Rigid Thermoform Plastic Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Rigid Thermoform Plastic Packaging Market Set to Expand to $62.9 Billion by 2034 Driven by Sustainability and E-commerce Growth

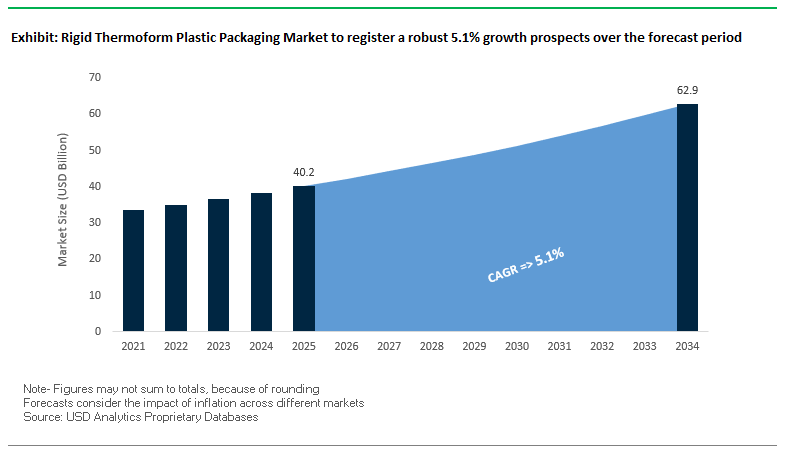

The global rigid thermoform plastic packaging market is projected to grow from $40.2 billion in 2025 to $62.9 billion by 2034, at a CAGR of 5.1%. The growth trajectory is fueled by demand in food and beverage packaging, adoption of recycled content, robust e-commerce logistics, and pharmaceutical packaging needs. This market offers strategic insights for buyers and investors focusing on durable, sustainable, and innovative packaging solutions.

Key Insights for Industry Professionals:

- Food & Beverage Dominance: Accounts for roughly 60% of market volume, driven by ready-to-eat meals and fresh produce packaging.

- Recycled Content Integration: Companies are integrating 25% or more post-consumer recycled (PCR) material to meet regulatory and consumer sustainability demands by 2025.

- E-commerce and Durability: Clamshells, trays, and rigid thermoformed containers provide tamper-evident, durable protection, reducing product damage during transit.

- Pharmaceutical and Medical Applications: Annual production of around 50 million units, driven by demand for secure, sterile, and tamper-evident packaging.

- Sustainability-Driven Innovation: Plant-based polymers and recyclable solutions are increasingly adopted to align with circular economy goals.

- Operational Efficiency Opportunities: Advanced thermoforming equipment and lightweighting strategies reduce material use and enhance production efficiency.

The rigid thermoform packaging market is therefore a convergence of durable design, sustainability, and regulatory compliance, creating high-value opportunities for global manufacturers and retailers.

Market Analysis: Industry Consolidation, Sustainability Initiatives, and Technological Advancements Are Driving Market Dynamics

The rigid thermoform plastic packaging sector has seen accelerated consolidation and innovation. In August 2025, Amcor and Flügger introduced a paint container with 50% recycled material, reflecting commitment to circular packaging. In the same month, Inteplast acquired German plastics board maker Con-pearl, enhancing capabilities in the rigid plastics market. Strategic mergers continue to redefine industry leadership; Amcor’s acquisition of Berry Global in July 2025 created a diversified global packaging powerhouse.

Sustainability-led initiatives have reshaped production priorities. In February 2025, Amcor partnered with Avantium NV to explore plant-based polyethylene furanoate, marking a major step toward bioplastic adoption. Facility expansions and technology upgrades are enhancing operational efficiency; for instance, ULMA Packaging’s April 2025 launch of TFX thermoformers aims to improve productivity by up to 10% and reduce vacuum cycle times by 20%.

Portfolio optimization also guides growth strategy. April 2025 saw Sonoco divest its Thermoformed and Flexibles Packaging business to TOPPAN Holdings for US$1.8 billion, allowing a focus on core rigid packaging strengths. ALPLA’s Italian acquisition the same month expanded injection molding capabilities, while January 2025 Macfarlane Group acquisition of Pitreavie enhanced recyclable transit packaging expertise.

Rigid Thermoform Plastic Packaging Market: Trends and Opportunities Driving Circular Growth

Strategic Shift to rPET and rPP to Meet PCR Content Mandates

A central trend in the rigid thermoform plastic packaging market is the rapid transition to recycled polyethylene terephthalate (rPET) and recycled polypropylene (rPP) to comply with legally binding post-consumer recycled (PCR) content mandates. According to a 2025 NAPCOR report, the volume of PET thermoforms collected for recycling in the U.S. and Canada nearly doubled—growing by 96% between 2016 and 2023. This expansion reflects a strong supply chain response to rising brand and regulatory demand for recycled content integration. In fact, by 2023, the average recycled content in PET thermoforms exceeded that of PET bottles, underscoring the industry’s progress toward establishing a closed-loop recycling system for thermoformed products. With the European Union’s Packaging and Packaging Waste Regulation (PPWR) and India’s Extended Producer Responsibility (EPR) frameworks mandating recycled content percentages, thermoformers are under growing pressure to secure consistent PCR feedstock and scale their use of rPET and rPP to maintain compliance while supporting corporate sustainability goals.

Lightweighting and Material Reduction through Advanced Engineering

Another defining trend is the lightweighting of thermoformed packaging through advanced design and material engineering. Manufacturers are optimizing tray and container geometries to reduce material use while maintaining structural integrity. A case study from a leading packaging supplier demonstrated a 30% reduction in material use for a transport tray by applying advanced thermoforming techniques compared to conventional processes. These improvements not only lower raw material costs but also enhance environmental performance by reducing total resource consumption. Beyond materials savings, lightweighting generates tangible downstream benefits: an article on thermoforming logistics reported that a 20% reduction in packaging weight translates into 10–15% savings in fuel costs for large-scale shipments. This dual benefit—cost competitiveness and carbon footprint reduction—makes lightweighting a cornerstone strategy for thermoformers and their brand partners in retail, foodservice, and industrial packaging.

Development of High-Barrier Monomaterial Thermoformed Solutions

A critical opportunity lies in the development of high-barrier monomaterial thermoformed packaging to replace non-recyclable multi-material structures. In August 2025, Reifenhäuser, ExxonMobil, and Multivac collaborated on a breakthrough solution: a 95% polyethylene (PE)-based thermoformable film that matches the stiffness and puncture resistance of traditional polyamide (PA)-containing laminates. Such innovation demonstrates how monomaterial solutions can balance recyclability with functional requirements. Barrier performance is especially important in food applications, where shelf life is tied directly to oxygen and moisture protection. New classes of mono-PE films are already achieving oxygen transmission rates (OTR) as low as 1–3 cm³/m²/24hr, a performance level once thought achievable only with multi-layer composites. By extending the shelf life of products like meat, cheese, and ready meals, these recyclable thermoformed structures address both sustainability imperatives and stringent product safety standards, making them a game-changer for high-value food packaging applications.

Integration of In-Mold Labeling (IML) for Premium Shelf Differentiation

The integration of In-Mold Labeling (IML) into thermoformed packaging presents another high-growth opportunity for manufacturers seeking premium aesthetics without compromising recyclability. Unlike traditional pressure-sensitive labels that rely on adhesives, IML fuses a thin PP or PET label directly into the container during the molding process, producing a monolithic, fully recyclable package. This ensures seamless recycling streams while eliminating contamination from adhesives. From a branding perspective, IML significantly enhances durability and visual appeal. Labels created through IML are scratch-resistant, moisture-proof, and chemical-resistant, making them ideal for dairy cups, deli containers, and refrigerated products where packaging must withstand challenging storage and handling conditions. A technical guide on IML notes that these containers retain their vibrant colors and branding even after repeated use, providing differentiation at the point of sale while supporting sustainability objectives.

Competitive Landscape: Leading Companies Are Driving Innovation, Sustainability, and Operational Efficiency in Rigid Thermoform Plastic Packaging

The rigid thermoform plastic packaging market is competitive, with top players leveraging mergers, technology, and sustainable practices to capture market share across food, beverage, and healthcare sectors. These companies excel in providing durable, recyclable, and high-performance packaging solutions.

Sonoco Products Company: Delivering Durable and Eco-Friendly Thermoformed Packaging Solutions

Sonoco offers thermoformed plastic containers, trays, and lids, primarily for food applications such as fresh produce, meat, and prepared meals. In April 2025, the company divested Thermoformed and Flexibles Packaging to TOPPAN Holdings to concentrate on core strengths. Sonoco’s advanced barrier solutions ensure product protection and extend shelf life, while its global operations and use of 100% recycled paperboard reinforce sustainability and supply chain control.

Amcor plc: Expanding Global Footprint Through Innovation and Recyclable Packaging Leadership

Amcor provides high-performance PET trays and clamshells across multiple sectors. The July 2025 merger with Berry Global created a global powerhouse. Amcor emphasizes 100% recyclable or reusable packaging by 2025 and has introduced AmFiber Performance Paper and sustainable sports closures for children’s beverages. Its lightweighting efforts have reduced plastic content in some products by over 16%, highlighting innovation in material efficiency.

Sealed Air Corporation (SEE): Leading Sustainability with Automation-Integrated Thermoform Packaging

SEE manufactures rigid thermoformed products for food service and processed meats under brands like CRYOVAC® and LIQUIBOX®. Its “Net Positive Circular Ecosystem” strategy targets 100% recyclable packaging by 2025. SEE integrates automation and digital solutions, aiming to double its automation portfolio by 2027 with over 80% of sales transacted digitally. In May 2023, the company rebranded to SEE®, reinforcing its commitment to packaging innovation.

Pactiv Evergreen Inc.: Advancing Sustainable Fresh Food Packaging with Thermoformed Solutions

Pactiv Evergreen specializes in thermoformed containers, cups, and trays for fresh food and beverage applications. The company focuses on sustainable, recyclable, and compostable packaging. In March 2025, a buyout milestone was achieved to optimize its portfolio, reflecting strategic alignment with sustainability and operational efficiency. Pactiv serves major retailers and food service companies, emphasizing high-quality fresh food packaging.

Silgan Holdings Inc.: Driving Shelf-Life Extension and High-Barrier Technology in Thermoformed Packaging

Silgan Holdings produces high-barrier thermoformed plastic containers for shelf-stable food. Its products offer microwavable packaging in double-seam or heat-seal versions to maximize product protection and shelf life. In August 2025, Silgan expanded its European operations through a key acquisition. The company focuses on innovative, cost-effective packaging technologies that improve product preservation, sustainability, and consumer convenience.

Rigid Thermoform Plastic Packaging Market Share Insights, 2025-2034

Trays Dominate Market Share by Product Type in the Rigid Thermoform Plastic Packaging Industry

Trays command the largest share at 35% in the rigid thermoform plastic packaging industry, underscoring their versatility and centrality to the food and beverage sector. Thermoformed trays are indispensable for packaging fresh meat, poultry, bakery goods, produce, and ready-to-eat meals, where modified atmosphere packaging (MAP) extends shelf life and minimizes food waste. Their ability to accommodate product-specific cavities and ensure superior product visibility makes them the backbone of retail-ready packaging. Furthermore, the industry’s pivot toward rPET-based trays enhances recyclability and aligns with global sustainability goals, ensuring that trays remain the largest and most future-proof product category within thermoforming.

Food & Beverages Control the Majority Market Share by End-Use in the Rigid Thermoform Plastic Packaging Industry

The food and beverages sector accounts for a commanding 60% share, making it the overwhelming driver of thermoform plastic packaging demand. The ability of thermoformed solutions to combine barrier protection, clarity, and cost efficiency is unmatched for fresh food categories where shelf life and presentation are critical. High-speed thermoforming processes deliver mass volumes at competitive costs, while MAP-enabled trays and lightweight clamshells directly address consumer and retailer needs. A significant driver is the integration of recycled PET (rPET) to meet circular economy mandates, making this sector both the largest consumer and the testing ground for innovation in rigid thermoform plastic packaging.

European Union: PPWR and ESPR Driving Recyclability and Reuse in Thermoformed Packaging

The European Union rigid thermoform plastic packaging market is undergoing a transformation under the Packaging and Packaging Waste Regulation (PPWR), which took effect in February 2025. The regulation mandates that all plastic components in packaging must contain specified minimum percentages of post-consumer recycled content by January 2030, accelerating the transition toward circularity. It also sets reuse targets across sectors, directly influencing demand for reusable thermoformed formats such as cups, trays, and bottles.

In parallel, the Ecodesign for Sustainable Products Regulation (ESPR) introduces the Digital Product Passport from mid-2024, creating full transparency of origin and compliance across packaging supply chains. Industry leaders are actively adjusting, with Amcor reporting that 95% of its rigid packaging portfolio is already recyclable, underscoring the region’s focus on aligning design with recyclability. Meanwhile, the EU’s PFAS restrictions in food contact packaging (effective August 2026) are catalyzing the development of new barrier technologies for thermoformed containers. Additionally, Deposit Return Systems (DRS) are being scaled across member states to secure high-quality recycled inputs, vital for sustaining thermoformed rigid plastics.

United States: EPR Expansion and PCR Content Adoption Reshaping Thermoform Packaging Market

The United States rigid thermoform plastic packaging market is defined by a growing regulatory push and corporate innovation. Extended Producer Responsibility (EPR) laws, already passed in seven states including Maryland, require Producer Responsibility Organizations (PROs) to fund up to 90% of packaging waste management by 2030, creating financial and operational incentives for circular packaging systems.

On the innovation front, Berry Global introduced a customizable rectangular bottle using up to 100% post-consumer recycled (PCR) plastic, catering to the beauty, home, and personal care industries. Similarly, Chlorophyll Water’s adoption of 100% rPET bottles, making it the first U.S. bottled water brand with Clean Label Project Certification, demonstrates the growing role of rigid thermoform packaging in sustainability positioning. The U.S. market is also preparing for closure-retention mandates, fueling demand for rigid thermoform containers with tethered caps that combine compliance, convenience, and litter reduction. With federal support through the Infrastructure Investment and Jobs Act, advanced recycling facilities are being scaled, strengthening the domestic PCR supply chain for thermoform packaging.

China: Policy Enforcement and Premium Consumer Demand Fueling Thermoform Packaging Growth

The China rigid thermoform plastic packaging market is rapidly evolving under the government’s “14th Five-Year Plan”, which emphasizes plastic pollution control and green development. From June 1, 2025, new regulations mandate that express delivery companies use eco-friendly, reduced, or reusable packaging, driving adoption of thermoformed plastic trays and containers in e-commerce and logistics.

At the same time, premiumization in food and beverage consumption is spurring demand for high-quality thermoform packaging with superior barrier properties. Multinational and domestic players alike are scaling solutions; for example, Coca-Cola’s Hong Kong operations now rely on 100% rPET bottles produced in China, a signal of increasing local closed-loop capability. The government is also incentivizing remanufacturing and tax-supported investments in green technologies, encouraging the integration of advanced thermoform designs into mainstream applications.

India: EPR Mandates and Food Safety Standards Expanding Thermoform Packaging Applications

The India rigid thermoform plastic packaging market is gaining momentum under the Plastic Waste Management (Amendment) Rules, 2024, which prioritize Extended Producer Responsibility (EPR) for producers, importers, and brand owners. From April 1, 2025, PIBOs must incorporate at least 30% recycled content in rigid plastic packaging, directly impacting thermoformed trays, bottles, and clamshells.

A pivotal development came in May 2025, when the Food Safety and Standards Authority of India (FSSAI) issued guidelines for food-grade rPET, introducing mandatory labeling and logo requirements to enhance consumer trust. This is particularly critical for dairy, beverages, and ready-to-eat segments where thermoform plastics are widely used. Additionally, India’s ethanol-blended fuel program is driving demand for HDPE jerrycans and rigid thermoformed containers. The PM Gati Shakti plan, with its focus on cold-chain infrastructure, is further boosting demand for PET preforms and thermoformed solutions in dairy and juice packaging.

Japan: Circular Economy Laws and Bio-Based Innovation Transforming Thermoform Packaging

The Japan rigid thermoform plastic packaging market is shaped by the Plastic Resource Circulation Strategy, which requires all packaging to be reusable or recyclable by 2025. The country is also targeting 2 million tons of bio-polypropylene (bio-PP) annually by 2030, enhancing renewable inputs for thermoform production.

The Plastic Resource Circulation Promotion Law (2025) mandates redesign of 12 categories of single-use plastics, incentivizing the transition to rigid thermoform alternatives. Industry collaborations are pivotal; LyondellBasell and Shiseido, with Futamura Chemical and Iwatani, are embedding bio-based PP into cosmetic packaging, a key growth segment. Additionally, Coca-Cola Bottlers Japan Inc. (CCBJI) has introduced a new aseptic production line in Aichi Prefecture, capable of producing 600 small PET bottles per minute, underscoring the demand for efficient thermoform bottle formats in beverages.

Brazil: Reverse Logistics and Solid Waste Law Reinforcing Thermoform Packaging Market

The Brazil rigid thermoform plastic packaging market is regulated by the National Solid Waste Policy (PNRS), which emphasizes reuse, recycling, and responsible disposal. A landmark change was Law No. 15,088 (January 2025), banning imports of solid waste including plastics, aimed at strengthening domestic recycling and sustainability practices.

The government is investing heavily in reverse logistics systems, obligating producers to manage post-consumer thermoform packaging waste. This has encouraged local companies to expand recycling-friendly rigid packaging formats. Food processing and retail industries are increasing adoption of MAP (Modified Atmosphere Packaging) and vacuum-sealed thermoformed trays, enhancing shelf life and freshness retention. Together, these measures position Brazil as a growing hub for sustainable rigid thermoform packaging solutions in Latin America.

Rigid Thermoform Plastic Packaging Market Report Scope

Rigid Thermoform Plastic Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$40.2 Billion

|

|

Market Size (2034)

|

$62.9 Billion

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

By Material (PET, PP, PS, PE, PVC), By Product Type (Trays, Clamshells, Blister Packs, Containers & Lids, Cups & Bowls), By End-Use Industry (Food & Beverages, Healthcare & Pharmaceuticals, Cosmetics & Personal Care, Electronics, Consumer Goods, E-commerce)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global, Inc., Huhtamaki Oyj, Sonoco Products Company, Sealed Air Corporation, Plastipak Holdings, Inc., DS Smith Plc, Mondi Group, Pactiv Evergreen Inc., Silgan Holdings Inc., Alpla Group, Placon Corporation, Anchor Packaging, Inc., Graham Packaging, Greiner Packaging International GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Rigid Thermoform Plastic Packaging Market Segmentation

By Material

By Product Type

- Trays

- Clamshells

- Blister Packs

- Containers & Lids

- Cups & Bowls

By End-Use Industry

- Food & Beverages

- Healthcare & Pharmaceuticals

- Cosmetics & Personal Care

- Electronics

- Consumer Goods

- E-commerce

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Rigid Thermoform Plastic Packaging Market

- Amcor plc

- Berry Global, Inc.

- Huhtamaki Oyj

- Sonoco Products Company

- Sealed Air Corporation

- Plastipak Holdings, Inc.

- DS Smith Plc

- Mondi Group

- Pactiv Evergreen Inc.

- Silgan Holdings Inc.

- Alpla Group

- Placon Corporation

- Anchor Packaging, Inc.

- Graham Packaging

- Greiner Packaging International GmbH

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive research methodology to deliver precise insights into the global rigid thermoform plastic packaging market. Our analysis integrates extensive secondary research, including corporate filings, sustainability disclosures, regulatory documents, industry reports, and trade publications, with primary interviews involving manufacturers, brand owners, recyclers, and distributors across food & beverages, healthcare, cosmetics, e-commerce, and consumer goods sectors. Market sizing and forecasting account for materials (PET, PP, PS, PE, PVC), product types (trays, clamshells, cups, bowls, containers, blister packs), and regional regulations such as the EU PPWR and ESPR, U.S. EPR laws, India’s Plastic Waste Management rules, China’s green packaging mandates, Japan’s Circular Economy Strategy, and Brazil’s PNRS. Our methodology also evaluates sustainability-driven innovation, including rPET and rPP adoption, lightweighting, high-barrier monomaterial thermoforms, and In-Mold Labeling (IML), alongside technological upgrades and operational efficiency strategies. This integrated approach ensures industry professionals gain a complete understanding of competitive dynamics, regulatory impacts, market opportunities, and investment strategies shaping growth in the rigid thermoform plastic packaging sector.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.