Packaging Additives Market Reaches $1.71 Billion by 2034 as PFAS-Free Processing Aids and Circular Resin Enhancers Redefine Film and Healthcare Packaging

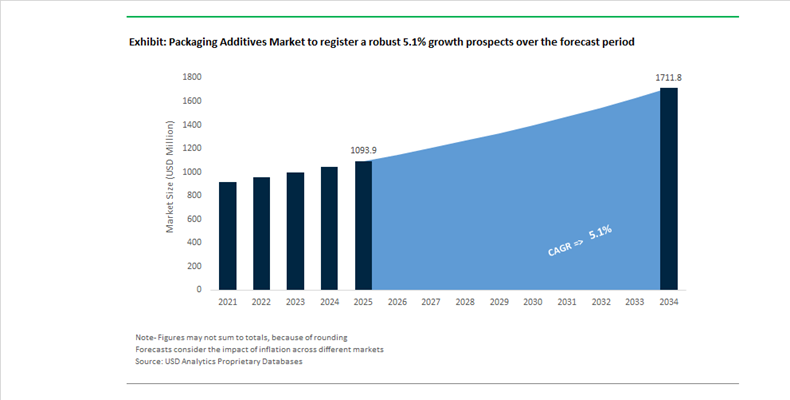

The Packaging Additives Market is valued at $1,093.9 Million in 2025 and is projected to reach $1,711.6 Million by 2034, expanding at a CAGR of 5.1%. Growth is anchored in the global shift toward recyclable mono-material packaging, high-performance recycled content (PCR) incorporation, and elimination of PFAS-based processing aids. Packaging additives including antioxidants, slip agents, anti-block agents, processing aids, UV stabilizers, and anti-scorch systems are becoming critical enablers of circular polymer processing. Regulatory pressure across the EU, North America, and parts of Asia is accelerating reformulation toward non-fluorinated, biomass-balanced, and bio-based additive chemistries, particularly in food-contact, pharmaceutical, and personal care packaging.

In late 2024, Clariant completed the transition to a fully PFAS-free additive portfolio, positioning its AddWorks® PPA range as a fluorine-free solution for melt fracture control and film extrusion stability. In 2024, BASF launched industry-first biomass balance plastic additives produced in Switzerland and Alabama, reducing product carbon footprint through mass balance renewable feedstocks. In October 2024, Evonik announced divestment of its polyolefin and polyester lines to sharpen focus on higher-margin specialty additives for coatings, adhesives, and healthcare applications.

Innovation intensified through 2025. In April 2025, Clariant introduced Ceridust™ 1310 as a high-performance alternative to volatile carnauba wax in printing inks, improving rub resistance and slip in packaging and paper coatings. In August 2025 at K 2025, BASF expanded its VALERAS® platform with Irgastab® solutions engineered to stabilize post-consumer resin streams, improving mechanical properties and processing consistency in recycled packaging. In early 2025, Avient achieved ISCC PLUS certification for its Mevopur™ bio-based masterbatches, enabling up to 70% packaging carbon footprint reduction in pharmaceutical applications.

Healthcare and mono-material packaging are key high-growth segments. In late 2025 and ahead of Pharmapack 2026, Avient introduced non-PFAS polymer processing aids for medical films to reduce die build-up and shark skin defects while meeting pharmaceutical purity standards. In January 2026, Avient expanded the Mevopur™ portfolio with low-retention additives for pipette tips and anti-block solutions for PET and PETG blister films. In July 2025, SIG Group partnered with PulPac to scale fiber-based closures, reducing reliance on plastic cap additives and improving carton recyclability. At the start of 2026, Clariant previewed biopolymer-based Ceridust micronized waxes as replacements for PTFE in food-contact inks.

Packaging Additives Market Trends and Opportunities

PCR-Compatible Additives Become Essential for High-Recycled-Content Packaging

The packaging additives market is undergoing a structural shift as brand owners move beyond basic recyclability claims toward high recycled content targets. Regulations and corporate sustainability commitments are converging around post-consumer recycled plastics, but PCR resins introduce mechanical degradation, moisture sensitivity, and inconsistent melt behavior. As a result, additive systems are increasingly positioned as performance enablers rather than optional formulation tools.

Under the EU Packaging and Packaging Waste Regulation, mandatory recycled content thresholds take effect from 2030 onward, requiring at least 30% recycled content in contact-sensitive PET packaging and up to 35% in other plastic formats. By 2040, these thresholds escalate to 50%–65%, making virgin-only formulations commercially obsolete. Research published in Plastics Engineering confirms that HDPE blends containing 30%–70% PCR cannot achieve virgin-equivalent performance without secondary antioxidants and compatibilizers. In the absence of these additives, melt flow degradation and cross-linking typically cause processing failures after 10–20 extrusion cycles.

In response, masterbatch suppliers such as Avient and Ampacet have launched dedicated recycled-content optimization portfolios. These systems integrate phosphite antioxidants, moisture scavengers, and processing stabilizers that eliminate surface defects such as fish eyes, which are common in high-moisture PCR streams. This trend reflects a broader market reality: recycled content targets are only achievable at scale when supported by advanced additive chemistry.

Non-PFAS Grease and Oil Barrier Additives Become Mandatory in Food Packaging

Food packaging is experiencing a rapid and irreversible shift away from per- and polyfluoroalkyl substances as regulatory bans accelerate across major markets. The voluntary phase-out announced by the U.S. FDA in February 2024, followed by the revocation of 35 food contact notifications by January 2025, effectively removed PFAS-based grease barriers from the U.S. market. Parallel legislation in California, New York, and Maine has reinforced a zero-tolerance approach to intentionally added PFAS in food-contact materials.

This regulatory reset has triggered immediate demand for alternative barrier additives, particularly aqueous coatings and bio-derived polymers that deliver heat and grease resistance without toxic persistence. A notable market pivot emerged in December 2025, when UK-based Xampla and DIC Group announced plans to scale Morro plant-based, PFAS-free coatings across Asia. These natural polymer systems align with Japan’s Plastic Resource Circulation Act, which targets a 25% reduction in single-use plastics by 2030. As PFAS exits the value chain, packaging additives are becoming central to food safety compliance and brand risk mitigation.

Active and Intelligent Additives to Reduce Food Waste

Food waste reduction is emerging as one of the most compelling growth opportunities for packaging additives. According to the UNEP Food Waste Index Report 2024, nearly 19% of food is wasted at the retail and household levels, representing an estimated €132 billion annual loss in Europe alone. Active packaging additives that interact with the internal atmosphere are increasingly viewed as a direct lever to protect margins and reduce supply chain inefficiencies.

Ethylene absorbers and oxygen scavengers have demonstrated the ability to extend the shelf life of fresh produce from 3–4 days to as much as 14–15 days, significantly reducing retail shrinkage. Data published by the International Atomic Energy Agency highlights the effectiveness of PVA-based active films that lower oxygen concentration inside packages to below 0.01%, preventing oxidative rancidity and fungal growth in meat and bakery products. As retailers place greater emphasis on waste reduction KPIs, active additives are moving from pilot programs into mainstream packaging specifications.

High-Performance Clarifying and Nucleating Agents for Transparent PCR Packaging

Consumer preference for clear, visually pure packaging remains strong across beverages and personal care, even as brands transition toward 100% recycled polymers. PCR resins inherently introduce haze and yellowing, creating a growing opportunity for advanced clarifying additives that restore optical clarity.

Sorbitol-based clarifiers and next-generation nucleating agents are increasingly deployed in rPET and rPP packaging to achieve near-virgin transparency. Beyond aesthetics, these additives offer a secondary efficiency benefit by enabling lower processing temperatures. Industry benchmarks show that modern nucleating agents can reduce injection molding energy consumption by 10%–15% while shortening cycle times. Asia-Pacific currently leads global consumption of these additives, driven by rapid expansion in rigid food packaging and aggressive lightweighting initiatives aligned with regional carbon reduction targets.

Packaging Additives Market Share and Segmentation Insights

Antioxidant Additives Lead Packaging Polymer Stabilization in High-Temperature Processing and Recycled Resin Applications

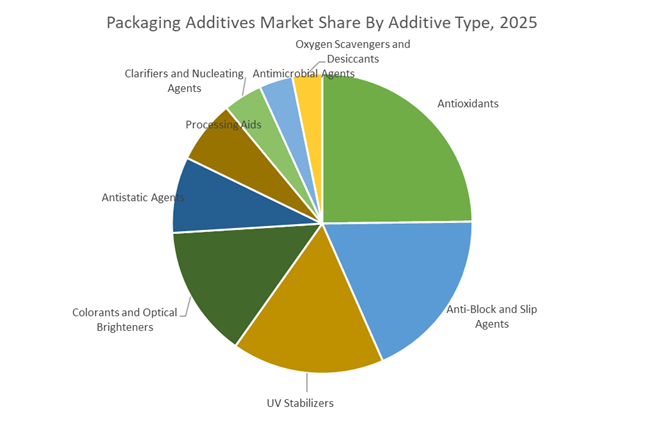

Antioxidants accounted for 24.80% of the Packaging Additives Market by additive type in 2025, reflecting their essential role in protecting polymer packaging materials during processing and throughout product life cycles. These additives prevent oxidative degradation that can occur during high temperature polymer extrusion, molding, and film production processes used in packaging manufacturing. Antioxidants also extend the shelf life of packaged goods by maintaining the structural integrity and clarity of plastic packaging materials. In 2025, demand for advanced antioxidant stabilization systems is rising as packaging producers incorporate higher recycled plastic content into packaging structures, requiring additive packages that stabilize degraded polymer chains while preventing discoloration, odor formation, and mechanical property loss during recycling and reprocessing.

Food and Beverage Packaging Drives Global Demand for Functional Packaging Additives

The food and beverage sector represented 58.60% of the Packaging Additives Market by end-use industry in 2025, making it the largest consumer of functional and processing additives used in packaging materials. Packaging systems for beverages, processed foods, dairy products, and ready meals require additives that maintain product safety, shelf stability, and packaging durability during storage and distribution. Antioxidants, UV stabilizers, oxygen scavengers, antimicrobial agents, and moisture control additives are widely incorporated into polymer packaging structures to protect food quality. In 2025, the growing focus on food waste reduction across global supply chains is accelerating the adoption of shelf life extending packaging technologies, with additive enhanced packaging systems supporting longer storage times and improved product preservation in retail and logistics environments.

Packaging Additives Market Competitive Landscape

The Packaging Additives Market is rapidly evolving toward circular-economy-compatible additives, PFAS-free processing aids, and bio-based stabilizers. Industry leaders are leveraging AI-driven material simulation, dynamic pricing strategies, and recycling-enabling chemistries to meet stringent sustainability, regulatory, and performance requirements across flexible and rigid packaging applications.

BASF leads circular packaging additives with mass-balance antioxidants and AI simulation tools

BASF SE is reinforcing its leadership in packaging additives through its VALERAS® portfolio, targeting circular packaging and low-carbon plastic additives. The March 2026 price increase of up to 20% reflects raw material inflation and freight cost pressures while maintaining value in high-performance stabilizers. BASF’s Irganox® 1010 BMBcert™ and Irganox® 1076 FD BMBcert™ are industry-first mass-balance certified antioxidants, reducing product carbon footprint via renewable feedstocks. Its IrgaCycle™ additives enable upcycling of post-consumer HDPE and PP, addressing degradation challenges in recycled packaging. Integration of Ultrasim® simulation within Creation Centers allows real-time prediction of additive performance, accelerating development of lightweight packaging. This combination of sustainability innovation, pricing power, and digital tools strengthens BASF’s competitive dominance.

Dow scales circular polyolefins and AI-driven additive innovation for packaging applications

Dow Inc. is advancing its packaging additives portfolio through its Transform to Outperform strategy, targeting $2 billion in EBITDA improvement via automation and digitalization. The GoodFlex recycling initiative establishes a scalable model for converting post-consumer plastic films into high-quality feedstock for new packaging materials. Despite $40 billion in 2025 sales, Dow achieved over $400 million in cost savings, enabling reinvestment into circular polyolefins and high-performance tie-layer additives. Its global presence across 29 countries supports rapid deployment of performance materials for packaging, electronics, and mobility sectors. The company is leveraging AI-driven manufacturing to accelerate development of sustainable barrier coatings. This integration of circularity, scale, and digitalization strengthens Dow’s market positioning.

Evonik enables PFAS-free processing and recycling-stage additives for high-quality recyclates

Evonik Industries AG is positioning itself as a specialty additives leader by focusing on recycling-enabling chemistries and PFAS-free processing aids. Its TEGO® CYCLE WA 111 and TEGO® RES 1100 system improves the wet-stage recycling process by removing inks, adhesives, and contaminants, enabling food-contact grade recyclates. The growing adoption of TEGO® PPA grades highlights demand for PFAS-free polymer processing aids amid tightening global regulations. Evonik’s Custom Solutions segment generated €5.5 billion in 2025, maintaining a 16.6% EBITDA margin despite industry challenges. The company is also optimizing its North American distribution network to ensure supply reliability for coatings and inks applications. This focus on sustainability, regulatory compliance, and specialty performance strengthens Evonik’s competitive edge.

Clariant advances heavy-metal-free catalysts and bio-based additives for recyclable packaging

Clariant AG is driving innovation in packaging additives through sustainable chemistry and heavy-metal-free solutions. Its AddWorks™ titanium-based catalysts eliminate antimony in PET production, improving recyclability and regulatory compliance. The company’s Portfolio Value Program targets over 85% of products to be classified as sustainable by 2027, reinforcing its long-term environmental strategy. Clariant’s Arena Circularity hub has accelerated commercialization of bio-based rice bran wax additives for food-contact plastics, supported by expanded EU approvals. The AddWorks™ PKG series delivers enhanced thermal stability and UV protection for polyolefin films used in industrial and agricultural packaging. This combination of sustainable innovation and regulatory alignment strengthens Clariant’s position in advanced packaging additives.

LyondellBasell integrates additives with circular polymers and advanced recycling investments

LyondellBasell (LYB) is transitioning toward a circular materials leader by integrating additives into its Circulen and Purell polymer portfolios. The expansion of Purell healthcare polymers includes specialized additives ensuring compliance with USP and EU Pharmacopeia standards for pharmaceutical packaging. Divestment of European assets by Q2 2026 sharpens focus on high-margin performance olefins and circular polymers in North America. The company is managing $2.9 billion in capital projects, including propylene expansion and advanced stabilizer integration. Strong liquidity, reaching $1.3 billion by 2026, supports investment in the MoReTec molecular recycling facility. This alignment of circular innovation, regulatory compliance, and capital strength enhances LYB’s competitive positioning.

Songwon strengthens stabilizer portfolio with regional expansion and pricing discipline

Songwon Industrial Group is maintaining its position in the packaging additives market through its expertise in polymer stabilizers and operational agility. The company reported sales of over 1 trillion KRW in 2025 while sustaining a 13.7% gross margin despite market oversupply. Its greenfield One Pack Systems (OPS) plant in Saudi Arabia is strategically positioned to serve the growing Middle Eastern packaging market with customized additive blends. Songwon is optimizing its cost structure through warehouse relocation and procurement adjustments to remain competitive in a pricing-sensitive environment. Its Tin Intermediates and PVC stabilizer segments continue to defend market share through technical support and flexible pricing strategies. This focus on efficiency, regional expansion, and product specialization sustains Songwon’s competitiveness.

Germany – Circular Additive Engineering and Regulatory-Led Reformulation

Germany’s packaging additives landscape is being reshaped by circularity mandates and proactive chemical governance. At K 2025 in Düsseldorf, Kisuma Chemicals unveiled magnesium-based additive systems engineered to improve color retention and odor control in post-consumer recycled plastics, directly addressing recyclate quality constraints in food and household packaging. In parallel, BASF SE expanded its VALERAS® platform in late 2025 with mechanical recycling additives that preserve melt-flow stability under high-speed automated packaging conditions, enabling PCR-rich polyolefin structures to meet industrial throughput requirements.

Regulation is the principal accelerator. Following the entry into force of the EU Packaging and Packaging Waste Regulation in February 2025, German producers redirected a majority of R&D toward de-inking and de-metallizing additives to achieve Grade A recyclability targets by 2030. Evonik Industries showcased bio-based wetting agents for aqueous barrier coatings, advancing paper-based food service formats without synthetic fluorochemicals. Infrastructure modernization is reinforcing this pivot, with BASF’s Ludwigshafen upgrade integrating AI-driven molecular modeling for rapid development of non-toxic antioxidants. A 2026 federal mandate eliminating Bisphenol A and derivatives from epoxy can linings is further accelerating demand for polyester-based additive alternatives across metal packaging.

China – Localized High-Performance Supply and Green Packaging Scale

China’s packaging additives market is scaling through localized high-performance production and platform-driven sustainability mandates. In November 2025, BASF SE commissioned a CFRP-enabled dispersant line in Nanjing to stabilize oxygen and moisture barriers in multilayer films, shortening supply chains for advanced additives. Policy direction from the Ministry of Industry and Information Technology of China requires major e-commerce platforms to reach 80% recyclable or compostable packaging by 2030, catalyzing near-term demand for compostable masterbatches based on PLA and PHA for mailers and protective films.

Chemical substitution and right-sizing are equally influential. The 2025 Green Packaging regime is phasing down non-recyclable laminates in favor of aqueous dispersion coatings and PFAS-free oil and water barriers for food delivery. An MoU between Nichetech Advanced Materials and BASF in early 2025 targets sustainable TPU films with integrated UV stabilizers for footwear and electronics packaging. MIIT controls on excessive packaging for health foods and cosmetics are driving adoption of anti-static and slip agents that enable thinner inserts without compromising rigidity. Concurrently, urban waste-sorting expansion is creating a dedicated market for fluorescent sorting markers that improve automated IR identification of polymer grades.

United States – PFAS Exit, Active Functions, and Disclosure Compliance

The U.S. packaging additives market is undergoing a decisive shift driven by chemical regulation and functional innovation. As of January 1, 2026, the U.S. Environmental Protection Agency finalized the listing of nine PFAS compounds as hazardous under RCRA, effectively mandating fluorine-free processing aids across blown film operations. Brand-led sustainability programs are reinforcing lightweighting, with Coca-Cola Europacific Partners reporting that advanced nucleating agents enabled a 15% reduction in PET bottle weight during 2025.

Innovation is broadening from compliance to performance. Late-2025 investments emphasized enzyme-based additives designed to accelerate polyolefin degradation in soil for agricultural mulch and temporary logistics. Active packaging also advanced, as U.S. startups including Loliware commercialized seaweed-derived functional additives delivering oxygen scavenging in home-compostable food films. Transparency requirements are tightening, with EPA updates to the Toxics Release Inventory in November 2025 obligating additive suppliers to notify customers annually about newly listed chemicals of concern, elevating documentation and reformulation readiness.

India – Food Safety Reform and Domestic Capability Building

India’s packaging additives market is being reconfigured by food safety reform and industrial self-reliance. In November 2025, the Food Safety and Standards Authority of India issued a draft amendment proposing a comprehensive ban on PFAS and BPA in food-contact materials by mid-2026, prompting accelerated substitution toward safer slip agents, antioxidants, and barrier enhancers. Standardization is tightening in parallel, as 2025 updates from the Bureau of Indian Standards mandate higher purity for slip and anti-blocking agents used in milk and edible oil pouches.

Capability building under Atmanirbhar Bharat is supporting domestic supply. Targeted grants in 2025 enabled local synthesis of Ziegler–Natta catalysts and associated stabilizers, reducing dependence on imported specialty intermediates. On the innovation frontier, IIT-Madras researchers unveiled mushroom mycelium-based additive systems that bind agricultural residues into biodegradable protective forms, offering an alternative to expanded polystyrene for electronics packaging and signaling a pathway for bio-derived cushioning solutions.

Comparative Snapshot – Packaging Additives by Country

Packaging Additives Market County Level Snapshot

|

Country

|

Primary Driver

|

Regulatory or Market Lever

|

Strategic Position

|

|

Germany

|

Circular recyclability and toxic substitution

|

EU PPWR; BPA elimination

|

Premium compliant solutions

|

|

China

|

Localized performance and platform mandates

|

MIIT green packaging rules

|

Scale-led adoption

|

|

United States

|

PFAS exit and active functions

|

RCRA PFAS listing; TRI updates

|

Rapid reformulation hub

|

|

India

|

Food safety and self-reliance

|

FSSAI draft bans; BIS purity

|

Emerging regulated growth

|

Packaging Additives Market Report Scope

Packaging Additives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1093.9 Million

|

|

Market Size (2034)

|

$1711.6 Million

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

By Additive Type (Antioxidants, UV Stabilizers, Anti-Block and Slip Agents, Antistatic Agents, Antimicrobial Agents, Processing Aids, Clarifiers and Nucleating Agents, Oxygen Scavengers and Desiccants, Colorants and Optical Brighteners), By Material Compatibility (Polyethylene, Polypropylene, Polyethylene Terephthalate, Bio-Based Plastics, Paper and Board), By Functionality (Functional Additives, Processing Additives, Sustainability Additives), By End-Use Industry (Food and Beverage, Healthcare and Pharmaceuticals, Personal Care and Cosmetics, Consumer Electronics, Logistics and E-Commerce)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF, Dow, Clariant, Evonik Industries, LyondellBasell Industries, Songwon Industrial, Milliken & Company, Croda International, Arkema, Avient, SABIC, Mitsubishi Chemical Group, Nouryon, ADEKA, Kisuma Chemicals

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Packaging Additives Market Segmentation

By Additive Type

- Antioxidants

- UV Stabilizers

- Anti-Block and Slip Agents

- Antistatic Agents

- Antimicrobial Agents

- Processing Aids

- Clarifiers and Nucleating Agents

- Oxygen Scavengers and Desiccants

- Colorants and Optical Brighteners

By Material Compatibility

- Polyethylene

- Polypropylene

- Polyethylene Terephthalate

- Bio-Based Plastics

- Paper and Board

By Functionality

- Functional Additives

- Processing Additives

- Sustainability Additives

By End-Use Industry

- Food and Beverage

- Healthcare and Pharmaceuticals

- Personal Care and Cosmetics

- Consumer Electronics

- Logistics and E-Commerce

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Packaging Additives Industry

- BASF

- Dow

- Clariant

- Evonik Industries

- LyondellBasell Industries

- Songwon Industrial

- Milliken & Company

- Croda International

- Arkema

- Avient

- SABIC

- Mitsubishi Chemical Group

- Nouryon

- ADEKA

- Kisuma Chemicals

*- List not Exhaustive