Lubricant Additives Market Outlook

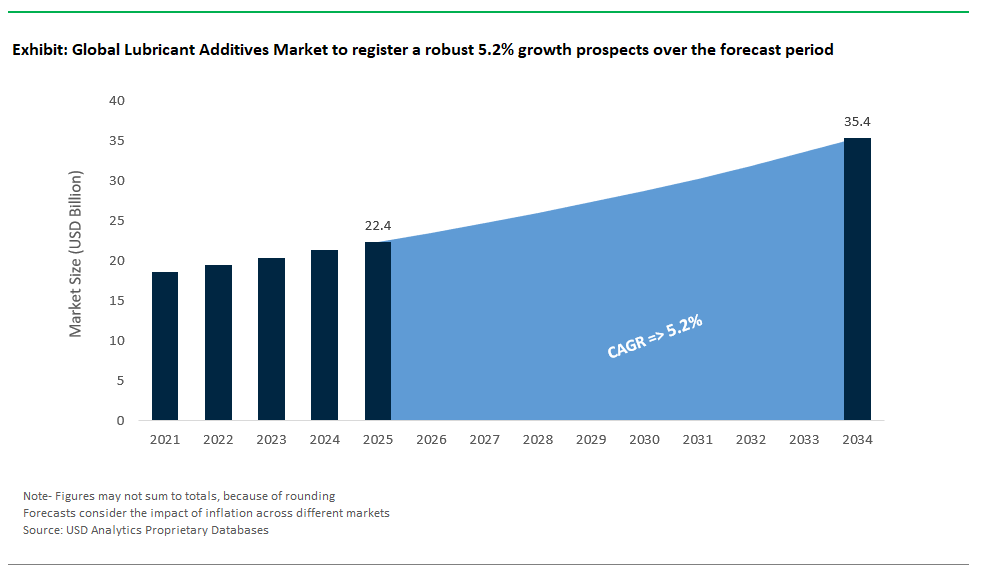

The lubricant additives sector is poised for robust growth, growing from $22.4 billion in 2025 to $35.4 billion by 2034 with a CAGR of 5.2%. This expansion reflects the critical role that lubricant additives play in making lubricants last longer and perform better in a wide range of automotive, industrial, and specialty applications.” Lubricant additives Under the hood of every car, boat and plane is a little heart called a lubricant, which provides protection to the system’s parts against wear, corrosion and overheating.

With the demand of enhanced performance standards in equipment, the market for lubricant additives appears to be increasingly influenced by the transition towards fuel-efficient engine oils, stringent global emission regulations and the rise of environmentally friendly lubricants (EALs) and bio-based additives. These chemicals serve to provide anti-wear, anti-oxidant, anti-corrosion, dispersancy, detergency and viscosity modifying properties all of which contribute to the performance and lifetime of the same. While the industry increasingly looks to green chemistry, R&D and tailored additive packages, ongoing partnerships keep competitors in check as the world becomes a place that is not merely the best lubricant technically, but also a green and sustainable lubricant.

Market Analysis: Strategic Acquisitions and Innovations Reshape the Lubricant Additives Industry

Industry developments in the global lubricant additives market demonstrate an industry on the move, characterised by the ongoing release of new products, M&A activity and a push for sustainable innovation. July 2025 saw the focus of research shift to eco-friendly lubricating technology, with the development of new additives packages aimed at reducing friction and wear, increasing energy efficiency and extending mechanical life. Artificial intelligence (AI) is also being piloted to optimize formulation and predict performance, signaling a digital transformation leap for the industry.

M&A is suddenly the talk of the industry. Vibra Energia and Cosan S.A. began discussions on Moove lubricants business in July-21, showcasing the evolving industry consolidation affecting global procurement and additive supply strategies. In India, Shell Lubricants’ recently concluded purchase of Raj Petro Specialities Pvt. enhances its regional power and will spur fresh demand for custom additive sourcing. In November Fuchs purchased IRMCO Advanced Metalforming Lubricants Technologies in Europe, adding to its position in metalworking fluids and demand for high performance additives.

The years 2024 and 2025 have seen the launch of Petrolad® 750 by the BRB Lube Oil Additives & Chemicals as a low cost high performance additive package for transmission and power steering fluids and is indicative of the market place emphasis on value and performance. January 2025 – Perstorp has introduced a new pair of synthetic esters at the Interflam exhibition for flame retardants, where they are critical as base fluids and additive carriers for Environmentally Acceptable Lubricants (EALs) and high-performance lubricants. Consolidation in the Industry Continues Paeonia Group acquired a leading lubricant testing and research company, Savant Group (formerly Intertek) to beef up advanced additive testing and performance validation capacities.

OEM approvals remain driving demand and validation of high-tier additives. Chevron Oronite obtained Volvo VDS-5 approval for its OLOA 61530 additive in 2024 for the heavy-duty lubricant market (November). The expanded distribution agreement, which was announced in 2024, between BASF (Burghausen, Germany) and Lubrizol (Wickliffe, OH), will enable EMGARD and Plurasafe product availability to reach further into industrial lubricants. These strategic plays and product evolutions reflect a market that is dynamic, global, and increasingly more about sustainability and performance.

Trends and Opportunities: Green Chemistry and Automotive Innovation Shape Lubricant Additives Growth

Rapidly Increasing demand for environmentally Friendly Lubricants and Bio Based Additives

The sustainability trend is quickly changing the lubricant additives sector. Regulations set out by organizations such as the U.S. EPA and the EU Ecolabel now require brae oil use, as they ensure that operations can use non-toxic, biodegradable and low bioaccumulating lubricants even when operating near environmentally sensitive sites, such as marine or forestry-related work. This development has generated an increasing use of synthetic esters including Polyalkylene Glycols (PAGs), and vegetable oils as base fluids for which specialized bio-based additives are needed for enhanced performance. Recent research suggests that almost half of the 40 million tons of lubricants that are used each year are released into the environment, underlining the urgency of finding greener alternatives.

Sector initiatives are taking circularity and sustainability to the next level. Trade associations such ATIEL and UEIL are developing new standards and working groups for re-refined base oils and renewable materials in lubricants. Players like LANXESS are already promoting OSPAR-certified additives for offshore use, positioning themselves against regulatory and environmental concerns. The result is a surge of R&D in the green chemistry of lubricant additives, where the challenges are to achieve high performance along with environmental acceptability. In addition, a collaboration between producers and base oil suppliers is gaining in importance for the development of lubricant formulations that are sustainable in their life cycle, changing also sourcing and production strategy in the industry.

Surging Automotive Demand for Fuel Efficiency and Extended Drain Intervals

The international motor vehicle market is a key growth propeller for lubricant additives as car manufacturers and end-users seek lubricants that help to meet increasingly challenging fuel economy and emission regulations while still maximizing engine life. State-of-the-art additive technology is allowing the most recent engine oils to address a growing list of 2024 ACEA specifications and new viscosity grades (such as F01) to ensure oil cleanliness, friction reduction and wear prevention in more stringent operating conditions. The need for better dispersants, detergents, anti-wear agents, and friction modifiers is greater than ever before for both gasoline and heavy-duty diesel engines. Efficient lubrication in industry can achieve energy savings of up to 10%, adds the US Department of Energy quoting actual savings in cost and emissions. The addition of new products – like BRB’s Petrolad® 750 and Chevron Oronite’s VDS-5 approved additives – further demonstrates this focus on performance and regulation. With OEMs increasingly specifying new standards and extending service intervals, the demand for better lubricant additives will continue to grow.

Competitive Landscape: Global Leaders Drive Innovation and Sustainability in Lubricant Additives

The lubricant additives market is defined by a select group of multinational leaders, each leveraging deep R&D, global distribution, and industry partnerships to maintain a competitive edge.

The Lubrizol Corporation: Advancing Additive Chemistry and Sustainability

Lubrizol is a global leader in additive technology for lubricants, with a broad product portfolio and a long-term commitment to R&D and digitalization. The February 2024 collaboration with BASF for the production and distribution of EMGARD and Plurasafe industrial products is a strategic extension into industrial additives. Lubrizol offers a range of dispersants, detergents, anti-wear, antioxidants, viscosity modifiers and friction modifiers for automotive to marine applications. Its main strategy focuses on sustainable technology and digital tools as well as enforcement of environmental regulations.

Infineum International Limited: Delivering Advanced Additive Solutions for Fuel Efficiency

An ExxonMobil, and Shell joint venture company, Infineum is a world-class formulator, manufacturer and marketer of fuel and lubricant additives. The latter, commissioned in 2014 consisting of a new-engine category II solution to MAN B&W engines, is just one example that reflects the innovative focus of their work,” he says. Medrades believes that Infineum’s focus is to offer additive technology that enables customers to extend oil drains, improve fuel economy and comply with the latest emissions and performance standards in automotive and industrial applications.

Afton Chemical Corporation: Customer-Centric Innovation and Global Growth

Afton Chemical, a part of NewMarket Corporation, is a worldwide leader in the development of high-performance additives, with substantial growth in Asia-Pacific and being customer-centric. Offering a variety of packages for engine oils, of transmission and axel fluids and industrial lubricants, Afton focuses on deliverable cost, regulation and unique performance profiles. Its model is to provide value-added, innovative products that address changing market and regulatory requirements, for example, increased gasoline mileage and reduced emissions.

Chevron Oronite Company LLC: OEM Approvals and Integrated Supply Leadership

Chevron Oronite, is a Chevron Corporation subsidiary that provides a broad range of quality additive products including sulfonate ashless dispersants, ionic dispersants, PIBSA dispersants, viscosity modifiers, and cold flow modifiers to the lubricant and fuel additive markets. Its automotive and industrial offering in the OLOA® and OGA® lines continue to satisfies customer needs, along with new OEM approvals like Volvo’s VDS-5 which further underscore the attractiveness to our heavy-duty lineup. AVE has a strong focus on ensuring OEM specs and environmental regulations are met with performance-based reliable solutions.

Evonik Industries AG: Sustainable Innovation in Viscosity Modifiers and Pour Point Depressants

A world leader in specialty chemicals, Evonik offers environmentally friendly lubricant additives such as VISCOPLEX® viscosity index improvers, pour point depressants, and VISIOMER® methacrylates for increased efficiency and low-temperature properties. The Company is committed to green chemistry, recycling, and support of the circular economy through quality products for automotive and industrial lubricants. According to Evonik, its approach is based on the innovation of new, next generation fuel and as8 additives that maximise fuel efficiency, life span and environmental compatibility, which makes it different to current additives on the market.

Lubricant Additives Market Share Analysis: Key Segment Insights for 2025

Dispersants and Detergents Drive Growth in Product Type Segment

The product type segment on the lubricant additives market in 2025 held the dominant 22% share and is led by the dispersants. To keep engines clean and running smoothly, this is a crucial part in modern lubricants since its role is to suspend sludge and soot. Detergents (part of the 18%), which work in concert with dispersants that neutralize acids and inhibit deposit formation to help engine oils perform through the miles, offer durability of engine oils and keep them reliable. Additional product segments such as AW/EPs, antioxidants, VIIs, friction modifiers, corrosion/rust inhibitors, pour point depressants and emulsifiers also perform critical functions in prolonging lubricant life, protecting equipment in extreme applications, enhancing fuel economy and maintaining stability in various environmental situations. While friction modifiers are becoming more critical worldwide, as fuel economy standards continue to get more stringent Corrosion inhibitors and pour point depressants have always been critical for operation in harsh and cold conditions.

Automotive Lubricants Command Application Segment, Supported by Industrial Demand

Application of lubricant additives is a major end-user industry and accounts for 65% of global lubricant additives market with automotive lubricants being the major application. Automotive has continued to be driven by ongoing demand for engine oils, transmission fluids and greases - all of it dependent on sophisticated additive chemistry to keep pace with next generation engine technology, emissions requirements and extended drain intervals. The expanding market for electric vehicles (EVs) further fuels additive demand with custom thermal management fluids and gear oils while mitigating declining internal combustion engine volumes. Specialized products, representing 35% of the market, include hydraulic fluids, metalworking fluids, turbine oils, and industrial lubricants. Such applications depend to a great extent on AW/EP additives, antioxidants and corrosion inhibitors in order to maintain reliable performance under harsh conditions ranging from mining and construction equipment to renewable energy systems and precision manufacturing entities.

.png)

China: Self-Reliant Growth and Localization of Additive Production

Lubricant additives market in China is led by enormous investments in manufacturing, infrastructure and one of the world's biggest automobile market. Continuing growth in heavy industry, steel/cement manufacture, and vehicle production are driving enormous demand for dispersants, detergents and special additives. The regulatory environment in China is changing to promote local companies to develop and provide more advanced, fuel efficient and environmentally friendly formulations. This emphasis on self-sufficiency is supported by rapid advancements in domestic strychnine synthesis and formulations. Now local players are ramping up to cater not just to domestic demand but bodies like the wider Asian supply chain, in the case of recent expansions in antioxidant production.

The focus on R&D and environmental considerations has made China the largest consumer and potentially the biggest exporter of premium lubricant additives. Regulatory movement in favor of cleaner lubricants, and better quality continues to drive and shape the industry, also localisation strategies to support costs remain a key part of the equation. As a growing number of Chinese companies now try to invest in innovation to cater to global OEM needs and special passenger and commercial vehicle applications, China is also set to emerge as a leading player on the global lubricant additives supply chain.

United States: Leading Innovation in High-Performance Additive Chemistry

The United States has some of the world's largest and most technically innovative lubricant additive makers including Lubrizol, Afton Chemical and Chevron Oronite. These receipts are international pacesetters of new generation additive chemistries that meet the demands of modern day engines, electric vehicles, aerospace and renewable field. Large R&D investments lead to the development of multifunctional additive packages, which facilitate fuel economy, long oil life, and challenging OEM and EPA specifications. Main article: Lubricants in the United States The United States motor vehicle industry remains a major market for lubricants, but opportunities for growth are slowing, with annual growth rates projected to reach 1 percent in the next five years. Industry analysis and researchers describe the need for measures to address the 'substantial pollution' the industry produces.

Tight regulations on chemical-safety standards, environment sustainability and emissions controls also continue to shape the development of new products and the market. S. manufacturers are seeing a growing interest in sustainable and bio-based additive solutions, driven by changing consumer and regulatory preferences. Strong techological base combined with skilled man power and global partnerships allow US to remain as a leader in global lubricant additives market.

Germany: Specialty Additive Development for High-Performance Markets

The German additive market is known for its leading chemical engineering and speciality chemical production, as well as high-performance automotive industry. Local firms, such as Evonik and LANXESS, are investing heavily to develop sustainable high-performance additives specific for premium vehicles and energy efficient industrial equipment. Government programs in Germany for green chemistry and industrial innovation have led to an environment conducive to the development of eco-friendly additives. The adherence to strict EU standards on chemicals and lubes guarantees that they comply with the highest safety and performance criteria and are as environmentally sound as they are effective.

Dispersants, detergents, advanced anti-wear and pour point depressant additives are in demand from automotive OEMs (original equipment manufacturers), industrial machinery manufacturers and metalworking industries. Innovation is the focus of evolutionary growing technologies of sulfur carrier technologies, and additives for renewable fuels and synthetic lubricants in Germany. As a result, Germany is positioned to serve as a major supplier of high-quality additives to local and worldwide markets.

India: Growing Automotive and Manufacturing Stretch Additive Market Size

Rising industrial growth, high automotive sales, and changing automotive norms are driving India's lubricant additives industry to new levels. The domestic production of lubricants and its raw materials, particularly dispersants, detergents and antioxidants, has grown substantially due to the country’s “Make in India” initiative and infrastructure investments. Rising demand in the automotive industry two and three wheelers, passenger cars, and commercial vehicles is complemented by robust consumption in power generation, cements and steel sectors.

Innovation in local mixing along with entry by international and local players have resulted in a dynamic and competitive market. According to market reports, Indian subscription, while the nation is becoming more and more self-sufficient in plastics, thanks to increased capacity additions and new regional supply chains, as witnessed recently in expansions of aminic antioxidant production. With an increased GBoL quality and stronger emission legislations, the Indian market is now seeing a growing need for specialty and performance additives.

Japan: Precision-Driven Demand for High-Performance Additives

Known for its precision engineering and quality-manufacturing traditions, Japan proved to be classic API country; the same held true for its lubricant additives market. The country is home to an advanced automotive industry, and a growing demand for highly sophisticated additives is seen in automotive, robotics, and electronics manufacturing, especially in the areas of friction modifiers, anti-wear agents, and antioxidants. Ongoing R&D spending is aimed at developing for next generation engine technology and to comply with stringent quality and environmental requirements. Japanese companies focus on reliabilty, stability and long-term plant and equipment life, leading to a demand for quality, high-purity additives. Customer demands and regulation are forcing an innovation focus on friction reduction and fuel economy as well. While Japan leads with high tech manufacturing and automotive technology, its demand for performance additives remains strong and very niche.

Lubricant Additives Market Report Scope

Lubricant Additives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$22.4 Billion

|

|

Market Size (2034)

|

$35.4 Billion

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Product Type (Dispersants, Detergents, Anti-wear Agents (AW) & Extreme Pressure (EP) Additives, Antioxidants, Viscosity Index (VI) Improvers, Friction Modifiers, Corrosion Inhibitors / Rust Inhibitors, Pour Point Depressants (PPD), Emulsifiers, Other Additives)

By Application (Automotive Lubricants, Industrial Lubricants)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Lubrizol Corporation, Infineum International Limited, Afton Chemical Corporation, Chevron Oronite Company LLC, Evonik Industries AG, BASF SE, LANXESS AG, Croda International PLC, Dover Chemical Corporation, SI Group, Inc., TotalEnergies, Fuchs Petrolub SE, Perstorp, BRB International (Petronas Chemicals Group Berhad), VANDERBILT CHEMICALS, LLC.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Lubricant Additives Market Segmentation

By Product Type

- Dispersants

- Detergents

- Anti-wear Agents (AW) & Extreme Pressure (EP) Additives

- Antioxidants

- Viscosity Index (VI) Improvers

- Friction Modifiers

- Corrosion Inhibitors / Rust Inhibitors

- Pour Point Depressants (PPD)

- Emulsifiers

- Other Additives

By Application

Automotive Lubricants

- Passenger Car Motor Oil (PCMO)

- Heavy Duty Engine Oil (HDEO)

- Automatic Transmission Fluid (ATF)

- Gear Oil

- Grease

- Other Automotive Lubricants

Industrial Lubricants

- Industrial Engine Oil

- Hydraulic Fluid

- Metalworking Fluid (MWF)

- Industrial Gear Oil

- Compressor Oil

- Turbine Oil

- Other Industrial Lubricants

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Lubricant Additives Market

- The Lubrizol Corporation

- Infineum International Limited

- Afton Chemical Corporation

- Chevron Oronite Company LLC

- Evonik Industries AG

- BASF SE

- LANXESS AG

- Croda International PLC

- Dover Chemical Corporation

- SI Group, Inc.

- TotalEnergies

- Fuchs Petrolub SE

- Perstorp

- BRB International (Petronas Chemicals Group Berhad)

- VANDERBILT CHEMICALS, LLC.

* List Not Exhaustive

Research Coverage

This report from USDAnalytics dynamically investigates the global Lubricant Additives Market, uncovering significant breakthroughs, reviewing evolving performance requirements, and highlighting major market dynamics. It delivers detailed analysis reviews and critical insights across product types and application sectors, providing a vital resource for lubricant formulators, OEMs, investors, and policymakers. The report thoroughly evaluates market segmentation, geographic expansion, technological advances, and regulatory impacts, using comprehensive historic data (2021–2024) and robust forecasts (2025–2034). It also assesses the roles of leading global and regional companies, enabling readers to capitalize on strategic growth opportunities and respond proactively to shifting trends in lubricant technology, sustainability, and regulation.

By Product Type: Dispersants, Detergents, Anti-wear (AW) & Extreme Pressure (EP) Additives, Antioxidants, Viscosity Index (VI) Improvers, Friction Modifiers, Corrosion/Rust Inhibitors, Pour Point Depressants, Emulsifiers, Other Additives (Demulsifiers, Anti-foam Agents, Tackifiers)

By Application: Automotive Lubricants (PCMO, HDEO, ATF, Gear Oil, Grease, Brake Fluids, Hydraulic Fluids), Industrial Lubricants (Engine Oil, Hydraulic Fluid, Metalworking Fluid, Gear Oil, Compressor Oil, Turbine Oil, Marine & Other)

Geographic Scope: Analysis covers 25+ countries across North America, Europe, Asia Pacific, Latin America, and Middle East & Africa

Historic Data: 2021–2024

Forecast Data: 2025–2034

Companies Covered: Lubrizol, Infineum, Afton Chemical, Chevron Oronite, Evonik, BASF, LANXESS, Croda, Dover Chemical, SI Group, TotalEnergies, Fuchs Petrolub, Perstorp, BRB International, Vanderbilt Chemicals

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.