Packaging Inserts and Cushions Market Size, Growth Forecast, and Key Insights

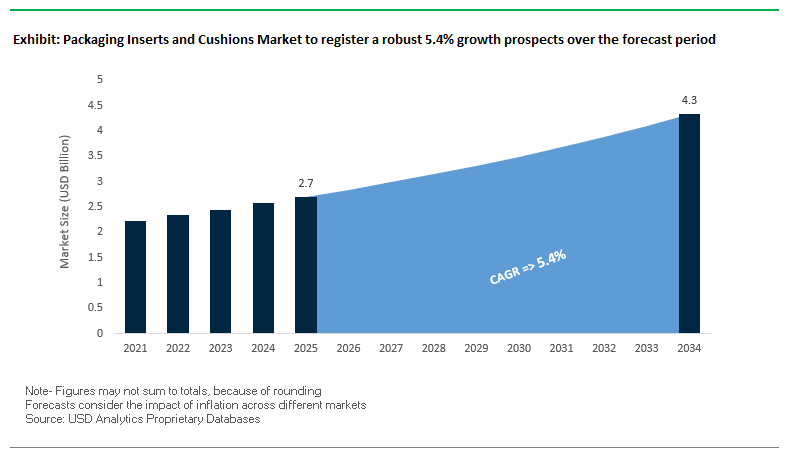

The Global Packaging Inserts and Cushions Market is projected to grow from $2.7 billion in 2025 to $4.3 billion by 2034, reflecting a CAGR of 5.4%. This market is pivotal in providing protective, organizational, and thermal cushioning across diverse industries, including electronics, automotive, pharmaceuticals, and e-commerce. Packaging inserts and cushions, made from materials such as corrugated paper, molded pulp, foam, and plastics, are integral to minimizing transit damage, ensuring product integrity, and enhancing customer satisfaction.

Key Insights for Industry Stakeholders

- E-commerce Growth: Rapid expansion of online retail drives demand for inserts that secure products, reduce returns, and enhance unboxing experiences.

- Sustainability and Circularity: Shift from traditional foams and plastics toward fiber-based, molded pulp, and recycled materials aligns with corporate ESG goals and environmental regulations.

- High-Value Product Protection: Inserts ensure sterility and safety for pharmaceuticals and protect sensitive components in electronics and automotive parts.

- Customization and Design Optimization: Advanced digital design and automation enable tailored inserts that minimize material use, reduce shipping costs, and improve aesthetics.

- Cold Chain and Thermal Performance: Specialized cushions support temperature-sensitive products, maintaining quality across global supply chains.

The market’s growth is fueled by sustainability initiatives, e-commerce demand, and innovation in material science, creating opportunities for high-performance and eco-friendly packaging solutions.

Recent Developments Driving the Packaging Inserts and Cushions Market

The Global Packaging Inserts and Cushions Industry is evolving rapidly, driven by sustainability, advanced manufacturing, and market consolidation. In July 2025, the Amcor-Berry Global all-stock combination officially closed, establishing a dominant player in flexibles and rigid packaging and impacting demand for inserts across multiple product categories. In May 2025, Mondi commissioned a €400 million paper machine at its Štětí mill, strengthening its sustainable paper and packaging capabilities, including materials for cushioning and inserts.

In February 2025, Stora Enso introduced Papira, a bio-based foam packaging material made from wood fiber, designed to be fully recyclable and biodegradable. Earlier, in February 2024, ExxonMobil and Pregis LLC developed a certified-circular polyethylene foam solution, advancing plastics circularity. In December 2024, Woamy, in partnership with Paptic and Secto Design, launched a bio-foam product for fully plastic-free, recyclable packaging. November 2024 marked the completion of the Smurfit Kappa-WestRock merger, creating Smurfit WestRock, a new leader in corrugated and paper-based cushioning.

Additionally, in September 2024, industry reports highlighted the adoption of mono-material packaging solutions, influencing insert design for improved recyclability. In June 2024, Ranpak expanded its paper packaging offerings in China, catering to the growing demand for sustainable paper-based cushions in e-commerce.

Trends and Opportunities Reshaping the Packaging Inserts and Cushions Market

Accelerated Corporate Phase-Out of Plastic Foam Cushioning in E-Commerce

The packaging inserts and cushions market is undergoing a rapid transformation as global e-commerce and retail leaders phase out plastic foam cushioning materials in favor of paper-based and molded fiber alternatives. Amazon set the precedent by eliminating single-use plastics from its Indian fulfillment centers in June 2020, a move aligned with its broader sustainability roadmap. IKEA has committed to eliminating all plastics from consumer packaging by 2028, already phasing out nearly 8,000 tons of EPS annually, and replacing it with fiber-based solutions. Similarly, HP Inc. has pledged to cut 75% of single-use plastic packaging by 2025, accelerating the adoption of molded fiber inserts across its electronics portfolio. These corporate decisions are not voluntary sustainability gestures but are largely compliance-driven, with policies such as the EU’s €0.80/kg plastic tax and U.S. state-level EPS bans exerting strong financial and regulatory pressure. Together, these initiatives represent a structural shift in how major companies approach protective packaging, making plastic-free cushioning a new industry standard.

Adoption of Automated, Right-Sized On-Demand Insert Systems

Automation is emerging as a critical enabler for operational efficiency and sustainability in the packaging inserts and cushions market. Companies like Ranpak have proven that on-demand paper cushioning systems can increase throughput by 4–5x while significantly reducing labor intensity. A 2025 3PL case study demonstrated a 15% reduction in shipping damage and lower dimensional shipping costs through the adoption of automated insert systems. Packaging leaders like Pregis are further advancing automation with their Sharp MaxPro Series, which integrates into high-speed fulfillment lines to generate custom-fit inserts in real time. These systems also address labor shortages, as a single operator with automation can equal the output of four manual packers. With the combined benefits of waste reduction, optimized parcel sizes, and labor efficiency, automated insert technologies are rapidly scaling from pilots to industry-wide adoption in e-commerce, logistics, and retail.

Development of Advanced Molded Pulp from Agricultural Waste

A significant growth opportunity lies in the commercialization of molded pulp inserts derived from agricultural residues, addressing both sustainability and performance needs. India alone generates 350 million tons of agricultural waste annually, creating a vast feedstock for sustainable molded packaging. Companies such as Ecovative Design have pioneered mycelium-based cushions grown on hemp hurd and other waste streams, already adopted by brands like Dell for shipping laptops. Beyond cushioning, academic research at the Bhabha Atomic Research Centre (2024) has highlighted innovations in biopolymer blends from rice straw and bagasse that enhance barrier properties, expanding applicability to moisture-sensitive goods. Unlike EPS or plastic foams, these solutions are curbside recyclable or compostable, creating a strong end-of-life narrative that resonates with ESG-focused brands. For companies seeking to reduce reliance on virgin fiber while achieving superior protection, agro-waste molded pulp represents a scalable, waste-to-value solution.

Integration of Smart Inserts for Enhanced Unboxing and Returns Management

The digital transformation of packaging inserts is opening lucrative opportunities for brand engagement, traceability, and consumer convenience. A leading e-commerce fashion retailer integrated QR codes on inserts, streamlining the returns process and reducing call center inquiries by 40%. In premium consumer goods, conductive inks on inserts have been used to trigger smartphone-based tutorials, with campaigns such as Estee Lauder’s Smashbox achieving 23% activation rates and dramatically increasing consumer interaction times. At the infrastructure level, HolyGrail 2.0 watermarking is being adapted to paperboard, enabling automated sorting between food-grade and non-food-grade materials at recycling facilities. Furthermore, NFC-enabled or serialized inserts are becoming vital tools in industries like pharmaceuticals, where counterfeit prevention and product authentication are critical. By merging functionality with interactivity, smart inserts not only improve operational processes but also create powerful consumer engagement and brand protection mechanisms, positioning them as a future growth frontier in protective packaging.

Competitive Landscape: Leading Companies Driving Innovation in Packaging Inserts and Cushions

The Global Packaging Inserts and Cushions Market is shaped by key players leveraging advanced materials, sustainability, and automated manufacturing to provide high-performance solutions for protective packaging.

Smurfit WestRock: Leading Paper-Based Protective Packaging with Circular Solutions

Smurfit WestRock, formed through the November 2024 merger of Smurfit Kappa and WestRock, is a global leader in paper-based protective inserts and cushioning solutions. Its vertically integrated model—from sustainable forest management to converting—ensures high-quality materials. The company provides corrugated inserts, paper cushion pads, and partitions, serving industrial and delicate consumer goods. Strategic focus lies in circular business models, innovation, and replacing plastics with fiber-based alternatives for sustainable packaging globally.

Pregis LLC: Advancing Air and Foam Cushioning with Sustainable Materials

Pregis LLC specializes in protective packaging solutions, including air cushions, foam-in-place systems, and paper-based inserts. In February 2024, it partnered with ExxonMobil to develop certified-circular PE foam, and in August 2025, expanded its paper portfolio with EasyPack GeoTerra. Pregis emphasizes sustainable packaging, material efficiency, and enhanced unboxing experiences, serving electronics, e-commerce, and pharmaceutical industries with high-performance and recyclable solutions.

Sealed Air Corporation: Innovating Foam-In-Place and Automated Cushioning Solutions

Sealed Air Corporation provides foam-based protective solutions, including Instapak® foam-in-place systems and Bubble Wrap® air cushions. The company is investing in touchless automation for e-commerce and industrial applications and developing products with recycled content and enhanced recyclability. Strategic focus is on reducing waste, improving supply chain efficiency, and delivering sustainable cushioning solutions.

Ranpak Holdings Corp.: Scaling Paper-Based Automation for Eco-Friendly Packaging

Ranpak is a global leader in paper-based cushioning, offering solutions like PadPak® and FillPak® machines that convert paper into void fill on demand. In June 2024, it expanded into the Chinese e-commerce market, and in August 2025, reported strong volume growth in cushioning products in North America. The company’s strategy emphasizes automation, sustainable alternatives to plastics, and scalable global expansion.

DS Smith Plc: Providing Fiber-Based Inserts to Replace Traditional Foam

DS Smith Plc focuses on sustainable, paper-based packaging solutions, including inserts, corrugated dividers, and molded pulp trays. Acquired by International Paper in April 2025, the company has replaced over one billion plastic items with fiber alternatives, demonstrating its commitment to eco-friendly, high-performance cushioning. DS Smith’s strategy centers on innovation, circular economy principles, and growth through sustainable packaging solutions.

Packaging Inserts and Cushions Market Share Insights, 2025-2034

Air Cushions Dominate Market Share by Product Type in the Packaging Inserts and Cushions Industry

Air cushions, also known as inflatable packaging, hold 28% of the packaging inserts and cushions market, making them the leading product type by share. Their growth is tied directly to the explosive expansion of e-commerce and logistics, where lightweight, space-efficient, and cost-effective protective packaging solutions are essential. Air cushions reduce material use and shipping costs by inflating on-site, offering superior void-fill and cushioning without occupying warehouse space pre-inflation. Their customizability, recyclability, and efficiency give them an edge over traditional options such as bubble wrap and loose fill. At the same time, sustainability pressures are driving innovation in recyclable films for air cushions, ensuring they align with corporate plastic reduction targets. While foam inserts remain critical for high-value electronics and fragile goods, and paper-based solutions are gaining traction as a sustainable alternative, air cushions remain the primary choice for high-volume, general-purpose e-commerce packaging.

E-Commerce & Logistics Lead Market Share by End-Use Industry in the Packaging Inserts and Cushions Industry

E-commerce and logistics account for 45% of demand in the packaging inserts and cushions market, highlighting their position as the dominant end-use sector. This leadership is a direct outcome of the global surge in online retail and direct-to-consumer distribution, which demands consistent, high-performance protective packaging to reduce transit damage and minimize returns. Air cushions, paper void fill, and bubble wrap are heavily consumed in this segment because they offer a balance of cost efficiency, protective performance, and storage optimization. Importantly, logistics companies and online retailers are driving innovation in eco-friendly cushioning solutions, such as recycled paper pads and biodegradable air cushions, to meet rising consumer expectations for sustainable packaging. While consumer electronics is the largest manufacturing-driven sector with a focus on precision foam inserts, and healthcare requires highly specialized protective solutions, it is the e-commerce and logistics ecosystem that commands the largest market share due to its scale, frequency, and continuous growth trajectory.

United States Packaging Inserts and Cushions Market Driven by EPR Regulations and Automation Integration

The United States packaging inserts and cushions market is increasingly influenced by Extended Producer Responsibility (EPR) laws, with states such as Maine, Maryland, and Washington mandating higher levels of recyclability and post-consumer recycled (PCR) content. These regulations are reshaping protective packaging design, pushing companies toward more sustainable and reusable cushioning solutions. As e-commerce continues to expand, compliance with such regulations is accelerating the adoption of air cushions, molded inserts, and lightweight fillers made from eco-friendly materials.

Technological advancements are another defining factor. Automation-ready protective packaging is becoming essential as consumer packaged goods (CPG) companies integrate robotics and AI-enabled vision systems into their packaging lines. Many firms report reducing line labor by up to 85% after adopting automation upgrades, which necessitates inserts and cushions designed for seamless integration with automated equipment. Corporate initiatives are also reinforcing this momentum. In August 2025, General Mills, Mars, and PepsiCo co-founded the US Flexible Film Initiative (USFFI) to advance recyclability of flexible packaging—much of which includes film-based cushions and inserts. Demand is particularly robust in e-commerce, food, and consumer goods sectors, where inserts safeguard products during shipping and provide insulation against temperature fluctuations.

Germany Packaging Inserts and Cushions Market Supported by PPWR and Sustainable Design Innovation

Germany’s packaging inserts and cushions market is shaped by the EU Packaging and Packaging Waste Regulation (PPWR) and the amended German Packaging Act (VerpackG) for 2025, which enforce stricter sustainability requirements. These frameworks drive manufacturers to adopt recyclable materials and minimize environmental impact by using ultra-lightweight, resource-saving cushions. Companies are prioritizing compliance through modular designs that optimize material use while enhancing recyclability.

Technological innovation is at the core of German market leadership. The German Packaging Institute (dvi), through its 2025 Packaging Awards, highlighted breakthroughs in sustainable protective packaging, underscoring Germany’s emphasis on eco-design and circular economy practices. With advanced recycling infrastructure already in place, the country is uniquely positioned to scale up closed-loop solutions for inserts and cushions. Demand remains strong across automotive, electronics, and food sectors, where protective packaging is indispensable for ensuring safe transit of delicate electronics, heavy automotive components, and temperature-sensitive food products.

China Packaging Inserts and Cushions Market Accelerated by Dual-Carbon Targets and E-Commerce Boom

China’s packaging inserts and cushions market is advancing under the government’s dual-carbon targets of carbon peaking by 2030 and neutrality by 2060. Regulatory measures introduced in June 2025 for the express delivery sector now mandate degradable and reusable packaging, directly increasing demand for sustainable protective inserts and cushioning solutions. These rules are reshaping the supply chain and promoting widespread adoption of environmentally friendly packaging across industries.

Technological upgrades are also playing a central role. Chinese manufacturers are investing in automation and AI-enabled production systems to boost efficiency and meet quality standards. Leading corporates are also strengthening capacity; Amcor’s new Huizhou facility, equipped with intelligent operations, highlights the trend toward high-quality and sustainable packaging systems tailored for e-commerce and food processing. With over 175 billion parcels delivered in 2024, the country’s massive logistics sector is the primary driver of demand for durable and automation-ready inserts and cushions. The consumer electronics sector is another critical growth engine, relying heavily on shock-absorbing foams and molded inserts for safe delivery.

India Packaging Inserts and Cushions Market Strengthened by Circular Economy Policies and E-Commerce Growth

The Indian packaging inserts and cushions market is supported by government initiatives such as Make in India and the Production Linked Incentive (PLI) scheme, which encourage domestic manufacturing and investment in advanced packaging technologies. The introduction of Extended Producer Responsibility (EPR) guidelines for plastic packaging reinforces the shift toward a circular economy, favoring recyclable and infinitely reusable cushioning solutions.

The market is witnessing growing corporate investments in recycling infrastructure. The Huhtamaki Foundation’s “CloseTheLoop” initiative, backed by ₹10 crore (US$1.18 million), is tackling post-consumer plastic waste by setting up recycling facilities that directly impact the supply of sustainable packaging inserts and cushions. India’s fast-growing e-commerce and food processing industries are key demand drivers. The need for lightweight, durable protective packaging is especially strong in on-the-go beverages, juices, sports drinks, and RTD teas and coffees, where inserts play a crucial role in product safety, shelf presentation, and brand integrity.

Japan Packaging Inserts and Cushions Market Shaped by Positive List Regulations and Sustainable Cushioning Materials

Japan’s packaging inserts and cushions market is adapting to the positive list system for food-contact materials, implemented in June 2025. This regulation restricts the use of synthetic substances in packaging, encouraging the development of safe, compliant, and recyclable protective materials. It is a critical driver for innovation in food-contact inserts and cushions.

Japanese companies are advancing high-quality and functional paper-based barrier solutions. Nippon Paper Industries’ SHIELDPLUS®, for instance, demonstrates how barrier materials can replace plastics while maintaining oxygen and flavor protection. These innovations extend into cushioning technologies designed for both safety and sustainability. With national targets to reduce greenhouse gas emissions by 46% by 2030 and achieve carbon neutrality by 2050, Japan is actively scaling up production of bio-PP plastic products, which will influence the next generation of protective inserts. Strong demand continues in ready-to-drink beverages, snack packaging, and consumer electronics, where lightweight and visually appealing protective packaging is essential.

Brazil Packaging Inserts and Cushions Market Influenced by ANVISA Regulations and PNRS Recycling Mandates

Brazil’s packaging inserts and cushions market is evolving under the National Solid Waste Policy (PNRS) and new 2025 regulations that place greater responsibility on manufacturers and consumers to manage product lifecycles. The Brazilian Health Regulatory Agency (Anvisa) also plays a key role, ensuring protective packaging used in food and beverages meets strict sanitary and safety standards.

Technological progress is centered on bio-based cushioning materials. Companies such as Klabin, in partnership with Optima and Soulpack, introduced a 100% recyclable paper-based diaper packaging solution, showcasing the market’s pivot toward sustainable protective packaging. Upcoming decrees are expected to require companies to recycle up to 50% of their packaging, directly influencing insert and cushion design. Demand is highest in the food and beverage sector, particularly for canned and processed foods, where barrier coatings and protective dividers prevent product damage and maintain quality.

Packaging Inserts and Cushions Market Report Scope

Packaging Inserts and Cushions Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.7 Billion

|

|

Market Size (2034)

|

$4.3 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Material Type (Paper & Paperboard, Plastics, Foams, Molded Pulp), By Product Type (Air Cushions, Bubble Wrap, Foam Inserts, Paper-based Inserts, Corner Protectors, Void Fill), By End-Use Industry (Food & Beverage, Consumer Electronics, Automotive & Industrial Goods, Healthcare & Pharmaceutical, Personal Care & Cosmetics, E-commerce & Logistics)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sealed Air Corporation, Pregis LLC, Smurfit Kappa Group Plc, DS Smith Plc, Sonoco Products Company, Ranpak Corp., International Paper Company, WestRock Company, Mondi Group, Huhtamaki Oyj, Jiffy Packaging, Storopack Hans Reichenecker GmbH, Zotefoams plc, The Dow Chemical Company, JSP Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Packaging Inserts and Cushions Market Segmentation

By Material Type

- Paper & Paperboard

- Plastics

- Foams

- Molded Pulp

By Product Type

- Air Cushions

- Bubble Wrap

- Foam Inserts

- Paper-based Inserts

- Corner Protectors

- Void Fill

By End-Use Industry

- Food & Beverage

- Consumer Electronics

- Automotive & Industrial Goods

- Healthcare & Pharmaceutical

- Personal Care & Cosmetics

- E-commerce & Logistics

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Packaging Inserts and Cushions Market

- Sealed Air Corporation

- Pregis LLC

- Smurfit Kappa Group Plc

- DS Smith Plc

- Sonoco Products Company

- Ranpak Corp.

- International Paper Company

- WestRock Company

- Mondi Group

- Huhtamaki Oyj

- Jiffy Packaging

- Storopack Hans Reichenecker GmbH

- Zotefoams plc

- The Dow Chemical Company

- JSP Corporation

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive research methodology to deliver precise and actionable insights into the global Packaging Inserts and Cushions Market. Our approach combines both primary and secondary research to ensure data accuracy, market relevance, and forecast reliability. Primary research involves structured interviews and consultations with key industry stakeholders, including packaging manufacturers, e-commerce leaders, logistics providers, and material suppliers, to capture qualitative trends, product innovations, and regulatory impacts. Secondary research leverages authoritative sources such as company annual reports, government publications, industry journals, trade associations, and patent filings to validate market dynamics, regional developments, and material adoption patterns. USDAnalytics integrates quantitative modeling techniques, including CAGR computation, market share analysis, and scenario-based forecasting, to project market size and growth trajectories from 2025 to 2034. Our methodology also considers emerging technologies like automated insert systems, molded pulp from agro-waste, and smart cushioning solutions, alongside regional regulations and sustainability initiatives that influence material choices and product deployment. By synthesizing cross-regional trends, competitive strategies, and end-use requirements, USDAnalytics provides a holistic, future-ready market perspective that equips business leaders, investors, and packaging professionals with actionable intelligence for strategic planning, innovation, and investment decisions.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.