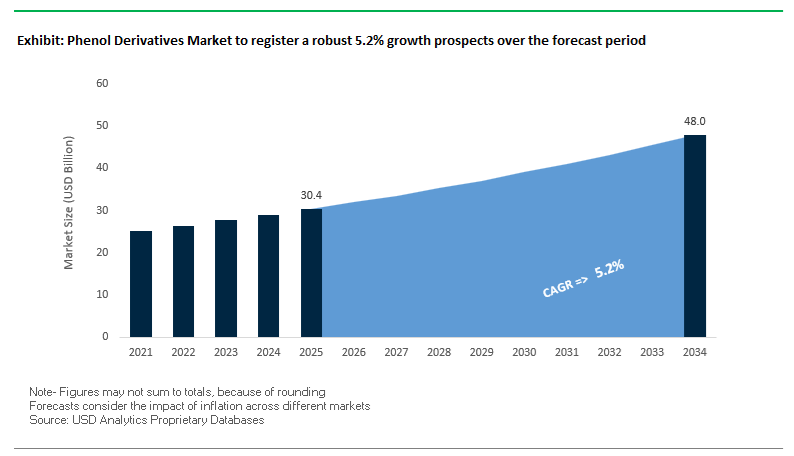

Phenol Derivatives Market Size 2025–2034: $30.4 Billion to $48 Billion at 5.2% CAGR Driven by BPA Expansion, Polycarbonate Integration, and Capacity Realignment

The global phenol derivatives market is projected to grow from $30.4 billion in 2025 to $48 billion by 2034, registering a CAGR of 5.2%. Market expansion is primarily supported by rising demand for bisphenol A (BPA), phenolic resins, caprolactam intermediates, alkylphenols, and acetone-linked derivatives across polycarbonate resins, epoxy systems, automotive components, wind energy blades, and electrical laminates. Phenol derivatives remain critical building blocks in engineering plastics, coatings, adhesives, laminates, and high-performance composites. Structural shifts in regional capacity, forward integration into polycarbonate production, and tightening supply conditions in Asia are reshaping global trade flows and pricing dynamics.

Asia-Pacific remains the epicenter of capacity expansion and integration. In April 2024, KBR signed a technology licensing agreement with SABIC Fujian Petrochemicals for a 250,000-ton-per-annum phenol plant in China, with construction initiated in 2024 and completion targeted for 2026. This project ranks among the largest phenol capacity additions in the region and reinforces integrated phenol-acetone value chains linked to BPA and polycarbonate production. In early January 2026, Asian phenol spot prices surged 14% amid maintenance turnarounds at major Chinese facilities combined with strong downstream BPA demand for wind turbine blade manufacturing. The spike underscores the tight coupling between phenol supply and renewable energy infrastructure growth.

India is accelerating import substitution and downstream integration in the phenol derivatives sector. In June 2025, Deepak Nitrite approved a ₹3,500 crore expansion through Deepak Chem Tech to establish new capacity of 300 KTA phenol and 185 KTA acetone. This strategic investment enables forward integration into polycarbonate resin production, positioning the company as one of India’s most vertically integrated phenol derivative manufacturers. In December 2025, Deepak Chem Tech commissioned a ₹515 crore nitric acid plant, strengthening internal feedstock availability for phenol-based agrochemical and pharmaceutical intermediates. Complementing this expansion, Haldia Petrochemicals signed a license amendment with Lummus Technology in November 2024 to boost capacity at its upcoming phenol and acetone facility in West Bengal, directly targeting India’s reliance on imported phenolic intermediates.

European producers are responding to high energy costs and sustainability mandates through restructuring and efficiency upgrades. In April 2024, Mitsui Chemicals announced closure of its 190,000 tons per year phenol plant at Ichihara by fiscal 2026, reflecting a transition toward higher-margin, sustainable derivatives under its “Basic & Green Materials” strategy. In November 2024, INEOS Phenol initiated process upgrades across European sites to improve phenol yield and reduce carbon intensity, reinforcing operational efficiency amid elevated regional utility costs. CEPSA Química also expanded phenol production capacity in Spain in June 2024 to meet rising demand for high-purity phenol used in Nylon 6 and epoxy resin applications across automotive and construction markets.

Downstream innovation in phenol-based materials is accelerating. In January 2024, Kumho P&B Chemicals launched high-performance phenolic resin grades engineered for electric vehicle battery housings and advanced circuit board laminates, enhancing thermal stability and flame resistance. In July 2025, Shell Lubricants completed acquisition of Raj Petro Specialities in India, expanding its transformer oil and process oil portfolio where phenol-derived antioxidants and stabilizers play a critical performance role. Meanwhile, in March 2025, Shell confirmed a strategic review of its European chemical assets, signaling potential reallocation of capital away from traditional phenol-acetone refinery integration.

Structural Trends and Opportunity Hotspots in the Phenol Derivatives Market

Strategic Realignment Toward Bisphenol-A Alternatives in Consumer and Food-Contact Materials

The phenol derivatives market is entering a compliance-driven transition cycle as regulatory scrutiny around Bisphenol-A intensifies across major consumer markets. The shift away from BPA is no longer a matter of brand positioning or voluntary sustainability commitments. It has become a binding requirement for companies operating in food packaging, consumer plastics, and coated metal applications.

A defining milestone was the enforcement of Regulation (EU) 2024/3190 from January 20, 2025, which bans BPA, its salts, and hazardous bisphenol derivatives in food-contact materials across the European Union. This regulation covers internal can coatings, reusable plastic bottles, and professional kitchenware, effectively removing BPA-based epoxy systems from large segments of the packaging value chain. The ongoing 18-month transition period places a hard compliance deadline of July 20, 2026 for most single-use applications, while limited exemptions for certain vegetable and fish preservation uses extend to July 20, 2028. These timelines are forcing accelerated reformulation programs focused on non-bisphenol phenolic resins, polyester coatings, and alternative cross-linking chemistries.

Regulatory spillover is amplifying the impact. In October 2025, the Food Safety and Standards Authority of India released a draft proposal aligning domestic standards with EU restrictions, targeting BPA in polycarbonate and epoxy packaging. Similar reassessments by the U.S. FDA in mid-2025, particularly around infant nutrition packaging, indicate that global consumer markets are converging toward BPA-free material standards. As a result, demand within the phenol derivatives market is shifting decisively toward BPA substitutes that can match thermal stability, adhesion, and chemical resistance without regulatory exposure.

Onshoring and Vertical Integration for Semiconductor-Grade ECN Resins

Parallel to consumer material reformulation, the electronics and semiconductor sector is driving a structurally different trend within phenol derivatives through the localization of Epoxy Cresol Novolac resin supply. ECN resins are critical inputs for epoxy molding compounds used to encapsulate advanced semiconductor devices, particularly in high-density packaging formats such as Fan-Out Wafer-Level Packaging and System-in-Package architectures supporting 5G and AI workloads.

These advanced applications require ECN resins with ultra-low ionic contamination, high glass-transition temperatures, and stable dielectric performance under elevated thermal loads. As global chipmakers seek to reduce geopolitical and logistics risk, ECN production is increasingly being treated as a strategic material rather than a commodity resin. This has accelerated onshoring and backward integration efforts in key regions.

In India, Haldia Petrochemicals entered a $59 million agreement with Lummus Technology in late 2024 to expand phenol and phenolic resin capacity. The project is designed to reduce import dependency and support India’s emerging semiconductor manufacturing ambitions. Similar localization strategies are visible across Asia, where governments are incentivizing domestic ECN supply to support advanced packaging ecosystems.

At the same time, new semiconductor material standards introduced for 2025 are accelerating the shift toward halogen-free epoxy molding compounds. This “zero-halogen” requirement is increasing R&D intensity for ECN producers, who must now engineer flame retardancy directly into resin backbones rather than relying on brominated additives. While this has raised development costs by an estimated 10–15%, it is also creating a barrier to entry that favors technically advanced phenol derivative suppliers.

Commercialization of Lignin-Derived Phenol for Sustainable Aromatics

One of the most strategically significant opportunities in the phenol derivatives market lies in the decarbonization of phenol itself. The industry is actively exploring routes to replace the traditional cumene process with bio-based pathways, and lignin has emerged as the most viable renewable feedstock for sustainable aromatic chemistry.

By late 2025, pilot-scale Reductive Catalytic Fractionation installations demonstrated the ability to extract phenolic monomers from lignocellulosic biomass at yields approaching theoretical limits. These lignin-derived phenols can function as drop-in replacements for fossil phenol in wood adhesives, insulation materials, and phenolic resins, allowing manufacturers to decarbonize without altering downstream processing infrastructure.

Policy alignment is reinforcing this opportunity. European Commission assessments in 2025 project that the bio-economy could generate up to €2 trillion in economic output and create 1.2 million jobs by 2030, with sustainable aromatics identified as a core growth pillar. This has prompted pulp and paper majors such as UPM and Stora Enso to integrate phenolic extraction into existing biorefinery operations.

Technological progress is also expanding the scope of bio-phenol beyond niche applications. Advances in hydrodeoxygenation catalysis, reported in October 2025, now allow lignin-derived intermediates to be selectively converted into BTX aromatics. This opens a long-term pathway toward a fully bio-based phenol derivative value chain that can serve coatings, resins, and engineering plastics markets at industrial scale.

High-Purity Alkylphenols for Lubricants and Aviation Fuel Additives

A second high-growth opportunity is emerging in specialty alkylphenol derivatives driven by changes in mobility and energy systems. The simultaneous rise of electric vehicles and sustainable aviation fuel mandates is reshaping additive demand in both lubricants and fuels.

In aviation, global SAF production is scaling rapidly to meet blending mandates, moving from approximately 600 million liters in 2023 toward more than 1.3 billion liters during 2024–2025. These synthetic and bio-derived fuels require robust antioxidant and corrosion inhibitor systems to maintain stability in low-aromatic, oxygenated fuel matrices. High-purity alkylphenols are increasingly specified as core building blocks for these additive packages due to their thermal stability and compatibility with non-petroleum fuels.

In the automotive sector, EV adoption is driving demand for new lubricant chemistries rather than eliminating it. Electric drivetrains rely on specialized gear oils and thermal fluids that must deliver both lubrication and electrical insulation. Alkylphenol-based dispersants and viscosity modifiers are being reformulated to improve dielectric performance and moisture resistance, reducing corrosion risk in high-voltage environments.

Fuel additive standards are further reinforcing this niche. In September 2025, BASF announced its next-generation Keropur gasoline performance additive series designed to exceed the new U.S. TOP TIER+ specifications. These formulations leverage advanced alkylphenol chemistry to meet stringent deposit control requirements at lower additive treat rates, highlighting the growing value of high-performance phenol derivatives in regulated fuel markets.

Phenol Derivatives Market Share and Segmentation Insights

Bisphenol A Leads Phenol Derivatives Market as Key Feedstock for Polycarbonate and Epoxy Resin Production

Bisphenol A accounted for 38.60% of the Phenol Derivatives Market by derivative type in 2025, reflecting its central role as a chemical intermediate used in the production of polycarbonate plastics and epoxy resins. These materials are widely used across automotive components, electronic housings, construction materials, and industrial coatings due to their mechanical strength, heat resistance, and transparency. The large-scale consumption of polycarbonate and epoxy materials continues to sustain strong demand for BPA derivatives. In 2025, increasing regulatory scrutiny on BPA in food contact applications is influencing product development strategies, with chemical manufacturers exploring BPA-free alternatives such as BPS, BPF, and bio-based bisphenols while maintaining BPA demand in industrial and non-food contact polymer applications.

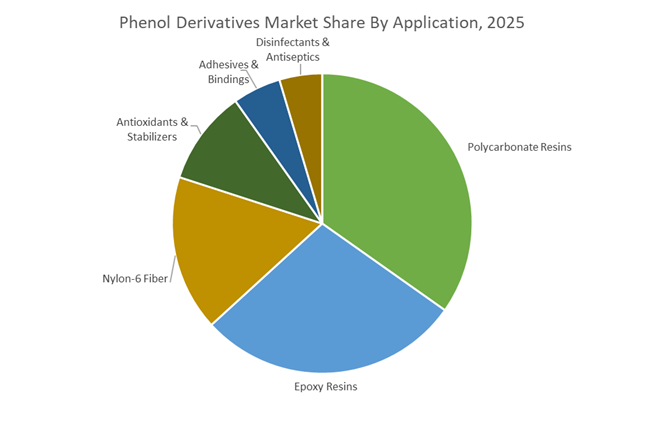

Polycarbonate Resins Segment Drives Phenol Derivative Consumption in High-Performance Engineering Plastics

Polycarbonate resins represented 34.80% of the Phenol Derivatives Market by application in 2025, making them the largest application segment for BPA-based chemical intermediates. Polycarbonate plastics are widely used in automotive lighting systems, electronic device housings, glazing materials, and industrial equipment due to their transparency, impact resistance, and thermal stability. Growing demand for durable engineering plastics continues to support polycarbonate production across multiple manufacturing sectors. In 2025, automotive lightweighting initiatives are increasing the adoption of polycarbonate materials for glazing systems, lighting components, and interior parts where reduced weight and improved design flexibility support vehicle efficiency and integration with advanced driver assistance sensor technologies.

Phenol Derivatives Market Competitive Landscape

The Phenol Derivatives Market is undergoing strategic rationalization, shifting toward high-value products such as BPA and MDI while phasing out inefficient capacity in Europe. Competition is driven by decarbonized cumene-phenol chains, integrated refining complexes in Asia, and rising demand from EV, construction, and advanced materials sectors.

BASF strengthens phenol derivatives leadership through Verbund expansion and cost optimization strategy

BASF SE is reinforcing its position in the phenol derivatives market through its “Winning Ways” strategy and large-scale Verbund integration. The Zhanjiang site in China, fully operational in 2026, supports demand for engineering plastics and downstream phenol derivatives in automotive and electronics. BASF reported €6.6 billion EBITDA in 2025 and targets further earnings growth supported by €2.3 billion cost savings by 2026. The divestment of its decorative paints business enables sharper focus on high-margin industrial chemicals. BASF is also advancing decarbonization through renewable electricity integration across phenol production. This combination of scale, efficiency, and sustainability strengthens its global competitiveness.

INEOS Phenol drives global supply leadership through capacity integration and bio-attributed product innovation

INEOS Phenol remains the largest global producer of phenol and acetone, leveraging scale and operational efficiency. The integration of Mitsui Phenols Singapore added 1 million tonnes of capacity, strengthening supply to ASEAN markets. In response to high European energy costs, the company is restructuring its regional operations to maintain competitiveness. Its INVIRIDIS™ bio-attributed phenol line supports downstream manufacturers seeking lower carbon footprints via mass balance approaches. The Marl cumene facility continues to deliver efficiency gains with significantly reduced CO2 emissions. This combination of global scale and sustainability innovation reinforces INEOS’s leadership position.

Mitsui Chemicals pivots to high-margin derivatives with phenol plant closure and MDI capacity expansion

Mitsui Chemicals is transitioning away from commodity phenol production toward high-value derivatives and green materials. The planned closure of its Ichihara phenol plant by 2026 marks a strategic exit from low-margin operations. Simultaneously, the expansion of MDI capacity at the Yeosu plant will increase output to 710,000 tons/year by 2027. The company is focusing on flame-retardant insulation and automotive applications, where demand remains strong. Mitsui is also investing in bio-based feedstocks and chemical recycling to support its green transformation strategy. This shift toward specialty derivatives enhances profitability and long-term competitiveness.

SABIC leverages Aramco integration to expand phenol-based polycarbonates for EV and infrastructure markets

SABIC is capitalizing on its integration with Saudi Aramco to strengthen its position in phenol-derived polycarbonates and thermoplastics. The company showcased its MEGAMOLDING™ platform at PlastIndia 2026, enabling large-scale EV battery enclosures and lightweight components. By 2025, SABIC achieved $1.5–$1.8 billion in synergy value, enhancing feedstock security and operational efficiency. Its TRUCIRCLE™ portfolio supports circular economy initiatives and low-carbon materials. SABIC’s strategic focus spans mobility, construction, energy, and healthcare applications. This integration of scale, innovation, and sustainability positions SABIC as a key global player.

Honeywell UOP enables process innovation with advanced phenol technologies and AI-driven optimization platforms

Honeywell UOP plays a critical role as the technology provider shaping the phenol derivatives market. Its acquisition of Johnson Matthey’s Catalyst Technologies business expands its capabilities in refining and petrochemical process solutions. UOP’s Q-Max™ and Phenol 3G technologies enable high-yield, energy-efficient production, as demonstrated by large-scale facilities like Lotte GS Chemical’s Yeosu plant. The company is advancing digitalization through Honeywell Performance+ Services, integrating AI to optimize plant efficiency and reduce waste. Its Ecofining™ process supports the transition to bio-based intermediates. This technology leadership makes Honeywell UOP indispensable to global phenol producers.

China – Import Substitution Anchored in High-End Derivatives and Digital Control

China’s phenol derivatives industry is entering a structurally defensive yet technologically ambitious phase. Under the MIIT’s Work Plan for Steady Growth (2025–2026), the chemical sector is mandated to exceed 5% annual added-value growth, with explicit prioritization of high-end phenol derivatives such as polycarbonate, epoxy resins, and engineering plastics. This policy signal is already translating into tangible trade outcomes. According to Mysteel in November 2025, China’s phenol import dependency is projected to decline to just 1–3% over 2026–2030 as newly added domestic capacities complete ramp-up and stabilize operations. The profitability rebound in downstream derivatives underscores this shift. In May 2025, domestic Bisphenol A gross profits surged 145% year on year, reflecting a tight but recovering electronics-grade resin supply chain aligned with domestic demand.

Operationally, China is coupling capacity growth with systemic digitization. The 2025 “AI + Petrochemicals” initiative is compelling phenol derivative plants to deploy AI-driven process optimization and blockchain-based traceability to meet national efficiency and safety benchmarks. This is particularly visible in Jiangbei New Material Technology Park in Nanjing, where BASF commissioned high-performance dispersant lines in November 2025 to support industrial coatings and polymer applications. These developments indicate that China’s phenol derivatives trajectory is less about volume expansion and more about securing technological self-sufficiency across high-end materials.

India – Capacity Tightness Forcing Accelerated Backward Integration

India’s phenol derivatives market is transitioning from import dependence to structural self-sufficiency, albeit under conditions of capacity strain. CRISIL Intelligence reported in June 2025 that domestic phenol production now accounts for roughly 60% of consumption, with imports from China collapsing from 48% in 2022 to just 4% in 2025. This sharp shift has driven utilization dynamics to an inflection point. Phenol production capacity utilization reached an exceptional 130% in fiscal 2024–2025, signaling acute supply tightness and forcing rapid decisions on debottlenecking and new investments.

The center of gravity in this transformation is the integrated phenol–cumene–BPA complex being scaled by Deepak Phenolics Limited through 2025–2026. This asset is strategically positioned to eliminate India’s reliance on imported polycarbonate feedstocks while serving construction, electronics, and automotive end uses. Demand-side momentum remains robust. Government programs such as Smart Cities Mission and Housing for All are driving double-digit growth in phenol-formaldehyde resins for laminates and plywood. To manage residual risks, Indian port-level chemical committees have also diversified sourcing corridors, facilitating selective imports from Belgium and Brazil to cushion against near-term volatility while domestic capacity additions come online.

France – State-Backed Modernization to Defend Strategic Capacity

France represents a policy-driven model of industrial defense within the European phenol derivatives landscape. In November 2025, INEOS announced a €250 million modernization program at its Lavera industrial site, supported by the French government. The investment is focused on upgrading cracker and derivative units to improve energy efficiency and materially reduce CO₂ emissions, reinforcing Lavera’s role as a strategic anchor for domestic phenol and downstream derivative production.

The French state has explicitly framed the Lavera complex as a symbol of national industrial independence, extending subsidies to protect an estimated 10,000 direct and indirect jobs across the chemical value chain. Sustainability is embedded into this strategy. The 2025 investment roadmap includes a transition toward green electricity for derivative processing, aligning production economics with the EU Carbon Border Adjustment Mechanism. As a result, France is positioning its phenol derivatives sector as policy-protected, decarbonization-aligned, and structurally resilient despite broader European cost pressures.

United States – Regulatory Pressure Redirecting Product Mix

The U.S. phenol derivatives industry is being reshaped more by regulation than by capacity expansion. In March 2025, BASF announced an investment at its Puebla site that directly impacts the North American supply chain by expanding aminic antioxidant capacity. These phenol-derived stabilizers are critical for high-performance lubricants, polymers, and thermal management fluids, particularly in automotive and industrial applications.

At the same time, regulatory constraints are narrowing permissible end uses. Under TSCA, the EPA confirmed that articles containing phenol, isopropylated phosphate (PIP 3:1) will be prohibited from U.S. distribution starting October 31, 2026. This has triggered reformulation efforts across textiles, electronics, and consumer goods. Complementing this, the EPA extended reporting deadlines to May 22, 2026, for manufacturers of 16 critical chemicals, including multiple phenol-based compounds, reinforcing compliance costs. Strategically, U.S. producers are reallocating R&D toward battery-grade electrolytes and lithium salts, where phenol-based stabilizers play a functional role in supporting the domestic EV battery supply chain.

Japan – Portfolio Segmentation and High-Tech Derivative Pivot

Japan’s phenol derivatives industry is undergoing deliberate portfolio segmentation to isolate commodity exposure while accelerating specialty growth. In May 2025, Mitsui Chemicals announced the split of its Basic and Green Materials business, separating commodity phenol production from higher-margin specialty derivatives. This restructuring is designed to improve capital discipline while sharpening focus on advanced applications.

Feedstock optimization is reinforcing this strategy. In December 2025, Idemitsu Kosan and Mitsui Chemicals finalized the consolidation of their Chiba ethylene complexes, securing stable upstream supply for phenol derivative plants. On the application front, Mitsui is leveraging phenol chemistry to develop Diffrar™ optical polymer wafers for AR glasses, signaling a pivot toward semiconductor-adjacent and photonics markets in 2026. Sustainability credentials are also strengthening. As of October 2025, major Japanese sites including Otake have achieved ISCC PLUS certification, enabling biomass-based phenol production via mass balance methods.

Germany – Manufacturing Retrenchment, Innovation Persistence

Germany illustrates the divergence between manufacturing economics and innovation capability in phenol derivatives. In 2025, INEOS confirmed the closure of its phenol and acetone plant in Gladbeck, citing punitive carbon costs and structurally high energy prices. The shutdown resulted in 279 job losses and underscored the erosion of cost competitiveness for bulk phenol production in Germany.

Despite this contraction, Germany remains a global innovation hub for phenol derivative processing technologies. In late 2025, BASF launched its X3D® 3D-printing technology for catalysts, enabling optimized synthesis of phenol derivatives in continuous-flow reactors. This innovation enhances reaction efficiency, reduces waste, and supports smaller-footprint specialty production. Consequently, Germany’s role is shifting away from volume manufacturing toward catalyst development, process intensification, and technology export within the global phenol derivatives ecosystem.

Comparative Snapshot – Phenol Derivatives Industry by Country

Phenol Derivatives Market County Level Snapshot

|

Country

|

Strategic Orientation

|

Primary Driver

|

Structural Character

|

|

China

|

Import substitution and digitization

|

High-end materials, AI-enabled plants

|

Scale with technological control

|

|

India

|

Rapid self-sufficiency under tight capacity

|

Integrated complexes, housing demand

|

Expansion-led, demand constrained

|

|

France

|

State-backed modernization

|

Industrial sovereignty, decarbonization

|

Policy-protected, efficiency focused

|

|

United States

|

Regulatory realignment

|

TSCA compliance, EV materials

|

Compliance-driven portfolio shift

|

|

Japan

|

Specialty transition

|

High-tech polymers, sustainability

|

Margin-focused, technology-led

|

|

Germany

|

Retrenchment with innovation

|

Carbon costs, catalyst R&D

|

Innovation hub, reduced scale

|

Phenol Derivatives Market Report Scope

Phenol Derivatives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$30.4 Billion

|

|

Market Size (2034)

|

$48 Billion

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Derivative Type (Bisphenol A, Phenolic Resins, Caprolactam, Alkyl Phenols, Adipic Acid, Salicylic Acid, Chlorophenols), By Application (Polycarbonate Resins, Epoxy Resins, Nylon-6 Fiber, Antioxidants & Stabilizers, Disinfectants & Antiseptics, Adhesives & Bindings), By End-Use Industry (Automotive & Transportation, Electrical & Electronics, Construction & Infrastructure, Pharmaceuticals & Healthcare, Textiles & Apparel, Energy)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

INEOS Phenol, Mitsui Chemicals Inc., BASF SE, Deepak Phenolics Limited, Sinopec, LG Chem Ltd., SABIC, Covestro AG, Lotte Chemical Corporation, Formosa Chemicals & Fibre Corporation, Hexion Inc., Sumitomo Bakelite Co. Ltd., SI Group Inc., Kumho P&B Chemicals Inc., PTT Phenol Company Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Phenol Derivatives Market Segmentation

By Derivative Type

- Bisphenol A

- Phenolic Resins

- Caprolactam

- Alkyl Phenols

- Adipic Acid

- Salicylic Acid

- Chlorophenols

By Application

- Polycarbonate Resins

- Epoxy Resins

- Nylon-6 Fiber

- Antioxidants & Stabilizers

- Disinfectants & Antiseptics

- Adhesives & Bindings

By End-Use Industry

- Automotive & Transportation

- Electrical & Electronics

- Construction & Infrastructure

- Pharmaceuticals & Healthcare

- Textiles & Apparel

- Energy

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Phenol Derivatives Industry

- INEOS Phenol

- Mitsui Chemicals Inc.

- BASF SE

- Deepak Phenolics Limited

- Sinopec

- LG Chem Ltd.

- SABIC

- Covestro AG

- Lotte Chemical Corporation

- Formosa Chemicals & Fibre Corporation

- Hexion Inc.

- Sumitomo Bakelite Co. Ltd.

- SI Group Inc.

- Kumho P&B Chemicals Inc.

- PTT Phenol Company Limited

*- List not Exhaustive