Thermoform Packaging Market Overview: Growth Driven by Food and Sustainable Materials

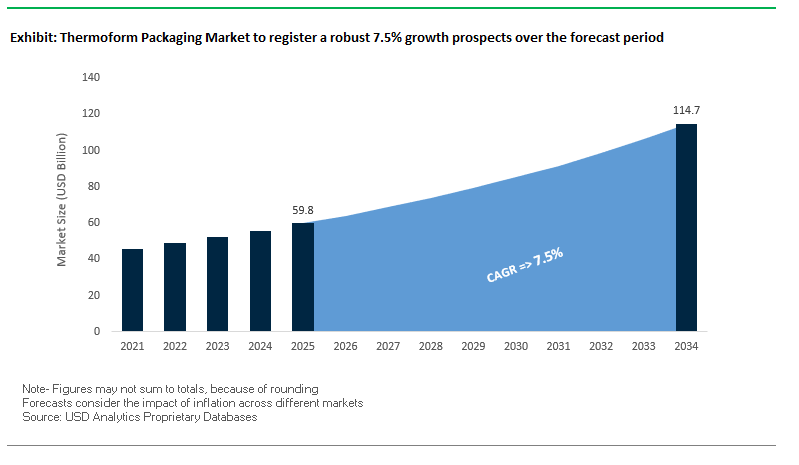

The Global Thermoform Packaging Market is valued at $59.8 billion in 2025 and is projected to reach $114.7 billion by 2034, expanding at a strong CAGR of 7.5%. This growth is fueled by the food and beverage sector’s reliance on thermoformed trays, clamshells, and containers, where consistent quality, shelf-life protection, and cost-efficiency are non-negotiable. With rising consumer expectations for convenience, safety, and sustainability, thermoform packaging is evolving to integrate post-consumer recycled (PCR) content and bio-based polymers.

Plastics, particularly PET and PP, continue to dominate this industry thanks to their barrier properties, affordability, and versatility. At the same time, automation in warehouses and distribution centers is making thermoform packaging indispensable, as its uniformity and light weight enable seamless integration with high-speed automated systems.

For professionals and buyers, this market answers pressing questions about how packaging can enhance brand value, reduce environmental impact, and align with global regulatory trends. Companies that adopt circular business models and invest in bio-based innovations are well-positioned to capture future demand.

Key Insights for Industry Professionals

- Plastics’ dominance (PET and PP) continues due to strong barrier properties and versatility.

- Food and beverage demand drives the largest share, particularly in ready meals, bakery, and fresh produce.

- Sustainability transition is accelerating with PCR content and bio-based materials gaining traction.

- Automation compatibility makes thermoform packaging critical for efficiency in global supply chains.

Market Analysis: Recent Industry Developments in Thermoform Packaging

The thermoform packaging sector has seen high-value acquisitions, portfolio realignments, and product innovations over the past two years, shaping a more consolidated and sustainable industry. In August 2025, Sealed Air Corporation launched its Instapak smart foam solution, designed for e-commerce fulfillment, reinforcing its shift toward automation-enabled packaging. Also in July 2025, Sonoco invested $30 million to expand adhesives and sealants capacity, strengthening its position in flexible and rigid packaging. That same month, Amcor expanded its healthcare packaging network in Costa Rica, enhancing its reach in Latin America.

Strategic consolidation remains a defining feature. In April 2025, Novolex acquired Pactiv Evergreen in a $6.7 billion deal, creating a new leader in food and beverage packaging across North America. In the same month, Sonoco sold its thermoformed and flexibles packaging unit to TOPPAN Holdings for $1.8 billion, realigning focus on its core businesses and high-growth cold chain packaging. Earlier in March 2025, Constantia Flexibles partnered with Aluflexpack AG, bolstering its premium flexible packaging leadership.

Sustainability-driven innovation continues to gain recognition. In January 2025, Neopac’s Polyfoil® Mono-Material Barrier Tube received the prestigious WorldStar Award for its recyclable, high-barrier design. Earlier in August 2024, Pactiv Evergreen launched Recycleware® Reduced-Density Polypropylene (RDPP) trays, a sustainable alternative to foam polystyrene, approved by the Association of Plastic Recyclers (APR).

Strategic Trends and Growth Opportunities Driving the Global Thermoform Packaging Market

Strategic Reshoring and Investment in North American Production Capacity

The thermoform packaging industry is experiencing a significant trend of reshoring, with major manufacturers investing heavily to expand production capabilities within North America. This strategy is primarily motivated by supply chain resilience, proximity to key clients, and supportive government policies. Leading firms such as Amcor have upgraded facilities in Oshkosh, Wisconsin, incorporating Class 7 cleanroom automation to meet rising healthcare and pharmaceutical demand. Government incentives under the U.S. Inflation Reduction Act and Infrastructure Investment and Jobs Act further encourage domestic manufacturing, creating favorable conditions for investment. Companies like Direct Pack Inc. are strategically expanding operations in Mexico to reduce dependency on complex global supply chains, ensuring quicker response times and reliable supply for North American customers. This reshoring trend underscores the critical importance of regional production in securing supply chain continuity and enhancing collaboration with clients in sensitive sectors like fresh food and healthcare.

Development of High-Barrier Mono-Material Thermoformed Structures

There is a critical opportunity to innovate high-barrier, mono-material thermoformed packaging that preserves shelf-life and barrier properties while being fully recyclable. Traditional multi-layer structures are challenging to recycle due to incompatible material layers, particularly in food and pharmaceutical applications. Companies like Coexpan are leading the way with mono-material polypropylene trays that maintain oxygen and moisture protection while simplifying recycling. Academic and industry collaborations are exploring advanced biopolymers and nanocomposite films to create recyclable structures with barrier properties equivalent to multi-layer plastics. Growing corporate commitments from companies like Unilever and Nestlé to fully recyclable packaging further amplify demand for high-performance, sustainable thermoform solutions. This opportunity allows packaging manufacturers to address regulatory pressures and environmental concerns while meeting functional performance requirements.

Integration of Smart Features and Advanced Automation

Thermoform packaging is increasingly evolving into a digital platform, presenting opportunities to embed smart features like NFC tags, QR codes, and RFID during manufacturing. This integration enhances traceability, consumer engagement, and supply chain efficiency. In pharmaceuticals, NFC-enabled blister packs provide a unique digital identity for each unit, improving anti-counterfeiting measures and supply chain security. For consumer goods, QR codes on thermoformed trays can educate users with nutritional data, recipes, and traceability information, strengthening brand transparency. In B2B applications, embedded RFID tags facilitate real-time tracking of sensitive components, particularly in electronics, optimizing inventory management and reducing manual labor costs. By combining automation with smart technology, thermoform packaging transforms from a passive container into a value-added product that enhances operational efficiency and customer interaction.

Competitive Landscape: Leading Companies in the Global Thermoform Packaging Industry

The thermoform packaging industry is characterized by intense competition among global giants and specialized innovators. Companies are differentiating themselves by investing in sustainable materials, global expansions, and integrated service offerings.

Pactiv Evergreen (Now part of Novolex): Expanding Sustainable Meat Trays

Pactiv Evergreen, now under Novolex, is a major player in North America with a broad portfolio of meat trays, dairy tubs, and clamshells. In August 2024, it launched Recycleware® RDPP meat trays, recognized by the APR for recyclability, replacing non-recyclable foam polystyrene. Its vertical integration ensures quality and efficiency, positioning it as a leader in circular food packaging solutions.

Amcor plc: Leveraging Global Scale for Thermoform Leadership

Amcor is a global powerhouse in both rigid and flexible packaging, with thermoform offerings that include cups, lids, and trays for food and healthcare. Its 2024–2025 acquisition of Berry Global created a global juggernaut in packaging, widening its healthcare and consumer portfolio. With AmPrima™ recycle-ready solutions and in-house design-to-commercialization capabilities, Amcor is advancing sustainable thermoform innovations at scale.

Sonoco Products Company: Reshaping Portfolio with Strategic Divestments

Sonoco has historically provided thermoformed solutions across food, healthcare, and industrial packaging. In April 2025, it divested its thermoformed and flexibles unit to TOPPAN Holdings, worth $1.8 billion, streamlining its portfolio to focus on core strengths like cold chain solutions. With its ISC Labs® testing services, Sonoco continues to provide validated packaging for pharmaceutical and biologics logistics.

Placon Corporation: Driving Circular PET Thermoforming Innovation

Placon, a North American leader, is known for its EcoStar® post-consumer recycled PET material. It was the first thermoforming company (2011) to open an in-house recycling center, enabling closed-loop sustainability. Its flagship Crystal Seal® and Fresh ’n Clear® trays are widely used in food and retail, combining functionality with eco-responsibility. Placon’s commitment to circular PET packaging makes it a sustainability pioneer.

Constantia Flexibles Group GmbH: Reinforcing Sustainability in Premium Segments

Constantia Flexibles specializes in high-barrier laminates and flexible packaging, often used in conjunction with rigid formats. In 2025, it received two WorldStar Awards for sustainable packaging, including its EcoPeelCover and EcoLamHighPlus solutions. Its acquisition of Aluflexpack AG in March 2025 reflects its ambition to strengthen its premium pharmaceutical and food packaging portfolio, further enhancing its global leadership.

Thermoform Packaging Market Share Insights

Blister Packaging Holds the Largest Market Share by Product Type in Thermoform Packaging

Blister packaging leads the thermoform packaging industry with 35% of the market, a position cemented by its critical role in pharmaceuticals and healthcare. Its dominance lies in its ability to deliver unit-dose accuracy, tamper-evidence, and high-barrier protection against moisture and contamination. For chronic disease management, blister packs also support patient adherence by organizing doses, which directly impacts health outcomes. With the global expansion of biologics and OTC drugs, blister packaging remains the default choice for compliance-driven pharmaceutical applications, anchoring its leadership despite sustainability concerns around multi-material laminates.

Food and Beverages Lead Thermoform Packaging Market Share by End-Use

The food and beverages industry represents 40% of thermoform packaging demand, positioning it as the largest volume driver. This dominance is linked to the widespread use of thermoformed trays and containers for fresh produce, meat, poultry, and ready meals. Modified atmosphere packaging (MAP) extends product shelf life, while transparent rigid structures improve consumer trust by enhancing product visibility at retail. For high-volume grocery applications, thermoform packaging offers an unmatched combination of scalability, barrier functionality, and cost efficiency, making it indispensable to global food supply chains.

United States: Sustainability and Smart Packaging Driving Thermoform Packaging Growth

The U.S. thermoform packaging market is experiencing strong growth, propelled by rising consumer demand for sustainable and recyclable solutions, particularly in the food, beverage, and medical device sectors. The adoption of bio-based plastics and cellulose-based films is increasing, supported by $52 million in funding from the U.S. Department of Energy for next-generation sustainable substrates. Technological advancements, such as smart packaging and serialization technologies, are accelerating compliance with the Drug Supply Chain Security Act (DSCSA), enabling precise track-and-trace systems to prevent counterfeiting and ensure patient safety.

The pharmaceutical sector is a major driver, with a growing need for user-friendly, portable packaging like blister packs for single-dose medications to support home-based treatments. Companies like Amcor and Placon are innovating with high-barrier, recyclable films and inert trays that reduce carbon footprint while maintaining product safety. Regulatory oversight by the FDA, including tamper-evident packaging, child-resistant closures, and clear labeling, continues to shape the market, encouraging manufacturers to deliver secure, sustainable, and compliant thermoform packaging solutions.

Germany: Circular Economy and Regulatory Compliance Boost Thermoform Packaging

The German thermoform packaging market is shaped by stringent regulations, such as the EU Packaging and Packaging Waste Regulation (PPWR, 2025), which mandates the adoption of eco-friendly and highly recyclable packaging. Germany’s leadership in the circular economy is reinforced by the Packaging Act (Verpackungsgesetz), which makes producers responsible for the entire life cycle of their packaging, fostering innovation in mono-material films like polyethylene (PE) and polypropylene (PP) to enhance recyclability.

Technological innovation is a hallmark of the German market, with converters embedding oxygen-barrier labels integrated with unique device identification (UDI) to maintain drug stability and comply with EU MDR regulations. Additionally, government mandates encouraging fiber-based alternatives over plastics are driving momentum in the thermoform segment. Germany also benefits from advanced packaging machinery, enabling high-speed, high-precision production for pharmaceuticals and other sensitive products, making the country a hub for efficient, sustainable, and compliant thermoform packaging solutions.

China: Green Transformation and Automation Fuel Thermoform Packaging Expansion

China’s thermoform packaging market is rapidly expanding due to the government’s dual carbon goals and policies promoting eco-friendly, reusable materials. Manufacturers are increasingly integrating automation, AI, and “5G plus industrial internet” technologies to optimize production processes, enhance efficiency, and improve flexible manufacturing capacity. Sustainability initiatives are gaining traction, particularly policies targeting the reduction of non-degradable plastics by 2025, which is boosting demand for paper-based and recyclable thermoform alternatives.

The growth of domestic e-commerce platforms has also fueled demand for secure, tamper-proof, and lightweight packaging, especially in electronics and medical devices. Regulatory reforms, including the June 2025 announcement by China’s National Medical Products Administration (NMPA) on Good Manufacturing Practice for Drugs, require pharmaceutical excipient and packaging manufacturers to maintain robust quality management systems, driving the adoption of high-standard thermoform packaging solutions across the country.

India: Government Incentives and Rising Demand Drive Thermoform Packaging Adoption

India’s thermoform packaging market is supported by the “Make in India” and “Zero Effect Zero Defect” initiatives, encouraging domestic manufacturing and high-quality production standards. The Production Linked Incentive (PLI) Scheme for the food processing industry, with an outlay of INR 10,900 crore, promotes standardized, high-quality packaging solutions, including thermoformed trays, clamshells, and containers.

Regulatory measures such as the Plastic Waste Management (Amendment) Rules are fostering a shift towards eco-friendly packaging materials, while Food Safety and Standards (Packaging and Labelling) Regulations ensure compliance for food-grade applications. Rising disposable incomes, urbanization, and consumer preference for convenient, single-serve, and on-the-go products are further driving the adoption of thermoform packaging. Together, these factors are propelling India’s market towards sustainable, high-quality, and consumer-focused thermoform packaging solutions.

Thermoform Packaging Market Report Scope

Thermoform Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$59.8 Billion

|

|

Market Size (2034)

|

$114.7 Billion

|

|

Market Growth Rate

|

7.5%

|

|

Segments

|

By Material Type (Plastics, Paper & Paperboard, Aluminum, Bioplastics), By Product Type (Blister Packaging, Clamshell Packaging, Skin Packaging, Trays & Lids, Containers), By End-Use Industry (Food & Beverages, Pharmaceuticals & Healthcare, Electronics, Personal Care & Cosmetics, Other End-Use Industries), By Technology (Vacuum Forming, Pressure Forming, Mechanical Thermoforming, Matched Mold Thermoforming)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global Inc., Sonoco Products Company, WestRock Company, DS Smith plc, Huhtamaki Oyj, Pactiv LLC, Constantia Flexibles, Sealed Air Corporation, Genpak, LLC, Placon, Greiner Packaging International GmbH, D&W Fine Pack LLC, Anchor Packaging, LLC, Mondi Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Thermoform Packaging Market Segmentation

By Material Type

- Plastics

- Paper & Paperboard

- Aluminum

- Bioplastics

By Product Type

By End-Use Industry

- Food & Beverages

- Pharmaceuticals & Healthcare

- Electronics

- Personal Care & Cosmetics

- Other End-Use Industries

By Technology

- Vacuum Forming

- Pressure Forming

- Mechanical Thermoforming

- Matched Mold Thermoforming

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Thermoform Packaging Market

- Amcor plc

- Berry Global Inc.

- Sonoco Products Company

- WestRock Company

- DS Smith plc

- Huhtamaki Oyj

- Pactiv LLC

- Constantia Flexibles

- Sealed Air Corporation

- Genpak, LLC

- Placon

- Greiner Packaging International GmbH

- D&W Fine Pack LLC

- Anchor Packaging, LLC

- Mondi Group

* List Not Exhaustive

Methodology

USDAnalytics has conducted an extensive and structured analysis of the global Thermoform Packaging Market, employing a combination of primary and secondary research to deliver actionable insights for industry professionals. Our approach integrates interviews with key stakeholders across packaging manufacturing, food and beverage, pharmaceuticals, and logistics sectors, alongside detailed examination of corporate filings, strategic acquisitions, product innovations, and sustainability initiatives. Market sizing and forecasts are derived from historical trends, material innovations in plastics, bioplastics, paper, and aluminum, and the rising adoption of automated and high-barrier thermoforming systems. Segmentation covers material type, product type, end-use industry, and technology, while regional analysis spans the U.S., Germany, China, and India, evaluating regulatory frameworks, sustainability mandates, and reshoring initiatives. Competitive intelligence profiles leading players, including Amcor, Pactiv Evergreen, Sonoco, Placon, and Constantia Flexibles, highlighting investments in automation, smart features, and eco-friendly packaging. By synthesizing these factors, USDAnalytics provides a comprehensive, professional overview of market dynamics, growth opportunities, and strategic imperatives for decision-makers seeking high-performance, sustainable, and technologically advanced thermoform packaging solutions.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.