Market Overview: Nanoparticle Volume Leadership, High Surface Area Materials, and Electronics Adoption Accelerate Market Expansion

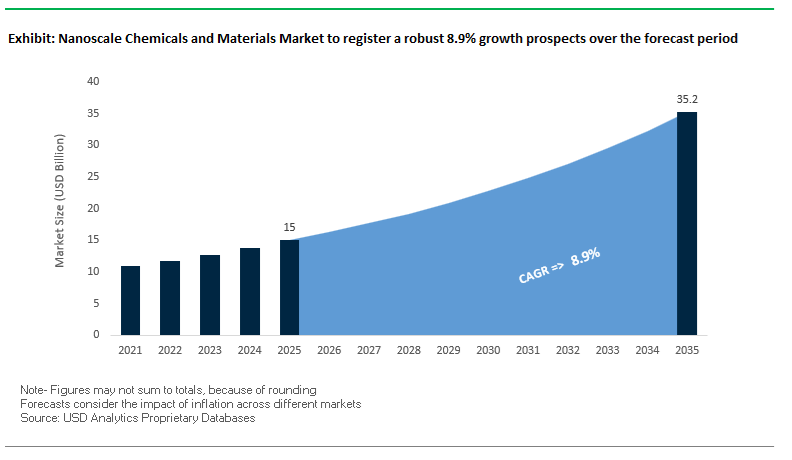

The Nanoscale Chemicals and Materials Market is projected to grow from USD 15.0 billion in 2025 to USD 35.2 billion by 2035, progressing at a strong CAGR of 8.9%. The rapid expansion of nanoscale materials in semiconductors, advanced electronics, catalysis, energy storage, antimicrobial coatings, filtration systems, and healthcare is driving significant demand for nanoparticles, nanostructured composites, nanocarbon materials, and nano-enabled additives. Manufacturers and formulators are scaling production of high-purity nanoscale oxides, nanoporous carbons, quantum dots, and engineered nanostructures to meet increasingly stringent performance specifications across industrial and consumer applications.

Nanoparticles retained a dominant 69% revenue share in 2024, solidifying their position as the backbone of the nanomaterials ecosystem—especially in catalysts, pigments, UV-absorbing coatings, and antibacterial surface treatments. The market is further shaped by advancements in nano-porous carbon materials, now reaching surface areas above 1,500 m²/g, enabling breakthrough performance in supercapacitors, electrochemical water treatment systems, and adsorption-driven environmental purification. Meanwhile, electronics accounted for 33% of total nanomaterials consumption in 2024, driven by the accelerating deployment of CMP nano-slurries, nanoscale transistors, nano-silver inks, and flexible display materials. The U.S. government continues to reinforce the strategic significance of nanotechnology with a USD 2.2 billion FY2025 NNI budget, ensuring sustained federal R&D funding for nanomaterial innovation across defense, energy, and biomedicine.

Key Insights for Nanomaterials Manufacturers, Semiconductor Suppliers & Advanced Materials OEMs

- Nanoparticles command 69%+ revenue share, dominating catalysis, pigments, and antimicrobial coating applications.

- Nano-porous carbons with >1,500 m²/g surface area drive breakthroughs in supercapacitors and water purification.

- Electronics consume 33% of global nanomaterials, led by CMP nano-slurries and nanoscale interconnect technologies.

- U.S. NNI allocates USD 2.2B+ annually, securing long-term nanotechnology leadership in defense & microelectronics.

Market Analysis: CNT Capacity Expansions, Quantum Dot Scale-Up, Patent Leadership Shifts, and Nanomedicine Acceleration Define Market Momentum

The global Nanoscale Chemicals and Materials ecosystem is undergoing large-scale transformation, shaped by major capacity expansions, cross-border collaborations, and new strategic focus areas. In March 2025, Gelion plc entered a strategic cooperation agreement with the Max Planck Institute to advance nanoscale materials for high-performance battery systems—an R&D alliance that highlights the central role of nanostructured chemistries in solid-state and next-generation rechargeable energy storage. Earlier, in November 2024, Nawah significantly expanded its footprint with the inauguration of a CNT facility in Rousset, France, boosting 3D Nanocarbon production from 20,000 m² to 400,000 m², positioning Europe as a critical hub for nano-enabled electronics manufacturing.

The CNT supply chain further strengthened when OCSiAl commissioned its first European TUBALL™ SWCNT plant in Serbia in October 2024, achieving a 60-ton/year starting capacity. These expansions reflect escalating industrial demand for CNT masterbatches in batteries, conductive polymers, EV components, composites, and anti-static materials. Meanwhile, the display industry is undergoing a pivotal shift: in May 2023 (reported October 2025), Nanoco Technologies formed a joint venture with Poly Optoelectronics to double global capacity for cadmium-free quantum dots, directly addressing surging demand for high-color-gamut displays and environmentally compliant materials.

China's strategic dominance in nanotechnology intellectual property continues to strengthen, with 40% of global nanotech patents attributed to China in 2024, surpassing U.S. and Japanese filings combined. Corporate strategies are evolving accordingly: in November 2025, Cabot Corporation identified battery materials and infrastructure applications as its primary 2026 growth drivers, underscoring a shift toward nanoscale conductive additives for EV batteries and grid-scale storage. Leadership transformations indicate further market repositioning: Evonik announced a new regional President for the Americas in December 2025, emphasizing heightened focus on nanoparticle-enabled drug delivery and biomaterials.

Downstream application growth is equally robust. In Q1 2025, DuPont raised its financial outlook due to strong electronics demand supported by advanced semiconductor fabrication requirements, which depend on ultra-high-purity nanoscale chemicals such as nano-silica CMP slurries and nanoscale dielectric materials. Collectively, these developments highlight a market entering a phase of rapid expansion, technological diversification, and geopolitical reshaping.

Breakthrough Trends and High-Value Commercial Opportunities Accelerating Next-Generation Nanoscale Materials Innovation

Market Trend 1: Commercialization of Precision-Engineered Nanoparticle Dispersions Enabling Ultra-Low-Defect CMP Slurries for Semiconductor Manufacturing

One of the most influential trends redefining the nanoscale chemicals and materials market is the rapid commercialization of high-purity nanoparticle dispersions purpose-built for Chemical Mechanical Planarization (CMP) in advanced semiconductor nodes. The performance and yield of sub-10 nm logic and memory devices depend on nanoparticle size precision and dispersion stability. CMP slurries now require exceptionally tight particle size distributions (PSD), with ceria or silica nanoparticles engineered to a D50 between 30 nm and 50 nm, enabling the ultra-smooth local planarity mandated by leading-edge semiconductor fabs.

Defectivity minimization is the critical differentiator. High-end CMP slurries are engineered to meet stringent industry requirements of fewer than 10 defects (>0.2 μm) per 200 mm wafer, as even microscale pits or scratches can render high-value wafers unusable. Selectivity performance is also intensifying: next-generation dielectric CMP formulations must consistently deliver oxide-to-nitride selectivity ratios of 10:1 or higher, ensuring precise polishing control without damaging underlying stop layers.

Achieving this performance requires advanced colloidal stabilization. Manufacturers maintain dispersion stability by tightly regulating Zeta Potential values above ±30 mV, preventing agglomeration and ensuring uniform removal rates. As semiconductor geometries tighten and wafer value rises, the role of nanoscale chemical engineering in CMP slurry optimization becomes a major competitive lever for materials suppliers.

Market Trend 2: Acceleration of MOF Nanocrystal Deployment for High-Selectivity Gas Storage and Separation Systems

The integration of Metal-Organic Framework (MOF) nanocrystals is emerging as a dominant trend across gas separation, purification, and energy storage systems. MOFs offer ultra-high BET surface areas reaching up to 7,000 m²/g—far exceeding the ≈1,000 m²/g performance ceiling of traditional zeolites. This provides unprecedented adsorption capacity and tunable molecular sieving properties, positioning MOFs as next-generation materials for carbon capture, hydrogen storage, and industrial gas separations.

In hydrogen energy systems, MOFs have demonstrated a gravimetric storage capacity of 7.5 wt% at 77 K, a pivotal benchmark for automotive-grade hydrogen storage solutions. For flue gas and CO₂ capture, specific MOF structures achieve exceptional CO₂/N₂ selectivity factors between 100 and 150, enabling efficient separation performance far beyond the capabilities of conventional adsorbents.

Size engineering is key to unlocking their industrial viability. By synthesizing MOFs in the 50–200 nm nanocrystal range, manufacturers drastically reduce mass transfer resistance, improving adsorption/desorption kinetics and cycle efficiency in PSA (Pressure Swing Adsorption) systems. These advancements are accelerating MOF adoption in advanced filtration, gas upgrading, and decarbonization applications.

Market Opportunity 1: Nanoscale Phase Change Materials (nanoPCMs) for High-Efficiency Thermal Management in High-Power Electronics

A major commercial opportunity emerges from the development of nanoscale Phase Change Materials (PCMs) engineered for thermal buffering in high-power electronics, data centers, EV power electronics, and 5G base stations. Conventional paraffin-based PCMs possess high latent heats of fusion between 180 and 250 J/g, and when encapsulated into 100–500 nm nanospheres, they maintain this high energy density while gaining superior thermal transfer kinetics.

Integrating nanoPCMs into Thermal Interface Materials (TIMs) has been shown to reduce peak device temperatures by 5°C to 10°C during high-power bursts, protecting components from thermal shock and increasing operational lifespan. The intrinsic isothermal behavior of PCMs allows systems to operate near the melting point for extended periods, offering thermal smoothing that conventional materials cannot achieve.

Nanoscale encapsulation prevents leakage during phase transitions and drastically improves surface-area-to-volume ratio, enhancing responsiveness to transient thermal loads. As power densities continue to rise across electronics and electrified mobility platforms, nanoPCM-enhanced TIMs represent a critical enabling technology for next-generation thermal management.

Market Opportunity 2: 2D Nanosheets (MXenes & h-BN) as High-Performance Conductive and Insulating Layers for Flexible Electronics

A second major opportunity is the integration of 2D nanosheets—including MXenes and hexagonal boron nitride (h-BN)—into flexible, stretchable, and wearable electronic systems. MXene nanosheets, such as Ti₃C₂Tx, exhibit metallic-level conductivity with sheet resistance as low as 0.3 Ω/sq, outperforming many carbon-based conductors and enabling highly efficient flexible circuits.

MXene films also show exceptional mechanical endurance, retaining over 90% of their conductivity after 10,000 bending cycles at a 1 mm radius, making them suitable for wearable biomedical devices, rollable displays, and soft robotics.

In parallel, h-BN nanosheets serve as outstanding electrical insulators and thermal spreaders. h-BN composites can deliver thermal conductivity values up to 15 W/m·K, compared with just 0.2–0.3 W/m·K for standard polymers, enabling efficient heat dissipation in flexible power electronics. h-BN also provides a remarkably high dielectric strength of ~790 V/μm, meeting insulation requirements for high-voltage, high-power flexible devices.

Together, MXenes and h-BN create a complementary material ecosystem that supports the development of thin, lightweight, and high-performance flexible electronics compatible with future consumer, industrial, and medical applications.

Country Analysis: National Innovation Engines Driving the Global Nanoscale Chemicals and Materials Market

United States: LNP Acceleration, Semiconductor Tooling Leadership, and Multi-Billion Dollar Federal Funding

The United States remains one of the strongest global accelerators of nanoscale chemicals and materials, supported by unprecedented federal investment and a rapidly expanding commercial adoption curve for Lipid Nanoparticle (LNP) technologies and semiconductor nanofabrication tools. The National Nanotechnology Initiative (NNI) requested over USD 2.2 billion for FY2025, reinforcing the critical role of nanomaterials in advanced manufacturing, sustainable energy systems, and semiconductor ecosystems. This funding directly supports nanoscale chemicals used in etching, deposition, metrology, catalysis, environmental remediation, and nanostructured energy storage materials, forming the backbone of the U.S. nanotechnology value chain.

Nanoscale chemicals are experiencing soaring demand due to the continued global commercialization of mRNA vaccines and nucleic-acid therapeutics, which has intensified R&D investment in Lipid Nanoparticles (LNPs) for targeted drug delivery. Major U.S. biotech companies are expanding their partnerships around LNP-enabled drug platforms, reflecting a structural, long-term surge in LNP demand. Meanwhile, advanced equipment suppliers such as CVD Equipment Corporation, which secured a USD 3.5 million follow-on order in November 2024 for chemical vapor infiltration systems, are enabling high-temperature, nanomaterial-enhanced components for aerospace and turbine applications. U.S.-based metrology leaders like Onto Innovation and Veeco Instruments continue to define global benchmarks in nanoscale inspection and deposition technologies crucial for semiconductor scaling, ensuring that the U.S. remains a dominant force in nanomanufacturing precision and supply chain resilience.

China: Carbon Nanomaterial Industrialization and Global Patent Leadership in Nanotechnology

China stands at the forefront of the global nanoscale chemicals and materials market, underpinned by unmatched production capacity in graphene, carbon nanotubes (CNTs), graphene oxide (GO), and nanostructured carbon composites. Between 2000 and 2024, China accounted for approximately 40% of the world’s nanotechnology patent filings, reflecting deep institutional investment, strong state-backed R&D funding, and large-scale industrial adoption. The country’s leadership in carbon nanomaterials is further reinforced through strategic academic partnerships, including collaborations between the National Center for Nanoscience and Technology (NCNST) and the Royal Society of Chemistry, enabling high-volume scientific output and commercialization-ready innovation in nanoscale chemicals.

China’s industrial ecosystem is centered around mega-scale production lines for CNTs used in EV batteries, conductive films, EMI shielding components, and structural composites, positioning the country as a global manufacturing and supply chain powerhouse. Provincial hubs—particularly in Jiangsu and Guangdong—continue to shift from low-cost output to precision nanomaterials manufacturing, with expanding capabilities in catalysis, nano-enhanced coatings, filtration membranes, and high-performance polymers. As China intensifies its investment in next-generation materials that integrate with artificial intelligence, 6G telecommunications, and quantum technologies, its dominance in nanoscale chemicals is expected to grow even further.

India: Strategic ANRF Funding and Deep-Tech Integration Boosting Nanomaterials Adoption

India is rapidly positioning itself as a significant emerging market for nanoscale chemicals and materials through government-led Deep-Tech investments and sector-specific funding that prioritizes indigenous innovation. The operational launch of the Anusandhan National Research Foundation (ANRF) in 2024 marks a pivotal moment, enabling long-term R&D financing for quantum materials, bio-nanosensors, nano-photonics, and high-value advanced materials. These investments are intended to accelerate translational science, bridge academic-industry collaboration, and develop domestic capacity for nanomaterial synthesis, testing, and commercialization.

Defense integration is another major growth catalyst. The ₹500 crore expansion of the Defence Ministry’s Technology Development Fund (TDF) is aimed at supporting the development of next-generation composite materials, nano-enhanced armor systems, and high-temperature coatings for aerospace applications. Additionally, the Bio-RIDE scheme is catalyzing innovations in nanotechnology-driven diagnostics, bio-manufacturing, and therapeutic nanocarriers. India’s simultaneous push for electronics manufacturing, renewable energy, and defense self-reliance is creating a robust domestic market for nanoscale catalysts, nano-enabled coatings, polymer nanocomposites, and functional nanomaterials that feed into mobility, healthcare, and strategic sectors.

Germany & the European Union: Sustainable Nanomanufacturing and High-Precision Specialty Chemical Integration

Germany and the broader EU continue to lead global innovation in sustainable nanomanufacturing, advanced surface chemistry, and high-performance specialty chemicals that integrate nanoscale materials into high-value industrial applications. European chemical majors such as BASF SE and Evonik Industries AG are investing heavily in scaling greener nanomanufacturing processes, targeting automotive lightweighting, next-generation coatings, catalyst optimization, and functional polymer enhancement. These advancements align with the EU’s climate neutrality mandates and circular economy goals, amplifying demand for nanomaterials that offer superior functionality with reduced environmental footprint.

Germany’s leadership in nanopositioning and nanomanipulation tools is another vital pillar of its competitiveness. Companies such as Kleindiek Nanotechnik GmbH provide high-resolution, precision nanoprobes and manipulation systems used in semiconductor R&D, failure analysis, photonics prototyping, and materials characterization. These capabilities strengthen Europe’s semiconductor resilience by enabling local development of nanoscale devices, sensors, and quantum technologies. The EU’s emphasis on sustainable chemistry and autonomous industrial supply chains ensures strong long-term momentum for nanoscale materials embedded in coatings, energy technologies, composites, and digital infrastructure.

United Kingdom: Rapid Scale-Up of Graphene Nanoplatelet Production and Defense-Grade Applications

The United Kingdom is gaining significant prominence in the Nanoscale Chemicals and Materials Market through accelerated commercialization of graphene nanoplatelets (GNPs) and the scaling of industrial production lines. Black Swan Graphene is tripling its domestic GNP production capacity—from 40 to 140 metric tons per year by 2025—at the Thomas Swan facility, marking one of Europe’s largest expansions in graphene output. This scale-up aims to meet growing demand from construction composites, conductive materials, polymer reinforcement, and thermal management applications.

A key differentiator for the UK is its progress in defense-grade nanomaterial adoption. Black Swan Graphene’s partnership to integrate graphene nanoplatelets into GC Shield, a patented ballistic protection system, highlights the strategic role of graphene in advanced armor technologies, enhancing both mechanical strength and energy absorption. This positions the UK as an innovation hub for high-performance protective materials, structural composites, and multifunctional nanomaterials designed for military, aerospace, and industrial applications.

South Korea: Nano Silver Leadership and Conductive Ink Dominance for Advanced Electronics

South Korea is a global leader in high-purity nano silver, nanoscale conductive materials, and advanced printed electronics, driven by its world-class display and semiconductor sectors. Advanced Nano Products Co., Ltd (ANP) plays a pivotal role by supplying high-purity nanomaterials including nano silver and Indium Tin Oxide (ITO), which are essential for OLED, QLED, Micro-LED, and flexible display manufacturing. These nanomaterials enable superior electrical conductivity, transparency, and durability, reinforcing South Korea’s position as a powerhouse in premium consumer electronics.

One of the fastest-growing segments in the Korean ecosystem is conductive nanomaterial-based inks, which are crucial for printed electronics, miniaturized circuits, advanced sensors, and wearable devices. South Korea’s integrated innovation chain—from semiconductor fabs to materials science labs—supports rapid development and commercialization of nanoscale materials with optimized particle size distribution, surface chemistry, and dispersibility. As the country accelerates its move toward flexible electronics, 6G communication hardware, and next-generation batteries, demand for nanoscale chemical precursors and functional nanomaterials is expected to surge substantially.

Competitive Landscape: Nanoscale Innovations, Specialty Chemical Integration, and CNT Masterbatch Leadership Shape Global Market Dynamics

The competitive environment in the Nanoscale Chemicals and Materials Market is defined by companies that combine materials science expertise, nanoscale formulation capabilities, and vertically integrated chemical production. Leaders are diversifying into high-growth areas such as battery materials, drug delivery nanoparticles, conductive additives, and sustainable nanotechnology platforms, establishing strong positions across industrial and high-tech applications.

BASF SE – BASF advances nano-catalysts and ultrafine pigments through sustainability-driven Verbund integration

BASF leverages its global chemical footprint to produce nanoparticulate TiO₂, ZnO, ultrafine pigments, and catalytic nanomaterials, forming the backbone of coatings, cosmetics, catalysis, and functional surface technologies. With its “Winning Ways” strategy launched in September 2024, BASF prioritizes materials enabling green transformation, such as nano-catalysts supporting low-CO₂ processes and energy-efficient industrial systems. Its Verbund manufacturing system provides unparalleled integration, enabling cost-efficient production of nanoscale precursors and large-volume specialty chemicals. BASF’s nano-enabled coatings, energy materials, and catalyst platforms solidify its position as a global leader in scalable nanotechnology solutions.

Dow Inc. – Dow strengthens nanocomposite and nanostructured silicone platforms under its Path2Zero sustainability initiative

Dow integrates nanoscale science across nanostructured silicones, polyolefin nanocomposites, and nanoporous films, delivering performance enhancements in separation technologies, packaging, and electrical applications. Its innovation pipeline emphasizes safer, sustainable materials, embedding environmental and health evaluations into the earliest R&D stages. Through its Path2Zero initiative, Dow is investing in net-zero industrial infrastructure that supports markets such as wire & cable, advanced packaging, and engineered polymers, all of which rely on nano-enhanced performance additives. The company’s focus on circularity and advanced material science positions it as a key supplier for next-generation nanoscale solutions.

Cabot Corporation – Cabot accelerates conductive nanocarbon adoption for EV batteries and sustainable industrial applications

Cabot’s portfolio includes carbon nanotubes (CNTs), nanoscale carbon black, and fumed metal oxides, enabling advanced conductive, mechanical, and reinforcement properties across industries. Cabot’s 2026 strategic outlook identifies Battery Materials as the company’s primary growth opportunity, with nanoscale conductive carbons playing a critical role in lithium-ion battery performance. Its strong sustainability track record—achieving 11 of 15 sustainability goals ahead of schedule—supports customer demand for low-emission, high-conductivity nanomaterials. With new 2030 targets emphasizing a 15% reduction in Scope 1 & 2 GHG intensity, Cabot is aligning environmental responsibility with nanomaterial innovation.

Evonik Industries AG – Evonik expands specialty nanomaterials for medical devices, batteries, and additive manufacturing

Evonik is a global leader in nanoscale materials through its AEROSIL® fumed silica, metal oxide nanoparticles, and lipid nanoparticle (LNP) formulations used in drug delivery. The company’s strategic emphasis on high-margin specialty segments—including medical devices, additive manufacturing, and battery technology—positions it for long-term growth. Evonik is also a strong advocate for responsible nanotechnology, shaping industry safety standards through continuous toxicological research and active regulatory engagement. Its internal restructuring in December 2025, prioritizing healthcare nanomaterials, signals deeper expansion into nanoparticle-enabled therapeutics and biomaterials.

OCSiAl Group – OCSiAl dominates SWCNT production and global masterbatch integration

OCSiAl maintains unrivaled leadership in Single-Walled Carbon Nanotube (SWCNT) production, driven by its TUBALL™ and TUBALL™ MATRIX masterbatch systems. With production capacity scaling toward hundreds of tons per year, OCSiAl enables mass-market SWCNT integration across polymers, rubbers, coatings, batteries, and composites. Its ultra-low loading concentrations (as low as 0.01 wt.%) make SWCNTs a commercially viable option for conductivity, mechanical strength, and electrostatic control. The company’s European expansion strengthens its position as the world’s primary SWCNT supplier, supporting industrial adoption across electronics, automotive, aerospace, and energy storage sectors.

Nanoscale Chemicals and Materials Market Report Scope

Nanoscale Chemicals and Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$15 Billion

|

|

Market Size (2035)

|

$35.2 Billion

|

|

Market Growth Rate

|

8.9%

|

|

Segments

|

By Material Composition (Carbon-Based, Metal-Based, Metal Oxide/Ceramic, Polymer & Lipid Nanomaterials, Quantum Dots), By Physical Form (Nanoparticles, Nanotubes, Nanofibers/Nanowires, Nanocomposites, Nanofilms/Nanosheets), By End-Use Application (Electronics & Semiconductors, Healthcare & Pharmaceuticals, Energy & Environmental Technologies, Automotive & Aerospace, Paints & Coatings)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF, Cabot Corporation, Advanced Nano Products, Arkema, DuPont, Nanophase Technologies, Evonik, Altair Nanotechnologies, Merck KGaA, OCSiAl, Showa Denko (Resonac), Nanoco Group, American Elements, CHASM Advanced Materials, Black Swan Graphene

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Nanoscale Chemicals & Materials Market Segmentation

By Material Composition

- Carbon-Based Nanomaterials

- Metal-Based Nanomaterials

- Metal Oxide / Ceramic Nanomaterials

- Polymer & Lipid Nanomaterials

- Quantum Dots

By Physical Form

- Nanoparticles

- Nanotubes

- Nanofibers / Nanowires

- Nanocomposites

- Nanofilms / Nanosheets

By End-Use Industry

- Electronics & Semiconductors

- Healthcare & Pharmaceuticals

- Energy & Environmental Technologies

- Automotive & Aerospace

- Paints & Coatings

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Nanoscale Chemicals & Materials Market

- BASF

- Cabot Corporation

- Advanced Nano Products (ANP)

- Arkema

- DuPont

- Nanophase Technologies

- Evonik

- Altair Nanotechnologies

- Merck KGaA

- OCSiAl

- Showa Denko (Resonac)

- Nanoco Group

- American Elements

- CHASM Advanced Materials

- Black Swan Graphene.

*- List not Exhaustive

Research Coverage

The latest Nanoscale Chemicals and Materials Market study from USDAnalytics delivers a deep-dive strategic assessment that connects cutting-edge science with commercial scale-up realities. Drawing on multi-year datasets and expert “analysis reviews”, this report investigates how nanoparticles, nanofibers, nanotubes, nanocomposites, and quantum materials are reshaping electronics, semiconductors, life sciences, energy, and advanced coatings. It examines manufacturing innovations in CMP nano-slurries, nano-porous carbons, MOF-based sorbents, nano-PCMs, MXenes, and h-BN, mapping where the most commercially relevant breakthroughs are emerging and how they translate into design wins at leading fabs and OEMs. The study highlights shifts in patent leadership, funding priorities such as the USD 2.2 billion NNI budget in the U.S., and fast-rising regional hubs in China, Europe, South Korea, India, and the U.K. with a clear focus on scalability, purity, and regulatory expectations. Detailed market modelling links nanoscale performance metrics—surface area, particle size distribution, zeta potential, conductivity, and dielectric strength—to revenue pools and margin profiles across key end-use clusters. With rigorous benchmarking of supplier strategies, technology roadmaps, and application pipelines, this report is an essential resource for executives and R&D leaders looking to de-risk investments, identify high-value partnerships, and capture early-mover advantage in nano-enabled chemicals and materials markets.

Scope Highlights

- Segmentation (comprehensive market breakdown)

- By Material Composition: Carbon-Based Nanomaterials, Metal-Based Nanomaterials, Metal Oxide / Ceramic Nanomaterials, Polymer & Lipid Nanomaterials, Quantum Dots

- By Physical Form: Nanoparticles, Nanotubes, Nanofibers / Nanowires, Nanocomposites, Nanofilms / Nanosheets

- By End-Use Industry: Electronics & Semiconductors, Healthcare & Pharmaceuticals, Energy & Environmental Technologies, Automotive & Aerospace, Paints & Coatings

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Time Frame: Historic data from 2021 to 2025 and detailed market forecasts from 2026 to 2034.

- Companies Covered: Analysis / profiles of 15+ leading players across chemicals, nanomaterials, and advanced functional materials manufacturing.