- Evergreen Packaging

- Lami Packaging (Kunshan) Co. Ltd.

* List Not Exhaustive

Methodology

The research methodology for the Liquid Packaging Carton Market combines primary and secondary approaches to ensure high data reliability and market accuracy. Primary research involved structured interviews with industry executives, packaging engineers, sustainability specialists, and supply chain stakeholders across key global regions, capturing insights on emerging trends, technological adoption, and regulatory impacts. Secondary research encompassed analysis of annual reports, patents, regulatory databases, sustainability disclosures, and verified industry publications to validate market dynamics and competitive positioning. Advanced data triangulation techniques were applied to corroborate market sizing, growth projections, and investment trends, integrating macroeconomic indicators, raw material pricing patterns, and innovations in aseptic and non-aseptic packaging technologies. Forecasting models employed both top-down and bottom-up approaches, while regional insights were contextualized against policy frameworks, consumer adoption trends, and trade flows. This rigorous, multi-layered methodology ensures that USDAnalytics delivers accurate, fact-based, and actionable insights tailored to professionals operating in the global Liquid Packaging Carton Market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.