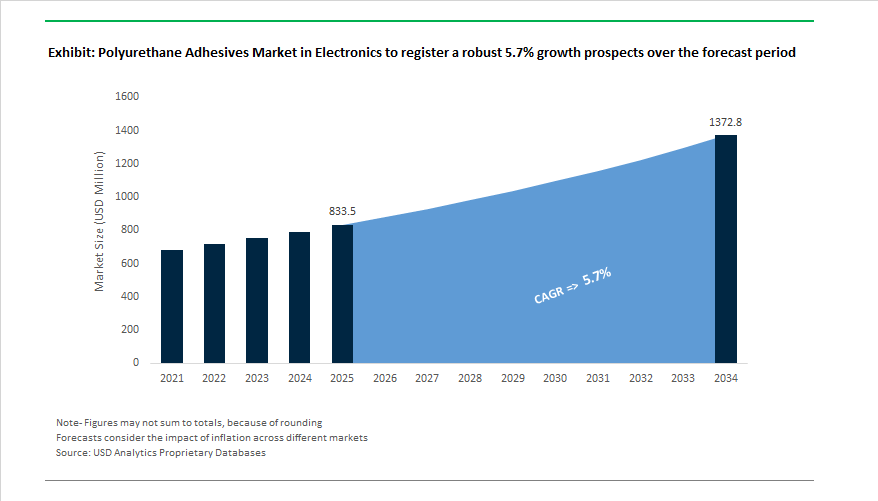

The Global Polyurethane Adhesives in Electronics Market is projected to grow from USD 833.5 million in 2025 to USD 1.37 billion by 2034, at a CAGR of 5.7%, reflecting polyurethane’s expanding role as a functional reliability material rather than a simple bonding medium. Growth is being shaped less by volume expansion in legacy consumer electronics and more by design complexity, thermal loading, and durability expectations in automotive electronics, power modules, and e-mobility systems.

In electronics manufacturing, polyurethane occupies a critical middle ground between rigid epoxies and soft silicones. OEMs increasingly specify PU adhesives where elastic stress absorption, dielectric stability, and adhesion to mixed substrates must coexist within compact assemblies. This positioning is particularly relevant as electronics architectures shift toward flexible printed circuits, multi-board stacks, and vibration-exposed modules, where brittle systems accelerate failure modes under thermal cycling and mechanical shock.

In addition, a structural shift is underway in formulation and procurement criteria. Electronics manufacturers are steadily moving toward low-monomer (<0.1%) and low-VOC polyurethane systems, not only to satisfy ECHA and REACH compliance, but also to simplify worker safety protocols and qualification processes across global plants. This transition is influencing adhesive selection earlier in the design phase, with environmental and safety documentation increasingly treated as gating requirements rather than downstream considerations.

Miniaturization is reshaping performance expectations. As bond lines shrink below 50 μm in flex circuits, wearable devices, and display assemblies, polyurethane formulations are being engineered for controlled flow, low modulus, and dimensional stability at ultra-thin geometries. In these applications, PU’s ability to maintain adhesion without inducing stress on delicate substrates such as polyimide films, epoxy-glass laminates, and chip-scale components is becoming a decisive advantage over higher-modulus alternatives. Further, the automotive and e-mobility segments are redefining the upper end of the specification curve. Polyurethane gap fillers and potting compounds are now integral to EV battery packs, inverters, and power electronics, where thermal conductivity exceeding 2.0 W/mK is required alongside vibration damping and electrical insulation. Unlike silicone-only systems, polyurethane formulations allow manufacturers to balance thermal management with mechanical cohesion, supporting long service life under continuous thermal cycling from −40°C to +125°C.

Encapsulation and potting applications further reinforce polyurethane’s relevance. PU-based potting compounds are increasingly specified to protect ADAS sensors, LED modules, and power control units from moisture ingress, vibration, and chemical exposure. Here, dielectric performance—across hardness ranges from Shore A50 to Shore D75—is gaining importance in procurement decisions, particularly as electronics migrate closer to heat sources and high-voltage environments.

The global polyurethane adhesives market for electronics is witnessing significant advancements with a strong emphasis on sustainability, regulatory compliance, and functional innovation.

In May 2024, Dow Inc. inaugurated a new production line for its VORATRON™ polyurethane systems at its Polyurethanes Systems House in Ahlen, Germany, dedicated to serving the e-mobility battery assembly market. The expansion enhances Dow’s ability to meet surging demand for thermally conductive polyurethane adhesives and gap fillers, enabling efficient thermal management in electric vehicle battery packs and power electronics. The same development aligns with the company’s broader MobilityScience™ initiative, which integrates materials expertise across automotive and electronic sectors.

In early 2024, H.B. Fuller introduced a single-component polyurethane adhesive specifically designed for flexible touch panel bonding in smartphones and wearable devices. This innovation achieves faster curing, enhanced optical clarity, and improved impact resistance, directly addressing the needs of consumer electronics miniaturization and durability. Meanwhile, Henkel AG & Co. KGaA expanded its TECHNOMELT® portfolio in 2023 to include bio-based polyurethane adhesives derived from renewable polyols, furthering its commitment to low-monomer and low-VOC adhesive solutions for sustainable manufacturing.

Regulatory forces also played a defining role. In February 2024, the European Chemicals Agency (ECHA) implemented mandatory training requirements for professionals handling diisocyanates in PU adhesives, prompting manufacturers to accelerate low-monomer innovations. Responding to this, BASF expanded its polyurethane dispersion (PUD) production capacity in Spain (2024) to support the demand for solvent-free adhesives across electronics, automotive, and packaging industries.

The sector also saw important M&A and R&D moves. In 2023, Bostik (Arkema) completed the acquisition of a European specialty materials company, gaining direct access to conductive and thermally functionalized polyurethane adhesives tailored for microelectronics and sensor applications. 3M, during the same year, launched a dual-cure polyurethane adhesive combining moisture and UV curing mechanisms, designed to address high-precision automotive and industrial electronic bonding. In September 2025, a leading research consortium announced the development of room-temperature-setting polydiene urethane adhesives with superior dielectric and elasticity properties, marking a major step forward in sustainable and efficient electronic component assembly.

Market Trend 1: Development of Low-Pressure Molding (LPM) Encapsulants for Delicate Component Protection

One of the most prominent technological shifts in the electronics adhesives market is the adoption of low-pressure molding (LPM) encapsulants based on advanced polyurethane and polyamide systems. These low-stress materials are engineered to encapsulate delicate electronic assemblies—including sensors, connectors, and printed circuit boards (PCBs)—without subjecting them to damaging mechanical or thermal stresses.

Unlike traditional high-pressure potting or injection processes, LPM operates at 20 to 580 psi (1.5 to 40 bar), with significantly lower processing temperatures, minimizing the risk of deformation in solder joints or miniature components. By using thermoplastic polyurethane (TPU) compounds, manufacturers can achieve high durability, watertight protection, and vibration resistance while reducing material waste and cycle time.

In high-volume applications such as automotive sensor modules and IoT wearables, LPM has revolutionized manufacturing efficiency—cutting encapsulation from 7–8 process steps down to just 3–4, and curing times from several hours to as little as 5 to 50 seconds. The cycle time advantage is crucial for large-scale automation in EV sensor assemblies, automotive harnesses, and consumer electronics, where Ingress Protection (IP) ratings of IP67 or higher are often required for under-the-hood reliability.

As electronics continue to miniaturize, LPM polyurethane encapsulants are becoming essential to deliver shock absorption, dielectric insulation, and environmental resilience—all at the low pressures needed for sensitive circuitry.

Market Trend 2: Formulation of Low-Outgassing and High-Purity Polyurethane Adhesives for High-Vacuum Electronics

The growing use of high-vacuum and optical systems, such as MEMS sensors, photonics, and precision lenses, has placed a sharp focus on developing low-outgassing polyurethane adhesives that meet space-grade material purity standards. In these advanced electronics, even minute emissions of Volatile Condensable Materials (VCMs) can deposit on critical surfaces, leading to optical fogging or micro-mechanical malfunction.

To address the, polyurethane systems are engineered to comply with NASA ASTM E595 outgassing standards, which require a Total Mass Loss (TML) below 1.0% and Collected Volatile Condensable Material (CVCM) under 0.10%. Advanced high-purity polyurethane formulations have demonstrated CVCM levels as low as 0.01%, making them suitable for aerospace-grade microelectronics and precision MEMS fabrication.

These low-outgassing adhesives are critical for ensuring the long-term stability of automotive MEMS accelerometers, LiDAR sensors, and camera modules, as well as industrial robotics and consumer imaging devices. By eliminating contamination risks and preserving optical transparency, high-purity polyurethane systems significantly improve the reliability and lifespan of sensitive components used in high-performance environments.

Market Opportunity 1: Thermal Management and Structural Bonding Solutions for AI and HPC Electronics

With the rapid adoption of Artificial Intelligence (AI), High-Performance Computing (HPC), and data center servers, the demand for thermally conductive polyurethane adhesives is surging. These advanced formulations serve a dual purpose—efficient heat dissipation and mechanical reinforcement—for securing heavy electronic components under extreme temperature gradients.

Modern polyurethane-based thermal interface adhesives are infused with conductive fillers such as Aluminum Oxide (Al₂O₃) and Aluminum Nitride (AlN), enabling thermal conductivity values between 1.2 W/m·K and 2.0 W/m·K, compared to approximately 0.14 W/m·K in unfilled variants. The conductivity enhancement is critical for AI server processors, GPU modules, and power management boards, where continuous high-speed operation generates substantial heat loads.

In addition, these materials are optimized for mechanical flexibility and shock resistance. Structural polyurethane adhesives in the segment can deliver shear strengths of 8–9 MPa on aluminum while maintaining 5% elongation at break, ensuring the bond can absorb expansion and contraction stresses caused by frequent temperature cycling.

By combining thermal management and mechanical reliability, polyurethane adhesives are emerging as the backbone of next-generation electronics assembly, particularly in data-intensive, high-wattage environments such as AI supercomputers and cloud server racks.

Market Opportunity 2: Enabling the Expansion of Flexible and Wearable Medical Electronics

The growing adoption of wearable medical devices and remote health monitoring systems is creating a specialized market for biocompatible, flexible polyurethane adhesives that can endure continuous body contact, mechanical movement, and sterilization processes. These materials are designed for skin-safe adhesion, breathability, and elasticity, serving applications like biosensors, ECG patches, smart textiles, and flexible electrode arrays.

Medical-grade polyurethane systems are engineered to comply with ISO 10993 biocompatibility standards—notably ISO 10993-5 for cytotoxicity and ISO 10993-10 for irritation and sensitization—ensuring their safety in continuous skin-contact devices. Unlike rigid epoxies, polyurethanes offer superior elongation, flexibility, and low modulus, making them ideal for applications requiring conformability to skin or soft tissue.

These adhesives are also chemically resistant, maintaining structural and adhesive performance during sterilization cycles using Ethylene Oxide (EtO) or gamma irradiation, and resisting degradation from sweat, sebum, and bodily fluids. The durability makes them well-suited for long-wear medical patches and disposable monitoring systems used in both hospital and home-care settings.

As digital health, telemedicine, and smart wearable ecosystems expand, medical-grade polyurethane adhesives are set to play an essential role in the convergence of electronics and biotechnology, where comfort, reliability, and skin compatibility drive adoption.

Competitive Landscape: Strategic Profiles of Leading Companies in the Polyurethane Adhesives in Electronics Market

The competitive landscape is dominated by a blend of global chemical and materials science leaders, each investing heavily in R&D, regional production capacity, and sustainable adhesive chemistry. Companies such as Henkel, Dow, 3M, H.B. Fuller, Bostik (Arkema), and Sika continue to drive performance standards in bonding, encapsulation, and heat management applications. The market is defined by strategic differentiation in thermal conductivity, sustainability, and precision processing technologies.

Henkel remains a cornerstone in the polyurethane electronics adhesives market with its LOCTITE® potting compounds and conformal coatings that safeguard PCBs and semiconductor assemblies from thermal shock, humidity, and chemical exposure. The company’s solutions are widely adopted in automotive control units, power electronics, and industrial sensors. Henkel’s continued focus on renewable polyols and low-VOC polyurethane adhesives under the TECHNOMELT® line exemplifies its sustainability-driven innovation strategy for both consumer and industrial electronics.

Through its MobilityScience™ platform, Dow leverages polymer and process expertise to provide thermally conductive polyurethane systems used in battery modules and power electronics. The company’s 2024 expansion at its Ahlen, Germany facility significantly enhanced capacity for VORATRON™ gap fillers and encapsulants, meeting rising EV battery thermal management demands. Dow’s leadership in high thermal conductivity (>2.0 W/mK) adhesives positions it as a preferred supplier for automotive OEMs pursuing safer, longer-lasting electric vehicle designs.

3M continues to set benchmarks in adhesive versatility with its dual-cure polyurethane formulations, enabling both UV and moisture curing for precision applications. These adhesives enhance productivity in automotive electronics, sensors, and display modules, providing excellent adhesion to low-surface-energy plastics and metals. Additionally, its Bumpon™ Protective Products offer superior shock absorption and vibration dampening, serving as multifunctional bonding and protective components for wearable and consumer electronics.

H.B. Fuller’s ELEKTRON® polyurethane adhesive series demonstrates cutting-edge engineering for high peel strength and flexibility in touchscreen, display, and advanced electronic component assembly. The company’s single-component PU adhesives, launched in 2024, provide faster curing and improved impact resistance, supporting next-generation device miniaturization. H.B. Fuller’s approach emphasizes custom co-creation with manufacturers, enhancing bonding efficiency and end-product reliability across the electronics value chain.

Following its 2023 European acquisition, Bostik broadened its Born2Bond™ portfolio to include functionalized, light-curing polyurethane adhesives ideal for low-pressure molding and microelectronics bonding. The integration of conductive PU formulations enhances thermal management and electrical conductivity in critical assemblies such as sensors and circuit boards. With Arkema’s upstream polymer expertise, Bostik is positioned at the intersection of electronics miniaturization and sustainable materials development.

Sika has established a strong foothold in industrial and outdoor electronic enclosure sealing, delivering flexible polyurethane sealants and adhesives that withstand moisture, UV radiation, and temperature extremes. Its solutions are widely used in EV charging stations, outdoor sensors, and telecom infrastructure. The company’s Purform® low-monomer PU technology enhances worker safety while maintaining high flexibility, making Sika a preferred supplier in industrial electronics assembly and infrastructure applications.

Country Analysis: Regional Insights and Strategic Developments in the Global Polyurethane Adhesives in Electronics Industry

China: Expanding Leadership in Polyurethane Adhesives for EV Batteries and High-Volume Electronics Manufacturing

China remains the undisputed global hub for polyurethane adhesives in electronics, driven by strong government subsidies, massive production capabilities, and rapid technological integration in electric mobility and consumer electronics. With over $230 billion in EV subsidies between 2009 and 2023, China’s aggressive push toward electrification has propelled demand for thermally conductive polyurethane gap fillers and encapsulants used in EV battery pack assembly, structural bonding, and module sealing. The materials ensure thermal stability, vibration resistance, and safety—key requirements for the expanding electric vehicle ecosystem.

Simultaneously, domestic players are investing heavily in isocyanate and polyol feedstock production to achieve raw material self-sufficiency and minimize exposure to global supply chain volatility. In consumer electronics, China’s unparalleled manufacturing scale in smartphones, tablets, and wearables continues to drive the use of PU potting compounds and conformal coatings for reliable component protection. Increasing R&D efforts are dedicated to low-outgassing polyurethane formulations tailored for flexible OLED displays and next-generation semiconductor encapsulation. Supported by robust policy backing and growing domestic innovation capacity, China is consolidating its position as the largest and most technologically advanced market for polyurethane adhesives in electronic manufacturing applications.

United States: Semiconductor Reshoring and High-Performance Electronics Driving Polyurethane Innovation

The United States polyurethane adhesives in electronics market is being redefined by the CHIPS and Science Act and massive investments in domestic semiconductor and advanced electronics manufacturing. The $52 billion federal initiative is triggering the construction of new fabrication facilities and advanced packaging plants across states such as Arizona, Texas, and Ohio. The boom is driving demand for specialized polyurethane packaging adhesives, die-attach materials, and thermal management compounds that enhance reliability in wafer-level and power electronics packaging.

The automotive sector continues to be a critical growth driver, with OEMs like Tesla and Ford prioritizing flame-retardant, high-impact polyurethane adhesives for EV battery pack integration and module bonding, replacing mechanical fasteners to reduce weight and improve structural performance. Additionally, the U.S. Department of Energy’s $140 million allocation in 2024 toward electronics R&D underscores growing federal support for innovation in polyurethane-based thermal interface materials and die-attach adhesives. The rise of low-VOC and bio-based PU dispersions, especially in California and other environmentally regulated states, is pushing manufacturers toward sustainable formulations for consumer electronics and automotive interiors. Through its strong innovation ecosystem and policy-driven investments, the United States is emerging as a global leader in high-performance and sustainable polyurethane adhesive technologies for next-generation electronics.

Germany: Precision Engineering and Sustainable Electronics Manufacturing Powering Polyurethane Adoption

Germany’s polyurethane adhesives in electronics industry is being shaped by its automotive electronics expertise, precision engineering, and sustainability mandates. The nation’s world-class automotive OEMs demand certified 2K polyurethane adhesive systems designed for ADAS sensor modules, electronic control units (ECUs), and camera housings, where long-term heat resistance and mechanical durability are critical. The precision-focused market underscores Germany’s leading role in high-specification electronic adhesive applications within Europe.

Germany’s dominance in industrial automation and robotics further stimulates demand for PU encapsulants, conformal coatings, and potting materials used to safeguard PCBs and electronic modules in harsh factory environments. Leading chemical companies such as Henkel and BASF are investing in solvent-free and bio-based polyurethane adhesive lines, aligning with EU REACH regulations and European Green Deal objectives. The push for VOC reduction and circularity is driving the transition toward eco-certified polyurethane materials across consumer electronics, EVs, and industrial systems. Combining sustainability with engineering precision, Germany stands as the European benchmark for high-performance, low-emission polyurethane adhesive innovation in electronic systems.

South Korea: Global Center for Display Technology and Semiconductor Polyurethane Applications

South Korea leads in the adoption and development of polyurethane adhesives for advanced electronics, display technology, and memory semiconductor manufacturing. The country’s dominance in OLED, QLED, and flexible display production has created surging demand for optically clear, ultra-thin polyurethane adhesives used in bezel-less smartphone screens, foldable device hinges, and touchscreen laminations. The adhesives offer superior optical transparency, flexibility, and reworkability, crucial for next-generation display assembly.

In the semiconductor sector, leading Korean manufacturers are driving R&D into polyurethane underfills, encapsulants, and gasketing materials for 3D-stacked memory chips and high-density logic packages. As 5G and 6G infrastructure expands, the need for dielectric polyurethane sealants with thermal and electrical insulation properties is growing, particularly for base stations and RF components. Supported by strong government incentives for digital infrastructure and material innovation, South Korea is establishing itself as a global hub for high-precision, electronics-grade polyurethane adhesive technologies that serve both the semiconductor and display industries.

Japan: Precision Materials Leadership and Polyurethane Innovation for Miniaturized Electronics

Japan’s polyurethane adhesives market for electronics is characterized by precision, miniaturization, and innovation in material performance. Japanese electronics and robotics manufacturers are driving the development of low-viscosity polyurethane potting adhesives that can penetrate micro-spaces and ensure void-free encapsulation of compact circuits and components. The formulations are critical for wearable electronics, consumer gadgets, and smart sensors, where miniaturization requires exceptional flow control and mechanical integrity.

The nation’s R&D centers are also pioneering thermally stable polyurethane grades optimized for power electronics applications, including silicon carbide (SiC) inverters and EV converters, which operate under extreme heat. Japan’s advanced robotics and Industrial IoT sectors rely heavily on elastic polyurethane bonding systems for securing sensors and cables subjected to continuous motion and vibration. Additionally, research into biodegradable and recyclable polyurethane materials aligns with Japan’s long-term sustainability commitments. Through its strong synergy of materials science, automation, and green innovation, Japan remains a global pioneer in high-precision polyurethane adhesives for miniaturized and high-temperature electronic systems.

India: Expanding Electronics Manufacturing Ecosystem and Growing EV Market Driving Polyurethane Consumption

India is emerging as a fast-growing market for polyurethane adhesives in electronics, fueled by government-backed industrialization, expanding EV adoption, and infrastructure modernization. Under the “Make in India” and Production Linked Incentive (PLI) schemes, major global OEMs are establishing local electronics manufacturing facilities, significantly boosting the domestic demand for polyurethane SMT (Surface Mount Technology) adhesives, potting compounds, and assembly sealants.

The country’s electric vehicle sector, led by the rapid rise of two- and three-wheel EVs, is generating new opportunities for cost-effective polyurethane adhesives and gap fillers used in battery modules and thermal management systems. Simultaneously, the growth of telecommunications and 5G network infrastructure is spurring the need for PU protective coatings and sealants designed to withstand high humidity, UV exposure, and temperature fluctuations. As India accelerates its electronics manufacturing output and invests in R&D for locally produced materials, the country is fast becoming a strategic hub for scalable, affordable, and high-performance polyurethane adhesive solutions in the global electronics value chain.

Polyurethane Adhesives Market in Electronics Report Scope

Polyurethane Adhesives Market in Electronics

|

Parameter

|

Details

|

|

Market Size (2025)

|

$833.5 Million

|

|

Market Size (2034)

|

$1,372.7 Million

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Technology (One-Component Moisture-Cure, Two-Component, Polyurethane Hot-Melt, Polyurethane Dispersions, UV-Curing), By Function (Electrically Conductive, Thermally Conductive, Flame-Retardant, Low-VOC/Solvent-Free, Optically Clear), By Application (Component Protection, Circuit Board Assembly, Display/Screen Bonding, Battery Assembly, Conformal Coatings, Structural Bonding), By End-Use Industry (Consumer Electronics, Automotive Electronics, Semiconductor & Microelectronics, Industrial & Medical Electronics, Telecommunications

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, Sika AG, 3M Company, Covestro AG, Dow Inc., Huntsman Corporation, BASF SE, Arkema S.A. (Bostik), Wacker Chemie AG, Dymax Corporation, Master Bond Inc., Ashland Global Holdings Inc., Franklin International, Jowat SE

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Technology/Composition

- One-Component Moisture-Cure

- Two-Component

- Polyurethane Hot-Melt

- Polyurethane Dispersions

- UV-Curing

By Function/End-Property

- Electrically Conductive

- Thermally Conductive

- Flame-Retardant

- Low-VOC/Solvent-Free

- Optically Clear

By Application

- Component Protection

- Circuit Board Assembly

- Display/Screen Bonding

- Battery Assembly

- Conformal Coatings

- Structural Bonding

By End-Use Industry

- Consumer Electronics

- Automotive Electronics

- Semiconductor & Microelectronics

- Industrial & Medical Electronics

- Telecommunications

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Polyurethane Adhesives in Electronics Market

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Sika AG

- 3M Company

- Covestro AG

- Dow Inc.

- Huntsman Corporation

- BASF SE

- Arkema S.A. (Bostik)

- Wacker Chemie AG

- Dymax Corporation

- Master Bond Inc.

- Ashland Global Holdings Inc.

- Franklin International

- Jowat SE

*- List not Exhaustive

Research Coverage

This report investigates the Global Polyurethane Adhesives in Electronics Market, delivering analysis reviews on the technology, demand, compliance, and manufacturing shifts that are redefining bonding, protection, and thermal management across consumer devices, automotive electronics, semiconductors, and industrial/medical systems. Developed by USDAnalytics, the study highlights breakthroughs in ultra-thin bond lines for miniaturization, low-monomer/low-VOC chemistries for REACH/ECHA compliance, and thermally conductive formulations for e-mobility and high-power electronics; it benchmarks supplier innovation, maps cost-to-serve drivers (materials, process efficiency, and yield), and quantifies adoption across key value-chain nodes—making this report an essential resource for CTOs, process engineers, procurement leaders, and product managers seeking reliable, sustainable, and scalable polyurethane solutions in advanced electronics manufacturing.

Scope Highlights

Segmentation:

- By Technology/Composition: One-Component Moisture-Cure; Two-Component; Polyurethane Hot-Melt; Polyurethane Dispersions; UV-Curing.

- By Function/End-Property: Electrically Conductive; Thermally Conductive; Flame-Retardant; Low-VOC/Solvent-Free; Optically Clear.

- By Application: Component Protection; Circuit Board Assembly; Display/Screen Bonding; Battery Assembly; Conformal Coatings; Structural Bonding.

- By End-Use Industry: Consumer Electronics; Automotive Electronics; Semiconductor & Microelectronics; Industrial & Medical Electronics; Telecommunications.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecasts 2025–2034.

Companies Covered: Analysis / profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.