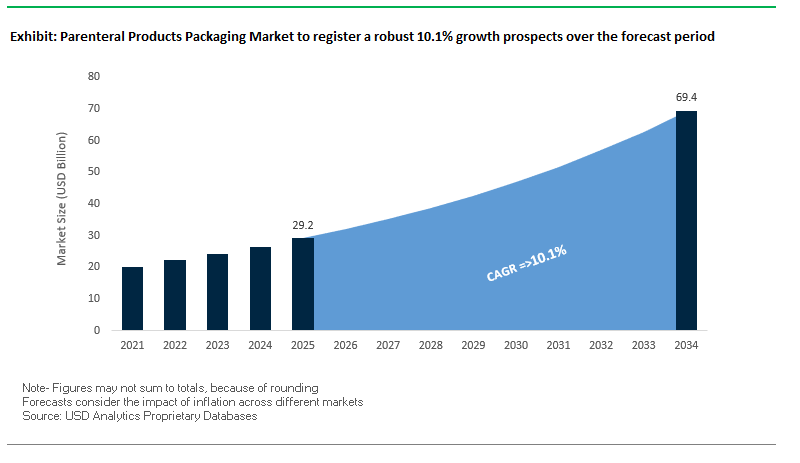

Parenteral Products Packaging Market to Surge from $29.2 Billion in 2025 to $69.4 Billion by 2034 at 10.1% CAGR Driven by Biologics and Patient-Centric Delivery Systems

The Global Parenteral Products Packaging Market is projected to grow from $29.2 billion in 2025 to $69.4 billion by 2034, registering a robust CAGR of 10.1%, propelled by rising biologics production, biosimilars expansion, and increasing demand for patient-centric injectable solutions. This specialized sector plays a critical role in the pharmaceutical ecosystem, ensuring the safety, efficacy, and stability of vaccines, biologics, and other sterile medications through advanced primary and secondary packaging solutions.

Key Insights for Industry Professionals:

- Biologics and Biosimilars Driving High-Performance Packaging Demand: Complex molecules require high-quality glass vials, pre-filled syringes, and advanced cartridges to maintain stability and minimize degradation.

- Shift Toward Patient-Centric Drug Delivery: Ready-to-use solutions such as auto-injectors, wearable injectors, and pre-filled syringes improve patient compliance and reduce medication errors.

- Enhanced Drug Containment and Safety: Packaging utilizes specialized coatings, barrier materials, and high-quality elastomers to prevent extractables, leachables, and container-drug interactions.

- Digitalization and Supply Chain Traceability: Integration of RFID tags and QR codes enables real-time tracking, anti-counterfeiting measures, and enhanced transparency.

- Sustainability in Materials and Processes: Growing emphasis on eco-friendly elastomers and recyclable components aligns with global circular economy principles.

The market is strategically positioned at the intersection of pharmaceutical innovation, patient safety, and supply chain optimization, offering high-value opportunities for packaging manufacturers, pharmaceutical developers, and healthcare stakeholders.

Recent Developments Highlight Strategic Investments and Sustainability Focus in Parenteral Packaging

The Parenteral Products Packaging Industry is rapidly evolving, with strategic expansions, acquisitions, and innovations reinforcing its growth trajectory. In August 2025, SCHOTT AG expanded its operations in India to include syringe and cartridge glass tubing, responding to the country’s surging biopharma demand. Simultaneously, SGD Pharma acquired Alphial S.r.l., enhancing its European footprint and tubular vial capabilities, while Gerresheimer announced the separation of its moulded glass business to sharpen focus on primary pharmaceutical packaging.

In July 2025, West Pharmaceutical Services appointed Robert McMahon as CFO, signaling leadership alignment for strategic growth. AptarGroup strengthened its clinical trial and drug delivery capabilities through the acquisition of a strategic materials manufacturer, supporting accelerated development pipelines. Datwyler focused on operational efficiency in June 2025 by streamlining its U.S. production network and in April 2025 began serial component supply for GLP-1 therapies, reflecting its commitment to high-growth biologics markets.

Earlier strategic initiatives include Datwyler’s February 2025 membership in the Circular Rubber Platform, showcasing sustainability commitments, and ongoing innovations in ready-to-use and patient-friendly packaging solutions.

Trends and Opportunities Transforming the Parenteral Products Packaging Market

Strategic Onshoring of Glass Packaging Manufacturing for Supply Chain Resilience

The parenteral products packaging market is experiencing a strategic reconfiguration as pharmaceutical packaging manufacturers pursue onshoring to strengthen supply chain resilience. The vulnerabilities exposed during the COVID-19 pandemic—when global shortages of vials and syringes delayed critical vaccine distribution—highlighted the risks of dependence on overseas production hubs. In response, leading glass packaging companies are bringing production closer to pharmaceutical markets in the U.S. and Europe. A global specialty glass manufacturer invested over EUR 40 million in a new melting tank for pharmaceutical tubing, while in late 2024, plans were announced for a new tubing facility in the United States. These investments represent a significant capacity build-out designed to guarantee steady supply.

Beyond mitigating geopolitical and logistical risks such as shipping delays, tariffs, and trade disputes, onshoring initiatives are directly linked to tighter quality control. Borosilicate glass, the gold standard for injectable packaging, requires precision manufacturing to meet the exacting standards of regulatory agencies and biopharma customers. By locating production near end-users, manufacturers enable faster feedback loops, closer collaboration with pharma companies, and improved responsiveness to product customization. This trend reflects a permanent shift toward regionalizing pharmaceutical glass production to reduce risk, enhance quality, and strengthen long-term supply security.

Accelerated Adoption of Ready-to-Use Systems and Integrated Delivery Devices

Another defining trend in the parenteral packaging sector is the accelerated transition from traditional vial-syringe formats to ready-to-use (RTU) systems such as pre-filled syringes (PFS), auto-injectors, and integrated delivery platforms. In the last decade, pre-filled syringes have accounted for a growing proportion of approvals for injectable drugs in the U.S. and Europe, particularly in biologics and specialty therapies. This shift reflects the demand for precise dosing, improved safety, and enhanced patient convenience.

The rise of patient-centric care models is amplifying adoption of devices such as auto-injectors, which allow patients to self-administer treatments for chronic conditions at home. A major medical device manufacturer demonstrated this trend in September 2021 with the launch of an auto-injector platform capable of accommodating both 1mL and 2.25mL syringes, underscoring the industry’s focus on flexibility and usability. These innovations reduce dosing errors, needle-stick injuries, and hospital visits, thereby improving adherence and patient outcomes. As biologics and biosimilars dominate the pharmaceutical pipeline, RTU systems and integrated delivery solutions are becoming indispensable, reshaping the competitive landscape of parenteral packaging.

Development of Novel Containment Solutions for High-Potency APIs (HPAPIs)

The rising pipeline of highly potent active pharmaceutical ingredients (HPAPIs), particularly in oncology, presents a critical opportunity for innovation in containment packaging. HPAPIs with Occupational Exposure Bands (OEB) of 4 and 5 require packaging solutions that protect both operators and patients at microgram exposure levels. Contract development and manufacturing organizations (CDMOs) are leading the charge by designing specialized containment systems tailored for HPAPIs. These solutions ensure safety in handling, storage, and transport while preventing cross-contamination in production facilities.

Simultaneously, there is rising demand for specialized glass vials and cartridges that provide superior barrier protection for high-value drugs. Innovations include customized containers engineered to minimize drug-container interaction and resist oxygen, light, and moisture penetration. For instance, in March 2022, a leading pharmaceutical glass company launched a 100mL vial specifically designed for oncology applications, reinforcing the market opportunity for bespoke, high-performance containment solutions. As the prevalence of oncology therapies and advanced biologics grows, the development of HPAPI-compatible packaging will become a key driver of competitive differentiation.

Innovation in Materials and Connectivity for At-Home Drug Administration

The rise of at-home care and digital health is opening new frontiers in parenteral packaging. One of the most promising opportunities lies in the integration of connectivity into injection systems. Smart injectors equipped with Bluetooth-enabled plunger rods can transmit dosage and administration data to healthcare providers in real time, enabling remote monitoring and compliance tracking without altering the drug container. This creates a clear, scalable pathway for pharma companies to add value to existing injectable portfolios by embedding connectivity without regulatory revalidation of the primary container.

Wearable drug delivery platforms represent another high-growth opportunity. Designed to deliver large volumes of medication subcutaneously, these discreet, hands-free devices are transforming patient experience by replacing frequent IV infusions with home-based therapies. A medical technology firm has already introduced a wearable system that automates drug transfer from pre-filled vials and delivers it over a programmed period. This innovation not only improves patient convenience but also reduces hospital resource burdens, aligning with healthcare system priorities to expand outpatient and home-based care. As demand for biologics and specialty injectables rises, innovations in smart, connected, and wearable delivery platforms will play a central role in the future of parenteral packaging.

Key Players Shaping the Global Parenteral Products Packaging Industry Through Innovation and Scale

The Parenteral Products Packaging Market is driven by leading companies leveraging advanced materials science, global manufacturing scale, and innovation to provide high-performance, safe, and sustainable drug containment solutions.

Gerresheimer AG Focuses on Profitable Growth Through Specialized Drug Delivery and Digital Innovation

Gerresheimer is a global leader in glass and plastic primary packaging and drug delivery devices. In August 2025, it announced the separation of its moulded glass business to streamline operations. Its acquisition of Bormioli Pharma contributed to H1 revenue and earnings growth, reflecting its focus on high-value biologics segments. Offerings include vials, ampoules, syringes, cartridges, auto-injectors, and insulin pens, complemented by a formula G growth strategy emphasizing sustainable, profitable expansion and digital solutions.

SCHOTT AG Expands Specialty Glass Production to Meet Growing Biopharma Demand in India

SCHOTT AG, a leader in specialty glass for pharmaceuticals, expanded its Indian manufacturing for syringe and cartridge tubing in August 2025. Its perfeXion® quality system ensures zero-defect manufacturing, and its portfolio includes vials, ampoules, syringes, and cartridges. SCHOTT’s strategy focuses on innovation, material development, and global leadership in biologics packaging.

SGD Pharma Strengthens European Market Presence with Strategic Acquisition of Alphial S.r.l.

SGD Pharma specializes in glass primary packaging, with expertise in tubular and moulded glass. The August 2025 acquisition of Alphial S.r.l. enhanced capabilities and European reach. Its offerings include Ready-to-Use vials, ampoules, and high-quality glass containers. SGD Pharma emphasizes innovation, sustainability, and expanding presence in key markets.

AptarGroup, Inc. Advances Drug Delivery Solutions Through Strategic Acquisitions and Device Expertise

AptarGroup leads in drug delivery components, including plungers, stoppers, closure systems, and nasal spray pumps. In July 2025, the acquisition of a strategic materials manufacturer enhanced clinical trial capabilities. Its PremiumCoat® ETFE-coated components minimize extractables and leachables, supporting safer and more effective drug delivery. Aptar focuses on patient-centric solutions and innovation in delivery devices.

West Pharmaceutical Services, Inc. Drives Quality and Innovation in Injectable Drug Packaging

West Pharmaceutical Services is renowned for elastomer formulations and polymer-based containment solutions. In July 2025, leadership updates included the appointment of a new CFO. Its portfolio features rubber stoppers, plungers, and Daikyo Crystal Zenith® polymer containment systems, delivering enhanced drug stability and regulatory compliance. West emphasizes customer-centric innovation and global manufacturing excellence.

Datwyler Holding AG Accelerates Growth in Biologics Through High-Performance Elastomer Components

Datwyler is a global leader in elastomer components for parenteral products, including stoppers, plungers, and caps. In April 2025, it started serial supply for GLP-1 therapies, and in June 2025 streamlined its U.S. production. Its Omniflex and NeoFlex™ products offer superior drug protection. Datwyler focuses on profitable growth, technical expertise, and sustainability through initiatives like the Circular Rubber Platform.

Parenteral Products Packaging Market Share Insights, 2025-2034

Vials lead Market Share by Product Type in Parenteral Packaging, while Pre-filled Syringes scale fastest

Vials retain the largest product-type share at 35% of parenteral packaging because they are the most versatile, validated, and automation-ready primary container for small molecules, biologics, and lyophilized drugs; their compatibility with diverse stopper/seal systems and proven stability files lowers regulatory risk and speeds fill-finish scalability. Pre-filled syringes (30%) are the structural growth engine as self-administration and patient-centric drug delivery accelerate—silicone-oil-free barrels, sensitive-biologic plungers, and integrated safety needles reduce medication errors and needlestick incidents while meeting stringent extractables/leachables controls. Bags & bottles sustain a durable share in large-volume parenterals (LVPs) as hospitals standardize on non-PVC, multi-layer films to enhance drug compatibility and reduce plasticizer migration. Cartridges expand with the proliferation of auto-injectors and pen systems in diabetes and chronic care, locking packaging selection to device platform strategy. Ampoules persist as a niche for single-dose, highly sensitive actives where rubber contact is undesirable, despite handling and particulate concerns. Finally, ready-to-use (RTU) systems—fully sterilized primary containers and drug-device combinations—capture premium, fast-growing share by compressing preparation time and error risk in critical-care settings. The product mix underscores how biologics, home care, and sterility assurance are realigning market share away from commodity containers to high-value, compliance-forward formats.

Pharmaceutical & Biotech hold dominant Market Share by Application in Parenteral Packaging

Pharmaceutical and biotechnology companies account for 65% of demand because parenteral packaging decisions are made at the aseptic fill-finish node, where stability, sterility assurance, and regulatory compliance dictate container closure selection across clinical and commercial scales. Sponsors’ pivot to biologics and biosimilars concentrates spend on pre-filled syringes, advanced vial systems, and RTU platforms that minimize line interventions and improve cGMP throughput. Hospitals and clinics represent the next-largest consumption base, pulling a wide portfolio—from LVP bags for hydration and nutrition to chemotherapy vials and emergency-use PFS—with purchasing criteria centered on workflow efficiency, dose accuracy, and safety-engineered devices to cut preparation time and contamination risk. Home healthcare & self-administration is the fastest-growing application: aging demographics, chronic disease prevalence, and payer pressure to de-institutionalize care are shifting share toward auto-injectors, pen cartridges, and wearable injectors, packaging that prioritizes usability, tamper evidence, and human-factors engineering. Across applications, share concentration reflects the premium placed on sterile barrier performance, container–drug compatibility, and end-user safety, with reimbursement and real-world adherence amplifying adoption of ready-to-use delivery formats.

United States Parenteral Products Packaging Market Accelerated by Biologics and Domestic Manufacturing Investments

The United States parenteral products packaging market is being reshaped by pharmaceutical industry investments, regulatory reforms, and advanced automation. Major players such as Eli Lilly and Johnson & Johnson are investing billions into domestic fill-finish capacity, which directly increases the demand for sterile vials, pre-filled syringes, and ready-to-use (RTU) systems. These formats are particularly valuable for biologics, personalized medicine, and biosimilars, where precision, sterility, and patient convenience are critical.

Government support is also reinforcing this market shift. Executive Order 14293 has streamlined approvals for new manufacturing facilities while tightening oversight of foreign imports, incentivizing companies to expand U.S.-based packaging operations. At the same time, the FDA is issuing guidance for combination products, enabling innovation where packaging doubles as a drug delivery system. Parallel to regulatory progress, the adoption of automation and robotics on secondary packaging lines is driving efficiency, reducing human error, and ensuring compliance with stringent sterility standards. Together, these developments are positioning the U.S. as a leader in high-value pharmaceutical packaging solutions.

China Parenteral Products Packaging Market Strengthened by Glass Preference and R&D Investments

The China parenteral products packaging market is expanding rapidly, driven by government-led modernization and a focus on safer drug delivery. Chinese authorities are urging pharmaceutical packaging companies to invest in R&D for innovative and eco-friendly materials, with an emphasis on stability and safety during long-term drug storage. A notable trend is the strong reliance on glass vials and ampoules, valued for their durability, non-reactivity, and transparency, making them the preferred material for biologics and vaccines.

The rise of China’s biologics and vaccine manufacturing capacity has amplified the need for advanced packaging solutions capable of ensuring sterility and drug integrity. With government backing, domestic companies are scaling up production to meet both local and export demand, while upgrading facilities to align with international quality standards. These trends confirm China’s growing role as a global hub for parenteral packaging innovation.

Germany Parenteral Products Packaging Market Driven by EU Regulations and Industry Leadership

The Germany parenteral products packaging market is heavily influenced by stringent EU sustainability and compliance regulations. The Packaging Act (VerpackG) and the EU Packaging and Packaging Waste Regulation (PPWR) are reshaping design standards by mandating recyclability, reduced waste, and increased use of recycled materials in secondary packaging. These rules are compelling manufacturers to balance sustainability with the uncompromising safety needs of parenteral drug packaging.

Germany is home to global leaders such as Gerresheimer and Schott AG, which dominate in pharmaceutical glass and advanced polymer packaging solutions. Both companies continue to expand production capacity and pioneer new manufacturing technologies that enhance barrier protection and sterility. Compliance and quality remain central, as German and EU regulations demand the highest standards of product safety, traceability, and recyclability, making Germany a benchmark market for sustainable pharmaceutical packaging innovation.

India Parenteral Products Packaging Market Expanding Under PLI Scheme and Vaccine Growth

The India parenteral products packaging market is advancing rapidly due to strong government support and the expansion of pharmaceutical manufacturing. The Production Linked Incentive (PLI) scheme incentivizes investment in high-value pharmaceutical products, including sterile packaging for injectables. Meanwhile, the Free Essential Drugs Initiative under the National Health Mission has increased bulk procurement of generics, placing pressure on manufacturers to deliver efficient, high-quality packaging and streamlined supply chain systems.

The growth of biosimilars and vaccine production is further boosting demand for specialized vials, syringes, and IV bags. Domestic firms are adopting IT-backed supply chain technologies for real-time tracking and quality assurance, aligning with global compliance standards. With the rise of e-health programs and an expanding middle-class population, India’s pharmaceutical packaging industry is moving beyond volume-based production to focus on quality-driven, export-ready parenteral packaging solutions.

Japan Parenteral Products Packaging Market Advancing with Smart and Sustainable Technologies

The Japan parenteral products packaging market is distinguished by its focus on technological innovation and smart packaging integration. Japanese companies and research institutions are pioneering the use of RFID tags, temperature indicators, and connected devices to monitor sensitive biologics and vaccines throughout the supply chain. The government is actively funding projects under its Green Innovation framework, supporting the creation of eco-friendly and intelligent drug delivery packaging systems.

Events like the annual Combination Product Seminar underscore Japan’s emphasis on integrated solutions that merge packaging with drug delivery functionality. At the same time, firms such as Nippon Paper Industries and Oji Holdings are investing in sustainable materials and new production facilities, aiming to reduce the industry’s carbon footprint. With strong regulatory oversight and a culture of precision manufacturing, Japan continues to lead in next-generation parenteral packaging technologies that balance performance, safety, and sustainability.

Brazil Parenteral Products Packaging Market Supported by ANVISA Reforms and Local Innovation

The Brazil parenteral products packaging market is experiencing growth as regulatory modernization improves agility for manufacturers. The National Health Surveillance Agency (ANVISA) has introduced reforms such as RDC 843/2024, which unifies and simplifies procedures for packaging and product registration. This streamlined framework enables faster market entry for innovative packaging solutions and encourages investment from both domestic and multinational firms.

The simplified environment has already encouraged companies to introduce advanced packaging innovations tailored for local needs. Partnerships, such as those pioneered by Nestlé Brazil with renewable packaging solutions, demonstrate the potential for crossover between food and pharmaceutical packaging technologies. With its large domestic healthcare market and ongoing regulatory clarity, Brazil is positioning itself as a regional hub for parenteral packaging growth and innovation.

Parenteral Products Packaging Market Report Scope

Parenteral Products Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$29.2 Billion

|

|

Market Size (2034)

|

$69.4 Billion

|

|

Market Growth Rate

|

10.1%

|

|

Segments

|

By Product Type (Vials, Pre-filled Syringes, Ampoules, Cartridges, Bags & Bottles, Ready-to-Use Systems), By Material (Glass, Plastics & Polymers, Elastomers, Others), By Packaging Type (Primary, Secondary), By Drug Type (Small Molecules, Biologics & Biosimilars, Vaccines, Insulin, Ophthalmics, Other Drugs), By Application (Hospitals & Clinics, Pharmaceutical & Biotechnology Companies, Home Healthcare & Self-Administration)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Gerresheimer AG, West Pharmaceutical Services, Inc., SCHOTT AG, Stevanato Group, Nipro Corporation, SGD Pharma, AptarGroup, Inc., Berry Global Inc., Amcor Plc, Catalent, Inc., Becton, Dickinson and Company, SiO2 Materials Science, Adelphi Healthcare Packaging, Datwyler Holding Inc., DWK Life Sciences GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Parenteral Products Packaging Market Segmentation

By Product Type

- Vials

- Pre-filled Syringes

- Ampoules

- Cartridges

- Bags & Bottles

- Ready-to-Use Systems

By Material

- Glass

- Plastics & Polymers

- Elastomers

- Others

By Packaging Type

By Drug Type

- Small Molecules

- Biologics & Biosimilars

- Vaccines

- Insulin

- Ophthalmics

- Other Drugs

By Application

- Hospitals & Clinics

- Pharmaceutical & Biotechnology Companies

- Home Healthcare & Self-Administration

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Parenteral Products Packaging Market

- Gerresheimer AG

- West Pharmaceutical Services, Inc.

- SCHOTT AG

- Stevanato Group

- Nipro Corporation

- SGD Pharma

- AptarGroup, Inc.

- Berry Global Inc.

- Amcor Plc

- Catalent, Inc.

- Becton, Dickinson and Company

- SiO2 Materials Science

- Adelphi Healthcare Packaging

- Datwyler Holding Inc.

- DWK Life Sciences GmbH

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive research methodology to deliver accurate and actionable insights into the Parenteral Products Packaging Market. Our approach integrates both primary and secondary research, leveraging proprietary databases, industry reports, company disclosures, and regulatory filings to evaluate market dynamics, competitive strategies, and growth drivers. We conduct in-depth interviews with key industry stakeholders—including manufacturers, distributors, pharmaceutical companies, and regulatory authorities—to validate trends such as the rise of biologics, pre-filled syringes, and patient-centric drug delivery systems. Quantitative data is analyzed using statistical and econometric models to determine market size, CAGR projections, and segment-wise opportunities, while qualitative assessments capture innovation trends, sustainability initiatives, and emerging technologies such as smart connected devices and barrier coatings. USDAnalytics combines regional market analyses, supply chain insights, and regulatory frameworks to provide a holistic view of market opportunities across North America, Europe, Asia-Pacific, and Latin America, enabling pharmaceutical packaging companies, investors, and healthcare stakeholders to make data-driven strategic decisions in a rapidly evolving parenteral packaging ecosystem.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.