Membrane Microfiltration Market Overview: Growth Driven by Water Scarcity, Biopharma Expansion, and Food Safety

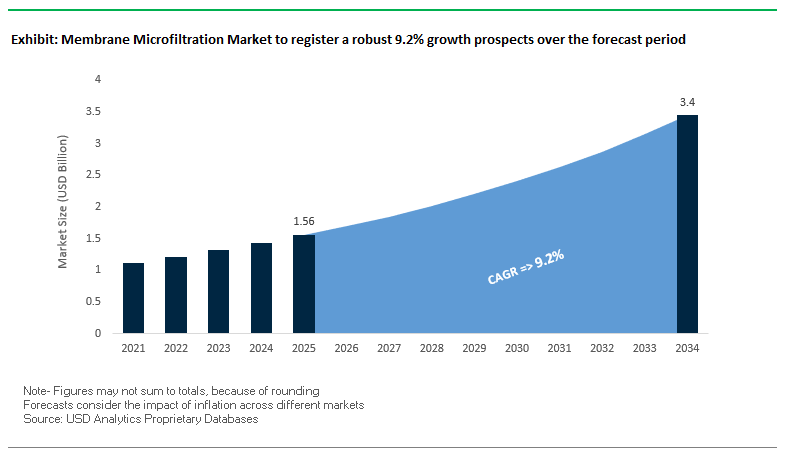

The global membrane microfiltration market is projected to reach USD 1.56 billion in 2025, growing steadily to USD 3.4 billion by 2034 at a CAGR of 9.2%. This strong growth is fueled by rising demand for advanced filtration solutions across water treatment, pharmaceuticals, food and beverage, and industrial wastewater management.

Key insights shaping the membrane microfiltration industry include:

- Stringent Water Quality Regulations: Governments in Asia-Pacific and Europe are enforcing stricter wastewater discharge laws, driving adoption of microfiltration membranes in industrial wastewater treatment.

- Pharmaceutical and Biopharmaceutical Growth: Over 200 new Antibody-Drug Conjugates (ADCs) currently in trials require sterile filtration, boosting demand for pharmaceutical microfiltration technologies.

- Rising Water Scarcity: Microfiltration is increasingly used as a pre-treatment step in desalination and reverse osmosis plants, ensuring long-term freshwater security.

- Food and Beverage Sector Expansion: Dairy and brewing industries rely on microfiltration systems for clarification, sterilization, and shelf-life extension.

Market Analysis: Recent Developments in Membrane Microfiltration Technologies

The membrane microfiltration market is witnessing dynamic growth, fueled by technological innovation, public-private partnerships, and investments in sustainable water infrastructure. Several recent developments highlight the sector’s momentum.

In May 2025, SUEZ and the Senegalese government were recognized by the UN for their public-private partnership in water treatment, emphasizing the role of advanced microfiltration in delivering safe public water. In June 2025, MilliporeSigma partnered with Simtra on a five-year agreement to support drug manufacturing, particularly ADCs, which require high-purity microfiltration processes.

By July 2025, SUEZ commissioned China’s largest membrane-based seawater desalination plant for Wanhua Chemical, with microfiltration serving as a critical pre-treatment step. Around the same time, the company also partnered with Seabex to test biochar for agricultural water retention, showcasing the broader applications of filtration technologies.

In August 2025, research highlighted microfiltration membranes in treating radioactive and heavy metal wastewater, underlining their potential for preventing secondary pollution. The same month, Asahi Kasei’s inclusion in the FTSE4Good Index reinforced the company’s sustainable manufacturing approach, while Nouryon’s new plant in Brazil expanded sodium chlorate capacity to support pulp and paper industries reliant on process water purification. Additionally, Sterlitech Corporation launched a dedicated food and beverage portal, strengthening the role of microfiltration in product quality control.

Emerging Trends and Growth Opportunities in the Membrane Microfiltration Market

Rising Demand for High-Purity Water Treatment Solutions

A major trend in the membrane microfiltration market is the surging demand for high-purity water, particularly in municipal and industrial applications. Regulatory pressure is a key factor, with agencies like the U.S. Environmental Protection Agency (EPA) enforcing strict Surface Water Treatment Rules that mandate the removal of pathogens such as Giardia lamblia and Cryptosporidium. This regulatory landscape positions microfiltration as a critical technology to ensure compliance, public health, and sustainability. Growing urban populations and water scarcity challenges further amplify the role of microfiltration as a frontline defense against microbial contamination in drinking water systems.

Technological Shift Toward Ceramic Membranes

The transition from traditional polymeric membranes to ceramic microfiltration membranes is reshaping the market due to the latter’s superior durability, chemical resistance, and service lifespan. Studies from institutions such as India’s CSIR-Central Glass & Ceramic Research Institute (CGCRI) emphasize the breakthrough performance of alumina-based ceramic membranes with clear water fluxes of 100–200 LMH, proving their viability for industrial water recycling and juice clarification. This advancement highlights a clear trend toward more resilient, sustainable, and cost-effective solutions for industries facing aggressive operational environments.

Expansion of Microfiltration in Food and Beverage Processing

The food and beverage sector is increasingly adopting microfiltration for “cold sterilization” and product clarification to enhance shelf life while retaining flavor, aroma, and nutritional integrity. Case studies, such as one featured in the Journal of Food Engineering on large-scale breweries, demonstrate that microfiltration effectively removes haze-forming particulates and microorganisms without altering sensory properties. This adoption underscores a broader industry shift toward non-thermal processing methods that align with the clean-label movement and consumer preference for minimally processed products.

Critical Role of Microfiltration in Biopharmaceutical Manufacturing

Biopharmaceutical applications represent one of the most vital areas of microfiltration adoption, where the technology supports sterile filtration, virus removal, and cell harvesting. A notable case study from a leading filtration company revealed how microfiltration membranes optimized fermentation broth clarification, reducing both costs and processing time compared to centrifugation. These membranes ensured high product purity and recovery rates, making them indispensable in maintaining compliance with stringent regulatory frameworks for drug safety and efficacy.

Opportunities for Market Expansion Across High-Value Applications

The evolving landscape of membrane microfiltration presents significant opportunities in high-value markets such as advanced pharmaceuticals, biotechnology, and industrial wastewater treatment. Increasing regulatory mandates, consumer demand for safe and natural products, and technological innovations in membrane design are accelerating adoption. Companies investing in ceramic and application-specific membrane systems stand to benefit the most, particularly in industries requiring high reliability under harsh operational conditions.

Market Share Analysis of Membrane Microfiltration

Market Share by Material Composition

Polymeric membranes are projected to dominate the market with around 75% share by 2025, primarily due to their cost-effectiveness, broad chemical compatibility, and disposability—attributes highly valued in pharmaceutical and food safety applications. Ceramic membranes, accounting for approximately 20%, are the fastest-growing segment, driven by their superior chemical and thermal resistance, longer operational lifespans, and ability to withstand CIP/SIP cleaning regimes. Metallic membranes, while limited to niche applications with extreme temperature and mechanical demands, maintain strategic importance in sectors like metallurgy and hot gas filtration, holding a small yet essential 5% share.

Market Share by Module Design Preferences

Module design preferences strongly influence market dynamics, with hollow fiber modules holding the largest projected share at 30% due to their high packing density and dominance in membrane bioreactors for municipal wastewater treatment. Pleated filter cartridges, with a 25% share, represent a core segment for sterile filtration in pharma and food industries, driven by their disposability and reliability. Spiral-wound modules hold 15% and are preferred in large-scale water treatment pre-filtration. Niche but critical modules such as syringe filters (10%) dominate laboratory and R&D environments, while plate & frame (8%) and tubular designs (7%) thrive in high-solid and fouling-prone streams like dairy or pigments. Depth filters, though smaller at 5%, remain essential as protective pre-filters.

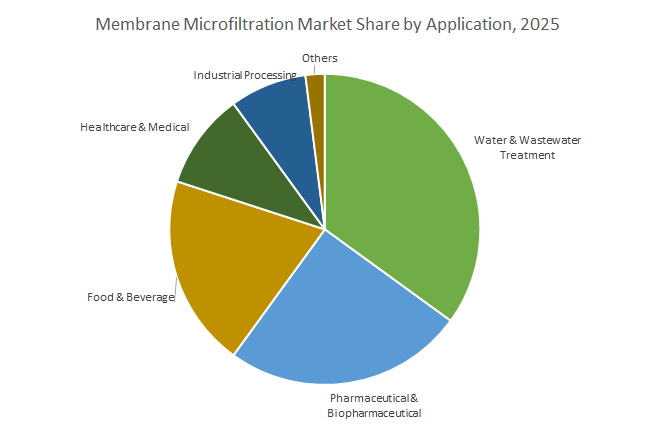

Market Share by Application Areas

Water and wastewater treatment is projected to remain the largest application segment with a 35% share by 2025, propelled by rising water reuse initiatives, population growth, and regulatory enforcement of water safety standards. Pharmaceuticals and biopharmaceuticals follow with a 25% share, representing the highest value segment where sterility, compliance, and patient safety outweigh cost considerations. Food and beverage applications account for 20%, benefiting from non-thermal sterilization and consumer-driven clean-label preferences. Healthcare and medical uses secure 10%, leveraging microfiltration for device sterilization, diagnostics, and dialysis. Industrial processing represents 8%, applying microfiltration in chemical, catalytic, and finishing operations. The remaining 2% includes specialized niches such as laboratories and electronics, where precision and reliability are critical.

China: Regulatory Compliance and Industrial Expansion Driving Microfiltration Adoption

China’s membrane microfiltration market is strongly influenced by stringent regulatory frameworks, technological advancements, and rapid industrial expansion. The Ministry of Ecology and Environment (MEE) mandates that all industrial entities discharging atmospheric and water pollutants obtain emission permits, pushing companies to adopt advanced microfiltration membranes to ensure compliance. In 2024, researchers developed hollow-fiber ultrafiltration (UF) membranes with enhanced antifouling properties, improving the long-term efficiency and reducing maintenance costs of membrane bioreactors (MBRs), where microfiltration plays a key role. China’s expanding municipal and industrial wastewater treatment sectors, including applications in radioactive and heavy metal wastewater treatment, are significant drivers for microfiltration membrane demand. Furthermore, government investments under the 14th Five-Year Plan (2021-2025) to expand natural gas production are increasing the adoption of microfiltration technologies in the oil and gas sector, positioning China as a critical market for advanced membrane solutions.

United States: Government Funding and Private Sector Innovation Driving Market Growth

The United States membrane microfiltration market is driven by substantial government funding, academic research, and corporate initiatives addressing emerging contaminants. The Infrastructure Investment and Jobs Act of 2021 allocates over $50 billion to the EPA to improve drinking water, wastewater, and stormwater infrastructure, with dedicated funding for contaminants such as PFAS, which require advanced microfiltration technologies. Research centers funded by the National Science Foundation (NSF) focus on developing next-generation membranes for water purification, chemical separations, and biopharmaceutical applications, providing continuous innovation in the microfiltration space. Private companies, including Veolia Water Technologies, have deployed microfiltration as a pretreatment step in treatment systems supplying water with regulated PFAS levels below threshold standards to over 140,000 Americans. This collaboration between government, academia, and industry underscores the U.S. as a leading market for microfiltration technology.

India: Government Initiatives and Infrastructure Investments Fueling Market Expansion

India’s microfiltration market is bolstered by government initiatives, strategic infrastructure investments, and industrial adoption. The Jal Jeevan Mission, alongside the Department of Science & Technology’s Water Technology Initiative, promotes R&D in filtration technologies to provide safe and affordable drinking water in rural regions. The Ghaziabad Nagar Nigam, issuing India’s first Certified Green Municipal Bond of ₹150 crore, has funded a state-of-the-art Tertiary Sewage Treatment Plant (TSTP) utilizing advanced microfiltration for industrial wastewater reuse, reducing reliance on freshwater sources. Additionally, VA TECH WABAG’s seven-year O&M contract for the 110 MLD SWRO Nemmeli Desalination Plant in Chennai, valued at approximately INR 415 crores, highlights the growing adoption of microfiltration in large-scale industrial and municipal water treatment projects. These initiatives demonstrate India’s strategic commitment to expanding microfiltration applications across multiple sectors.

Germany: Industrial Applications and Ceramic Membrane Innovations Leading Adoption

Germany is a global leader in membrane microfiltration, particularly in industrial wastewater treatment and ceramic membrane innovations. PWT Wassertechnik specializes in a range of microfiltration processes for industrial water reuse, ensuring compliance with European environmental regulations. German companies like CERAFILTEC are pioneering ceramic membrane bioreactors (MBRs) through strategic partnerships, representing a transformative approach to long-lasting and robust microfiltration systems. MANN+HUMMEL, a multinational German firm, focuses on developing innovative membrane and digital solutions for industrial water treatment and green energy applications, reinforcing Germany’s position as a technology hub for microfiltration solutions across industrial and municipal sectors.

Japan: Academic Research and Global Technology Leadership Enhancing Market Position

Japan’s membrane microfiltration market is driven by cutting-edge academic research and corporate technology leadership. Kobe University’s Membrane Engineering Group, in a 2024 study, highlighted the development of novel functional membranes, including biomimetic and highly porous microfiltration membranes for water and atmospheric applications. Toray Industries, a global leader, continues to develop high-performance RO membranes for large-scale desalination plants, such as projects in Saudi Arabia, where microfiltration is often used as a critical pretreatment step. Japan’s strong focus on research and export of advanced membrane technologies positions it as a key contributor to global microfiltration adoption.

Australia: Water Recycling Initiatives and Research Driving Sustainable Adoption

Australia faces significant water scarcity, making it a leading market for membrane microfiltration in water recycling and reuse initiatives. The Sydney Water Wollongong Water Resource Recovery Facility utilizes a combination of microfiltration and reverse osmosis to treat wastewater for non-potable applications, including sports field irrigation. Academic research at the Institute for Sustainable Industries and Liveable Cities (ISILC), Victoria University, focuses on increasing water recovery from desalination processes and mitigating membrane fouling and scaling, two critical challenges in sustainable water treatment. These initiatives highlight Australia’s strategic adoption of microfiltration technologies to improve water resilience and efficiency.

Competitive Landscape: Leading Companies in the Membrane Microfiltration Market

The competitive landscape of the global membrane microfiltration market is defined by technological innovation, expansion into high-demand industries, and sustainability-driven strategies. Companies are investing in new membrane materials, digital optimization tools, and large-scale infrastructure projects to capture market share.

Pall Corporation: Strength in Biopharmaceutical Microfiltration

Pall Corporation, a Danaher company, is a global leader in filtration and purification technologies, with a strong foothold in life sciences and industrial applications. Its Allegro™ STR single-use bioreactors are widely adopted in gene therapy and vaccine manufacturing, while its contract with Exothera in May 2023 underscores its role in biopharma expansion. With ongoing capacity expansions in Germany, Pall is enhancing its support for the food and beverage filtration membrane segment.

SUEZ Water Technologies & Solutions: Expanding Global Water Infrastructure

Now part of Veolia, SUEZ delivers integrated water treatment systems using microfiltration and ultrafiltration membranes for both industrial and municipal clients. Its landmark desalination project in China (July 2025) and modernization project in Angola highlight its expertise in large-scale water infrastructure. Leveraging Veolia’s global network, SUEZ is positioned as a frontrunner in sustainable industrial water purification.

Merck KGaA (MilliporeSigma): Driving Pharmaceutical Microfiltration Innovation

MilliporeSigma, the life sciences arm of Merck KGaA, dominates the pharmaceutical microfiltration market with solutions for drug manufacturing, sterile filtration, and biopharmaceuticals. Its five-year agreement with Simtra (June 2025) strengthens its position in ADC and complex therapy manufacturing. The acquisition of Exelead Inc. has expanded its expertise in mRNA therapeutics, while its focus on green manufacturing aligns with rising ESG mandates in the pharma industry.

Koch Membrane Systems (KMS): Engineering Tailored Microfiltration Solutions

With more than five decades of experience, Koch Membrane Systems is recognized for custom-engineered filtration systems. Its TARGA® II Hollow Fiber ultrafiltration system reduces capital costs through high-density packing and efficiency. KMS serves diverse markets, including industrial wastewater treatment, dairies, and breweries, with a strong emphasis on long-lasting membranes that minimize fouling and reduce operational costs.

3M: Diversified Filtration Solutions with Biopharma Investments

3M’s Separation and Purification Sciences Division provides advanced microfiltration membranes across pharmaceuticals, food & beverage, and industrial applications. In May 2023, the company announced a $146 million investment to expand its biopharma filtration manufacturing capacity, underscoring its commitment to healthcare and life sciences. Additionally, 3M’s healthcare spin-off strategy positions it to sharpen focus on biopharma and filtration technologies as a standalone entity.

Membrane Microfiltration Market Report Scope

Membrane Microfiltration Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.56 Billion

|

|

Market Size (2034)

|

$3.4 Billion

|

|

Market Growth Rate

|

9.2%

|

|

Segments

|

By Material (Polymeric Membranes, Ceramic Membranes, Metallic Membranes), By Module Design (Hollow Fiber, Spiral Wound, Tubular & Multi-tubular, Plate & Frame, Pleated Filter Cartridges, Syringe Filters, Depth Filters), By Application (Water & Wastewater Treatment, Food & Beverage, Pharmaceutical & Biopharmaceutical, Industrial Processing, Healthcare & Medical, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, DuPont de Nemours, Inc., SUEZ, Toray Industries, Inc., Pentair plc, Xylem Inc., Asahi Kasei Corporation, Koch Industries, Kubota Corporation, The Dow Chemical Company, MANN+HUMMEL, Evoqua Water Technologies, LG Chem, W. L. Gore & Associates, Inc., Merck KGaA

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Membrane Microfiltration Market Segmentation

By Material

- Polymeric Membranes

- Ceramic Membranes

- Metallic Membranes

By Module Design

- Cross-flow Modules

- Hollow Fiber

- Spiral Wound

- Tubular & Multi-tubular

- Plate & Frame

- Direct Flow Modules

- Pleated Filter Cartridges

- Syringe Filters

- Depth Filters

By Application

- Water & Wastewater Treatment

- Food & Beverage

- Pharmaceutical & Biopharmaceutical

- Industrial Processing

- Healthcare & Medical

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Membrane Microfiltration Industry include-

- Veolia

- DuPont de Nemours, Inc.

- SUEZ

- Toray Industries, Inc.

- Pentair plc

- Xylem Inc.

- Asahi Kasei Corporation

- Koch Industries

- Kubota Corporation

- The Dow Chemical Company

- MANN+HUMMEL

- Evoqua Water Technologies

- LG Chem

- W. L. Gore & Associates, Inc.

- Merck KGaA

*- List not Exhaustive

Research Coverage

This report investigates the membrane microfiltration market, delivering analysis reviews on how water scarcity, biopharma scale-up, and food safety mandates are accelerating adoption across utilities and process industries. It highlights breakthroughs in ceramic and advanced polymeric media, long-life modules that withstand aggressive CIP/SIP, and pre-treatment designs that stabilize downstream RO and desalination performance. The study further highlights regulatory pressure on pathogen and PFAS control, rising sterile operations in pharmaceuticals and ADC manufacturing, and non-thermal “cold sterilization” for beverages. With granular views on module preferences (hollow fiber, pleated cartridges, spiral-wound, tubular, plate & frame), operating economics, and hygiene validation, this report is an essential resource for engineers, product managers, and investors planning compliant, high-uptime filtration assets. Developed by USDAnalytics, it translates membrane performance and lifecycle metrics into procurement-ready insights for decision-makers. Scope Includes-

- Segmentation: By Material (Polymeric, Ceramic, Metallic), By Module Design (Cross-flow: Hollow Fiber, Spiral Wound, Tubular & Multi-tubular, Plate & Frame; Direct Flow: Pleated Filter Cartridges, Syringe Filters, Depth Filters), By Application (Water & Wastewater Treatment; Food & Beverage; Pharmaceutical & Biopharmaceutical; Industrial Processing; Healthcare & Medical; Others)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic data 2021–2024; forecasts 2025–2034.

- Companies: Profiles of 15+ companies

Methodology

Our approach combines primary interviews with utilities, OEMs, EPCs, and QA/Regulatory leads, and secondary research across standards, filings, and peer-reviewed studies. Market sizing integrates a top-down view (end-market flowsheets, plant counts, retrofit cycles) with bottom-up BOM models for dominant modules and media, normalized by flux (LMH), fouling factors, and cleaning intervals. Forecasts apply learning-curve effects for ceramic and high-area polymeric modules, sensitivity to energy/chemistry costs, and scenario testing for regulatory thresholds (pathogen log-removal, turbidity, PFAS). Competitive benchmarking tracks ASME BPE/GMP considerations, integrity-test regimes, and total cost per 1,000 m³ or per batch in pharma/food settings. All outputs undergo cross-validation against historical commissioning and announced capacity expansions.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Membrane Microfiltration Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Insights for Stakeholders

1.3. Global Market Snapshot

2. Membrane Microfiltration Market Outlook (2025–2034)

2.1. Introduction: Growth Drivers and Industry Transformation

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $1.56 Billion

2.2.2. Forecasted Market Size (2034): $3.4 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 9.2%

2.3. Key Market Trends and Opportunities

2.3.1. Surging Demand for High-Purity Water Solutions

2.3.2. Technological Shift Toward Ceramic Membranes

2.3.3. Expansion in Food and Beverage Processing

2.3.4. Critical Role in Biopharmaceutical Manufacturing

3. Recent Developments and Strategic Shifts

3.1. Market Trend: Public-Private Partnerships and Industrial Water

3.1.1. SUEZ and Senegalese Government Partnership

3.1.2. SUEZ Commissions China’s Largest Desalination Plant

3.2. Market Trend: Biopharma and Life Sciences Collaboration

3.2.1. MilliporeSigma Partners with Simtra on Drug Manufacturing

3.2.2. 3M’s Investment in Biopharma Filtration Capacity

3.3. Market Opportunity: Diversification and Sustainability

3.3.1. Microfiltration in Radioactive and Heavy Metal Wastewater Treatment

3.3.2. Sterlitech Corporation Launches Food and Beverage Portal

3.3.3. Asahi Kasei’s Inclusion in Sustainability Indices

4. Competitive Landscape: Leading Companies

4.1. Market Overview: From Filtration Specialists to System Integrators

4.2. Key Competitive Factors

4.2.1. Technological Innovation and Material Science Expertise

4.2.2. Global Footprint and Application-Specific Solutions

4.2.3. Strategic Partnerships and Acquisitions

4.3. Profiles of Top Players

4.3.1. Pall Corporation (Danaher)

4.3.2. SUEZ Water Technologies & Solutions (Veolia)

4.3.3. Merck KGaA (MilliporeSigma)

4.3.4. Koch Membrane Systems (KMS)

4.3.5. 3M

5. Membrane Microfiltration Market – Segmentation Insights

5.1. By Material

5.1.1. Polymeric Membranes

5.1.2. Ceramic Membranes

5.1.3. Metallic Membranes

5.2. By Module Design

5.2.1. Hollow Fiber

5.2.2. Pleated Filter Cartridges

5.2.3. Spiral-Wound Modules

5.2.4. Syringe Filters

5.2.5. Others (Plate & Frame, Tubular, Depth Filters)

5.3. By Application

5.3.1. Water & Wastewater Treatment

5.3.2. Pharmaceutical & Biopharmaceutical

5.3.3. Food & Beverage

5.3.4. Healthcare & Medical

5.3.5. Industrial Processing

6. Country Analysis and Outlook: Membrane Microfiltration Market

6.1. China: Regulatory Compliance and Industrial Expansion

6.2. United States: Government Funding and Private Sector Innovation

6.3. India: Government Initiatives and Infrastructure Investments

6.4. Germany: Industrial Applications and Ceramic Membrane Innovations

6.5. Japan: Academic Research and Global Technology Leadership

6.6. Australia: Water Recycling Initiatives and Research

6.7. Other Key Countries

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Membrane Microfiltration Market Size Outlook by Region (2025-2034)

7.1. North America Membrane Microfiltration Market Size Outlook to 2034

7.1.1. By Material

7.1.2. By Module Design

7.1.3. By Application

7.2. Europe Membrane Microfiltration Market Size Outlook to 2034

7.2.1. By Material

7.2.2. By Module Design

7.2.3. By Application

7.3. Asia Pacific Membrane Microfiltration Market Size Outlook to 2034

7.3.1. By Material

7.3.2. By Module Design

7.3.3. By Application

7.4. South America Membrane Microfiltration Market Size Outlook to 2034

7.4.1. By Material

7.4.2. By Module Design

7.4.3. By Application

7.5. Middle East and Africa Membrane Microfiltration Market Size Outlook to 2034

7.5.1. By Material

7.5.2. By Module Design

7.5.3. By Application

8. Company Profiles: Additional Leading Players

8.1. Veolia

8.2. DuPont de Nemours, Inc.

8.3. SUEZ

8.4. Toray Industries, Inc.

8.5. Pentair plc

8.6. Xylem Inc.

8.7. Asahi Kasei Corporation

8.8. Koch Industries

8.9. Kubota Corporation

8.10. The Dow Chemical Company

8.11. MANN+HUMMEL

8.12. Evoqua Water Technologies

8.13. LG Chem

8.14. W. L. Gore & Associates, Inc.

8.15. Merck KGaA

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures