Rising Adoption of Membrane Bioreactor Systems Driving Strong Market Growth

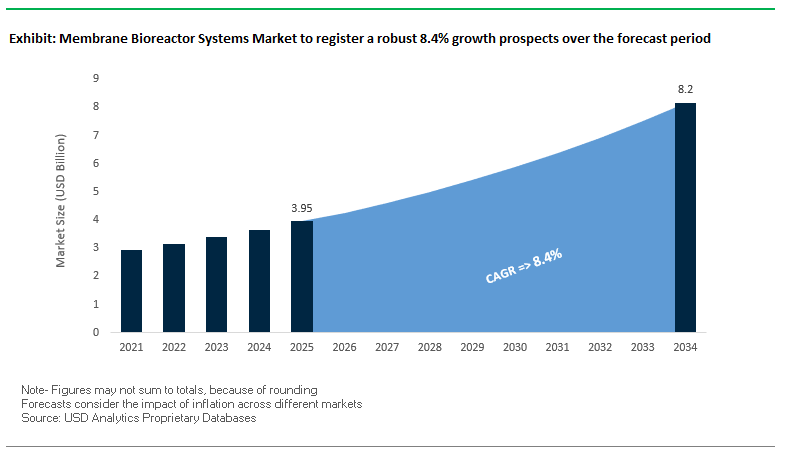

The Global Membrane Bioreactor (MBR) Systems Market is projected to expand from USD 3.95 billion in 2025 to USD 8.2 billion by 2034, growing at a robust CAGR of 8.4%. This surge reflects the critical role MBR systems play in addressing stringent wastewater discharge regulations, water reuse demands, and urbanization-driven land constraints. For industry Stakeholders and buyers, MBR systems provide an optimal balance of high-quality effluent treatment, compact footprint, and operational efficiency, making them indispensable in municipal and industrial wastewater management.

Key Insights Shaping the MBR Market

- Meeting Stringent Water Quality Standards: MBR systems enable compliance with global zero-liquid discharge (ZLD) targets by removing nearly all suspended solids and bacteria, producing effluent suitable for reuse in irrigation, industrial cooling, and even potable blending.

- Compact Footprint for Urban Areas: Compared to conventional wastewater treatment plants, MBRs require far less land, making them highly attractive for densely populated urban centers, resort destinations, and residential communities.

- Energy Efficiency in Operations: Technological advances in aeration and control systems have reduced blower energy consumption by 16.9%, significantly cutting lifecycle costs.

- Water Reuse for Municipal and Industrial Demand: MBR effluent supports non-potable reuse applications like cooling towers, irrigation, and landscaping, helping industries and municipalities address water stress.

Market Analysis: Recent Developments in the MBR Systems Industry

The past year has seen significant momentum in the membrane bioreactor systems industry, with global leaders investing in new technologies, projects, and sustainability-driven initiatives.

In July 2025, SUEZ announced the commissioning of a new biogas production unit at the Seine Aval wastewater treatment plant in Paris. The project highlights how membrane technologies, including MBRs, are being integrated with renewable energy solutions to achieve energy independence. In the same month, Veolia set new benchmarks for large-scale water reuse in Brazil, showcasing its focus on advancing water circularity in Latin America.

August 2025 saw a breakthrough scientific study demonstrating that graphene-modified hollow fiber membranes can improve fouling resistance and flux rates by 30%. This innovation has the potential to cut operational costs for municipal MBR systems, making them more accessible for large-scale deployment. Also in August, research highlighted the efficiency of hybrid MBR systems combined with nanofiltration (NF) and reverse osmosis (RO), enabling higher pollutant removal, including micropollutants and emerging contaminants.

In June 2025, SUEZ expanded its footprint in Asia by winning three new water projects, including a major seawater reverse osmosis (SWRO) plant in the Philippines, where MBR and advanced pretreatment technologies are expected to play a key role. The same month marked the appointment of Xavier Girre as CEO of SUEZ, signaling a strategic leadership shift to drive global expansion in water and waste management solutions.

May 2025 was notable for Asahi Kasei, which unveiled its new medium-term management plan, Trailblaze Together, placing its Life Science and membrane technologies at the core of growth strategy. Meanwhile, in July 2025, Veolia confirmed it will equip France’s largest treated wastewater reuse project in Argelès-sur-Mer, reinforcing its dominance in water reuse solutions.

Key Trends Shaping the Membrane Bioreactor Systems Market

The membrane bioreactor systems market is undergoing a significant transformation, with stricter regulations, water scarcity, and technological innovation driving adoption. A critical trend is the influence of environmental regulations and water scarcity, which are accelerating the use of MBRs in both municipal and industrial applications. For instance, the Central Pollution Control Board (CPCB) in India has mandated tighter effluent standards, while the National Green Tribunal (NGT) has levied fines of over ₹80,000 crore on states for failing to manage wastewater effectively. This reflects a global trend where governments are mandating advanced treatment technologies to secure compliance.

Another major trend is the innovation in membrane materials and hybrid processes, with researchers developing advanced membranes resistant to fouling and capable of higher permeability. Studies in Frontiers in Membrane Science and Technology show hybrid systems integrating MBR with NF or RO to achieve superior removal of micropollutants, which expands the application scope of MBRs, especially in potable reuse projects. Furthermore, the rise of decentralized and modular treatment systems is another defining trend, with companies investing in containerized MBRs for hotels, remote industrial sites, and residential complexes. These flexible solutions are rapidly gaining traction as urbanization and infrastructure challenges demand localized treatment.

In addition, strategic investments and industry consolidation are shaping the competitive landscape, highlighted by Xylem’s acquisition of Evoqua, which consolidated expertise in advanced wastewater treatment and strengthened their MBR portfolio. These dynamics underline the market’s trajectory toward integration, scalability, and resilience.

Emerging Opportunities in the Membrane Bioreactor Systems Market

The growth of the membrane bioreactor systems market presents several compelling opportunities. One of the most promising lies in municipal wastewater reuse, particularly in regions facing acute water scarcity. Cities are increasingly adopting MBRs to upgrade existing plants to higher nutrient removal standards and to produce reclaimed water for irrigation, industrial use, or even indirect potable reuse. Another major opportunity is within industrial wastewater treatment, where MBRs are becoming the technology of choice for industries such as food & beverage, textiles, pharmaceuticals, and chemicals due to their ability to handle high-strength wastewaters while producing reusable effluent. Decentralized applications also represent an untapped opportunity, as modular MBR units can serve off-grid areas or industrial clusters where centralized treatment is impractical. Moreover, with continuous advancements in energy-efficient and fouling-resistant membranes, opportunities for cost reduction and wider adoption are expanding. Strategic partnerships and R&D collaborations further open doors for scaling hybrid MBR solutions, especially in high-value applications like landfill leachate treatment and direct potable reuse projects. Companies that can innovate in scalability, modularity, and hybrid integration stand to capture the most growth in this rapidly consolidating yet innovation-driven market.

Market Share Analysis of the Membrane Bioreactor Systems Market

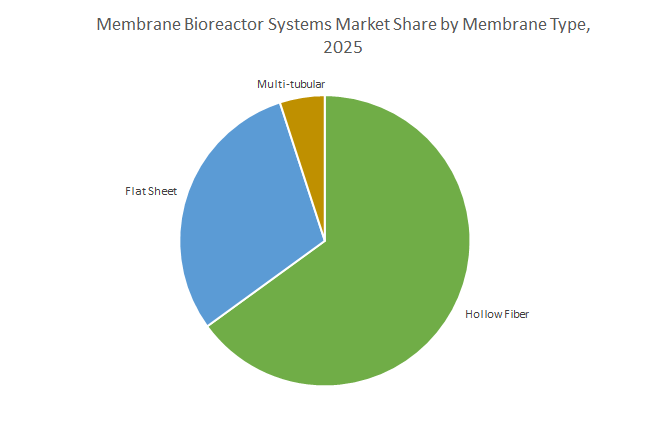

Market Share by Membrane Type

The membrane bioreactor systems market by membrane type is dominated by hollow fiber membranes, projected to capture 65% of the share in 2025. Their high surface-area-to-volume ratio and cost-effectiveness make them the preferred choice for large-scale municipal and industrial applications, as they offer compact footprints and low capital costs. Hollow fiber membranes also support backpulsing and air scouring, ensuring better fouling control and lower operational downtime. Flat sheet membranes, with a stable 30% share, are widely chosen for industrial wastewater streams prone to clogging, such as textile effluents containing fibers or grease-rich wastewater. Their mechanical robustness and easy cleaning process often by manual removal provide operational reliability for smaller and specialized plants. Multi-tubular membranes, though holding only about 5% share, play a critical role in niche applications such as landfill leachate and food processing wastewater, where high-solids loading and viscous effluents render other configurations inefficient. While their overall share is small, their application is indispensable in these demanding treatment environments.

Market Share by System Configuration

The membrane bioreactor systems market by system configuration is overwhelmingly led by submerged (immersed) MBRs, which are projected to account for 95% of installations by 2025. Submerged systems have become the industry standard in both municipal and industrial sectors due to their significantly lower energy consumption compared to external configurations, as they do not require high cross-flow velocities. Their simple design, operational ease, and scalability make them the preferred choice for large wastewater treatment plants across urban and industrial regions. External (sidestream) MBRs, projected at 5%, are limited to specialized high-strength wastewater applications. These include scenarios with extremely high sludge concentrations, elevated operating pressures, or cases requiring high shear rates to control membrane fouling. Although their higher energy demand restricts broader adoption, they are strategically important for industries with challenging effluent profiles, making them a niche yet critical part of the MBR landscape.

Market Share by Application

The membrane bioreactor systems market by application reveals a strong dominance of municipal wastewater treatment, projected to contribute nearly 60% of the market by 2025. Rapid urbanization, stricter nutrient removal regulations, and the growing emphasis on wastewater reuse are fueling municipal adoption, especially in regions with water scarcity. The compact footprint of MBRs further enables upgrades of existing treatment facilities in space-constrained urban settings. Industrial wastewater treatment, accounting for the remaining 40%, is the value-driven segment that showcases the versatility of MBR technology. Industries such as food & beverage (12%) and landfill leachate (8%) represent leading sub-segments, with the former requiring efficient biological treatment of high organic loads and the latter demanding robust solutions to handle toxic and variable leachates. Pharmaceuticals & chemicals (7%) and textiles (6%) are also expanding their adoption due to strict discharge norms targeting toxicity and color removal, respectively. Pulp & paper (4%) and other industrial users (3%) contribute smaller shares but highlight the adaptability of MBRs across diverse wastewater streams. Collectively, the industrial segment underscores MBR technology’s role in reducing water footprints, cutting disposal costs, and supporting sustainability agendas across industries.

China: Regulatory Mandates and Strategic MBR Investments

China’s membrane bioreactor (MBR) systems market is strongly influenced by strict environmental regulations and large-scale government investments. The Ministry of Ecology and Environment (MEE) enforces rigorous wastewater discharge standards, driving the adoption of advanced MBR systems to increase water reuse rates, which China aims to raise by over 25% by 2025. The government has committed approximately USD 8 billion between 2021 and 2025 to develop new sludge processing facilities, a critical component of modern MBR infrastructure. Technological advancements, including the 2024 development of hollow-fiber ultrafiltration membranes with enhanced antifouling properties, aim to reduce operational costs and improve efficiency in MBR systems. Key applications include municipal wastewater treatment, exemplified by Beijing Kunyu River WWPT, which has a capacity of 100,000 m³/d, demonstrating China’s robust deployment of MBR technology for both municipal and industrial wastewater reuse.

United States: Federal Funding and Private Sector MBR Deployment

The U.S. MBR systems market benefits from substantial government funding and private sector innovation. The Bipartisan Infrastructure Law allocates over $50 billion to the EPA to upgrade water infrastructure, targeting emerging contaminants like PFAS that require advanced MBR and membrane filtration solutions. NSF-funded research centers drive innovation in water purification, chemical separations, and biopharmaceutical processing, contributing to technological growth in the MBR space. Companies such as Veolia Water Technologies have deployed MBR treatment capacities to supply water meeting regulated PFAS thresholds to over 140,000 Americans, highlighting private sector leadership in integrating MBR systems for both municipal and industrial wastewater treatment applications.

India: Policy Support and Green Infrastructure Initiatives

India’s membrane bioreactor systems market is growing due to regulatory mandates, urban infrastructure projects, and industrial adoption. The Central Pollution Control Board (CPCB) has introduced stringent discharge standards for all sewage treatment plants effective 2025, mandating the use of advanced MBR systems. Infrastructure projects like the Ghaziabad Nagar Nigam’s Tertiary Sewage Treatment Plant (TSTP), funded by India’s first Certified Green Municipal Bond worth ₹150 crore, utilize MBR and other membrane technologies for wastewater reuse, reducing dependence on freshwater. Additionally, VA TECH WABAG’s seven-year O&M contract for the 110 MLD SWRO Nemmeli Desalination Plant in Chennai, valued at INR 415 crores, highlights significant financial commitment to maintaining and operating MBR-based water treatment systems across India.

Germany: Industrial MBR Applications and Technological Leadership

Germany is a global leader in applying MBR systems for industrial wastewater treatment. Companies like Cerafiltec provide ceramic flat membranes for MBR projects with capacities ranging from 250 m³/d for industrial applications to 10,000 m³/d for municipal treatment. The Fraunhofer Institute for Interfacial Engineering and Biotechnology (IGB) in Heidelberg has developed a decentralized MBR plant with a rotating disk filter, offering high flux and low energy consumption. German multinational MANN+HUMMEL focuses on innovative membrane and digital solutions to address global water challenges, emphasizing MBR applications for industrial processes and green energy solutions, reinforcing Germany’s leadership in sustainable wastewater treatment.

Japan: R&D-Driven MBR Growth and Government Support

Japan’s membrane bioreactor systems market is propelled by strong academic research, corporate innovation, and government initiatives. In 2025, Toray introduced next-generation hollow fiber membranes with 20% higher permeability and reduced fouling, significantly lowering operational costs for MBR systems. The Ministry of the Environment allocated USD 1.2 billion in 2024 to promote sustainable wastewater infrastructure, supporting MBR adoption. Japan has over 3,000 full-scale MBR applications in operation, ranging from small-scale industrial and on-site household wastewater treatment to large municipal facilities, showcasing the country’s mature and diversified MBR market.

Australia: Water Reuse Leadership and Advanced MBR Research

Australia, facing significant water stress, is a leading market for MBR systems due to its focus on water recycling and reuse. Facilities like the Sydney Water Wollongong Water Resource Recovery Facility integrate microfiltration and reverse osmosis with MBR technology to treat wastewater for reuse in irrigating sports fields and industrial applications. Academic research at Victoria University’s Institute for Sustainable Industries and Liveable Cities (ISILC) focuses on increasing water recovery from desalination and minimizing membrane fouling and scaling, critical challenges in MBR systems. These initiatives position Australia as a hub for innovation in membrane-based wastewater treatment and sustainable water management.

Competitive Landscape: Leading Companies in the Global MBR Systems Market

The competitive landscape of the membrane bioreactor systems market is defined by global leaders focusing on technology innovation, energy efficiency, and large-scale water reuse projects. Companies such as SUEZ, Kubota, Mitsubishi Chemical Aqua Solutions, Toray, Memstar, and Xylem dominate the market with diverse product portfolios and strong global project footprints.

SUEZ Water Technologies & Solutions Strengthens Circular Water Management

SUEZ, now integrated under Veolia, leverages its advanced MBR systems as part of a holistic water cycle management strategy. The company is recognized for its large-scale project execution, such as China’s largest membrane-based seawater desalination plant and the Seine Aval biogas integration project in Paris. By focusing on circular economy initiatives, including biochar and biogas recovery from wastewater, and investing in digital monitoring tools, SUEZ enhances both operational efficiency and environmental outcomes.

Kubota Corporation Expands Global Reach with Submerged MBR Leadership

Kubota pioneered the submerged membrane unit (SMU) technology in 1991 and continues to dominate with its flat sheet membranes, known for durability, anti-fouling, and low maintenance. The company has installed over 7,300 MBR systems worldwide, including the largest MBR sewage treatment plant in the Middle East. Kubota’s recent innovations demonstrate up to 43% savings in air flow energy, a key operational cost driver, further strengthening its competitiveness in municipal and industrial wastewater markets.

Mitsubishi Chemical Aqua Solutions Advances Hollow Fiber Innovations

Mitsubishi Chemical Aqua Solutions, with more than 5,000 MBR projects worldwide, specializes in hollow fiber membrane technology through its flagship product STERAPORE™. The membrane’s compact design and high permeate quality make it suitable for municipal, industrial, and even drinking water applications. In June 2024, the company received the Fukuoka Prefecture Governor’s Award for contributions to recycling-oriented water management, reflecting its commitment to sustainability and innovation.

Toray Industries Leverages Polymer Science for Wastewater Reuse

Toray Industries applies its expertise in polymer and material science to develop advanced hollow fiber and flat sheet membranes for MBR systems. The company’s India sewage reuse demonstration plant (March 2024) highlights its strategy of addressing water scarcity in emerging markets. Backed by its Water Research Center in India, Toray is investing heavily in R&D to design membranes tailored to regional water treatment challenges, reinforcing its global leadership in sustainable water solutions.

Memstar Pte Ltd Drives Growth with TIPS PVDF Membrane Technology

Memstar, a specialist in Thermally Induced Phase Separation (TIPS) PVDF hollow fiber membranes, has deployed its systems at over 400 sites worldwide, treating more than 6 million cubic meters of water daily. Its 3G-TIPS fibers provide superior fouling resistance and durability, enabling performance in challenging wastewater streams. With manufacturing bases in Singapore, China, and the USA, Memstar is strategically positioned to meet global demand with localized support and services.

Xylem Inc. Delivers Modular, Plug-and-Play MBR Solutions

Xylem differentiates itself with modular MBR systems designed for compact footprints and plug-and-play scalability. Its solutions are widely adopted across industries, with a case study in Colorado demonstrating success in treating food industry wastewater while meeting strict BOD, TSS, and nutrient discharge limits. By integrating MBR systems with advanced pumps, mixers, and monitoring tools, Xylem delivers cost-effective, energy-efficient solutions. The company’s broader mission of “solving water” positions it as a trusted leader in municipal and industrial reuse projects.

Membrane Bioreactor Systems Market Report Scope

Membrane Bioreactor Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.95 Billion

|

|

Market Size (2034)

|

$8.2 Billion

|

|

Market Growth Rate

|

8.4%

|

|

Segments

|

By Type (Hollow fiber, Flat sheet, Multi-tubular), By System Configuration (Submerged, External), By Application (Municipal wastewater treatment, Industrial wastewater treatment, Food & Beverage, Landfill Leachate, Pharmaceuticals & Chemicals, Textiles, Pulp & Paper)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

SUEZ, DuPont de Nemours, Inc., Veolia, Pentair plc, Xylem Inc., Toray Industries, Inc., Asahi Kasei Corporation, Kubota Corporation, The Dow Chemical Company, Mitsubishi Chemical Corporation, MANN+HUMMEL, Evoqua Water Technologies, LG Chem, Koch Industries, V.A. TECH WABAG Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Membrane Bioreactor Systems Market Segmentation

By Type

- Hollow fiber

- Flat sheet

- Multi-tubular

By System Configuration

By Application

- Municipal wastewater treatment

- Industrial wastewater treatment

- Food & Beverage

- Landfill Leachate

- Pharmaceuticals & Chemicals

- Textiles

- Pulp & Paper

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Membrane Bioreactor Systems Industry include-

- SUEZ

- DuPont de Nemours, Inc.

- Veolia

- Pentair plc

- Xylem Inc.

- Toray Industries, Inc.

- Asahi Kasei Corporation

- Kubota Corporation

- The Dow Chemical Company

- Mitsubishi Chemical Corporation

- MANN+HUMMEL

- Evoqua Water Technologies

- LG Chem

- Koch Industries

- V.A. TECH WABAG Ltd.

*- List not Exhaustive

Research Coverage

This report investigates the global membrane bioreactor (MBR) systems market, delivering analysis reviews on how discharge-limit tightening, water-reuse mandates, and space constraints are accelerating MBR deployments across municipal and industrial plants. It highlights breakthroughs in aeration control, fouling-resistant membranes, and hybrid MBR-NF/RO trains that boost flux and cut lifecycle energy, while recent partnerships, leadership moves, and large reference projects reshape competitive positioning. Mapping adoption drivers from compact footprints to high-quality effluent for reuse, and translating operating metrics into bankable outcomes, USDAnalytics equips buyers and operators with decision-grade insights. With technology benchmarking, country rollouts, and end-user qualification criteria, this report underscores why this report is an essential resource for utilities, EPCs, and industrial owners planning resilient, regulation-ready wastewater upgrades. Scope Includes-

- Segmentation: By Type (Hollow Fiber; Flat Sheet; Multi-tubular), By System Configuration (Submerged; External), By Application (Municipal Wastewater Treatment; Industrial Wastewater Treatment Food & Beverage, Landfill Leachate, Pharmaceuticals & Chemicals, Textiles, Pulp & Paper)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic data 2021–2024; forecasts 2025–2034.

- Companies: Profiles of 15+ companies

Methodology

We apply a mixed-methods approach combining primary interviews (utilities, plant operators, OEMs/EPCs, regulators, and QA/validation leads) with secondary research (standards, patents, technical papers, and filings). Market sizing integrates top-down triangulation from municipal/industrial capex, retrofits, and reuse mandates with bottom-up BOM models that normalize for membrane area, flux (LMH), SRT/MLSS, aeration energy, cleaning intervals, and replacement cycles. Forecasts incorporate learning curves for modules/blowers, energy-price sensitivity, nutrient-limit and PFAS policy cadence, and hybrid-train adoption (MBR→NF/RO). Competitive benchmarking evaluates fouling propensity, air-scour efficiency, integrity testing, uptime, and lifecycle cost per 1,000 m³. Outputs are cross-validated against commissioning data, announced projects, and scenario stress-tests for high-strength/variable influents.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Membrane Bioreactor Systems Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Insights for Stakeholders

1.3. Global Market Snapshot

2. Membrane Bioreactor Systems Market Outlook (2025–2034)

2.1. Introduction: Growth Drivers and Industry Transformation

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $3.95 Billion

2.2.2. Forecasted Market Size (2034): $8.2 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 8.4%

2.3. Key Market Insights

2.3.1. Meeting Stringent Water Quality Standards

2.3.2. Compact Footprint for Urban Areas

2.3.3. Energy Efficiency in Operations

2.3.4. Water Reuse for Municipal and Industrial Demand

3. Recent Developments and Strategic Shifts

3.1. Market Trend: Water Reuse and Circularity

3.1.1. SUEZ Commissions Biogas Production Unit in Paris

3.1.2. Veolia Sets New Benchmarks for Water Reuse in Brazil

3.1.3. Veolia to Equip France’s Largest Treated Wastewater Reuse Project

3.2. Market Trend: Technological Innovation

3.2.1. Scientific Study on Graphene-Modified Membranes

3.2.2. Research on Hybrid MBR Systems

3.3. Market Opportunity: Global Expansion and Strategic Realignment

3.3.1. SUEZ Wins New Water Projects in Asia

3.3.2. Asahi Kasei Unveils Growth Plan Focused on Membranes

3.3.3. New Leadership Appointment at SUEZ

4. Competitive Landscape: Leading Companies

4.1. Market Overview: From Technology Specialists to Global Solution Providers

4.2. Key Competitive Factors

4.2.1. Technology Innovation and R&D Focus

4.2.2. Global Project Footprint and Localized Support

4.2.3. Operational Efficiency and Lifecycle Cost Reduction

4.3. Profiles of Top Players

4.3.1. SUEZ Water Technologies & Solutions

4.3.2. Kubota Corporation

4.3.3. Mitsubishi Chemical Aqua Solutions

4.3.4. Toray Industries

4.3.5. Memstar Pte Ltd

4.3.6. Xylem Inc.

5. Membrane Bioreactor Systems Market – Segmentation Insights

5.1. By Type

5.1.1. Hollow Fiber

5.1.2. Flat Sheet

5.1.3. Multi-tubular

5.2. By System Configuration

5.2.1. Submerged

5.2.2. External

5.3. By Application

5.3.1. Municipal Wastewater Treatment

5.3.2. Industrial Wastewater Treatment

5.3.2.1. Food & Beverage

5.3.2.2. Landfill Leachate

5.3.2.3. Pharmaceuticals & Chemicals

5.3.2.4. Textiles

5.3.2.5. Pulp & Paper

6. Country Analysis and Outlook: Membrane Bioreactor Systems Market

6.1. China: Regulatory Mandates and Strategic Investments

6.2. United States: Federal Funding and Private Sector MBR Deployment

6.3. India: Policy Support and Green Infrastructure Initiatives

6.4. Germany: Industrial MBR Applications and Technological Leadership

6.5. Japan: R&D-Driven MBR Growth and Government Support

6.6. Australia: Water Reuse Leadership and Advanced MBR Research

6.7. Other Key Countries

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Membrane Bioreactor Systems Market Size Outlook by Region (2025-2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By Type

7.1.2. By Application

7.2. Europe Market Size Outlook to 2034

7.2.1. By Type

7.2.2. By Application

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By Type

7.3.2. By Application

7.4. South America Market Size Outlook to 2034

7.4.1. By Type

7.4.2. By Application

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By Type

7.5.2. By Application

8. Company Profiles: Additional Leading Players

8.1. SUEZ

8.2. DuPont de Nemours, Inc.

8.3. Veolia

8.4. Pentair plc

8.5. Xylem Inc.

8.6. Toray Industries, Inc.

8.7. Asahi Kasei Corporation

8.8. Kubota Corporation

8.9. The Dow Chemical Company

8.10. Mitsubishi Chemical Corporation

8.11. MANN+HUMMEL

8.12. Evoqua Water Technologies

8.13. LG Chem

8.14. Koch Industries

8.15. V.A. TECH WABAG Ltd.

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures