Plastic Bags and Sacks Market Size, Overview, and Growth Outlook (2025–2034)

Plastic Bags and Sacks Market Poised for Growth Amid Rising Retail and Consumer Demand

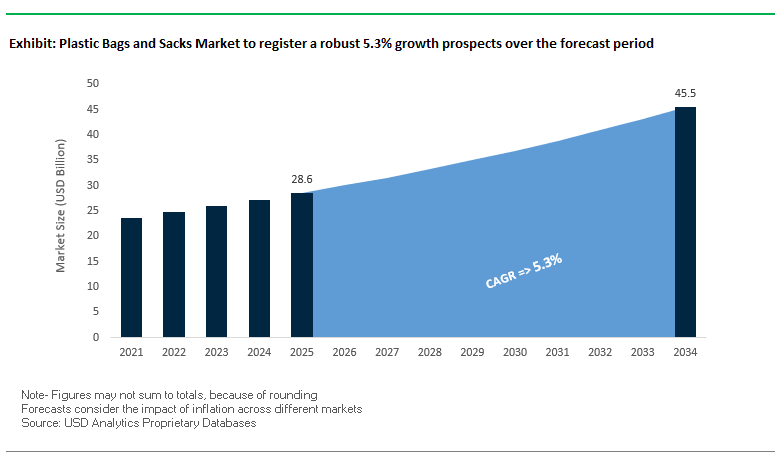

The global plastic bags and sacks market is projected to grow from $28.6 billion in 2025 to $45.5 billion by 2034, achieving a CAGR of 5.3%. Driven primarily by the retail and consumer sectors, the industry continues to expand as businesses seek cost-effective, durable, and versatile packaging solutions. The market remains dominated by T-shirt bags, widely used for groceries, apparel, and consumer goods due to their convenience, affordability, and adaptability.

Key Insights for industry professionals and packaging buyers:

- Retail and Consumer Segments Drive Market Expansion: Over two-thirds of demand originates from retail and consumer applications, highlighting the sector’s pivotal role in shaping market trends.

- T-shirt Bags Remain a Core Product Segment: Their widespread adoption underscores continued reliance on traditional polyethylene-based products for daily packaging needs.

- Sustainable Alternatives Gain Momentum: Biodegradable plastics like polylactic acid (PLA) and starch blends represent the fastest-growing segment, driven by regulatory pressures and increasing consumer preference for eco-friendly packaging.

- Critical Role in Food Safety: Moisture-barrier and durability properties of plastic bags help maintain product freshness, prevent contamination, and reduce spoilage in the food and beverage industry.

- Innovation and Circular Economy Integration: Companies are increasingly investing in recyclable, reusable, and high-performance materials to meet evolving sustainability standards.

Market Analysis: Plastic Bags and Sacks Industry Sees Strategic Collaborations and Sustainable Innovation

The plastic bags and sacks market has been shaped by a series of strategic initiatives, mergers, and sustainable innovations. In September 2025, Siegwerk participated in a flexible packaging summit to showcase circular packaging solutions, emphasizing sustainable applications for plastic bags. Similarly, in August 2025, Mondi launched its FunctionalBarrier Paper Ultimate, an ultra-high barrier paper alternative, putting competitive pressure on conventional plastics.

Corporate consolidation and cross-industry collaborations are reshaping the competitive landscape. In July 2025, Smurfit Kappa and WestRock merged to form Smurfit WestRock, strengthening their global footprint and providing alternative fiber-based solutions to the plastic bags sector. Amcor and Cofigeo, in June 2025, collaborated to introduce a monomaterial polypropylene tray, reflecting a broader trend toward sustainable, single-material packaging.

The industry’s focus on sustainable solutions continues to accelerate. In May 2025, Ball Corporation and Açaí Motion launched a sustainable aluminum drink can, signaling growing adoption of alternatives to plastic. Novolex expanded its reusable shopping bag program in April 2025, meeting consumer demand for eco-conscious packaging. Additionally, in March 2025, Constantia Flexibles acquired Aluflexpack, increasing its presence in flexible packaging for food, beverage, and pharma applications, while in February 2025, Berry Global partnered with Mars to transition candy pantry jars to 100% recycled plastic, highlighting the shift to recycled content.

Transformative Trends and Emerging Opportunities in the Plastic Bags and Sacks Market

Accelerated Regulatory Phase-Out of Single-Use and Lightweight Plastic Bags

The global plastic bags and sacks market is undergoing a structural shift as policymakers accelerate bans and restrictions on single-use plastics. A 2024 global analysis confirmed that 127 countries have now implemented some form of legislation on plastic bags, with 27 countries enforcing outright bans and 30 imposing consumer-facing fees. This regulatory momentum marks a sharp increase compared to 2019, when public policies targeting plastic bags had merely tripled within a decade. Europe has been at the forefront with the EU’s Single-Use Plastics Directive (SUPD), which sets ambitious reduction targets—50% per capita reduction by 2025 and 65% by 2026 relative to 2010 levels. Member states are achieving results through aggressive taxation and fees: Sweden, for example, reported a 75% reduction in single-use bag consumption between 2020 and 2021 after implementing a national bag tax. In the United States, regulatory action is similarly intensifying. By March 2025, 19 states had jurisdiction-wide bans on single-use plastics, and California’s updated legislation, effective January 2026, goes further by banning thicker-gauge plastic bags previously marketed as “reusable.” This regulatory push is closing loopholes and forcing systemic transitions away from disposable formats, fundamentally reshaping demand patterns across retail, grocery, and consumer goods packaging sectors.

Strategic Pivot Toward Durable, Reusable Plastic Bags and PCR Content

In response to stringent bans and evolving consumer expectations, the plastic bags and sacks industry is pivoting toward durable, reusable alternatives with high post-consumer recycled (PCR) content. Retailers are playing a critical role in this transformation. Walmart, as a founding partner of the “Beyond the Bag” initiative, has pledged to integrate 20% PCR content into its North American private brand packaging by 2025, covering more than 30,000 items. Its next-generation reusable bags are engineered for extended lifespans, supporting dozens to hundreds of shopping trips, directly aligning with durability mandates set by state legislations. IKEA has also taken a bold step by committing to transition all plastics in its product portfolio—including bags, packaging, and household goods—to recycled or renewable sources by 2030. Currently, one-third of its plastic-based products already use these sustainable feedstocks, with recycled PET bottles repurposed into functional products such as kitchen fronts. These corporate strategies underscore how regulatory compliance, sustainability pledges, and customer loyalty are converging to accelerate the adoption of reusable plastic bags and PCR-based solutions.

Development of High-Performance Polymer-Lined Paper Sacks

The demand for sustainable alternatives has unlocked significant opportunities in hybrid materials, particularly polymer-lined paper sacks for high-barrier applications. Mondi is spearheading this innovation with its €16 million investment into producing FunctionalBarrier Paper Ultimate, a next-generation solution combining recyclable paper substrates with minimal functional plastic liners. Internal assessments highlight that this barrier paper reduces CO₂ emissions substantially compared to conventional multi-layer plastic or aluminum-based formats, while still delivering strong protection against oxygen and water vapor. In collaboration with construction industry partners, Mondi also developed paper-based sacks that use 60% less plastic compared to conventional humidity-resistant bags. These solutions are particularly impactful for packaging cement and powder-based products, where barrier performance is critical. By reducing reliance on plastics while retaining protective properties, polymer-lined paper sacks represent a scalable and commercially viable pathway for industries such as food, construction, and agriculture to lower plastic consumption while ensuring product integrity.

Expansion of Chemical Recycling for Flexible Plastic Waste Streams

Another high-impact opportunity lies in chemical recycling, which is gaining momentum as a complementary solution to mechanical recycling for hard-to-process flexible plastics. Industry association Plastics Europe reports a significant rise in chemical recycling investments—from €2.6 billion in 2025 to €8 billion projected by 2030. These facilities are expected to deliver 2.8 million tons of recycled output annually by 2030, with pyrolysis technologies accounting for nearly 80% of installed capacity. A prime example is the SABIC–Plastic Energy joint venture in the Netherlands, which produced its first commercial batch of “TACOIL” on September 1, 2025. Derived from mixed post-consumer plastic waste, this feedstock serves as a direct substitute for virgin naphtha, enabling the production of high-quality polymers that meet stringent food-contact safety requirements. The plant is set to recycle 20,000 tons of plastic waste annually, directly contributing to the EU’s 2030 recyclability targets. Chemical recycling not only strengthens the supply of virgin-quality PCR materials but also plays a pivotal role in creating a circular economy for polyolefins, positioning it as one of the most transformative opportunities in the plastic bags and sacks market.

Competitive Landscape: Leading Companies Are Driving Innovation and Sustainability in Plastic Bags and Sacks

The global plastic bags and sacks market is led by companies focused on sustainability, product innovation, and high-performance solutions, offering both traditional and eco-conscious alternatives to meet industry demand.

Berry Global Group, Inc.: Championing Recycled Plastic Adoption and Sustainable Packaging Solutions

Berry Global is a leading provider of plastic bags, liners, and flexible films across food, retail, and industrial applications. In February 2025, Berry collaborated with Mars to convert candy pantry jars to 100% recycled plastic, while also receiving recognition for containers using 30% post-consumer recycled content. Berry’s extensive global footprint and broad product portfolio make it a key player in advancing sustainable packaging.

Mondi Group: Driving Circular Economy through Innovative High-Performance Paper and Plastic Alternatives

Mondi, a global leader in paper and flexible packaging, offers plastic bags and sacks with advanced barrier properties. In August 2025, Mondi introduced re/cycle PaperPlus Bag Advanced, reducing HDPE use by up to 60%. The company focuses on fiber-based, recyclable, and high-performance solutions, strengthening its position as a sustainable alternative in the plastic packaging sector.

Novolex: Expanding Global Reach with Reusable and Sustainable Packaging Solutions

Novolex provides plastic and paper bags, as well as specialty packaging products for foodservice, retail, and industrial sectors. In April 2025, the company launched the next phase of its reusable shopping bag program, while a May 2025 plant acquisition in Europe enhanced its global footprint. Novolex also operates two U.S.-based recycling centers, specializing in HDPE film, highlighting its commitment to sustainability.

Amcor plc: Innovating High-Performance Plastic Bags with Sustainability at the Core

Amcor offers flexible and rigid plastic bags with features such as moisture barriers, vivid printing, and reinforced handles. The company’s Catalyst™ program drives collaboration with brands to create sustainable packaging, aiming to make all packaging recyclable or reusable by 2025. Amcor combines high-performance design with eco-conscious materials, addressing both industrial and consumer demands.

Inteplast Group Corporation: Delivering Durable, High-Quality Plastic Bags for Diverse Applications

Inteplast manufactures a wide range of plastic bags and sacks including trash liners, produce bags, and reclosable storage solutions. The company emphasizes high-quality resins and advanced manufacturing technology, producing durable and versatile products. Notable offerings include Get Reddi storage and freezer bags with dual-zip closures, and high-density commercial trash can liners, catering to food storage, waste management, and industrial needs.

Plastic Bags and Sacks Market Share Insights, 2025-2034

Trash Bags & Liners Dominate Market Share by Product Type in the Plastic Bags and Sacks Industry

Trash bags and liners hold the largest share of the plastic bags and sacks market at 28%, cementing their role as the most indispensable product type across household, institutional, and municipal waste management applications. Unlike single-use carry bags, trash liners face minimal regulatory disruption because sanitation requirements make them a non-discretionary commodity. Their demand profile is highly inelastic, driven by rapid urbanization, increasing municipal solid waste volumes, and institutional reliance in healthcare, hospitality, and office environments. T-shirt bags, with 22% share, continue to retain relevance despite global bans due to exemptions for fresh produce and pharmaceuticals and widespread usage in regions with less stringent regulations. Industrial woven sacks and rubble bags remain resilient in agriculture and construction, supported by their strength, reusability, and barrier properties. Gusseted and lay-flat bags provide niche but stable roles in food packaging and protective covering, while shopping bags are in managed decline, offset by thicker reusable formats. The overall segmentation highlights how waste management and industrial durability keep trash bags, liners, and industrial sacks at the core of long-term market resilience, even as consumer-facing categories face heavy legislative pressure.

Retail & Consumer Goods Lead Market Share by Application in the Plastic Bags and Sacks Industry

The retail and consumer goods sector accounts for 30% of plastic bags and sacks demand, making it the largest application segment despite being the most disrupted by regulation. Growth is now concentrated in durable and reusable plastic bags, in-store specialty packaging, and exempt categories such as produce, bakery, and meat bags. The industrial segment follows closely, maintaining a stable position by serving agriculture, construction, and chemicals, where the functional need for strength and durability outweighs consumer-led environmental concerns. Waste management remains the non-discretionary core, underpinning demand for trash liners in households, municipalities, and institutions, and sustaining long-term volumes despite sustainability debates. Food and beverage packaging leverages barrier properties to preserve freshness, especially for frozen and processed products, while institutional use focuses on specialized liners for healthcare, hospitality, and biohazard waste. The segment split demonstrates how regulatory headwinds reshape retail applications, while industrial, waste management, and food packaging applications remain structurally resilient and critical to the market’s stability.

United States Plastic Bags and Sacks Market Influenced by DSCSA and State-Level Bans

The United States plastic bags and sacks market is undergoing rapid transformation, driven by both federal compliance requirements and state-level bans. The Drug Supply Chain Security Act (DSCSA) is a critical factor, mandating advanced serialization and tracking on packaging, including sacks and bags for pharmaceutical and healthcare logistics. This is pushing manufacturers toward smarter packaging systems that integrate barcodes and RFID for improved traceability. At the same time, the U.S. Department of Agriculture (USDA) enforces strict guidelines for food-grade bags and sacks, ensuring contamination-free packaging for food safety.

Sustainability policies are reshaping the landscape, with California’s 2024 single-use carryout bag ban set to take full effect in January 2026, allowing only recycled paper or certified reusable plastic bags. Similarly, Washington’s ESHB 1293 regulation increases charges on plastic carryout bags to 12 cents from 2026, creating economic disincentives for single-use plastics. Innovations are focused on high-recycled-content sacks that meet new regulations and appeal to eco-conscious consumers. Additionally, there is growing emphasis on standardized labeling for recyclability and reusability, helping consumers make informed choices while ensuring regulatory compliance.

European Union Plastic Bags and Sacks Market Driven by SUP Directive and Circular Economy Goals

The European Union plastic bags and sacks market is heavily regulated under the EU Directive on Single-Use Plastics (SUP Directive), which sets aggressive consumption reduction targets. By end of 2025, member states must reduce lightweight plastic carrier bag usage to an average of 40 bags per citizen annually, forcing retailers and manufacturers to accelerate the transition toward reusable, recyclable, and compostable alternatives. Countries such as France have already gone beyond EU requirements, banning lightweight plastic bags at points of sale, permitting only compostable bio-based options.

Meanwhile, national-level taxation frameworks such as Italy’s plastics tax (2023) further discourage disposable plastic consumption by applying levies on plastic bags and other short-life packaging formats. In response, companies are investing in durable reusable bags capable of at least 125 uses, and developing mono-material bags that align with recyclability standards. The region’s strong circular economy agenda is also fostering innovations in high-recycled-content plastic bags and sacks, positioning Europe as a leader in sustainable retail and food packaging solutions.

China Plastic Bags and Sacks Market Driven by Bans on Thin Bags and Biodegradable Alternatives

The China plastic bags and sacks market is defined by a strict regulatory framework, particularly the government’s “plastic limit order”, which bans bags thinner than 0.025 mm. To further curb plastic pollution, the government enacted a June 2025 regulation aimed at reducing delivery waste by mandating recycled materials and promoting reusable systems across China’s vast e-commerce sector. Authorities like the National Development and Reform Commission (NDRC) and the Ministry of Ecology and Environment (MEE) are jointly enforcing bans on environmentally harmful plastics and strengthening recycling systems.

China is strongly promoting the use of biodegradable and oxo-degradable plastics as alternatives to conventional single-use plastic bags. With recycling rates already surpassing 30% in 2021, the government is pushing for further progress under its circular economy strategy. The rise of biodegradable plastic bags and sacks is also being supported by large-scale investment in domestic production capacity, ensuring supply meets the needs of retail, e-commerce, and food delivery applications.

India Plastic Bags and Sacks Market Shaped by EPR and Bioplastic Innovations

The India plastic bags and sacks market is governed by the Plastic Waste Management Rules, 2016 (amended 2022), which emphasize Extended Producer Responsibility (EPR). Under this framework, manufacturers and brand owners are legally required to collect, recycle, and responsibly dispose of plastic bags and sacks, ensuring accountability across the supply chain. Campaigns such as Swachh Bharat Abhiyan (Clean India Mission) further promote door-to-door waste segregation and sustainable waste handling practices.

Innovation is flourishing, with startups introducing bioplastics from unconventional sources—for example, a newly patented bioplastic derived from ghee residue highlights India’s ability to convert agricultural waste into eco-friendly alternatives. Funding initiatives, such as investment in Dharaksha Ecosolutions, underscore the rising momentum of sustainable packaging solutions. Additionally, the Food Safety and Standards Authority of India (FSSAI) is consulting stakeholders on food-grade sustainable packaging, promoting a shift toward biodegradable and recyclable bags and sacks. With government backing and a fast-growing middle class, India is emerging as a hub for next-generation sustainable packaging technologies.

United Kingdom Plastic Bags and Sacks Market Supported by Plastic Packaging Tax and Traceability Requirements

The United Kingdom plastic bags and sacks market is guided by the Plastic Packaging Tax (PPT), introduced in April 2022, which applies to plastic packaging with less than 30% recycled content. This tax has been highly effective, with HMRC reporting 51% compliance in 2024–2025, meaning over half of plastic packaging now meets recycled content thresholds. The PPT provides strong financial incentives for companies to adopt recycled plastics in bag and sack production, boosting the circular economy.

While the UK has disapplied the EU’s Falsified Medicines Directive (FMD) post-Brexit, the country continues to enforce strict anti-counterfeiting and traceability requirements, affecting plastic sacks used in pharmaceuticals and logistics. A major trend is the development of single-material recyclable bags, addressing challenges with complex multi-layer formats that are difficult to recycle. With growing consumer demand for eco-friendly retail packaging, the UK market is increasingly aligned with sustainability and compliance-driven packaging innovation.

Canada Plastic Bags and Sacks Market Driven by SUP Prohibition Regulations and Zero-Waste Goals

The Canada plastic bags and sacks market is regulated under the Single-use Plastics Prohibition Regulations (SUPPR), which ban the manufacture, import, and sale of plastic checkout bags and other disposable items. The regulations are part of Canada’s Zero Plastic Waste by 2030 plan, projected to eliminate over 1.3 million tonnes of hard-to-recycle plastic waste and prevent 22,000 tonnes of plastic pollution from entering the environment.

While bans are in place, exceptions exist to ensure accessibility, such as allowing the sale of single-use flexible straws under controlled conditions. To support compliance, the Canadian government provides guidelines for selecting sustainable alternatives, such as compostable plastics made from polylactic acid (PLA) and fiber-based packaging. With nationwide enforcement and consumer awareness, Canada is rapidly transitioning to biodegradable and recyclable sacks, positioning itself as a regional leader in sustainable packaging transformation.

Plastic Bags and Sacks Market Report Scope

Plastic Bags and Sacks Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$28.6 Billion

|

|

Market Size (2034)

|

$45.5 Billion

|

|

Market Growth Rate

|

5.3%

|

|

Segments

|

By Material (HDPE, LDPE, LLDPE, PP, Bio-Degradable Materials, Recycled Content Plastics, Others), By Product Type (T-shirt Bags, Gusseted Bags, Lay-flat Bags, Trash Bags & Liners, Woven Sacks, Rubble Sacks, Shopping Bags, Others), By Application (Retail & Consumer Goods, Food & Beverages, Institutional, Industrial, Waste Management)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Novolex Holdings, LLC, Berry Global, Inc., Amcor plc, Mondi Group, Interplast Group, Sonoco Products Company, Uflex Ltd., Winpak Ltd., Coveris S.A., International Plastics, Inc., Advance Polybag, Inc., Superbag, Ltd., Unistar Plastics Co., Cardia Bioplastics Ltd., Polybags Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Plastic Bags and Sacks Market Segmentation

By Material

- HDPE

- LDPE

- LLDPE

- PP

- Bio-Degradable Materials

- Recycled Content Plastics

- Others

By Product Type

- T-shirt Bags

- Gusseted Bags

- Lay-flat Bags

- Trash Bags & Liners

- Woven Sacks

- Rubble Sacks

- Shopping Bags

- Others

By Application

- Retail & Consumer Goods

- Food & Beverages

- Institutional

- Industrial

- Waste Management

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Plastic Bags and Sacks Market

- Novolex Holdings, LLC

- Berry Global, Inc.

- Amcor plc

- Mondi Group

- Interplast Group

- Sonoco Products Company

- Uflex Ltd.

- Winpak Ltd.

- Coveris S.A.

- International Plastics, Inc.

- Advance Polybag, Inc.

- Superbag, Ltd.

- Unistar Plastics Co.

- Cardia Bioplastics Ltd.

- Polybags Ltd.

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive and structured methodology to deliver precise insights into the Plastic Bags and Sacks Market. Our approach integrates extensive primary research via interviews with key stakeholders, including packaging manufacturers, sustainability experts, retail and industrial buyers, and material innovators. This is complemented by secondary research from regulatory filings, industry reports, patent databases, and verified company disclosures. Market sizing and CAGR calculations are performed using both top-down and bottom-up approaches, examining segmentation by material type, product type, and end-use applications. We analyze emerging trends such as high-performance polymer-lined paper sacks, biodegradable plastics, chemical recycling of flexible plastic waste, and post-consumer recycled (PCR) content adoption. Regional regulatory frameworks—including the EU Single-Use Plastics Directive, UK Plastic Packaging Tax, India’s EPR regulations, China’s thin-plastic bans, and U.S. state-level single-use plastic restrictions—are assessed for their impact on demand and innovation. Competitive benchmarking evaluates strategic mergers, collaborations, and sustainability initiatives by leading companies such as Berry Global, Mondi Group, Novolex, Amcor, and Inteplast Group, providing professionals with actionable intelligence on market dynamics, growth opportunities, and regulatory-driven transformations in plastic bags and sacks.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.