Pharmaceutical Labeling Market Size, Overview, and Growth Outlook (2025–2034)

Pharmaceutical Labeling Market to Reach $10.3 Billion by 2034 Driven by Serialization, Smart Labels, and Patient-Centric Solutions

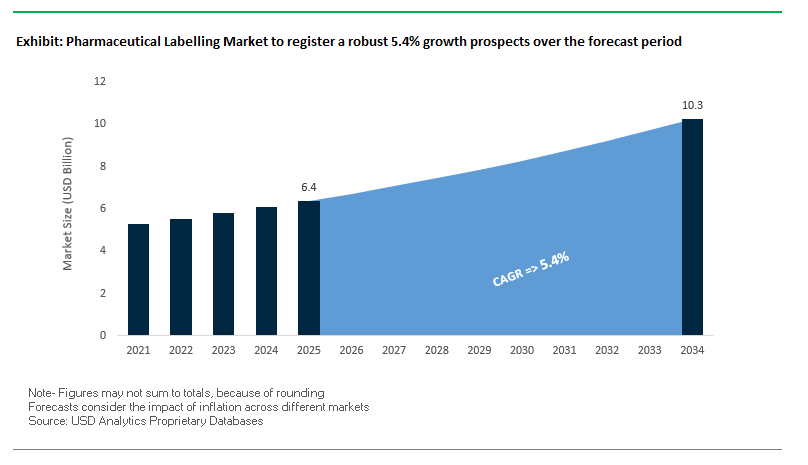

The Global Pharmaceutical Labeling Market is projected to grow from $6.4 billion in 2025 to $10.3 billion by 2034, with a CAGR of 5.4%. The market encompasses both primary packaging labels and patient information leaflets, ensuring product authenticity, safety, and regulatory compliance across the pharmaceutical supply chain.

Key Insights for industry professionals and buyers:

- Regulatory Compliance Drives Serialization and Traceability: Mandatory initiatives like the U.S. DSCSA and EU FMD are essential for combating counterfeiting and ensuring product authenticity.

- Shift Toward Patient-Centric and Accessible Labeling: Larger fonts, clear instructions, and multilingual content improve adherence and reduce medication errors.

- Integration of Digital and Smart Labels: QR codes, NFC tags, and other embedded technologies enhance security, traceability, and patient engagement.

- E-Labeling Adoption is Rising: Regulatory mandates for electronic product information are pushing companies toward digital access solutions, including text-to-voice and multilingual support.

- Sustainability and Eco-Friendly Materials: Increasing demand for less-plastic and recyclable label materials aligns with broader environmental goals.

Market Analysis: Recent Developments Highlight Focus on Smart, Sustainable, and Compliant Pharmaceutical Labeling

The pharmaceutical labeling industry is experiencing rapid technological and strategic evolution. In August 2025, ProAmpac released its Sustainability Impact Report, reflecting growing emphasis on eco-friendly label materials and adhesives. The same month, AbbVie announced positive topline results from its Phase 3 UP-AA trial, likely triggering demand for new product labeling and patient leaflets. In July 2025, the Pet Sustainability Coalition initiated programs promoting sustainable packaging, influencing labeling innovations across multiple markets, including pharmaceuticals.

Sustainability and digital integration remain central themes. June 2025 research highlighted consumer preference for reduced-plastic packaging, driving innovation in label materials. May 2025 saw Duni Group discontinue PFAS-containing packaging, reinforcing the trend toward non-toxic adhesives and coatings. In April 2025, Freyr emphasized AI adoption in labeling, enabling automated regulatory compliance analysis and error reduction.

The industry also responds to strategic acquisitions and collaborations. In February 2025, Berry Global and VOID Technologies partnered to develop high-performance sustainable films suitable for flexible, high-barrier labels. January 2025 witnessed Johnson & Johnson’s $14.6 billion acquisition of Intra-Cellular Therapies, necessitating integration of new labeling systems to accommodate expanded product lines.

Transformative Trends and Emerging Opportunities in the Pharmaceutical Labelling Market

Rapid Adoption of Digital Output for On-Demand and Variable Labeling

The pharmaceutical labelling market is undergoing a fundamental transformation as digital output becomes the cornerstone for on-demand and variable labelling solutions. Clinical trial supply chains highlight the benefits of this shift, with a pilot project on digital display labels (DDLs) reducing relabeling timelines from months to just a single day. This efficiency is critical in trials where regulatory modifications, patient information updates, or dosage adjustments must be implemented immediately across global sites. Beyond trials, the pharmaceutical sector’s growing emphasis on patient-centric care models, especially with the rise of biologics and personalized medicines, is creating demand for highly flexible labelling systems. Digital printing allows companies to produce small, tailored batches of labels with variable data such as patient-specific instructions, serialized codes, or localized regulatory information. This adaptability minimizes waste, ensures compliance with dynamic regulations, and supports market agility. As the sector advances toward more specialized treatments, on-demand digital labelling will play a decisive role in aligning supply chain responsiveness with patient safety and regulatory compliance.

Integration of NFC and RFID for Enhanced Patient Engagement and Anti-Counterfeiting

Digital technologies are transforming pharmaceutical labelling into a multifunctional platform for security, compliance, and patient engagement. Counterfeit medicines remain a critical challenge, with estimates suggesting billions of dollars lost annually to fake products. The use of RFID tagging, as demonstrated by Pfizer’s 2006 initiative with Viagra, has proven effective in enabling real-time verification across wholesale and retail supply chains. Today, RFID is expanding into mainstream use, empowering stakeholders to scan labels and confirm authenticity against centralized databases. In parallel, Near-Field Communication (NFC) technology is driving patient engagement. By tapping an NFC-enabled carton with a smartphone, patients can instantly access instructional videos, dosage reminders, or digital patient information leaflets (PILs). Unlike traditional static labels, this interactive model ensures patients with complex or home-administered therapies receive real-time, personalized guidance. As counterfeit prevention and patient adherence rise to the forefront of pharmaceutical priorities, the integration of RFID and NFC in labelling is redefining packaging from a static identifier into a dynamic enabler of trust, transparency, and education.

Development of Sustainable Label Substrates and Adhesives

Sustainability has become a non-negotiable driver in pharmaceutical packaging, with labelling emerging as a crucial area for innovation. Corporate ESG commitments from leading drugmakers are setting clear deadlines—Novartis aims for 100% recyclable packaging by 2025, while Merck targets 2030—placing pressure on suppliers to deliver recyclable and renewable labelling solutions. Labels made from recycled content, bio-based films, or adhesives designed for improved recyclability are increasingly being commercialized. The industry is also exploring mono-material laminates, which simplify recycling by reducing material complexity. Academic research underscores the urgency of this transition: producing just one kilogram of active pharmaceutical ingredients can generate nearly 100 kilograms of waste, spotlighting the sector’s need for more sustainable supply chain practices. Labels, often overlooked in sustainability discussions, are now becoming a focal point for reducing environmental impact. By embedding recyclable materials and eco-friendly adhesives into pharmaceutical labelling, companies can align regulatory compliance with corporate sustainability pledges while differentiating themselves in a market increasingly scrutinized for environmental performance.

Expansion of Augmented Reality (AR) for Regulatory and Multilingual Compliance

The pharmaceutical labelling market also presents significant opportunities in leveraging digital overlays such as Augmented Reality (AR) to enhance patient understanding and global regulatory compliance. Research on AR tools like the Mediscan application demonstrates how scanning a drug package can provide patients with dynamic overlays displaying dosage instructions, side effects, and interactive guidance. This enhances both adherence and patient confidence, particularly for therapies requiring detailed self-administration. AR-enabled labelling also supports the transition toward e-labeling, which has been recognized in global harmonization initiatives as a scalable solution for multilingual compliance. By embedding QR codes or digital identifiers, companies can provide cloud-based access to updated, region-specific product information, eliminating the logistical burden of printing multiple translations on a physical label. This ensures that healthcare professionals and patients worldwide can instantly access accurate and localized information. As pharmaceutical markets globalize and regulatory frameworks tighten, AR and e-labeling not only ensure compliance but also transform labels into powerful tools for patient education, engagement, and cross-border accessibility.

Competitive Landscape: Leading Pharmaceutical Labeling Companies Are Driving Innovation in Smart, Sustainable, and Compliant Solutions

The global pharmaceutical labeling market is shaped by key players leveraging materials science, advanced printing technologies, and regulatory expertise to provide high-performance, durable, and intelligent labeling solutions.

CCL Industries Inc.: Delivering Vertically Integrated, High-Security Pharmaceutical Labels

CCL offers specialty labels including pressure-sensitive, shrink sleeves, and in-mold labels for vials, bottles, and syringes, alongside extended content labels (ECL). The company invests in enhanced security features like holograms and tamper-evident seals. Its global manufacturing network and printing expertise enable customized solutions that meet stringent regulatory and quality standards. CCL strategically focuses on innovation, sustainability, and providing high-value labeling solutions for pharmaceutical clients.

Schreiner Group GmbH & Co. KG: Pioneering Smart and Functional Labels for Patient Safety and Compliance

Schreiner Group specializes in functional and smart labels with integrated technologies such as RFID, NFC, and tamper-evident features. The Schreiner MediPharm division targets pharmaceutical labeling, supporting cold chain management and patient adherence. Known for customized, high-tech solutions, Schreiner emphasizes R&D investment to develop intelligent labels that enhance security, regulatory compliance, and patient-centric functionality.

WS Packaging Group, Inc.: Advancing Sustainable and Variable Data Labeling Solutions

WS Packaging provides pressure-sensitive labels and printed packaging for pharmaceuticals. The company focuses on sustainable labeling initiatives, eco-friendly materials, and inks. Investments in variable data printing technologies support pharmaceutical serialization and traceability requirements. WS Packaging’s strategy is to offer reliable, cost-effective, and on-time labeling solutions that meet evolving customer needs.

UPM Raflatac: Innovating Sustainable Label Materials for High-Performance Pharmaceutical Applications

UPM Raflatac supplies high-quality face materials, adhesives, and liners critical for pharmaceutical labeling. The RafCycle™ recycling service and development of recycled-content, water-based adhesive materials demonstrate commitment to sustainability. Known for material innovation and high reliability, UPM Raflatac ensures labels withstand temperature changes, chemicals, and compliance challenges. The company’s strategic focus is on sustainable, efficient, and compliant labeling solutions.

3M Company: Enhancing Pharmaceutical Labeling Through Advanced Adhesives and Materials Science

3M provides specialty adhesives, films, and tapes for tamper-evident and security labels. Investments in temperature-resistant adhesives support biologics and cold chain storage requirements. 3M leverages its materials science expertise to deliver high-performance, reliable, and sustainable labeling solutions. The company focuses on science-based innovation, circular economy initiatives, and reducing environmental impact.

Pharmaceutical Labelling Market Share Insights, 2025-2034

Pressure-Sensitive Labels Dominate Market Share by Label Type in Pharmaceutical Labelling

Pressure-sensitive labels (PSLs) hold a commanding 65% share of the pharmaceutical labelling market, making them the uncontested leader across global drug packaging formats. Their dominance is anchored in their adaptability for vials, bottles, syringes, and medical devices, where regulatory compliance, variable data printing, and high-speed application are non-negotiable. PSLs seamlessly integrate serialization features such as 2D data matrices and RFID tags to meet global track-and-trace regulations (e.g., DSCSA, EU FMD), positioning them as the cornerstone of compliance-driven labelling. Shrink sleeve labels, while smaller in share, add value for tamper-evidence and 360° branding on complex containers, and wrap-around labels remain relevant for high-volume cylindrical bottles in OTC drugs and nutraceuticals. Booklet and outsert labels, categorized under “others,” play a critical compliance role by delivering mandated prescribing information that exceeds the space available on primary packaging. Though niche, in-mold labels (IML) serve specific hospital and diagnostic packaging needs, offering abrasion resistance and permanence. Overall, the leadership of PSLs highlights how efficiency, compliance, and versatility converge to make them the backbone of pharmaceutical labelling.

Prescription Drugs Hold the Largest Share by Application in Pharmaceutical Labelling

Prescription drugs account for 40% of pharmaceutical labelling demand, reflecting the strictest regulatory oversight and the highest compliance burden in the industry. Every prescription product requires serialization, tamper-evidence, and often multilingual content, making labels a high-value component of the packaging system. Beyond compliance, this segment integrates advanced features like anti-counterfeit holograms and track-and-trace barcodes to ensure patient safety and supply chain transparency. OTC drugs follow as the second-largest share, balancing regulatory requirements with consumer marketing through visually engaging, shelf-differentiating labels. Biopharmaceuticals carve out a distinct and fast-growing niche due to the need for labels that withstand extreme cold chain storage without adhesive failure. Medical devices demand sterility-compatible labels that endure autoclaving, gamma radiation, or ETO sterilization, while nutraceuticals leverage labelling as a marketing asset to drive consumer trust. Clinical trial labelling remains a specialized but high-margin niche requiring customized, protocol-specific labelling with blind codes and rapid turnaround. Together, these dynamics show that regulatory intensity and patient safety keep prescription drugs at the core of labelling demand, while biologics and clinical trials drive innovation in specialty label formats.

United States Pharmaceutical Labelling Market Driven by FDA Regulations and Smart Packaging Integration

The United States pharmaceutical labelling market is undergoing significant transformation under the Food and Drug Administration’s (FDA) 2025 regulations aimed at improving patient medication information (PMI) and overall health literacy. These rules mandate stricter typography standards, including minimum font sizes and contrast ratios, to improve readability and patient safety. A major shift is the Drug Supply Chain Security Act (DSCSA) requirement for GS1 DataMatrix and Code 128 barcodes on all prescription drug labels, which strengthens traceability and anti-counterfeiting compliance.

Pharmaceutical companies are increasingly investing in smart labels with NFC tags and QR codes, allowing patients to access dosage reminders, product authenticity details, and support resources through smartphones. Advanced verification technologies now scan prescription labels before dispensing, reducing medication error risks. Additionally, AI-driven monitoring systems such as those at Gilead Sciences’ new manufacturing hub are enhancing real-time digital quality control. These innovations highlight the U.S. as a leader in digital and patient-centric pharmaceutical labelling solutions.

European Union Pharmaceutical Labelling Market Influenced by FMD and PPWR Regulations

The European Union pharmaceutical labelling market is primarily shaped by the Falsified Medicines Directive (FMD), which mandates serialization of all prescription drugs through unique 2D barcodes and tamper-evident seals. This regulation continues to drive innovation in anti-counterfeiting measures, with manufacturers incorporating holographic elements, invisible inks, and multi-layer security features into pharmaceutical labels.

The Packaging and Packaging Waste Regulation (PPWR), effective from August 2026, introduces PFAS restrictions, influencing materials used in pharmaceutical labeling. Companies are also adopting digitally accessible patient information leaflets (PILs) to complement physical labels, ensuring patients receive up-to-date information. Accessibility requirements, including braille labels and multi-language packaging, are expanding across pan-European markets. The European Medicines Agency (EMA) enforces strict oversight of labelling changes, making Europe a hub for regulatory-compliant and technologically advanced pharmaceutical labelling solutions.

China Pharmaceutical Labelling Market Strengthened by NMPA and Serialization Adoption

The China pharmaceutical labelling market is regulated by the National Medical Products Administration (NMPA), which updated its Good Manufacturing Practice (GMP) annexes in June 2025. These updates require pharmaceutical packaging manufacturers to establish robust quality management systems and collaborate closely with marketing authorization holders (MAHs) during audits. The Center for Drug Evaluation (CDE) further tightened biosimilar labelling requirements in February 2025, mandating direct comparability data and prohibiting indication extrapolation without clinical studies.

China is rapidly adopting serialization and 2D DataMatrix codes to ensure supply chain transparency and reduce counterfeiting risks. The market emphasizes tamper-evident and child-resistant labelling features, aligning with global safety standards. With its fast-growing domestic pharmaceutical industry and strong regulatory oversight, China is positioning itself as a leader in secure, traceable, and compliant pharmaceutical labelling practices.

United Kingdom Pharmaceutical Labelling Market Transformed by Post-Brexit Regulations

The United Kingdom pharmaceutical labelling market has introduced new regulatory requirements as part of the Windsor Framework, mandating that all medicines carry a clearly legible “UK Only” label from January 1, 2025. By June 30, 2025, this label must be printed directly on packaging, ending the use of stickers. Unlike the EU, the UK has disapplied the Falsified Medicines Directive (FMD), creating demand for UK-specific traceability systems.

The Medicines and Healthcare products Regulatory Agency (MHRA) enforces requirements for minimum 7-point font size and easily understandable labelling, improving readability. The market is shifting toward digital tracking systems to safeguard supply chain integrity. These regulatory adjustments, combined with consumer safety priorities, make the UK an emerging market for innovative, compliance-focused pharmaceutical labelling solutions.

India Pharmaceutical Labelling Market Strengthened by CDSCO and Make in India Initiatives

The India pharmaceutical labelling market is regulated by the Central Drugs Standard Control Organization (CDSCO), which has mandated QR codes on secondary and tertiary drug packaging to combat counterfeit medicines. Guidelines also address common errors such as incorrect expiry formats and unreadable font sizes, raising the bar for patient safety. With India recognized as the “pharmacy of the world”, supplying over 50% of global vaccine demand, strong labelling practices are vital for both exports and domestic markets.

The Make in India initiative is supporting local manufacturers to develop security labels and tamper-evident solutions, ensuring quality and global competitiveness. As India’s middle class grows and OTC products gain popularity, demand for innovative, traceable, and regulatory-compliant labelling systems is surging. This regulatory-driven transformation is positioning India as a key global hub for pharmaceutical labelling innovation and manufacturing.

Japan Pharmaceutical Labelling Market Pioneering Digital Transformation with E-Labels

The Japan pharmaceutical labelling market is pioneering with the e-labelling system introduced under the Act on Securing Quality, Efficacy, and Safety of Products, phasing out traditional paper inserts. Patients and healthcare professionals can now access the most updated product information via a GS1 barcode linked to the Pharmaceuticals and Medical Devices Agency (PMDA) database. This digital-first approach enhances information accessibility, accuracy, and regulatory compliance.

Japan is also driving innovation in smart pharmaceutical labels capable of monitoring patient adherence and real-time medication tracking. The country’s strong regulatory oversight emphasizes tamper-evident and high-security labels for vials and bottles. In parallel, government incentives are encouraging the adoption of sustainable labelling materials, making Japan a leader in digital, smart, and eco-friendly pharmaceutical labelling systems.

Pharmaceutical Labelling Market Report Scope

Pharmaceutical Labelling Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.4 Billion

|

|

Market Size (2034)

|

$10.3 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Label Type (Pressure-Sensitive, Shrink Sleeve, Wrap-around, In-mold, Others), By Product Type (Blister Pack Labels, Bottle Labels, Vial & Ampoule Labels, Syringe Labels, Sachet Labels, Box & Carton Labels), By Material (Paper, Plastic, Metalized Films, Others), By Application (Prescription Drugs, OTC Drugs, Biopharmaceuticals, Medical Devices, Clinical Trials, Nutraceuticals), By Functionality (Barcodes & Serialization, Anti-Counterfeit, Temperature-Sensitive, Extended Content Labels, Braille & Tactile, RFID Labels)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Avery Dennison Corporation, CCL Industries Inc., 3M Company, Schreiner Group GmbH & Co. KG, UPM Raflatac, SATO Holdings Corporation, Resource Label Group, LLC, Consolidated Label Co., Denny Bros Ltd., Multi-Color Corporation, WS Packaging Group, Inc., H.B. Fuller Company, Herma GmbH, The Label Shoppe, Essentra Plc

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Pharmaceutical Labelling Market Segmentation

By Label Type

- Pressure-Sensitive

- Shrink Sleeve

- Wrap-around

- In-mold

- Others

By Product Type

- Blister Pack Labels

- Bottle Labels

- Vial & Ampoule Labels

- Syringe Labels

- Sachet Labels

- Box & Carton Labels

By Material

- Paper

- Plastic

- Metalized Films

- Others

By Application

- Prescription Drugs

- OTC Drugs

- Biopharmaceuticals

- Medical Devices

- Clinical Trials

- Nutraceuticals

By Functionality

- Barcodes & Serialization

- Anti-Counterfeit

- Temperature-Sensitive

- Extended Content Labels

- Braille & Tactile

- RFID Labels

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Pharmaceutical Labelling Market

- Avery Dennison Corporation

- CCL Industries Inc.

- 3M Company

- Schreiner Group GmbH & Co. KG

- UPM Raflatac

- SATO Holdings Corporation

- Resource Label Group, LLC

- Consolidated Label Co.

- Denny Bros Ltd.

- Multi-Color Corporation

- WS Packaging Group, Inc.

- H.B. Fuller Company

- Herma GmbH

- The Label Shoppe

- Essentra Plc

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive, multi-layered research methodology to deliver accurate and actionable insights into the Pharmaceutical Labelling Market. Our approach integrates primary research, including interviews with labeling manufacturers, pharmaceutical companies, regulatory bodies, and supply chain stakeholders, with secondary research sourced from corporate filings, scientific publications, trade associations, and validated industry databases. Market sizing and CAGR projections are derived using both top-down and bottom-up analyses, accounting for regional adoption trends, label types, materials, and application-specific demand across prescription drugs, biopharmaceuticals, and medical devices. USDAnalytics evaluates technological advancements such as smart labels, e-labeling, NFC/RFID integration, and augmented reality overlays, alongside sustainability innovations in recyclable substrates and eco-friendly adhesives. Regulatory frameworks including FDA, EMA, CDSCO, PMDA, and post-Brexit UK mandates are carefully analyzed to assess their impact on labeling requirements and compliance. Competitive benchmarking focuses on strategic acquisitions, product innovations, and global expansion of leading players. This methodology ensures industry professionals gain a holistic understanding of market dynamics, growth drivers, and emerging opportunities to support strategic decisions in compliance, patient engagement, and supply chain optimization.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.