Market Overview: Regulatory Substitution and EV Architecture Shifts Propel Hybrid MS Polymer Adhesives and Sealants

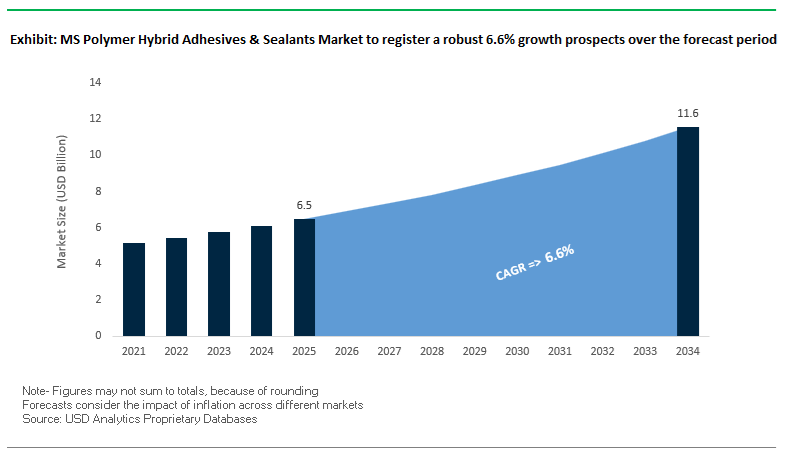

The Global MS Polymer Hybrid Adhesives and Sealants Market is projected to expand from USD 6.5 billion in 2025 to USD 11.6 billion by 2034, growing at a CAGR of 6.6%, as low-emission construction practices and next-generation mobility platforms reshape material selection across industries. Market growth is being driven by the rising preference for low-VOC, isocyanate-free bonding systems, particularly in green building projects and electric vehicle (EV) manufacturing, where adhesives must deliver durability, flexibility, and regulatory compliance simultaneously.

Hybrid MS Polymer systems—engineered to combine the elastic recovery of silicones with the mechanical toughness of polyurethanes—are increasingly specified where traditional chemistries fall short. In construction, their zero-VOC and odorless profiles are gaining importance as developers pursue LEED-aligned and EU Green Deal–compliant projects, especially in occupied buildings and enclosed environments. As a result, over 64% of construction manufacturers now favor hybrid MS Polymer sealants, reflecting a clear substitution trend away from solvent-containing and isocyanate-based products.

Transportation and industrial assembly are emerging as parallel growth engines. The shift toward multi-material EV architectures—incorporating aluminum, coated steels, plastics, and composites—is increasing reliance on hybrid adhesives that can bond dissimilar substrates without primers or complex surface treatments. Approximately 36% of newly developed hybrid MS Polymer adhesives demonstrate enhanced multi-substrate compatibility, simplifying assembly workflows and reducing process variability in automotive and industrial production. In battery electric vehicles, the role of these materials is expanding rapidly; BEVs now use up to 7 pounds of hybrid adhesives and sealants per vehicle, representing a 250% increase compared to HEVs, driven by requirements in battery housings, body bonding, and vibration isolation.

Movement accommodation and environmental durability continue to differentiate the segment. Modern hybrid MS Polymer sealants deliver ≥±25% joint movement capability, supporting façade systems, curtain walls, and structural glazing exposed to thermal expansion and dynamic loads. Their ability to maintain bonding integrity across −40°C to +90°C, combined with strong UV and weathering resistance, is reinforcing adoption in exterior construction and mobility applications where long service life is a procurement priority.

The MS Polymer Hybrid Adhesives and Sealants market is undergoing significant transformation, led by capacity expansions, product innovations, and sustainability-driven business models. The market’s strategic direction reflects a pronounced shift toward advanced polymer integration, regional production optimization, and next-generation silane chemistry to meet evolving global standards.

In March 2025, Wacker Chemie AG announced an ambitious investment plan targeting capacity expansion across its Silicones and Polymers divisions, anticipating a 10% sales increase in specialty silane-based products. This move enhances the global supply of key MS Polymer raw materials used in construction sealants and industrial hybrid formulations. Earlier, in January 2025, Wacker reported continued growth in hyperpure polysilicon production for semiconductors, underscoring its strategic integration in high-purity silane feedstocks, which are critical for high-performance MS Polymer hybrid formulations.

In July 2024, Mohm Chemical introduced the x’traseal MS-602, a next-generation MS Polymer sealant targeting the construction sector, emphasizing superior adhesion and mechanical durability. Around the same time, the automotive and EV sectors saw rising adhesive demand, with Kelley Blue Book’s January 2024 data showing 1.2 million EV sales in the U.S., accounting for 7.6% of total new vehicle sales—a major growth catalyst for MS Polymer-based structural bonding and battery sealing technologies.

In November 2023, Henkel AG & Co. KGaA launched a medical-grade, IBOA-free light-cure adhesive, setting a new industry benchmark for safe, high-performance adhesive formulations—a direction that mirrors MS Polymer advancements in health and safety compliance. Earlier, in May 2023, Bostik (Arkema Group) expanded its hybrid portfolio with Supergrip SG6518 and SG6520—woodworking adhesives based on hybrid polyurethane and silane-modified polymers. This launch reinforced Arkema’s strategy of advancing smart adhesives for construction and industrial applications.

Innovation also extended to regional specialization. In February 2023, 3M Company unveiled a medical-grade polymer adhesive capable of 28-day skin adherence, highlighting its cross-sector R&D strength in durable polymer bonding technologies. Meanwhile, H.B. Fuller, in January 2023, launched Swift Melt 1515-I, a bio-compatible hot-melt adhesive in India and Africa, reinforcing its focus on region-specific compliance and specialty market growth.

Market Trend 1: Regulatory-Driven Substitution of Polyurethane and Solvent-Based Systems in Automotive and Construction

A powerful regulatory shift is propelling the widespread adoption of MS Polymer Hybrid Adhesives across construction and automotive sectors, as governments impose stringent restrictions on hazardous chemicals—especially diisocyanates and volatile organic compounds (VOCs)—found in traditional polyurethane (PU) systems.

The European Union’s REACH Regulation on Diisocyanates, fully enforceable from August 24, 2023, mandates mandatory training and certification for all professional users handling products containing more than 0.1% monomeric diisocyanates by weight. The regulation has created immediate compliance challenges and increased operational costs for PU adhesive users, making isocyanate-free MS Polymer Hybrids a preferred alternative for both manufacturers and contractors seeking regulatory simplicity and safety assurance.

Health data from Europe’s occupational safety authorities reported over 5,000 annual cases of work-related asthma and dermal sensitization attributed to diisocyanate exposure. The public health concern has reinforced the transition toward low-VOC, non-toxic MS Polymer formulations, which provide the same mechanical strength and flexibility as PUs without releasing harmful substances during application or curing.

In addition, from February 2022, EU labeling laws required PU product packaging to include the warning: “Adequate training is required before industrial or professional use of the product.” The measure accelerated supply chain realignment, as distributors and professional users began substituting PU with MS Polymer Hybrid sealants—products that do not require special handling certifications.

The outcome is clear: construction and automotive OEMs are actively switching to MS Polymer Hybrids for body-in-white sealing, joint bonding, and façade systems. With global emphasis on green chemistry, the transition marks a fundamental redefinition of industry standards in adhesive sustainability, worker safety, and environmental compliance.

Market Trend 2: Formulation Advances Enabling High-Performance Prefabrication and Off-Site Construction

The rise of modular construction and Design for Manufacturing and Assembly (DfMA) methods is fueling demand for rapid-curing, high-adhesion MS Polymer Hybrid formulations that enable high-speed, high-precision assembly in factory settings.

Advanced MS Polymer hybrids offer tack-free times as short as 15–35 minutes and achieve cure depths exceeding 8 mm within seven days under standard conditions, making them ideal for fast-paced off-site construction workflows. These adhesives deliver consistent curing even in high-humidity environments and exhibit superior gap-filling capability for complex substrates, supporting seamless integration of materials like coated steel, composites, and plastics used in modular buildings.

Modern two-component hybrid silane polymer adhesives have been designed to bond low surface energy (LSE) plastics, including polypropylene (PP), polyethylene (PE), and polyether ether ketone (PEEK)—materials often found in high-performance composite systems. Their broad substrate compatibility eliminates the need for primers, reducing assembly time while ensuring long-term durability and elasticity under stress, vibration, or thermal cycling.

The industrial investment trend mirrors the technological shift. In December 2021, Sika AG announced the establishment of a technology center and advanced manufacturing facility in Pune, India, dedicated to producing high-performance adhesives and sealants for modular construction and automotive applications. Such investments underscore the global expansion of MS Polymer production to meet the surging demand for prefabrication adhesives, which deliver both speed and structural reliability in modern industrial and construction assembly.

Market Opportunity 1: Penetrating the Electric Vehicle (EV) Battery Pack Assembly and Sealing Market

The electric vehicle revolution presents one of the most lucrative opportunities for MS Polymer Hybrid adhesives, which are increasingly used in battery pack sealing, structural bonding, and thermal protection applications. As EV designs demand lightweighting, superior vibration damping, and flame retardancy, hybrid adhesives are emerging as integral materials for safe and efficient battery enclosure manufacturing.

New formulations of fire-retardant MS Polymer hybrid sealants are engineered to comply with stringent fire-safety certifications such as UL94 V-0, essential for EV battery enclosures under regulations like China’s GB 38031-2020 and Europe’s UNECE R100 Rev. 3. These hybrids provide robust ingress protection against moisture, dust, and heat, ensuring the longevity and reliability of lithium-ion battery systems across various climatic conditions.

From a performance perspective, MS Polymer adhesives play a key role in lightweighting EV assemblies by replacing mechanical fasteners and welding. Their high tensile strength and elastic modulus distribute mechanical stresses more efficiently, improving crash resistance while lowering overall vehicle mass. For example, bonding the battery lid to the enclosure housing with structural MS Polymers results in a stiffer, leak-proof design that also supports improved thermal management and energy efficiency.

As global EV production continues to scale, with forecasts exceeding 50 million units by 2035, the integration of MS Polymer Hybrid adhesives into battery module assembly, housing sealing, and component protection represents a rapidly growing, high-margin segment of the adhesives market.

Market Opportunity 2: Addressing the Global Infrastructure Rehabilitation and Water Management Demand

The worldwide focus on infrastructure modernization and climate resilience is generating massive demand for durable, weather-resistant hybrid sealants capable of withstanding extreme conditions in bridges, dams, water treatment facilities, and pipelines. MS Polymer Hybrid formulations—known for their chemical resistance, elasticity, and long-term adhesion stability—are ideally positioned to meet these needs.

According to the World Bank, achieving the UN Sustainable Development Goals (SDG 6) for clean water and sanitation by 2030 requires annual investments of USD 131–141 billion, leaving a global funding gap that will inevitably drive intensive rehabilitation activity in existing water infrastructure. These large-scale projects require high-performance polymer sealants for waterproofing, crack repair, and joint restoration under demanding hydrostatic pressure and chemical exposure conditions.

In the United States, government initiatives such as the FAST Act and sustained EPA/USDA infrastructure funding programs have prioritized the upgrade of water utilities, wastewater systems, and transportation networks. Significantly, operations and maintenance (O&M) spending for these systems is currently twice as high as new construction investment, underscoring the ongoing demand for fast-curing, flexible, and long-lasting sealants that extend infrastructure service life with minimal downtime.

MS Polymer Hybrid adhesives and sealants, with their UV, salt, and chemical resistance, provide unmatched performance for structural sealing in harsh outdoor environments. From bridge expansion joints to concrete crack sealing and water barrier systems, these materials are poised to become indispensable to the next generation of infrastructure repair and maintenance solutions worldwide.

MS Polymer Hybrid Adhesives & Sealants Market Share Insights, 2025-2034

Market Share by Product Type/Resin

The silane-terminated polyether (SPE) segment leads the global MS polymer hybrid adhesives and sealants market, holding a projected 47.2% market share in 2025, driven by its balanced mechanical properties, strong adhesion profile, and environmental compliance. SPE-based hybrids combine the flexibility of polyethers with the chemical stability of silane curing, making them the preferred formulation for construction sealants, industrial adhesives, and façade systems. Their excellent UV resistance, paintability, and compatibility with a wide range of substrates — including metals, plastics, glass, and concrete — have made them indispensable in building envelopes, roofing joints, and structural glazing applications. The increasing adoption of low-VOC, isocyanate-free sealant systems across Europe and North America has accelerated SPE demand, as manufacturers prioritize eco-friendly formulations with long-term elasticity and minimal shrinkage.

The silane-terminated polyurethane (SPUR) segment maintains a strong position, driven by its enhanced chemical and mechanical resistance, particularly suited for automotive, marine, and heavy industrial bonding applications. SPUR hybrids provide higher tensile strength and faster curing times than SPE systems, making them ideal for vibration-prone or high-load environments. Meanwhile, modified polyether polymers (MPP) and other hybrid formulations cater to specialized performance requirements, such as enhanced adhesion to challenging substrates or extreme temperature stability. Innovations in next-generation hybrid chemistries are focusing on improving curing kinetics, bio-based content, and crosslinking efficiency, supporting the market’s broader shift toward sustainable, multifunctional adhesive solutions.

Market Share by End-Use Industry

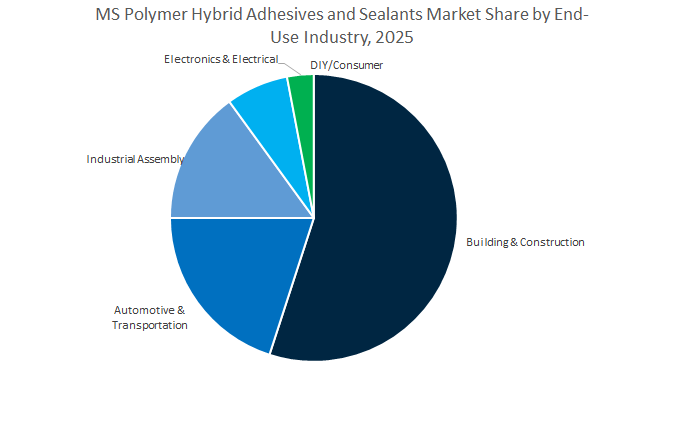

The building and construction sector dominates the global MS polymer hybrid adhesives and sealants market, projected to hold 59.1% share in 2025, reflecting the sector’s extensive reliance on high-performance hybrid sealants for façade, roofing, and concrete joint applications. These materials offer superior durability, weatherability, and adhesion on varied substrates, outperforming traditional silicones and polyurethanes while aligning with LEED and BREEAM green certification standards. The surge in infrastructure renovation, high-rise projects, and waterproofing activities in Asia-Pacific and Europe continues to fuel demand for SPE- and SPUR-based sealants. In addition, their isocyanate-free chemistry, low odor, and paintability make them highly desirable for interior finishing, tiling, and glazing in modern architectural projects.

The automotive and transportation industry is a major growth driver, leveraging hybrid adhesives for structural bonding, direct glazing, and body sealing applications in both conventional and electric vehicles. The trend toward lightweighting and noise reduction is promoting wider adoption of MS polymer hybrids over mechanical fastening and solvent-based adhesives. Similarly, the industrial assembly sector is witnessing increasing use of hybrid systems in appliance manufacturing, HVAC assembly, and equipment fabrication, where the combination of flexibility, chemical resistance, and fast curing delivers operational efficiency. The DIY/consumer segment is also expanding as hybrid formulations become available in retail cartridges and sealant packs, targeting general household, flooring, and decorative repairs.

The Global MS Polymer Hybrid Adhesives and Sealants market is moderately consolidated, led by Henkel AG & Co. KGaA, Sika AG, 3M Company, Wacker Chemie AG, H.B. Fuller Company, and Kaneka Corporation. These companies dominate through advanced polymer innovation, global manufacturing integration, and sustainability alignment, reinforcing their leadership in the next-generation adhesive chemistry landscape.

Henkel continues to set industry benchmarks with its LOCTITE hybrid adhesives and sealants, designed for high-performance construction, automotive, and electronics applications. The company’s R&D pipeline emphasizes low-VOC, high-strength, and sustainable polymer chemistry, aligning with global green building and safety standards. Its comprehensive bonding systems, integrating hybrid MS Polymer technologies, offer exceptional chemical resistance, flexibility, and adhesion across multi-material assemblies. Henkel’s November 2023 medical-grade adhesive launch highlights its leadership in safe, advanced polymer development applicable across industries.

Sika AG stands as a global powerhouse in hybrid adhesive and sealant technologies, leveraging its Sikaflex and Sikasil brands across construction and automotive sectors. With a strong presence in façade, roofing, and modular building applications, Sika’s hybrid products deliver exceptional weather resistance, displacement flexibility, and sustainability compliance. The company’s R&D centers develop energy-efficient and elastic bonding systems meeting European construction codes. Sika’s global manufacturing footprint and tailored regional solutions make it a preferred supplier for climate-adaptive and eco-certified infrastructure projects.

3M continues to lead through polymer science and cross-sector innovation, delivering hybrid adhesives and sealants optimized for automotive, aerospace, and industrial assembly. The company’s solutions emphasize fast curing, chemical resistance, and vibration damping, aligning with the growing demand for lightweight, electric vehicle bonding applications. Its February 2023 R&D innovation in skin-bonding polymer adhesives demonstrates 3M’s deep material expertise, which it effectively translates to industrial-grade MS Polymer hybrids. The company’s core strength lies in developing customized hybrid systems for extreme environments and multi-material bonding challenges.

Wacker Chemie AG serves as a backbone of the hybrid adhesives value chain, producing silane-modified polymers (SMPs) through its GENIOSIL line—vital for the MS Polymer ecosystem. The company’s capacity expansion plans (March 2025) reflect its commitment to ensuring reliable silane supply and advancing low-emission, weather-resistant adhesive systems. With strong expertise in silicone and polymer integration, Wacker enables downstream formulators to achieve tailored curing profiles, adhesion versatility, and environmental performance. Its vertical integration strategy ensures control over quality and innovation throughout the polymer supply chain.

H.B. Fuller leverages a broad adhesive portfolio encompassing hybrid, polyurethane, and reactive hot-melt technologies to serve the construction, automotive, and consumer goods industries. The company’s Swift Melt 1515-I launch in 2023 underscores its commitment to bio-compatible and regionally compliant products. Fuller continues to expand its hybrid MS Polymer presence in flooring, window assembly, and packaging applications, offering durable, easy-to-apply solutions. Through targeted acquisitions and partnerships, H.B. Fuller enhances local manufacturing capabilities and strengthens its foothold in Asia, the Middle East, and Africa.

Kaneka Corporation remains the originator and patent holder of MS Polymer technology (Silyl-Modified Polyether), supplying high-purity reactive resins globally. Its Kaneka MS Polymer™ series serves as the foundation for thousands of hybrid adhesive and sealant formulations. The company’s R&D advancements focus on enhanced UV stability, thermal resistance, and fast curing characteristics, supporting both construction and industrial markets. As a base polymer provider, Kaneka influences the performance standards of downstream adhesives worldwide, maintaining a critical role in the hybrid sealants ecosystem.

Country Analysis: Active Hubs in the Global MS Polymer Hybrid Adhesives and Sealants Market

China: Rapid Expansion in Silane-Modified Polymer Production and EV Integration

China has emerged as one of the fastest-growing centers for MS Polymer hybrid adhesive production, driven by its large-scale EV manufacturing base and expansive construction market. The acquisition of a 60% stake in Jining-based SICO Performance Material Co., Ltd by Wacker Chemie AG (2021) marked a strategic milestone, enabling localized production of critical silane precursors essential for MS polymer synthesis. The investment strengthens domestic supply chains and reduces import dependency for silane-terminated polymer materials, enhancing China’s position as a self-sufficient manufacturing hub.

The Ministry of Ecology and Environment’s stringent VOC emission regulations have further accelerated the transition away from solvent-based sealants, promoting low-VOC hybrid systems in high-density industrial clusters. Demand is particularly strong in electric vehicle (EV) assembly, where SMP adhesives are preferred for their ability to bond dissimilar substrates and provide thermal and vibration stability in battery enclosures. Meanwhile, major global players like Arkema (Bostik) continue expanding regional capacity to serve construction megaprojects and infrastructure upgrades. With expanding EV output, green policies, and robust building demand, China is solidifying its role as a strategic global production hub for SMP hybrid adhesives.

United States: Green Construction Standards and Automotive Lightweighting Drive Demand

The United States remains a critical innovation and consumption hub in the MS Polymer Hybrid Adhesives and Sealants Market, propelled by green building legislation and automotive modernization initiatives. The tightening of low-VOC regulations by the EPA and regional agencies like California’s CARB is reshaping adhesive formulations, pushing manufacturers toward 100% solids, solvent-free, isocyanate-free MS Polymer systems. The formulations are now integral to commercial and residential construction, particularly in LEED-certified and net-zero energy buildings.

The U.S. market is witnessing significant advancements in modular and prefabricated construction adhesives, with companies such as 3M and H.B. Fuller launching high-strength SMP solutions that enhance production speed and material compatibility. Federal infrastructure spending on bridge and tunnel restoration is another key driver, specifying durable, flexible hybrid sealants designed to endure extreme thermal and structural stresses. In parallel, the Detroit automotive cluster is utilizing fatigue-resistant MS Polymer adhesives for vehicle lightweighting and improved crash performance. Moreover, R&D investments in fire-retardant SMP formulations align with the country’s evolving safety codes and sustainable materials roadmap, ensuring continuous innovation across multiple industrial sectors.

Germany: European Powerhouse for Sustainable and Automated SMP Adhesive Manufacturing

Germany continues to lead the European MS Polymer Adhesives Market, combining regulatory rigor with advanced manufacturing technologies. Under REACH compliance and Blue Angel certification programs, solvent-based adhesives are rapidly being phased out, and solvent-free, isocyanate-free MS Polymer systems are now the standard for both industrial and architectural applications. German adhesive majors like Henkel and Wacker Chemie AG have spearheaded The transition, developing high-tensile, fast-curing SMP adhesives compatible with robotic dispensing systems in automotive assembly lines.

The country’s research community, supported by Horizon Europe’s sustainability and circular economy goals, is investing heavily in bio-based and recyclable silyl-modified polymer formulations. The initiatives not only enhance environmental compliance but also future-proof the industry against raw material volatility. Germany’s transportation and rail sectors rely extensively on flame-retardant hybrid adhesives meeting EN 45545 standards, crucial for passenger safety. With its dual strengths in technical R&D and export leadership, Germany remains a benchmark for innovation, automation, and eco-efficiency in MS Polymer sealant production across the EU.

Japan: Pioneer in Silane-Modified Polymer Technology and Seismic-Resilient Construction

Japan holds a unique position as the originator and continuous innovator of Silyl Modified Polymer (SMP) technology, primarily driven by Kaneka Corporation’s pioneering research. The country’s advancements focus on polymer backbone optimization for improved weatherability, adhesion versatility, and long-term durability. Given Japan’s frequent seismic activity, high-flexibility hybrid sealants with superior elongation are essential in ensuring structural integrity in curtain wall, glazing, and façade joints of skyscrapers and commercial complexes.

Japan’s industrial adhesives ecosystem extends beyond construction into electronics, appliances, and infrastructure restoration. Fast-curing, single-component SMP adhesives are increasingly utilized in high-speed production lines, supporting manufacturers’ needs for efficiency and precision. In addition, MS polymer coatings and sealants are specified in anti-corrosion applications for bridges and public infrastructure, aligning with the nation’s long-term urban resilience strategy. With its heritage in SMP technology and focus on precision engineering, Japan continues to set the global benchmark for high-performance and seismic-grade polymer adhesives.

France: Driving Flame-Retardant Innovation and Green Building Compliance

France stands at the forefront of hybrid sealant sustainability and safety innovation, leveraging its strong domestic chemical industry and forward-looking environmental policies. Arkema’s Bostik division has expanded its global reach by acquiring Poliplas (Brazil, 2021), reinforcing its leadership in hybrid-technology adhesives and SMP systems. France’s A+ indoor air quality rating standards have become pivotal drivers in the country’s adoption of low-emission hybrid adhesives, particularly in commercial and residential construction projects seeking eco-certification.

In line with Europe’s green building and fire safety mandates, French R&D facilities are focusing on flame-retardant (FR) SMP sealant formulations that comply with EN 45545-2 and marine sector fire safety standards. The local industry is also exploring SMP-based hot melt adhesives for flexible packaging and electronic component assembly, emphasizing both performance and recyclability. France’s combination of regulatory foresight, innovation in polymer chemistry, and cross-sector application diversification cements its role as a European hub for next-generation hybrid sealant technologies.

South Korea: Technological Integration in Automotive, Electronics, and Marine Applications

South Korea has become a pivotal market for hybrid MS Polymer adhesives, driven by its advanced automotive, electronics, and shipbuilding industries. The government’s green construction incentives are promoting large-scale adoption of low-emission SMP sealants, positioning them as a core material for sustainable infrastructure development. Major automakers such as Hyundai and Kia are incorporating MS Polymer bonding systems into their body-in-white structures to improve crash performance, corrosion resistance, and lightweight design for both EVs and ICE vehicles.

The country’s electronics manufacturing dominance fuels significant demand for solvent-free, precision hybrid adhesives used in thermal management and device assembly. In the marine sector, South Korea is a leading adopter of marine-grade SMP sealants, offering high elasticity and saltwater resistance critical for offshore and shipyard applications. With a robust focus on eco-compliance and performance optimization, South Korea is transforming into a high-tech production hub for specialized hybrid sealant systems.

United Kingdom: Retrofitting and Fire-Safe Hybrid Sealant Adoption

The United Kingdom represents one of Europe’s most dynamic hybrid adhesive markets, driven by retrofit initiatives, modular construction, and post-Grenfell fire safety regulations. Government-backed programs aimed at improving the energy efficiency of existing building stock are boosting demand for flexible, high-adhesion MS Polymer sealants used in window, door, and façade retrofits. The rise of off-site and modular construction techniques has created significant opportunities for fast-curing, pre-applied hybrid adhesives, enhancing on-site assembly speed and durability.

Following the Grenfell Tower fire, UK building codes have undergone a fundamental transformation, prioritizing non-combustible and fire-retardant materials. The shift has spurred industry-wide R&D into enhanced FR SMP formulations that comply with BS 8414 and EN 13501 safety classifications. Coupled with expanding use in commercial renovation and sustainable housing, the UK is rapidly becoming a center of innovation for fire-safe, energy-efficient MS Polymer adhesives in Europe.

MS Polymer Hybrid Adhesives & Sealants Market Report Scope

MS Polymer Hybrid Adhesives & Sealants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.5 Billion

|

|

Market Size (2034)

|

$11.6 Billion

|

|

Market Growth Rate

|

6.6%

|

|

Segments

|

By Product Type (Silane Terminated Polyether, Silane Terminated Polyurethane, Modified Polyether Polymer, Other Hybrid Formulations), By Application (Adhesives, Sealants, Coatings), By End-Use Industry (Building & Construction, Automotive & Transportation, Industrial Assembly, DIY/Consumer, Electronics & Electrical), By Curing Mechanism (Moisture-Cure, Two-Component), By Function (Structural Adhesives, Non-Structural Adhesives, Elastic Sealants, High-Strength Sealants), By VOC Content (Low-VOC, Zero-VOC

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, Sika AG, Wacker Chemie AG, Arkema S.A. (Bostik), 3M Company, Dow Inc., H.B. Fuller Company, Kaneka Corporation, Huntsman Corporation, Tremco Illbruck GmbH & Co. KG, Soudal N.V., Mapei S.p.A., DL Chemicals, AGC Chemicals, Hermann Otto GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Type/Resin

- Silane Terminated Polyether

- Silane Terminated Polyurethane

- Modified Polyether Polymer

- Other Hybrid Formulations

By Application

- Adhesives

- Sealants

- Coatings

By End-Use Industry

- Building & Construction

- Automotive & Transportation

- Industrial Assembly

- DIY/Consumer

- Electronics & Electrical

By Curing Mechanism

- Moisture-Cure

- Two-Component

By Function

- Structural Adhesives

- Non-Structural Adhesives

- Elastic Sealants

- High-Strength Sealants

By VOC Content

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in MS Polymer Hybrid Adhesives and Sealants Market

- Henkel AG & Co. KGaA

- Sika AG

- Wacker Chemie AG

- Arkema S.A. (Bostik)

- 3M Company

- Dow Inc.

- H.B. Fuller Company

- Kaneka Corporation

- Huntsman Corporation

- Tremco Illbruck GmbH & Co. KG

- Soudal N.V.

- Mapei S.p.A.

- DL Chemicals

- AGC Chemicals

- Hermann Otto GmbH

*- List not Exhaustive

Research Coverage

This report investigates the MS Polymer Hybrid Adhesives and Sealants Market through decision-grade competitive and technology intelligence, delivers analysis reviews of demand catalysts across green construction, e-mobility, and industrial assembly, curates breakthroughs in hybrid MS chemistries that blend silicone-like elasticity with polyurethane-level toughness, and highlights performance levers such as joint displacement capacity, primerless multi-substrate adhesion, and UV/weather endurance that shorten cycles and reduce total cost-in-use; produced by USDAnalytics, this report is an essential resource for product managers, sourcing leaders, application engineers, and investors who need defensible forecasts, compliance alignment, and clear route-to-market strategies in a rapidly evolving, low-VOC hybrid bonding landscape.

Scope Highlights

Segmentation:

- By Product Type/Resin: Silane Terminated Polyether; Silane Terminated Polyurethane; Modified Polyether Polymer; Other Hybrid Formulations.

- By Application: Adhesives; Sealants; Coatings.

- By End-Use Industry: Building & Construction; Automotive & Transportation; Industrial Assembly; DIY/Consumer; Electronics & Electrical.

- By Curing Mechanism: Moisture-Cure; Two-Component.

- By Function: Structural Adhesives; Non-Structural Adhesives; Elastic Sealants; High-Strength Sealants.

- By VOC Content: Low-VOC; Zero-VOC.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Timeframe: Historic data: 2021–2024; Forecasts: 2025–2034.

Companies: Analysis/profiles of 15+ companies covering strategies, portfolios, and recent developments.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.