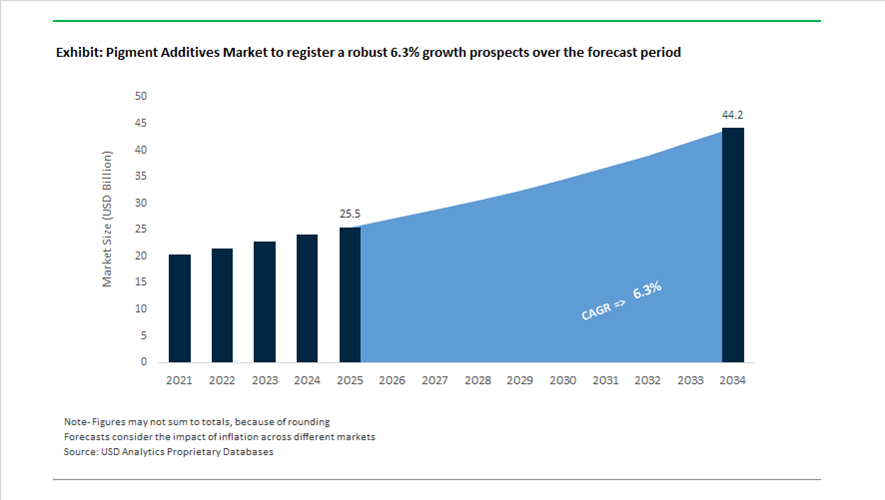

Pigment Additives Market Size 2025–2034: $25.5 Billion to $44.2 Billion at 6.3% CAGR Driven by High-Performance Dispersants, Effect Pigments, and Sustainable Stabilizers

The global pigment additives market is projected to expand from $25.5 billion in 2025 to $44.2 billion by 2034, registering a CAGR of 6.3%. Growth in the pigment dispersants, surface treatment additives, rheology modifiers, stabilizers, and effect pigment enhancers segment is being propelled by rising demand in automotive coatings, architectural paints, plastics, printing inks, cosmetics, and high-performance composites. Pigment additives play a critical role in improving color strength, dispersion stability, gloss retention, UV resistance, and durability, particularly in solvent-based and waterborne coating systems. As OEM automotive finishes, EV battery enclosures, and weather-resistant architectural coatings demand higher aesthetic performance and longevity, advanced pigment additive chemistries are becoming integral to formulation strategies.

Strategic consolidation reshaped the global competitive landscape in 2024 and 2025. In January 2024, Altana acquired the Silberline Group, strengthening its ECKART division in aluminum-based effect pigments and related stabilization additives. In July 2024, Arclin acquired RG Dispersants to integrate naphthalene sulfonate dispersants targeting construction-grade pigment stabilization. The most transformative transaction occurred in March 2025 when Sudarshan Chemical Industries finalized acquisition of Germany’s Heubach Group, creating a global pigment and additive powerhouse with 19 manufacturing sites. This merger significantly enhances R&D scale in high-performance pigment dispersants and specialty additives for automotive coatings and engineered plastics.

Technology-driven differentiation intensified through 2024–2026. In early 2024, BASF commercialized Efka PX 4360, a high-performance dispersing agent engineered for solvent-based industrial coatings, enabling higher pigment loading and improved viscosity control for carbon black and organic pigments. In November 2025, BASF commissioned a new dispersant production line in Nanjing utilizing Controlled Free Radical Polymerization technology, reinforcing supply of advanced additives for high-end automotive and industrial coatings across Asia-Pacific. In February 2026, Sun Chemical introduced Glacier™ Exterior Ceramic White S1303M, featuring synthetic mica-based surface treatment additives delivering improved weather resistance and satin-effect aesthetics for architectural and automotive finishes.

Sustainability and regulatory compliance are becoming central growth drivers in the pigment additives market. Effective January 1, 2025, Sun Chemical implemented a global price increase across its pigment and color materials portfolio, reflecting higher raw material costs and investments in environmental compliance. In 2025, Clariant expanded its Velsan® bio-based stabilizer portfolio, targeting natural pigment compatibility in cosmetics and food-contact packaging applications. In mid-2025, ICL Group demonstrated industrial-scale deployment of Puraloop® recycled phosphorus technology, supporting production of sustainable phosphorus-based intermediates used in fire-retardant pigment additives and stabilizers. These initiatives align with tightening environmental standards and lifecycle carbon reduction mandates across coatings and plastics markets.

Regulatory developments in the United States are also influencing formulation strategies. The U.S. EPA is expected to implement revised risk evaluation rules in 2026 concerning particle size and batch-processing methods for pigments such as PV 29. These changes recognize manufacturing controls that mitigate fine-particle inhalation risks, providing regulatory clarity for pigment additive producers supplying industrial and architectural markets.

Collaborative innovation further accelerated in early 2026 when DIC Corporation and Sun Chemical showcased bio-based polyurethane dispersions and amine-free high-solid resins at Paint India, highlighting reduced VOC and greenhouse gas emissions in automotive and wood coatings. These resin systems require advanced dispersing and stabilization additives optimized for high-solid formulations.

Trends and Opportunities in the Global Pigment Additives Market

Strategic Formulation Shift Toward Functionalized and Multifunctional Pigment Additive Systems

The pigment additives market in 2024–2025 is undergoing a clear structural transition from single-function dispersants and stabilizers toward multifunctional additive systems engineered to deliver multiple performance attributes simultaneously. Coatings, plastics, and construction material manufacturers are increasingly demanding additive packages that combine dispersion stability, corrosion resistance, antimicrobial protection, and thermal regulation within a single formulation. This shift is driven by the need to simplify formulations, reduce processing steps, and meet tightening environmental and performance standards in architectural and automotive applications.

A prominent example of this trend emerged in July 2025, when Sun Chemical Performance Pigments introduced Sunbrite Yellow 74 for architectural coatings. The product integrates a tailored additive package that delivers 15–20% higher tint strength while remaining fully compatible with zero-VOC colorant systems. This formulation reduces the reliance on secondary rheology modifiers and improves batch-to-batch consistency, which is a critical metric for large-scale decorative coatings producers operating under stringent quality control regimes.

Parallel innovation is occurring in the energy-efficiency domain. Rising global cooling costs and urban heat island mitigation policies have accelerated demand for infrared-reflective and thermochromic pigment additives. Industry bulletins from 2025 indicate that smart pigment systems incorporating reflective additives can significantly reduce heat absorption in building envelopes and automotive exteriors, supporting municipal energy-reduction mandates across the EU and North America. In addition, antimicrobial pigment additives have moved from niche to mainstream following heightened post-pandemic hygiene awareness. Silver-based and organic antimicrobial additives are now being integrated into paints, flooring, and HVAC coatings for healthcare and public infrastructure, offering long-term pathogen resistance despite their premium cost profile.

Accelerated Transition Toward Bio-Based and Renewable Pigment Additives

Environmental regulation and brand-driven sustainability targets are fundamentally reshaping additive selection criteria. The EU Packaging and Packaging Waste Regulation and parallel initiatives in North America have elevated bio-based content from a marketing differentiator to a procurement requirement, particularly in packaging, textiles, and consumer goods. As a result, renewable surfactants, dispersants, and wetting agents are replacing petroleum-derived chemistries across pigment additive formulations.

In March 2025, Evonik Coating Additives launched its first mass-balanced solutions for inks and coatings, including TEGO® Wet 270 eCO. These bio-attributed additives enable formulators to reduce product carbon footprints without compromising surface wetting and flow performance in high-speed industrial printing. Similarly, in June 2024, Fine Organic Industries secured USDA Certified Biobased Product labels for its plant-derived oleochemical additives, accelerating their adoption in the U.S. packaging market to meet 2025 sustainability commitments set by major FMCG brand owners.

One of the most disruptive developments occurred in July 2025 with the scale-up of BioBlack, a 100% bio-based pigment dispersion system utilizing carbon-negative additives. Designed as a sustainable alternative to petroleum-derived carbon black, BioBlack aligns with forthcoming EU compostability mandates for packaging labels scheduled for 2028. This transition signals a broader economic realignment in which renewable pigment additives are no longer confined to premium niches but are becoming commercially viable at industrial scale.

Pigment Additives as Enablers of Next-Generation Battery Electrode Manufacturing

The global gigafactory expansion is creating a high-margin growth opportunity for pigment additives tailored to energy storage applications. Lithium-ion and emerging sodium-ion battery production relies on the uniform dispersion of abrasive conductive materials such as carbon black and graphene within electrode slurries. Poor dispersion directly impacts rate capability, cycle life, and energy density, elevating the strategic importance of advanced dispersants and rheology modifiers.

In March 2025, NEI Corporation, in collaboration with HydroGraph Clean Power, launched the NANOMYTE® FGA-1 graphene dispersion series. These additives leverage a proprietary detonation synthesis process to achieve a lower percolation threshold than conventional carbon black, enabling improved electrical conductivity at reduced loading levels. This directly enhances EV battery performance while lowering material costs per kilowatt-hour.

Manufacturing innovation is further amplifying additive demand. In December 2025, Titomic and Rensselaer Polytechnic Institute advanced cold-spray dry-coating technologies aimed at eliminating solvent-based electrode slurries. These processes require specialized pigment and additive systems embedded within metal powders that react during deposition to form submicrometre ceramic phases, improving electrode mechanical integrity without energy-intensive drying steps. Concurrently, impending PFAS restrictions are accelerating R&D into non-PFAS binders and aqueous dispersion additives capable of maintaining chemical stability under high-voltage battery operation, creating a premium opportunity space for specialty additive suppliers.

Pigment Additives Powering Digital Printing for Textiles and Flexible Substrates

Digital printing is rapidly replacing analog dyeing and printing processes across textiles and flexible substrates, driven by customization, reduced water usage, and on-demand manufacturing. This shift depends heavily on pigment additives that deliver wash-fastness, color vibrancy, and soft hand-feel without extensive pre-treatment, particularly on polyester-rich and blended fabrics.

In October 2025, Sun Chemical expanded its digital textile portfolio at ITMA Asia with Xennia Sapphire PT pigment inks. These formulations integrate additive systems compliant with the ZDHC Roadmap to Zero, enabling instant fixation and high color strength on challenging substrates while meeting stringent wastewater and chemical discharge standards. Similarly, the Artistri® P1600 series launched by DuPont in late 2024–2025 redefined the Direct-to-Film segment by incorporating high-performance dispersants that prevent nozzle clogging in industrial printheads, supporting high-speed customization in e-commerce-driven fashion supply chains.

Regional policy support is reinforcing this opportunity. Data from India’s Ministry of Chemicals and Fertilizers in 2024 shows rising capital inflows into domestic textile chemicals, supporting the adoption of pigment-based digital inks that reduce water consumption by up to 90% compared to traditional dyeing. This combination of sustainability mandates, digital manufacturing, and fast fashion economics positions pigment additives as a core enabler of the next phase of textile and flexible substrate printing growth.

Pigment Additives Market Share and Segmentation Insights

Dispersing and Wetting Agents Lead Pigment Additive Demand in High-Performance Coating and Ink Formulations

Dispersing and wetting agents accounted for 34.80% of the Pigment Additives Market by functionality in 2025, reflecting their critical role in pigment dispersion and color performance optimization. These additives break down pigment agglomerates and stabilize pigment particles within liquid formulations, enabling improved color strength, gloss development, and transparency in paints, coatings, and printing inks. Effective dispersion is essential for achieving uniform pigment distribution in high-performance formulations. In 2025, next-generation polymeric dispersants designed for nanoparticle stabilization are gaining importance as pigment manufacturers develop finer particle pigments with higher surface areas that require advanced steric stabilization to prevent flocculation in demanding coating and ink systems.

Paints and Coatings Sector Drives Pigment Additive Consumption in Architectural and Industrial Coatings

Paints and coatings represented 48.60% of the Pigment Additives Market by application in 2025, reflecting the extensive use of pigment additives in architectural paints, automotive coatings, and industrial protective coatings. Pigment additives enable consistent color development, improved dispersion, controlled rheology, and enhanced durability across a wide range of coating formulations. The scale of global coatings production continues to sustain high additive consumption across decorative and industrial segments. In 2025, the shift toward waterborne, high-solids, and bio-based coating technologies is reshaping pigment additive demand, with manufacturers developing dispersants, rheology modifiers, and stabilization additives designed to maintain color performance and formulation stability in environmentally responsible coating systems.

Pigment Additives Market Competitive Landscape

The global pigment additives market is transitioning toward specialty, sustainability-driven solutions, including bio-based dispersants, EV battery additives, and recycled plastic compatibility enhancers. Competitive dynamics are shaped by high-margin product innovation, circular economy alignment, and advanced formulation technologies across coatings, inks, plastics, and personal care.

BYK Advances Circular Additives and Digital Formulation Platforms for High-Performance Coatings

BYK (ALTANA Group) leads the pigment additives market with a focus on high-performance dispersants and circular economy solutions. The March 2026 launch of SCONA additives enhances compatibility in recycled polypropylene (PP) and mixed polymer streams for automotive applications. The August 2025 establishment of BYK do Brasil strengthens localized technical service and coatings market penetration in South America. A global price increase of 5.2% in February 2026 reflects raw material cost pressures and investment in CO₂-neutral production. The BYK account platform enables digital formulation support, offering real-time regulatory data and digital twin capabilities for coatings and inks. Product strategy integrates sustainability, digitalization, and high-performance additive chemistry.

Evonik Expands High-Margin Dispersants with Focus on UV-Cured Systems and Advanced Industrial Applications

Evonik Industries AG is strengthening its position in pigment additives through innovation in hyperdispersants and specialty coating additives. The January 2026 launch of TEGO® Dispers 695 introduces a solvent-free, 100% active dispersant designed for radiation-curing and solvent-borne PU inks, improving pigment stabilization and reducing grinding time. The company reported €14.1 billion in 2025 sales, with €5.5 billion generated from its Custom Solutions segment despite a 4% volume decline. A streamlined North American distribution network announced in May 2026 enhances technical support and market reach. Strategic focus includes achieving 11% ROCE through high-performance additives for 3D printing, membrane technologies, and advanced coatings. Portfolio development emphasizes high-value, application-specific dispersants.

Clariant Strengthens Bio-Based Additives Portfolio with Focus on Low-Carbon and Energy Transition Applications

Clariant AG is repositioning as a pure-play specialty chemicals company centered on sustainable pigment additives and functional materials. The company reported a 17.8% EBITDA margin in FY2025, supported by its Performance Improvement Program delivering CHF 50 million in savings. Divestment of its pigments business enables concentration on high-growth additive segments such as lithium purification and renewable diesel processing. The EcoTain® label highlights products meeting stringent lifecycle sustainability standards, supported by a top-tier EcoVadis rating in 2026. Capacity expansion in China and the Middle East aligns with regional petrochemical and sustainable fuel demand. Strategy focuses on bio-based additives, low-carbon chemistry, and high-margin specialty solutions.

DIC Integrates Pigments and Additives for High-Value Color Solutions Across Electronics and Beauty Applications

DIC Corporation, through Sun Chemical, combines pigment manufacturing with additive technologies to deliver integrated color solutions. The July 2025 launch of Chione™ Electric Amber SB90D introduces a synthetic mica-based pigment with high chromaticity, UV stability, and non-bleeding performance for cosmetics and sun care. Expansion in India, highlighted by participation in PAINTINDIA 2026, targets coatings and automotive demand growth. Integration of BASF’s Colors & Effects business enhances capabilities in inorganic and effect pigments combined with proprietary additive systems. The company provides turnkey solutions for LCD and OLED color filters through vertical integration of pigments and resins. Product development focuses on precision color performance and application-specific additive compatibility.

Elementis Expands Specialty Rheology and Pigment Stabilizers with Focus on Personal Care and Sustainable Coatings

Elementis plc is advancing its transformation into a high-margin specialty additives company under the “Elevate Elementis” strategy. The company reported a 21.2% adjusted operating margin in 2025, with the Personal Care division achieving 32.4% margins driven by premium cosmetic additives. The divestiture of its pharmaceutical manufacturing business in Q2 2026 for approximately $40 million sharpens focus on coatings and personal care segments. Capacity expansion at the St. Louis facility increased production of rheology modifiers and pigment dispersants by 20% since H1 2025. The acquisition of Alchemy Ingredients enhances its portfolio of natural-based additives for clean beauty and sustainable coatings. Product strategy emphasizes rheology control, pigment stabilization, and bio-based additive innovation.

India – Consolidation-Led Global Scale with Regulatory Hardening

India has moved decisively from a fragmented pigment additives base to a globally integrated platform, driven by acquisition-led scale and policy-backed manufacturing depth. The March 2025 acquisition of the Heubach Group by Sudarshan Chemical Industries structurally repositioned India as a global pigment additives supplier, bringing 19 manufacturing sites across Europe, the Americas, and Asia under a single operating umbrella. This transaction is not merely capacity-driven but strategically expands India’s access to high-performance dispersants, stabilizers, and surface-treated pigments used in automotive coatings, industrial inks, and specialty plastics. Parallel to this, outward investment momentum accelerated when Aditya Birla Group acquired Cargill’s specialty chemicals facility in Georgia, strengthening India’s footprint in the North American pigment additives ecosystem.

Domestically, structural enablers are reinforcing competitiveness. Under the Union Budget 2025–2026, substantial allocations to the chemicals ministry have prioritized sunrise segments such as specialty additives for coatings and advanced materials. The rollout of Quality Control Orders in February 2025 for more than 150 chemical products has raised the compliance threshold, effectively filtering low-grade imports and improving pricing power for certified pigment additive producers. At the same time, India’s specialty chemicals segment, including pigment dispersants and stabilizers, has experienced high-teens revenue growth driven by construction, automotive, and packaging demand. The creation of port-linked chemical hubs under the NITI Aayog roadmap further improves export logistics, positioning India as a structurally reliable supplier rather than a cost-only alternative.

China – Regulatory Tightening Reshaping Additive Chemistry

China’s pigment additives industry is undergoing a material reset driven by food-contact safety rules and emissions transparency. The revised GB 4806.10-2025 standard issued by the National Health Commission in September 2025 significantly expands the list of permitted substances for food-contact coatings, while simultaneously tightening migration limits. The introduction of a near-zero detection threshold for Primary Aromatic Amines has forced rapid reformulation of azo-based pigment additives, accelerating substitution toward low-migration dispersants and surface-treated pigments. This regulatory shift is reshaping R&D priorities across ink, packaging, and can-coating value chains.

Environmental compliance is emerging as an equally powerful driver. From January 2026, mandatory real-time VOC monitoring in paint and ink plants is pushing demand toward water-borne and low-VOC dispersing agents. Circularity initiatives are also gaining traction, exemplified by BASF commissioning its loopamid facility in Shanghai in early 2025, integrating advanced pigment additives to preserve color consistency in recycled polyamide textiles. At the upstream level, China’s industrial policy continues to prioritize ultra-high-purity reagents under the 2025–2026 stabilization plan, strengthening domestic supply of electronic-grade pigment additives used in displays and printed electronics.

Germany – Technology-Led Differentiation in High-Value Additives

Germany’s pigment additives industry remains anchored in technology intensity rather than volume leadership. In December 2025, BASF announced a new Ludwigshafen facility scheduled for 2026 that applies X3D catalyst shaping through additive manufacturing. This approach enables precise control over additive particle geometry, improving throughput and consistency in dispersants and stabilizers used in high-performance coatings. BASF’s sustained R&D spend of approximately €2 billion annually underscores Germany’s role as a development hub for next-generation, sustainability-aligned pigment additives.

Specialty effect additives are another defining pillar. ECKART has expanded its portfolio toward mobility-centric applications, including radar-transparent metallic pigment additives that allow autonomous driving sensors to function through coated surfaces. The launch of reduced Product Carbon Footprint aluminum pigment portfolios in late 2025 aligns German suppliers with automotive OEM decarbonization targets. Collectively, Germany’s strategy emphasizes premium performance, regulatory leadership, and application-specific innovation over scale expansion.

Switzerland – Portfolio Optimization and Flame-Retardant Leadership

Switzerland’s pigment additives landscape is characterized by portfolio optimization and leadership in functional additives. Clariant initiated a leadership transition in late 2025 to accelerate integration of high-value cosmetic and performance additive businesses, including Lucas Meyer Cosmetics. Capacity expansion in phosphorus-based flame-retardant additives under the Exolit brand reflects rising demand from e-mobility, electronics, and 5G infrastructure, where thermal stability and compliance with halogen-free standards are critical.

Strategic partnerships further reinforce Switzerland’s innovation role. Clariant’s joint venture with FUHUA finalized in November 2025 focuses on next-generation flame-retardant additives for construction and automotive end uses. In parallel, expansion of the AddWorks portfolio toward bio-based masterbatch additives highlights Switzerland’s emphasis on recyclability and circular plastics, particularly for emerging markets in Latin America and Mexico. This positions Swiss suppliers as solution providers in sustainability-driven pigment additive applications.

United States – Sustainability-Driven Reformulation and Design-Led Demand

In the United States, pigment additives demand is increasingly shaped by sustainability finance and design-led end markets. In July 2025, Sun Chemical introduced Sunbrite Yellow 74, delivering higher tint strength while remaining compatible with VOC-free architectural coatings. Such launches reflect a broader shift toward high-efficiency additives that reduce formulation loadings without compromising color performance.

Regulatory anticipation is influencing capital allocation. US pigment additive producers are increasingly tapping green bonds to fund transitions away from PFAS-based surfactants, ahead of anticipated EPA Sustainable Chemistry guidelines expected in late 2026. Automotive aesthetics remain a strong demand engine, with BASF Coatings unveiling its 2025–2026 color collections built around advanced effect additives for electric vehicles. These trends reinforce the US market’s orientation toward premium applications where sustainability compliance and visual differentiation converge.

Comparative Snapshot – Pigment Additives Industry by Country

Pigment Additives Market County Level Snapshot

|

Country

|

Strategic Orientation

|

2025–2026 Inflection

|

Competitive Position

|

|

India

|

Acquisition-led global scale

|

Heubach integration, QCO enforcement

|

Emerging global consolidator

|

|

China

|

Regulation-driven reformulation

|

Food-contact and VOC mandates

|

High-volume adaptive producer

|

|

Germany

|

Technology and sustainability

|

X3D catalyst shaping, PCF focus

|

Premium innovation hub

|

|

Switzerland

|

Functional additive leadership

|

Flame-retardant and bio-based expansion

|

Specialty solutions leader

|

|

United States

|

Design and sustainability pull

|

PFAS-free shift, EV aesthetics

|

High-value application market

|

Pigment Additives Market Report Scope

Pigment Additives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$25.5 Billion

|

|

Market Size (2034)

|

$44.2 Billion

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Functionality (Dispersing & Wetting Agents, Rheology Modifiers & Thickeners, Light Stabilizers, Defoaming Agents, Leveling & Surface Additives, Flame Retardants, Antimicrobial Additives), By Formulation (Water-Based, Solvent-Based, Powder-Based, Radiation-Curable), By Pigment Type (Organic Pigment Additives, Inorganic Pigment Additives, Effect Pigment Additives), By Application (Paints & Coatings, Plastics & Polymers, Printing Inks, Textiles, Cosmetics & Personal Care)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Clariant AG, Sudarshan Chemical Industries Ltd., Evonik Industries AG, Altana AG, Sun Chemical Corporation, Lanxess AG, Huntsman Corporation, Croda International Plc, Lubrizol Corporation, Aditya Birla Group, Heubach Group, Solvay SA, Arkema SA, Dover Chemical Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Pigment Additives Market Segmentation

By Functionality

- Dispersing & Wetting Agents

- Rheology Modifiers & Thickeners

- Light Stabilizers

- Defoaming Agents

- Leveling & Surface Additives

- Flame Retardants

- Antimicrobial Additives

By Formulation

- Water-Based

- Solvent-Based

- Powder-Based

- Radiation-Curable

By Pigment Type

- Organic Pigment Additives

- Inorganic Pigment Additives

- Effect Pigment Additives

By Application

- Paints & Coatings

- Plastics & Polymers

- Printing Inks

- Textiles

- Cosmetics & Personal Care

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Pigment Additives Industry

- BASF SE

- Clariant AG

- Sudarshan Chemical Industries Ltd.

- Evonik Industries AG

- Altana AG

- Sun Chemical Corporation

- Lanxess AG

- Huntsman Corporation

- Croda International Plc

- Lubrizol Corporation

- Aditya Birla Group

- Heubach Group

- Solvay SA

- Arkema SA

- Dover Chemical Corporation

*- List not Exhaustive