Micro Packaging Market Overview: Size, CAGR, and Industry Insights

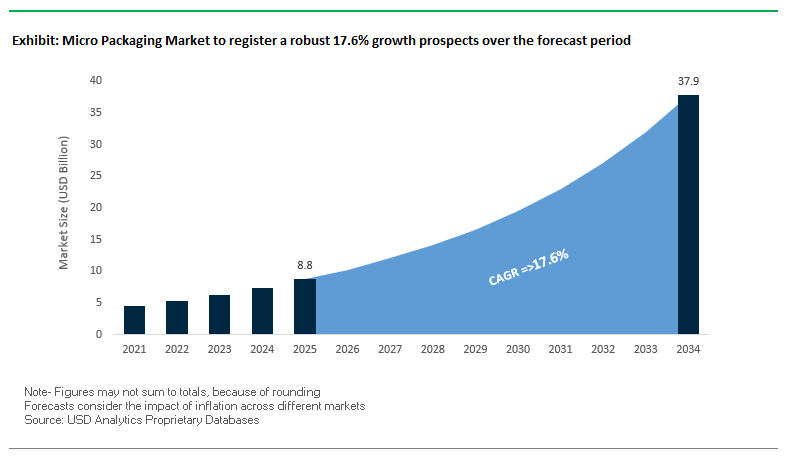

The global Micro Packaging Market is projected to grow from $8.8 billion in 2025 to $37.9 billion by 2034, representing a robust CAGR of 17.6%. This remarkable growth is driven by the increasing adoption of micro packaging solutions in pharmaceuticals, healthcare, electronics, and food sectors, fueled by the need for precision, safety, and sustainable packaging solutions. Micro packaging enables efficient drug delivery systems, component protection, and shelf life extension, positioning it as a critical enabler for modern industries.

Key Insights for Industry Professionals:

- Pharmaceutical and medical dominance: Strong demand for vials, ampoules, pre-filled syringes, and tamper-evident containers drives the market.

- Smart and active packaging integration: Features like RFID tags, QR codes, and sensors enable real-time tracking, anti-counterfeiting, and patient adherence monitoring.

- Electronics and miniaturization: Precision micro packaging protects sensitive electronic components from dust, moisture, and static electricity.

- Food safety and shelf life extension: Incorporation of oxygen-scavenging films and antimicrobial coatings improves freshness and reduces food waste.

- Sustainability and material efficiency: Lightweight and recyclable materials reduce environmental impact while enhancing packaging efficiency.

Micro Packaging Market Analysis: Key Recent Developments

The micro packaging industry has experienced significant strategic moves and technological innovations in recent months. In August 2025, Gerresheimer AG announced its intention to separate its molded glass business, focusing on core healthcare packaging solutions. In the same month, Amcor plc completed its merger with Berry Global, creating a global leader in consumer and healthcare packaging solutions. Additionally, SCHOTT Pharma partnered with SHL Medical to develop a new cartridge and autoinjector system, enabling patients to self-administer medications at home, a major advancement in patient-centric healthcare.

By July 2025, Gerresheimer AG ended discussions with private equity investors regarding a takeover, emphasizing independent growth strategies. Simultaneously, WestRock and Smurfit Kappa debuted as Smurfit WestRock on the New York and London Stock Exchanges, strengthening their global presence in paper-based packaging solutions. AptarGroup launched an all-plastic trigger spray pump and its first nasal pump made with 52% bio-based material, demonstrating a commitment to sustainable, non-aerosol dispensing solutions.

Earlier in the year, in June 2025, Gerresheimer AG introduced a digital database solution to accelerate drug launch timelines, reinforcing the integration of digital health solutions in micro packaging. Milestones in April 2025 included US antitrust clearance for the Amcor-Berry merger, while November 2024 saw Sonoco Products Company acquire Eviosys, enhancing its position in global metal food can and aerosol packaging.

Strategic Trends and Emerging Opportunities in the Micro Packaging Market

Pharmaceutical Industry Adoption of Unit-Dose Blisters for Solid Oral Chemotherapeutics

The micro packaging market is undergoing a structural transformation as the pharmaceutical sector embraces unit-dose blister packaging for oral chemotherapeutics and high-potency active pharmaceutical ingredients (HPAPIs). This shift is driven by the dual imperatives of patient safety and healthcare worker protection, given the risks associated with handling hazardous drugs.

Unit-dose formats prevent powder exposure during tablet handling, significantly reducing cross-contamination risks. According to Stokes Pharmacy, blistered chemotherapy tablets reduce reliance on PPE and minimize occupational hazards for healthcare providers. The individual sealing of doses also supports regulatory compliance with GMP standards, aligning with FDA and EMA guidance that emphasizes contamination control and adherence.

Beyond safety, unit-dose packaging enhances medication adherence. The ability for patients to track consumption visually makes blisters particularly effective in oncology regimens, where missed doses compromise treatment outcomes. This trend reflects a broader regulatory and clinical consensus: unit-dose formats are no longer optional but essential in high-risk therapeutic categories.

Integration of Smart and Connected Features in Micro-Primary Packaging

The convergence of digital health and pharmaceutical packaging is catalyzing the development of smart micro packaging solutions that embed connectivity and traceability into primary formats such as blisters and mini-bottles.

Smart packaging enables medication adherence tools, where NFC tags and QR codes trigger reminders, patient education videos, or refill notifications. For instance, CCL Healthcare demonstrates how smartphone-enabled blister packs can integrate seamlessly with patient management apps. These features not only improve adherence in chronic disease therapies but also reduce hospital readmissions.

Additionally, embedded RFID and NFC technologies meet requirements under the U.S. Drug Supply Chain Security Act (DSCSA), ensuring end-to-end traceability. In clinical research, these systems are invaluable—automatically recording consumption times to generate precise compliance data. This positions smart micro packaging as a critical enabler for supply chain integrity, patient safety, and real-world evidence generation.

Development of Sustainable and Bio-Based Materials for Single-Dose Formats

As environmental scrutiny intensifies, the market is seeing a surge in innovation around sustainable and bio-based micro packaging. Single-use blister packs, though effective, are criticized for their environmental footprint, creating opportunities for fiber-based, compostable, and bioplastic materials.

In February 2024, Sanofi Consumer Healthcare joined the Blister Pack Collective to co-develop recyclable fiber-based blisters. Similarly, Keystone Folding Box Co. launched paper-based blister solutions in June 2024, providing eco-friendly alternatives for OTC and nutraceutical products. Academic studies on PLA and PEF bioplastics highlight their potential to reduce carbon intensity while maintaining barrier performance for sensitive drugs.

With patients and healthcare providers increasingly factoring sustainability into purchasing decisions, pharma companies face mounting pressure to adopt greener solutions. This creates a high-value growth avenue for packaging innovators who can combine regulatory compliance, barrier integrity, and environmental responsibility in next-generation unit-dose designs.

Advanced Aseptic Micro Packaging for Cell and Gene Therapies

The explosive rise of advanced therapeutic medicinal products (ATMPs) such as CAR-T and gene therapies is fueling demand for aseptic micro packaging that ensures sterility and stability in cryogenic environments. Unlike conventional drugs, these therapies are patient-specific, high-value, and highly sensitive to contamination and temperature excursions.

According to Cytiva, many ATMPs must be stored and transported at -196°C in liquid nitrogen, with damage occurring if temperatures exceed -120°C. This necessitates micro packaging formats engineered for cryogenic durability. Materials must resist fracture, preserve sterility, and withstand logistical stress during cold chain handling.

Moreover, the chain of identity requirement in personalized medicine elevates the role of packaging as a regulatory safeguard. Labels and tracking systems must remain legible and secure under extreme cold, ensuring therapies reach the correct patient without error. Publications from Kymanox emphasize that packaging innovation in this space is not just about containment—it is integral to regulatory compliance, patient safety, and therapeutic success.

Competitive Landscape: Leading Players in the Global Micro Packaging Industry

The micro packaging market is dominated by companies that combine advanced material science, sustainable innovation, and precision manufacturing to deliver high-performance packaging solutions. These leaders differentiate through their healthcare focus, technological integration, and global footprint, catering to pharmaceutical, medical, and consumer goods sectors.

Amcor plc: Creating a Global Leader Through Strategic Merger

Amcor is a global leader in flexible and rigid micro packaging solutions, serving the pharmaceutical, medical, and consumer goods industries. In August 2025, Amcor completed its merger with Berry Global, establishing a global packaging powerhouse. The company’s multi-compartment trays in partnership with Cofigeo enhance convenience and sustainability. Amcor’s strengths lie in its innovative, lightweight solutions and comprehensive service integration, including design, manufacturing, and logistics support.

Gerresheimer AG: Expanding Core Healthcare Packaging Focus

Gerresheimer is a leading provider of primary healthcare and cosmetic packaging, including vials, ampoules, and syringes. In August 2025, it announced plans to separate its molded glass business to concentrate on core packaging. Gerresheimer emphasizes sustainability, targeting 100% renewable electricity and a 50% CO2 reduction by 2030, while offering digital health solutions to accelerate new drug launches.

AptarGroup, Inc.: Innovating Sustainable Dispensing Solutions

Aptar specializes in consumer dispensing and healthcare delivery systems, offering micro packaging for nasal sprays, autoinjectors, and pharmaceutical containers. In July 2025, the company launched a nasal pump with 52% bio-based material and an all-plastic trigger spray pump, reflecting its commitment to sustainable, eco-friendly innovation. Aptar’s products enhance patient adherence, safety, and functionality across healthcare, personal care, and food applications.

SCHOTT AG: Advancing Specialty Glass for Healthcare

SCHOTT Pharma provides vials, ampoules, cartridges, and syringes for the pharmaceutical industry. In August 2025, its collaboration with SHL Medical resulted in a 5 ml sterile cartridge compatible with autoinjector systems, empowering home-based patient medication administration. SCHOTT leverages its specialty glass expertise to produce durable, safe, and reliable micro packaging solutions for global healthcare clients.

WestRock Company (Smurfit WestRock): Creating a Global Paper Packaging Leader

WestRock merged with Smurfit Kappa in July 2025, forming Smurfit WestRock, a global leader in paper-based packaging. Its micro packaging offerings include folding cartons and corrugated containers for pharmaceuticals and medical devices. The company emphasizes sustainable paper-based solutions, utilizing recycled and renewable materials to reduce environmental impact while providing customized packaging for diverse industries.

Micro Packaging Market Share Insights

Blister and Strip Packs Hold the Largest Market Share by Packaging Type in the Micro Packaging Industry

Blister and strip packs command 30% of the micro packaging market, establishing themselves as the pharmaceutical unit-dose standard. Their dominance is linked to the global demand for secure, contamination-free drug delivery systems that guarantee dosage accuracy and compliance. Each cavity provides an independent sterile environment, protecting sensitive formulations from moisture, oxygen, and physical damage throughout their shelf-life. Regulatory mandates for child-resistant and tamper-evident features further cement blister packs as the primary solution for solid oral dosage forms. Pouches and sachets follow closely, gaining traction in nutraceuticals, cosmetics, and food single-serve formats, but blister packs retain leadership due to the sheer scale of tablet and capsule production worldwide, their compatibility with high-speed filling lines, and their role in ensuring patient adherence in both developed and emerging healthcare systems.

Pharmaceuticals and Medical Devices Drive the Largest Market Share by Application in the Micro Packaging Industry

Pharmaceuticals and medical devices represent 55% of total demand for micro packaging, making them the industry’s most critical and value-intensive end-use. This dominance is a direct consequence of the stringent sterility and regulatory requirements governing unit-dose drugs, implantable devices, diagnostic kits, and surgical tools. Micro packaging solutions—whether blister packs, vials, or micro-trays—ensure product integrity, tamper evidence, and patient safety across global supply chains. The ongoing expansion of biologics, personalized medicine, and injectable therapies intensifies the reliance on high-precision formats that maintain sterility and dosage accuracy. While electronics and semiconductors represent a fast-growing adjacent segment, the pharmaceutical sector’s non-discretionary, recurring demand and compliance-driven packaging needs ensure it remains the undisputed driver of global micro packaging consumption.

United States: EPR Regulations and Smart Packaging Innovations Shape the Micro Packaging Market

The United States micro packaging market is undergoing a significant transformation driven by regulatory and technological shifts. The Food and Drug Administration (FDA), the Environmental Protection Agency (EPA), and state-level Extended Producer Responsibility (EPR) laws—particularly in California—are pushing manufacturers to create recyclable, mono-material, and sustainable micro packaging solutions. These regulatory forces are reshaping the industry by prioritizing environmentally friendly designs that fit into existing recycling systems while meeting strict healthcare and food safety standards.

Technological innovation is accelerating, with a strong emphasis on smart and active packaging solutions. Companies are integrating RFID tags, QR codes, and embedded sensors to track supply chains, prevent counterfeiting, and engage consumers in real-time. ProAmpac’s 2024 launch of a fully recyclable PE film, R-2000, for microwave and frozen food applications, underscores the shift toward sustainable, high-performance packaging. Strategic investments are reinforcing this momentum—Berry Global introduced a bio-based micro tray solution in 2025, while TransPak opened a 300,000-square-foot Texas facility specializing in semiconductor equipment packaging. With strong demand from pharmaceuticals, medical devices, and electronics, the U.S. micro packaging industry remains a global leader in both scale and innovation.

Germany: EU Packaging Regulations and R&D Leadership Advance High-Performance Micro Packaging

Germany’s micro packaging market is heavily influenced by the European Union’s Packaging and Packaging Waste Regulation (PPWR), which came into force in January 2025. These rules emphasize recyclability and circular economy practices, compelling German manufacturers to innovate in paper-based and recyclable plastic micro packaging. This regulatory environment is driving a rapid shift away from traditional multi-material laminates toward mono-material solutions that meet both performance and sustainability targets.

Germany also leads in R&D-driven technological innovation, particularly in advanced film-coating and printing technologies. Pharmaceutical applications are a core strength, with ultra-thin barrier coatings being developed for micro vials containing sensitive biologics and injectable drugs. The NanoPack Consortium’s EU-backed initiative to create antimicrobial surfaces with improved shelf life directly impacts Germany’s micro packaging leadership. Corporate investments are reinforcing this dominance: Air Liquide’s €250 million commitment to the semiconductor industry in Germany will expand the supply of high-purity materials, which aligns closely with the needs of micro packaging for electronics and medical applications.

China: Dual-Carbon Policies and Automation Propel Domestic Micro Packaging Expansion

China’s micro packaging market is thriving under strong government backing for high-end manufacturing. National policies that align with dual-carbon sustainability goals are fast-tracking standards and simplifying approval processes for innovative products, encouraging companies to scale advanced production. Regulatory reforms by the National Medical Products Administration (NMPA) are further streamlining the approval of medical and pharmaceutical packaging, strengthening the country’s push toward global competitiveness.

Chinese manufacturers are rapidly adopting automation and artificial intelligence to enhance quality and efficiency, with domestic companies scaling capacity to meet booming demand from electronics and pharmaceuticals. Meanwhile, global FMCG players are expanding local facilities to reduce supply chain risks, boosting the role of local micro packaging suppliers. Applications in snack food packaging and consumer electronics are surging, where high-quality, tamper-proof, and sustainable micro packaging is becoming essential. Together, these advancements position China as a powerhouse in the global micro packaging market.

India: Government Policies and Circular Economy Models Drive Micro Packaging Market Growth

India is rapidly emerging as a growth hub for micro packaging, backed by strong government policies. The Make in India initiative and Production Linked Incentive (PLI) scheme are fostering domestic manufacturing, while the 2023 National Medical Devices Policy is creating favorable conditions for healthcare-related packaging. At the same time, the Central Pollution Control Board (CPCB) has mandated Extended Producer Responsibility (EPR) registration for all medical device manufacturers and importers using plastic packaging, adding regulatory pressure to adopt sustainable formats.

Innovation in technology is also advancing, particularly in flexible and recyclable packaging solutions. In June 2024, Uflex Ltd. introduced barrier-coated paper-based micro packaging formats for single-serve sachets, significantly reducing plastic use in food and beverage packaging. Investments are flowing into new facilities and R&D from major companies such as Cosmo Films Ltd, Jindal Poly Films Ltd, and Uflex Ltd, all of which are accelerating innovation across consumer electronics, e-commerce, and pharmaceuticals. With sustainability at its core, India’s micro packaging market is balancing regulatory compliance, rapid consumption growth, and advanced material innovation.

Japan: Precision Engineering and High-Functionality Micro Packaging Solutions Lead the Market

Japan’s micro packaging market is defined by its precision-driven approach and focus on advanced technologies. Manufacturers such as Toppan and Dai Nippon Printing are internationally recognized for innovations in paper-based and flexible films. In 2021, Toppan Printing’s launch of a virusweeper film-type packaging with antibacterial and antifungal functionality showcased Japan’s leadership in creating micro packaging solutions that directly address healthcare and hygiene concerns.

Regulations from the Pharmaceuticals and Medical Devices Agency (PMDA) enforce strict quality and safety standards, with amendments to the Pharmaceuticals and Medical Devices Act ensuring stable drug supply. These policies directly influence pharmaceutical packaging, one of Japan’s most critical application areas. Meanwhile, demand for specialty and high-performance products is rising in cosmetics, automotive, and display technologies. Micro packaging solutions with superior optical clarity, durability, and barrier properties are becoming standard in these industries. Japan’s mix of regulatory rigor, innovation in functionality, and a focus on premium applications continues to position it as a global leader in the micro packaging market.

Micro Packaging Market Report Scope

Micro Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.8 Billion

|

|

Market Size (2034)

|

$37.9 Billion

|

|

Market Growth Rate

|

17.6%

|

|

Segments

|

By Material (Paper & Paperboard, Plastic, Glass, Metal, Others), By Packaging Type (Blister and Strip Packs, Vials & Ampoules, Pouches & Sachets, Trays, Jars & Bottles, Others), By Application (Pharmaceuticals & Medical Devices, Electronics & Semiconductors, Food & Beverage, Personal Care, Others), By End-User (Pharmaceutical & Biotechnology Companies, Consumer Electronics Manufacturers, Food & Beverage Companies, Personal Care & Cosmetics Companies)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor Plc, Berry Global Inc., Uflex Ltd., Jindal Poly Films Ltd., CCL Industries Inc., Sealed Air Corporation, Mondi Group, Stora Enso Oyj, Avery Dennison Corporation, WestRock Company, Sonoco Products Company, Tetra Pak Group, Daikin Industries, Ltd., Crown Holdings, Inc., International Paper Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Micro Packaging Market Segmentation

By Material

- Paper & Paperboard

- Plastic

- Glass

- Metal

- Others

By Packaging Type

- Blister and Strip Packs

- Vials & Ampoules

- Pouches & Sachets

- Trays

- Jars & Bottles

- Others

By Application

- Pharmaceuticals & Medical Devices

- Electronics & Semiconductors

- Food & Beverage

- Personal Care

- Others

By End-User

- Pharmaceutical & Biotechnology Companies

- Consumer Electronics Manufacturers

- Food & Beverage Companies

- Personal Care & Cosmetics Companies

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Micro Packaging Market

- Amcor Plc

- Berry Global Inc.

- Uflex Ltd.

- Jindal Poly Films Ltd.

- CCL Industries Inc.

- Sealed Air Corporation

- Mondi Group

- Stora Enso Oyj

- Avery Dennison Corporation

- WestRock Company

- Sonoco Products Company

- Tetra Pak Group

- Daikin Industries, Ltd.

- Crown Holdings, Inc.

- International Paper Company

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous, multi-step research methodology to deliver actionable insights on the global Micro Packaging Market. Our analysis combines primary research through interviews with industry experts, manufacturers, healthcare and electronics professionals, and supply chain stakeholders with secondary research sourced from corporate filings, patent data, regulatory publications, and scientific literature. We evaluate market drivers such as precision packaging for pharmaceuticals, smart and connected micro packaging, single-dose formats, and sustainable materials, along with technological innovations like digital health integration and aseptic packaging for ATMPs. Advanced forecasting models are applied to analyze market growth, regional trends, and regulatory impacts across the U.S., Europe, China, India, and Japan. USDAnalytics also examines corporate strategies, including mergers, capacity expansions, and R&D investments, while assessing materials, barrier performance, sustainability, and digital traceability features. This methodology ensures that industry professionals receive a comprehensive understanding of micro packaging dynamics, competitive landscape, emerging opportunities, and strategic growth pathways in high-value end-use sectors such as pharmaceuticals, medical devices, electronics, and food.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.