Plastic-Based Water Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Plastic-Based Water Packaging Market Expected to Reach $20.6 Billion by 2034 Driven by PET Dominance and Sustainable Innovations

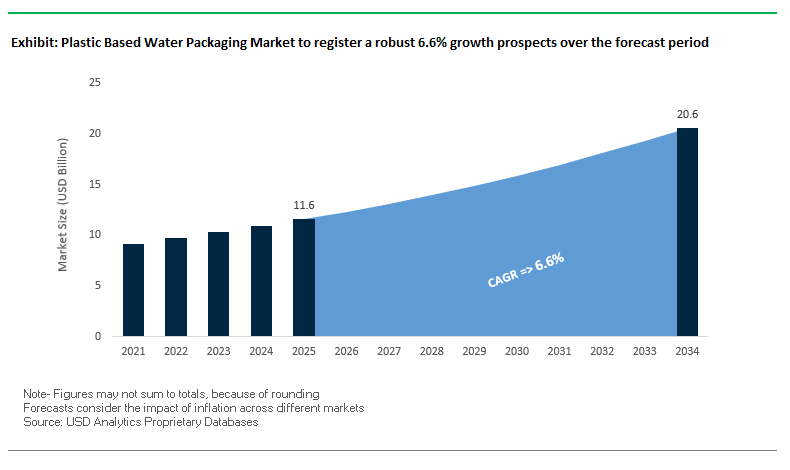

The global plastic-based water packaging market is projected to grow from $11.6 billion in 2025 to $20.6 billion by 2034, representing a CAGR of 6.6%. The market’s expansion is fueled by the dominance of PET bottles, increasing recycled content adoption, and consumer preference for lightweight, convenient, and sustainable packaging. PET’s transparency, durability, and recyclability make it the material of choice for still, sparkling, and flavored water, accounting for the majority of consumption.

Key Insights for industry professionals and buyers:

- PET Remains the Preferred Material: Widely used for its clarity, lightweight, and durability, enabling safe and attractive water packaging.

- Shift to Recycled PET (rPET): Brands are increasingly using 100% recycled PET to minimize environmental impact while maintaining product safety.

- Growing Still Water Consumption: Over 70% of global bottled water consumption is still water, driven by health-conscious consumers and on-the-go convenience.

- Lightweighting as a Sustainability Strategy: Reducing bottle weight lowers material use, transportation costs, and carbon footprint.

- Sustainability Driving Innovation: Nanocoatings, barrier films, and circular economy initiatives are reshaping packaging technology and design.

Market Analysis: Plastic-Based Water Packaging Industry Evolves Through Sustainability, Nanotechnology, and Circular Economy Initiatives

The plastic-based water packaging market has witnessed rapid innovation and strategic collaborations aimed at sustainability. In September 2025, Siegwerk showcased circular packaging innovations at a flexible packaging summit, highlighting sustainable solutions relevant for bottled water. In August 2025, Mondi scaled up FunctionalBarrier Paper Ultimate, a paper-based alternative suitable for water packaging, challenging conventional PET usage.

Industry consolidation and global mergers are also impacting market dynamics. In July 2025, Smurfit Kappa and WestRock merged to form Smurfit WestRock, strengthening competition for plastic water bottles. Sustainability-focused product launches are shaping consumption trends, including The Coca-Cola Company’s 100% recyclable packaging goal by 2025 and Nfinite Nanotechnology’s collaboration with Amcor in April 2025 to enhance oxygen barrier performance in recyclable and compostable packaging.

Innovation is further reflected in material and process breakthroughs. In February 2025, research in Nano Letters demonstrated ultrathin ALD nanocoatings, enhancing barrier properties for PET bottles. PepsiCo’s collaboration with LanzaTech the same month to produce bottled water from captured carbon emissions represents a major step toward a circular economy, integrating sustainability into production and packaging.

Emerging Trends and Growth Opportunities in the Plastic-Based Water Packaging Market

Mandated Integration of Post-Consumer Recycled (PCR) Content in Bottles

Global legislation is creating a regulated and irreversible demand for recycled PET (rPET) in water packaging, transforming material sourcing strategies across the beverage industry. The European Union’s Single-Use Plastics Directive (SUPD) mandates that all single-use PET bottles must contain at least 25% recycled content by January 1, 2025, increasing to 30% by 2030. This creates a legally binding requirement that not only drives adoption of rPET but also reshapes procurement models for beverage brands. Similarly, India’s updated Plastic Waste Management Rules, effective April 2025, require all PET bottles to incorporate a minimum of 30% recycled content. This shift marks a departure from downcycling practices where PET waste was previously redirected into textiles and fibers, instead ensuring circular reuse within food and beverage applications. These mandates are intensifying the competition for food-grade rPET, compelling companies to secure stable supply chains through direct investment and long-term supplier agreements. With governments worldwide tightening recycled content rules, plastic-based water packaging is becoming a frontline battleground for sustainability compliance and material innovation.

Strategic Backward Integration by Beverage Giants into rPET Production

To mitigate supply chain risks and ensure consistent access to high-quality rPET, leading beverage companies are vertically integrating into recycling infrastructure. Coca-Cola HBC set a precedent in January 2025 by opening its first company-owned packaging collection hub in Nigeria, with an expected processing capacity of 13,000 metric tonnes of PET bottles annually. This initiative provides direct control over feedstock quality and availability, reducing reliance on volatile recycling markets. Similarly, Nestlé has expanded its commitment to the circular economy, co-investing nearly $1 billion in Circular Services in the United States, a major developer of recycling infrastructure, to scale up rPET supply. Danone has also embedded circularity into its long-term ESG roadmap, pledging to halve its virgin fossil-based packaging use by 2040, while building in-house rPET production capabilities and co-financing collection systems worldwide. These strategic backward integration initiatives not only strengthen supply security but also align corporate practices with regional EPR (Extended Producer Responsibility) frameworks, positioning beverage leaders as central players in the transition toward a closed-loop plastics economy.

Development of Enhanced Barrier rPET for Sensitive Products

One of the biggest hurdles in scaling rPET for water packaging is its relatively weaker barrier performance compared to virgin PET, which makes it less effective for oxygen-sensitive products like flavored waters and juices. To overcome this, companies are advancing material engineering and coating technologies. In 2025, Eastman partnered with Doloop to unveil a 100% rPET beverage bottle manufactured from chemically recycled PET that matches virgin PET’s mechanical and barrier performance. This breakthrough allows rPET bottles to maintain flavor integrity and extend shelf life, addressing a critical limitation for high-value beverages. Complementary innovations include advanced co-extrusion techniques, such as multi-layer films incorporating a thin EVOH (ethylene vinyl alcohol copolymer) barrier layer within an otherwise recyclable PE or PET structure. Such designs preserve oxygen and CO₂ resistance while remaining fully compatible with recycling streams. These developments underscore a major growth opportunity: commercializing high-performance rPET bottles that combine sustainability with uncompromised product protection.

Design of Lightweight, Connected Packaging for E-commerce and Direct-to-Consumer Channels

The rapid expansion of e-commerce and direct-to-consumer (DTC) water brands is reshaping packaging requirements, driving demand for lightweight, durable, and digitally connected formats. For online distribution, packaging must minimize logistics costs while ensuring structural integrity during shipping. Recent innovations in lightweight polyethylene (PE)-based courier bags have demonstrated significant cost savings in distribution, offering a scalable solution for high-volume water brands competing in the DTC channel. At the same time, smart packaging integration is unlocking new engagement and traceability opportunities. By embedding QR codes or NFC tags directly into bottle labels or caps, brands can offer consumers access to supply chain data, sustainability certifications, and recycling guidance. For example, connected water bottles allow customers to trace the journey from bottling facility to doorstep, reinforcing transparency and brand trust. This convergence of lightweighting and digital connectivity positions e-commerce-ready packaging as a strategic growth avenue for water brands aiming to balance cost efficiency, regulatory compliance, and consumer experience.

Competitive Landscape: Leading Companies Are Driving Innovation and Sustainability in Plastic-Based Water Packaging

The global plastic-based water packaging market is dominated by companies investing in recycled materials, lightweight design, and high-barrier packaging solutions, supporting both consumer convenience and environmental sustainability.

Amcor plc: Combining Nanotechnology and Recyclable PET to Deliver Sustainable Water Packaging Solutions

Amcor offers PET bottles and rigid containers for still, sparkling, and flavored water, alongside closures and films. In April 2025, it partnered with Nfinite Nanotechnology to validate nanocoatings for recyclable and compostable packaging. The company focuses on sustainability and innovation, targeting fully recyclable packaging by 2025, while balancing high-barrier protection and lightweight designs.

Plastipak Packaging, Inc.: Pioneering High-Quality Recycled PET Bottles with Vertical Integration

Plastipak designs and manufactures rigid plastic containers and preforms with a high percentage of recycled content through its URT platform. Its vertically integrated recycling model provides a closed-loop solution, enhancing efficiency and sustainability. Plastipak’s strategy emphasizes complete packaging solutions, lightweight designs, and environmentally responsible production.

Silgan Holdings Inc.: Delivering Customized High-Barrier and Lightweight Bottles for Global Beverage Brands

Silgan provides plastic containers, closures, and dispensing systems, with a focus on lightweighting and use of recycled materials. Its strategy centers on customized, sustainable, and high-performance packaging solutions that preserve product freshness, enhance consumer convenience, and support circular economy goals.

Berry Global Group, Inc.: Leveraging a Broad Portfolio and Recycled Content Expertise in Bottled Water Packaging

Berry Global manufactures bottles, closures, and flexible films for water and beverages, actively incorporating recycled content. Its collaboration with brands like Mars demonstrates a commitment to the circular economy. Berry’s broad portfolio and manufacturing footprint allow it to provide sustainable, high-performance packaging solutions globally.

Sidel International AG: Innovating Ultra-Lightweight Water Bottles and Streamlined Packaging Equipment

Sidel offers blow molding, filling, and labeling equipment for plastic water bottles, alongside ultra-lightweight bottle designs that reduce PET usage. The company provides integrated solutions, including engineering, maintenance, and training, to enhance production efficiency and sustainability for beverage manufacturers.

Plastic Based Water Packaging Market Share Insights, 2025-2034

Purified Water Dominates Market Share by Application in the Plastic-Based Water Packaging Industry

Purified water accounts for 35% of the global plastic-based water packaging market, making it the undisputed leader across all application categories. Its dominance is rooted in low-cost production, mass availability, and efficient packaging formats that cater to both national and private-label brands. The use of PET bottles for purified water has become highly standardized, allowing producers to optimize resin usage, preform manufacturing, and lightweighting strategies at scale. Mineral water continues to maintain a premium niche, leveraging its natural sourcing narrative to justify higher price points, often packaged in customized bottles with rPET integration to meet sustainability mandates. Still water remains the foundation of consumption across all markets, but the fastest growth is concentrated in sparkling and flavored water, where packaging innovation must withstand carbonation pressure while delivering aesthetic appeal. Spring water, marketed for authenticity, and flavored water, aligned with the wellness trend, remain smaller but strategically important, as they depend heavily on differentiated packaging designs for shelf impact and brand positioning. The segmentation highlights how purified water drives bulk demand while premium and functional subcategories accelerate packaging diversification.

500 ml to 1 Liter Bottles Hold the Largest Market Share by Container Size in Plastic-Based Water Packaging

The 500 ml to 1 liter segment commands 40% of the plastic-based water packaging industry, representing the sweet spot for single-serve consumption. These sizes dominate convenience stores, vending channels, and retail shelves globally, making them the highest-volume driver for PET preform and bottle producers. Lightweighting and the incorporation of recycled PET (rPET) are most advanced in this category, as brand owners balance sustainability with the need to maintain strength and clarity. The less than 500 ml category supports impulse-driven consumption and on-the-go hydration, while 1–5 liter multi-serve formats dominate family and office use, driven by affordability per liter and reinforced packaging features like ergonomic grips and pouring spouts. The bulk water segment (5+ liters) remains smaller in volume but structurally important, as it supports dispenser systems and recurring delivery models in both residential and B2B markets. This segmentation demonstrates how packaging innovation is closely tied to container size, with single-serve PET bottles continuing to set the global benchmark in both volume leadership and material efficiency.

United States Plastic Based Water Packaging Market Driven by Lightweighting and Smart Packaging

The United States plastic based water packaging market is undergoing a major shift toward lightweighting and sustainable PET bottle designs. Leading beverage brands such as Coca-Cola are introducing lighter-weight PET bottles to cut down on raw material use while maintaining durability and performance, aligning with both sustainability goals and cost efficiency. This trend is complemented by innovations in post-consumer recycled (PCR) PET integration, with manufacturers steadily increasing PCR percentages to meet state-level mandates and consumer expectations for eco-friendly packaging.

Regulatory oversight remains a key driver. The Food and Drug Administration (FDA) enforces strict food-contact safety standards, ensuring PET bottles used for water comply with contamination prevention guidelines. Meanwhile, the USDA provides additional guidance on packaging materials for consumer safety. At the state level, laws such as Washington’s ESHB 1293 and California’s 2024 single-use packaging ban, which come into force in January 2026, will further restrict certain plastic-based food packaging formats, creating pressure on water brands to adopt compliant alternatives. In parallel, the rise of e-commerce water delivery services has increased demand for robust, tamper-proof, and shippable bottle formats. Companies are also investing in smart packaging technologies like QR codes and NFC tags, allowing brands to share sourcing information, recycling instructions, and product authenticity, enhancing consumer trust and engagement.

European Union Plastic Based Water Packaging Market Aligned with PPWR and Reusable Systems

The European Union plastic based water packaging market is strongly shaped by the Packaging and Packaging Waste Regulation (PPWR), which took effect in February 2025 and mandates strict recyclability and reusability standards. From August 2026, bottled water packaging containing PFAS above specified thresholds will be prohibited, reshaping material choices in the sector. Additionally, by 2030, water bottles with recyclability rates below 70% will not be classified as recyclable, forcing companies to redesign packaging with mono-material PET structures.

Regulatory frameworks are extending beyond recyclability. The harmonized recycling label, mandated by 2028, will make consumer labeling more transparent across all EU member states. Furthermore, EU requirements from February 2025 ensure that plastic packaging on the market must qualify as reusable under defined criteria, boosting the adoption of deposit return schemes and refillable water bottle systems. Alongside compliance, European water brands are exploring circular economy models and digital traceability tools, influenced by frameworks like the Falsified Medicines Directive (FMD), which mandates serialization in pharmaceuticals but has also inspired traceability solutions across food and beverage packaging.

China Plastic Based Water Packaging Market Expands with Recycling Infrastructure and Biodegradable Plastics

The China plastic based water packaging market is adapting to a stricter regulatory environment focused on waste reduction and sustainable materials. A regulation effective from June 2025 targets the express delivery sector by mandating reduced wrapping, recycled content, and reusable systems. This aligns with broader directives from the National Development and Reform Commission (NDRC) and the Ministry of Ecology and Environment (MEE), which are tightening controls on plastic pollution and pushing industries toward biodegradable and oxo-degradable plastics.

The market is also shaped by the ban on plastic waste imports in 2018, which forced China to build domestic PET recycling infrastructure to supply its massive bottled water industry. Local companies are investing heavily in closed-loop recycling systems to meet PET bottle demand while aligning with the government’s circular economy vision. Additionally, the positive list for food-contact materials and new adhesive standards (GB 4806.15-2024, effective February 2025) are redefining compliance requirements for water packaging producers. Together, these policies are accelerating the adoption of food-grade rPET bottles and innovative, eco-friendly packaging designs suitable for China’s booming bottled water and e-commerce channels.

India Plastic Based Water Packaging Market Driven by EPR and Recycling Targets

The India plastic based water packaging market is progressing under the Plastic Waste Management Rules (2016, amended 2022), which enforce Extended Producer Responsibility (EPR) obligations on brand owners and manufacturers. This mandates companies to collect and recycle a significant share of plastic packaging, including bottled water containers. Building on this, the government has announced mandatory recycled content requirements: 30% rPET in packaging by 2026, increasing to 60% by 2029.

Private and public partnerships are driving growth. Varun Beverages and Indorama Ventures are investing in large-scale PET recycling plants to supply food-grade rPET for water packaging. Meanwhile, the Food Safety and Standards Authority of India (FSSAI) is actively consulting stakeholders on sustainable food packaging, boosting adoption of biodegradable and recyclable alternatives. Alongside regulatory drivers, India’s expanding middle-class consumer base and rising demand for packaged drinking water are fueling rapid market expansion. With government-backed initiatives and investments in recycling infrastructure, India is positioning itself as a major hub for eco-friendly, recycled-content water packaging solutions.

United Kingdom Plastic Based Water Packaging Market Shaped by Plastic Packaging Tax and Deposit Return Scheme

The United Kingdom plastic based water packaging market is heavily influenced by the Plastic Packaging Tax (PPT), introduced in April 2022, which applies to plastic packaging with less than 30% recycled content. By the 2024–2025 fiscal year, HMRC data showed that 51% of manufactured or imported plastic packaging already met the threshold, demonstrating market adaptation. Additionally, the government’s Smart Sustainable Plastic Packaging (SSPP) Challenge, a £60 million initiative, has supported over 80 projects aimed at recycling and packaging innovation.

Future regulations are set to further boost recycling. The proposed deposit return scheme for plastic bottles, expected to launch later this decade, will raise collection and recycling rates, creating a more efficient closed-loop system for bottled water. Companies are also investing in single-material, recyclable PET bottles, supported by advancements in recycling technology. With consumer expectations leaning toward sustainability, UK water brands are positioning themselves as leaders in eco-conscious packaging design, leveraging recycled PET, lightweight bottles, and innovative traceability solutions.

Japan Plastic Based Water Packaging Market Innovates with Bottle-to-Bottle Recycling and Ocean-Degradable Plastics

The Japan plastic based water packaging market is at the forefront of innovative recycling and biodegradable packaging technologies. Researchers at the RIKEN Center for Emergent Matter Science (CEMS) have developed an ocean-degradable plastic that fully dissolves in seawater, holding promise for future water bottle applications. Industry leaders such as Suntory are spearheading “bottle-to-bottle” mechanical recycling, where discarded PET bottles are converted into new ones. The company has also launched label-free bottles and crushable 2L PET bottles, designed for easy storage and improved consumer recycling behavior.

The government is promoting circular economy initiatives, reinforcing waste reduction through positive list regulations for food-contact materials. These policies ensure safety compliance while pushing for innovation in recyclable and biodegradable packaging. At the same time, Japan’s growing e-commerce and home delivery market is boosting demand for durable, lightweight, and recyclable PET water bottles. With strong collaboration between industry, academia, and regulators, Japan is emerging as a global leader in next-generation water packaging solutions that combine sustainability, safety, and consumer convenience.

Plastic Based Water Packaging Market Report Scope

Plastic Based Water Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.6 Billion

|

|

Market Size (2034)

|

$20.6 Billion

|

|

Market Growth Rate

|

6.6%

|

|

Segments

|

By Material (PET, HDPE, LDPE, PP, Recycled Content Plastics, Bio-based plastics), By Packaging Type (Bottles, Jugs, Pouches & Sachets, Cups, Others), By Application (Still Water, Sparkling Water, Flavored Water, Purified Water, Mineral Water, Spring Water, Others), By Container Size (Less than 500 ml, 500 ml–1 L, 1–5 L, More than 5 L), By End-Use Industry (Retail, Food Service, Institutional, E-commerce)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global, Inc., Novolex Holdings, LLC, Mondi Group, AptarGroup, Inc., Gerresheimer AG, Huhtamaki Oyj, Alpla-Werke Alwin Lehner GmbH & Co KG, Nippon Closures Co., Ltd., Sidel (Tetra Laval Group), WestRock Company, Sonoco Products Company, Rexam (Ball Corporation), Alpha Packaging, Plastipak Holdings, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Plastic Based Water Packaging Market Segmentation

By Material

- PET

- HDPE

- LDPE

- PP

- Recycled Content Plastics

- Bio-based plastics

By Packaging Type

- Bottles

- Jugs

- Pouches & Sachets

- Cups

- Others

By Application

- Still Water

- Sparkling Water

- Flavored Water

- Purified Water

- Mineral Water

- Spring Water

- Others

By Container Size

- Less than 500 ml

- 500 ml–1 L

- 1–5 L

- More than 5 L

By End-Use Industry

- Retail

- Food Service

- Institutional

- E-commerce

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Plastic Based Water Packaging Market

- Amcor plc

- Berry Global, Inc.

- Novolex Holdings, LLC

- Mondi Group

- AptarGroup, Inc.

- Gerresheimer AG

- Huhtamaki Oyj

- Alpla-Werke Alwin Lehner GmbH & Co KG

- Nippon Closures Co., Ltd.

- Sidel (Tetra Laval Group)

- WestRock Company

- Sonoco Products Company

- Rexam (Ball Corporation)

- Alpha Packaging

- Plastipak Holdings, Inc.

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive and data-driven methodology to provide authoritative insights into the Plastic-Based Water Packaging Market. Our research combines primary data collection through interviews with beverage manufacturers, packaging suppliers, sustainability experts, and industry stakeholders, with secondary research from regulatory filings, corporate reports, scientific publications, and trade journals. Market sizing, growth forecasting, and CAGR analysis are conducted using both top-down and bottom-up approaches, segmented by material (PET, HDPE, LDPE, PP, recycled content plastics, bio-based plastics), packaging type (bottles, jugs, pouches & sachets, cups, others), container size, application (still, sparkling, flavored, purified, mineral, spring water), and end-use industry (retail, food service, institutional, e-commerce). USDAnalytics evaluates market evolution through sustainability-driven innovations, including rPET adoption, lightweighting, high-barrier coatings, nanotechnology applications, and circular economy initiatives. Regional regulatory frameworks—such as the EU PPWR, UK Plastic Packaging Tax, India’s EPR mandates, U.S. FDA and state-level requirements, China’s green packaging rules, and Japan’s positive list system—are analyzed for their impact on packaging design and material selection. Competitive benchmarking highlights strategic mergers, vertical integration, and technological innovations by leading players such as Amcor, Plastipak, Berry Global, and Sidel, providing industry professionals with a clear understanding of market dynamics, opportunities, and global sustainability trends shaping the plastic-based water packaging landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.