Packaging Labels Market Size, Growth Forecast, and Key Insights

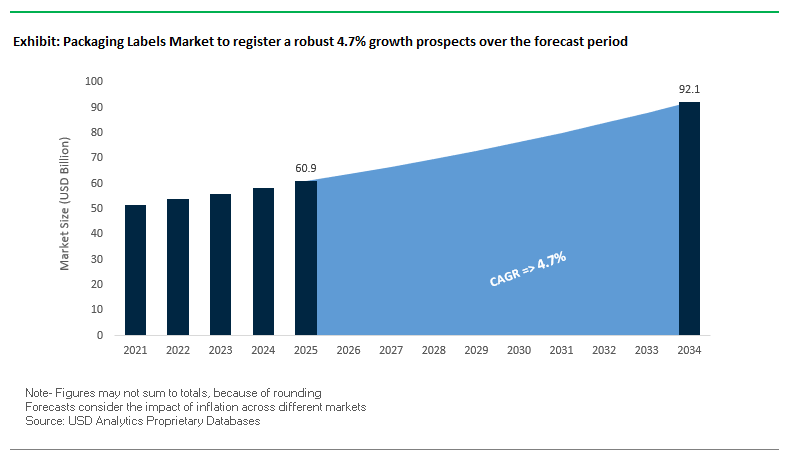

The Global Packaging Labels Market is projected to expand from $60.9 billion in 2025 to $92.1 billion by 2034, representing a CAGR of 4.7%. This market is critical in delivering branding, product information, traceability, and functional solutions across industries such as food and beverage, pharmaceuticals, consumer goods, and logistics. Labels serve not only as a communication medium but also as a tool for consumer engagement, regulatory compliance, and supply chain efficiency.

Key Insights for Industry Stakeholders

- Sustainability Trends: Rising demand for recycled-content labels, bio-based materials, and wash-off solutions facilitates bottle-to-bottle recycling and aligns with corporate ESG objectives.

- Digital Printing and Customization: Advances in digital printing enable small-batch, high-customization label runs, enhancing brand visibility for seasonal promotions and limited editions.

- Smart Labels and Traceability: RFID, QR codes, and other digital identification solutions are increasingly used for anti-counterfeiting, product authentication, and supply chain transparency.

- Interactive and Intelligent Labels: Sensors and freshness indicators enhance consumer trust, reduce waste, and provide actionable usage instructions.

- Regulatory Compliance: Labels play a pivotal role in meeting global food, pharmaceutical, and consumer goods regulations, ensuring safety and legal adherence.

The market is shaped by technological innovation, sustainability initiatives, and growing demand for smart labeling, providing opportunities for advanced and eco-friendly solutions.

Recent Developments Driving the Packaging Labels Market

The Global Packaging Labels Industry has witnessed significant strategic and technological developments, highlighting its focus on sustainability, digitalization, and market consolidation. In August 2025, Avery Dennison announced a $390 million acquisition of Meridian Adhesives Group’s U.S.-based flooring adhesives business, strengthening its specialty adhesives portfolio. In the same month, UPM Adhesive Materials invested in a new state-of-the-art coating line in Johor Bahru, Malaysia, to accelerate growth in Southeast Asia.

In July 2025, UPM Adhesive Materials expanded its production capacity in Mills River, North Carolina, addressing the rising demand for advanced labels. Sun Chemical launched the SunCure Advance ECO UV series for folding carton applications, compatible with various label substrates. In May 2025, Avery Dennison opened a joint venture apparel manufacturing facility in Vietnam, producing apparel and RFID-enabled digital identification products.

Earlier in June 2025, UPM Raflatac was rebranded UPM Adhesive Materials, signaling a strategic shift toward sustainable labeling solutions. In April 2025, the partnership between UPM Raflatac and Mark Andy was renewed to deliver innovative printing solutions in the Americas, marking the sixth consecutive year of collaboration. In March 2025, UPM showcased its Carbon Action plastic label portfolio at Labelexpo Mexico, designed to promote circularity in labeling.

Trends and Opportunities Transforming the Packaging Labels Market

Mandated Adoption of Digital Watermarks for Advanced Recycling Sortation

The packaging labels market is being reshaped by the regulatory and operational success of digital watermarking technology, which has proven its ability to transform recycling efficiency. The HolyGrail 2.0 initiative, led by AIM (European Brands Association), concluded industrial-scale trials in Germany in late 2024. These trials processed nearly 56,000 items daily with over 90% detection efficiency, confirming that digital watermarks work reliably under real-world conditions. More importantly, the system achieved SKU-level sortation, identifying 5,949 product types over 100 days, allowing packaging to be cleanly separated into food-contact and non-food-contact streams. This precision is a game-changer for meeting the European Union’s Packaging and Packaging Waste Regulation (PPWR) requirements for recycled content, as it creates a consistent supply of high-quality recycled material. Major corporations are already transitioning from trials to adoption—P&G, Mondelēz International, and Arla Foods introduced digitally watermarked packaging in German and Danish markets in 2024, signaling that this technology is moving into full-scale commercial use. As regulatory frameworks tighten, digital watermarking labels are poised to become a cornerstone of the circular packaging economy.

Rapid Shift to Wash-Off Adhesives to Facilitate Package Recyclability

The second defining trend is the market-wide adoption of wash-off adhesives in labels, directly driven by the need to improve recycling outcomes for PET and HDPE packaging. Traditional adhesives often contaminate recycling streams, downgrading the value of recovered material. In contrast, wash-off adhesives release labels completely during the hot caustic wash stage, ensuring uncontaminated PET flakes suitable for food-grade applications. For HDPE bottles, companies like TEXYEAR have commercialized acrylic water-based adhesives such as the 230 series, specifically designed for standard wash-off conditions. These technologies ensure cleaner separation and higher-value recycled outputs. Global brands are making this a non-negotiable requirement for their suppliers, pushing adoption throughout the value chain. While unit costs for adhesives may be higher, recyclers benefit from a more valuable end-product that offsets the expense. This balance of compliance, economics, and sustainability is propelling wash-off adhesives from innovation to industry standard across beverage, dairy, and personal care packaging.

Development of Fibre-Based Functional Barriers for Direct Object Printing

A significant growth opportunity exists in fiber-based functional barriers that enable printing directly on paper substrates, eliminating the need for multi-material laminates. Academic and industry research is accelerating innovations in bio-derived and compostable coatings that provide oxygen, grease, and moisture resistance on paper. This development allows for the replacement of polyethylene (PE) liners in applications like cups and corrugated packaging. Companies such as Solenis are already commercializing printing-press applied barrier coatings, enabling converters to integrate functional coatings in-house during flexographic or digital printing, reducing logistical complexity and costs. Research at Clemson University’s Sustainable Packaging Innovation Lab is further advancing the space by using agricultural waste feedstocks to produce compostable adhesives for produce labels, enabling both the label and the produce to be composted together. These solutions not only reduce reliance on plastics but also provide recyclable, compostable, and monomaterial pathways for brand owners. The commercial success of these technologies would directly address one of the largest performance gaps in sustainable packaging.

Expansion of Smart Labels for Perishable Goods Quality Monitoring

The expansion of smart labels represents one of the most transformative opportunities in the packaging labels market, especially for high-value perishable and pharmaceutical supply chains. Time-Temperature Indicators (TTIs) and freshness sensors are being deployed to combat global food waste, offering real-time visual signals of spoilage risk. Research has demonstrated their ability to outperform conservative use-by dates, reducing unnecessary disposal of safe food. In the pharmaceutical sector, TTIs provide a safeguard for vaccines and temperature-sensitive drugs, changing color irreversibly if storage conditions are compromised, thus enhancing patient safety and regulatory compliance. From an economic standpoint, smart labels are cost-effective compared to electronic data loggers, allowing item-level monitoring at scale. Beyond logistics, they also enhance consumer trust, as visible freshness or safety indicators reinforce brand reliability and product transparency. Brands adopting these labels can position themselves as leaders in safety, sustainability, and innovation, turning packaging into a platform for quality assurance and consumer engagement.

Competitive Landscape: Leading Companies Shaping the Packaging Labels Market

The Global Packaging Labels Market is dominated by leading players who leverage materials science, digital printing, and sustainability initiatives to provide innovative, high-performance, and eco-friendly labeling solutions.

Avery Dennison Corporation: Innovating Smart and Sustainable Label Solutions

Avery Dennison is a global leader in pressure-sensitive and functional labeling materials. In August 2025, the company acquired Meridian Adhesives Group’s flooring adhesives business, and in May 2025, it launched a joint venture in Vietnam for RFID and digital identification products. Avery Dennison offers labels for food, beverage, and personal care, alongside atma.io digital solutions connecting physical products to the digital ecosystem. The company focuses on sustainability and innovation, targeting net-zero carbon emissions by 2050.

CCL Industries Inc.: Delivering End-to-End Specialty Label Solutions

CCL Industries is a global leader in specialty packaging, labels, and films, with a diversified portfolio including CCL Label, Avery, and Checkpoint. The company invests in bottle-to-bottle recycling technologies and has pursued bolt-on acquisitions to strengthen its global capabilities. Its offerings include pressure-sensitive labels, shrink sleeves, and in-mould labels, featuring sustainability-focused solutions like EcoStream® and EcoFloat®. CCL’s strategy emphasizes innovative, high-quality specialty packaging with a focus on sustainability and brand protection.

UPM Adhesive Materials: Leading Sustainable Self-Adhesive Labels

UPM Adhesive Materials, formerly UPM Raflatac, specializes in self-adhesive label materials, with a strong emphasis on sustainable paper and film products. In August 2025, it invested in a coating line in Malaysia and expanded U.S. production in North Carolina. Key offerings include RAFNXT+ carbon-reduced labels and other sustainable adhesive solutions. UPM focuses on circular economy principles, creating labels from renewable or recycled materials while enhancing recyclability.

Lintec Corporation: Integrating Core Technologies for High-Performance Labels

Lintec Corporation is a Japanese manufacturer combining adhesive applications, specialty paper, surface improvement, and system development to produce advanced label products. The company aims to increase overseas sales to 50% under its new medium-term plan. Lintec provides adhesive papers, films, and barcode/labeling equipment across industries including food, automotive, and electronics. Its strategy is centered on global expansion, sustainability, and creating innovative solutions.

Fuji Seal International Inc.: Expanding Shrink Sleeve and Eco-Friendly Labeling

Fuji Seal International is a global leader in shrink sleeve and pressure-sensitive labels. The company focuses on overseas expansion and eco-friendly labeling solutions, including RecShrink™ recyclable labels compatible with PET bottles. Fuji Seal offers labels and pouches, supporting food, beverage, and personal care applications. Its strategic emphasis is on recycling-oriented innovation and providing sustainable packaging services aligned with the circular economy.

Packaging Labels Market Share Insights, 2025-2034

Pressure-Sensitive Labels Dominate Market Share by Label Type in the Packaging Labels Industry

Pressure-sensitive labels (PSLs) hold 50% of the global packaging labels market, making them the undisputed leader due to their versatility, compatibility, and ability to integrate advanced smart-label technologies. PSLs can adhere to a wide variety of surfaces including plastic, glass, and metal, enabling their use across industries from water bottles and food jars to pharmaceutical vials and consumer goods. Their high-speed application, cost efficiency, and ability to incorporate features such as QR codes, NFC, holograms, and tamper-evident constructions reinforce their dominance. Shrink sleeves and in-mold labels (IML) are gaining momentum as premium, 360-degree branding formats in beverages and rigid plastics, yet PSLs remain the default choice because they combine branding flexibility, regulatory compliance, and functional durability. Wet-glue labels continue to decline, limited to legacy glass-bottle applications, while RFID-enabled labels in the “Others” category point toward the next wave of track-and-trace and anti-counterfeiting innovation.

Food & Beverage Industry Leads Market Share by End-Use in the Packaging Labels Market

The food and beverage industry consumes 40% of all packaging labels, cementing its role as the largest end-use segment. This dominance is driven by the unparalleled unit volume of packaged products, from ready-to-drink beverages and packaged snacks to frozen foods and condiments. The sector’s reliance on PSLs, shrink sleeves, and wraparound labels stems from the need for compliance-driven prime labels that display nutritional information, barcodes, and regulatory content, while also delivering high-impact branding on crowded retail shelves. Moreover, beverage companies are at the forefront of adopting shrink sleeves for 360-degree graphics and tamper evidence, while food manufacturers increasingly demand recyclable facestocks and inks that align with sustainability mandates and closed-loop recycling streams. Pharmaceutical and healthcare packaging follows as a high-value segment requiring serialization and authentication features, but food and beverage remains the engine of scale and innovation, shaping trends for the entire labels industry.

United States Packaging Labels Market Driven by GS1 Sunrise 2027 and RFID Integration

The United States packaging labels market is undergoing a major transformation with the GS1 Sunrise 2027 Project, which mandates the transition from traditional barcodes to 2D barcodes. This regulatory shift is accelerating the adoption of RFID-enabled smart labels, reshaping label design to accommodate expanded data requirements and support traceability. Alongside this, Extended Producer Responsibility (EPR) laws at the state level are driving packaging converters to increase recyclability and incorporate post-consumer recycled (PCR) content in label materials. These shifts are creating significant opportunities for sustainable label innovation across industries.

Technological advancements such as digital printing and smart labeling are central to market growth. Smart labels with RFID and NFC technology allow real-time tracking across supply chains, while digital printing enables mass customization, shorter runs, and faster response to consumer demands. Corporate initiatives reinforce these changes, with companies like General Mills, Mars, and PepsiCo launching the US Flexible Film Initiative (USFFI) in August 2025 to support scalable recycling of flexible packaging that includes labels. Strong demand is seen in e-commerce and consumer packaged goods (CPG), where automation-ready and data-rich labels ensure efficient last-mile delivery and improved consumer communication.

Germany Packaging Labels Market Strengthened by PPWR and Transparency Regulations

Germany’s packaging labels market is directly shaped by the EU Packaging and Packaging Waste Regulation (PPWR) and the amended German Packaging Act (VerpackG), which mandate higher recyclability and clear labeling standards. These regulations are pushing the adoption of mono-material labels, removable adhesives, and de-inkable inks to ensure effective recycling. In January 2025, new parcel labeling rules also came into effect, requiring special identification for parcels with higher weights on both domestic and international shipments.

Technological innovation is strong, with Germany emerging as a hub for advanced label printing systems that meet high accuracy standards in logistics, pharmaceuticals, and food packaging. New 2025 regulations require more detailed sustainability disclosures on packaging, compelling companies to provide information on material composition, recyclability, and certifications directly on labels. This transparency is key for reducing contamination in recycling streams. Demand is strongest in food, pharmaceuticals, and logistics, where labeling ensures safety compliance, ingredient disclosure, allergen tracking, and full supply chain traceability.

China Packaging Labels Market Shaped by GB 7718-2025 and Digital Labeling Standards

The packaging labels market in China is adapting to GB 7718-2025, a new food labeling standard that will take effect on March 16, 2027. Published by the National Health Commission (NHC) and State Administration for Market Regulation (SAMR), the regulation requires mandatory disclosure of eight allergenic substances, introduces restrictions on claims such as “free of,” and enforces higher standards for clarity and accuracy of labeling. These reforms prioritize consumer protection and food safety.

A major technological advancement under GB 7718 is the acceptance of digital labeling through QR codes and similar technologies, enabling companies to supplement paper-based labels with additional consumer information. Regulations also require high-contrast fonts and minimum sizes to improve legibility of food dates and prohibit misleading claims, addressing consumer safety concerns. With surging demand in consumer goods, e-commerce, and electronics, the Chinese market requires highly efficient, compliant, and cost-effective label production to match its scale of output.

India Packaging Labels Market Supported by PLI Scheme and Digital Printing Expansion

India’s packaging labels market is benefiting from Make in India and the Production Linked Incentive (PLI) scheme, which encourage domestic investment and manufacturing. Regulatory requirements, including EPR rules mandating 30% recycled content in rigid plastics by April 2025, are directly influencing the choice of label substrates and adhesives. These rules are reinforcing the move toward eco-friendly and recyclable label solutions that align with circular economy goals.

Technological innovation is gaining momentum through the adoption of digital printing and embellishment technologies. Demand for mid-web label presses that print across diverse substrates reflects India’s transition beyond traditional pressure-sensitive labels into shrink sleeves, wraparounds, and specialty formats. Corporate sustainability efforts, such as the Huhtamaki Foundation’s “CloseTheLoop” recycling initiative, are also reshaping the labeling industry. With growing demand from food, beverage, and pharmaceuticals, labels are now integral to brand presentation, product safety, and compliance in India’s booming retail and e-commerce ecosystem.

Japan Packaging Labels Market Advanced by Positive List Rules and E-Labeling Expansion

Japan’s packaging labels market is evolving under new food-contact regulations that came into force on June 1, 2025. The positive list system now specifies approved substances for use in food packaging, impacting the design and production of compliant labels. This regulatory shift is fostering the development of eco-friendly adhesives, coatings, and substrates for labels that meet both safety and sustainability requirements.

Japan is also seeing strong momentum in e-labeling technologies. In 2025, QR codes, Unique Device Identifiers (UDIs), and patient-friendly e-label formats gained wider adoption across pharmaceuticals and medical devices. This trend reduces material usage while improving consumer access to critical information. With Japan targeting a 46% reduction in greenhouse gas emissions by 2030, companies are prioritizing sustainable label solutions. Demand is especially high in ready-to-drink beverages, snacks, and consumer goods, where labels balance aesthetic appeal, compliance, and sustainability.

Brazil Packaging Labels Market Driven by ANVISA Warning Labels and PNRS Recycling Mandates

Brazil’s packaging labels market is shaped by ANVISA’s front-of-pack warning label regulation (RDC-429/2020), which became fully enforceable in 2025. This regulation requires clear, prominent labels on foods high in sugar, sodium, or saturated fats, fundamentally altering labeling practices for packaged foods and beverages. Such rules are creating demand for high-contrast, standardized, and consumer-friendly labels that improve transparency and encourage healthier consumer choices.

The market is further influenced by the National Solid Waste Policy (PNRS), which requires companies to recycle up to 50% of their products, affecting both packaging materials and the labels used. Companies are investing in advanced label printing technologies and sustainable substrates to meet these requirements. Demand is concentrated in the food and beverage sector, where Brazil’s strong canned goods industry depends on safe, effective, and compliant labeling. The combination of nutrition disclosure, recycling mandates, and growing consumer awareness is positioning Brazil as a key market for sustainable and regulatory-compliant packaging labels.

Packaging Labels Market Report Scope

Packaging Labels Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$60.9 Billion

|

|

Market Size (2034)

|

$92.1 Billion

|

|

Market Growth Rate

|

4.7%

|

|

Segments

|

By Label Type (Pressure-Sensitive, Shrink Sleeves, In-Mold, Wraparound, Wet-Glue, Others), By Material Type (Paper & Paperboard, Plastic, Metalized Films, Synthetic Materials), By End-Use Industry (Food & Beverage, Personal Care & Cosmetics, Pharmaceutical & Healthcare, Home & Household Care, E-commerce & Logistics, Other Industrial Applications), By Printing Technology (Flexography, Rotogravure, Digital, Offset)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Avery Dennison Corporation, CCL Industries Inc., Multi-Color Corporation, Jindal Films Ltd., UPM Raflatac Oyj, Fuji Seal International, Inc., Lintec Corporation, Sato Holdings Corporation, Coveris Holdings S.A., Huhtamaki Oyj, WS Packaging Group, Inc., Essel Propack, WestRock Company, DS Smith Plc, Amcor plc

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Packaging Labels Market Segmentation

By Label Type

- Pressure-Sensitive

- Shrink Sleeves

- In-Mold

- Wraparound

- Wet-Glue

- Others

By Material Type

- Paper & Paperboard

- Plastic

- Metalized Films

- Synthetic Materials

By End-Use Industry

- Food & Beverage

- Personal Care & Cosmetics

- Pharmaceutical & Healthcare

- Home & Household Care

- E-commerce & Logistics

- Other Industrial Applications

By Printing Technology

- Flexography

- Rotogravure

- Digital

- Offset

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Packaging Labels Market

- Avery Dennison Corporation

- CCL Industries Inc.

- Multi-Color Corporation

- Jindal Films Ltd.

- UPM Raflatac Oyj

- Fuji Seal International, Inc.

- Lintec Corporation

- Sato Holdings Corporation

- Coveris Holdings S.A.

- Huhtamaki Oyj

- WS Packaging Group, Inc.

- Essel Propack

- WestRock Company

- DS Smith Plc

- Amcor plc

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous and integrated research methodology to provide precise insights into the global Packaging Labels Market. Our approach combines primary and secondary research to ensure data accuracy, market relevance, and actionable forecasts. Primary research includes detailed interviews and surveys with key stakeholders such as packaging manufacturers, brand owners, retailers, and material suppliers to capture emerging trends, regulatory impacts, and technological innovations. Secondary research leverages company reports, industry journals, trade publications, and government data to validate market dynamics, growth drivers, and regional developments. USDAnalytics applies quantitative techniques, including CAGR computation, market sizing, and trend projection, spanning from 2025 to 2034, while considering factors such as digital printing, smart labels, sustainable materials, and regulatory compliance. Our analysis also integrates innovations like wash-off adhesives, fiber-based functional barriers, and time-temperature indicator labels, as well as regional legislation in North America, Europe, China, India, Japan, and Brazil. By synthesizing competitive intelligence, market drivers, technological advancements, and regulatory landscapes, USDAnalytics delivers a comprehensive, future-ready view of the packaging labels market, supporting strategic decision-making, investment planning, and product development for industry professionals.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.