Sealing and Strapping Packaging Tapes Market Size, Overview, and Growth Outlook (2025–2034)

Sealing and Strapping Packaging Tapes Market Set to Reach $30.7 Billion by 2034 Fueled by E-Commerce and Sustainability Trends

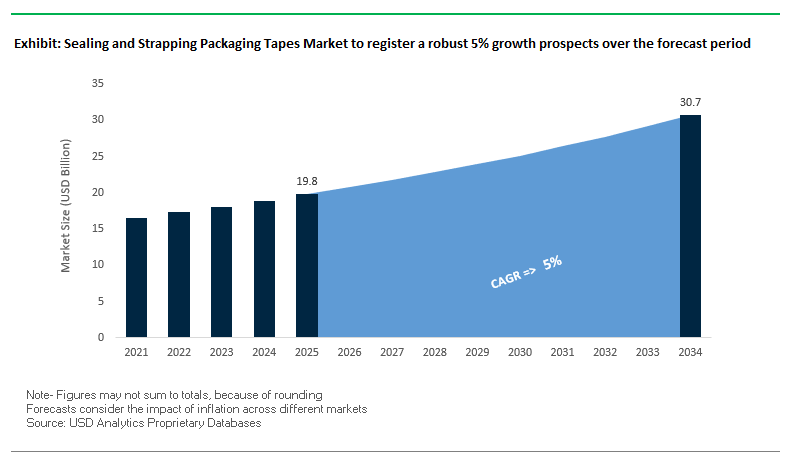

The global sealing and strapping packaging tapes market is expected to grow from $19.8 billion in 2025 to $30.7 billion by 2034, at a CAGR of 5%. This growth is driven by rapid expansion of e-commerce, demand for durable and sustainable tapes, and technological innovation in smart packaging solutions. Industry professionals can leverage these insights to enhance supply chain efficiency, adopt eco-friendly solutions, and capitalize on emerging applications in logistics and industrial sectors.

Key Insights for market participants:

- E-commerce and Logistics Demand: Over 55% of the market volume is consumed by logistics and warehousing, with continuous growth projected due to e-commerce expansion.

- Acrylic Adhesive Dominance: Acrylic adhesives lead due to excellent durability, UV resistance, and reliable bonding across diverse climates.

- Sustainable Materials Shift: Companies like Intertape Polymer Group (IPG) achieved 75% of revenue from recyclable, reusable, or compostable products, surpassing sustainability goals a year early.

- Rising Demand for Smart Tapes: Emerging smart tapes with integrated sensors for tamper-evidence and structural monitoring are gaining traction for high-value shipments.

- Opportunities in Industrial Automation: Integration with case-sealing machines and automated packaging lines provides operational efficiency and real-time data monitoring.

- Innovation in Customization: Custom-printed tapes enhance brand visibility while maintaining high-performance sealing standards.

The market is poised at the intersection of logistics efficiency, sustainability, and smart technology adoption, making it a key growth sector for packaging professionals.

Market Analysis: Strategic Sustainability and Technological Innovations Are Driving Growth in Packaging Tapes

The sealing and strapping tapes market has seen a strong push toward sustainability and operational efficiency. In August 2025, Intertape Polymer Group (IPG) achieved TRUE Gold Zero Waste Certification at its Chicago facility, highlighting industry leadership in eco-conscious practices. In July 2025, Shurtape Technologies launched its AP 251 Acrylic Packaging Tape, providing brand messaging capabilities and robust sealing for shipping boxes. That same month, a leading European adhesive company acquired a U.S.-based specialist, strengthening its footprint in North American industrial and medical tape markets.

Product innovation continues to shape market dynamics. In May 2025, IPG launched a polyethylene surface protection film tape, catering to manufacturing and shipping applications. April 2025 saw Shurtape introduce a curbside-recyclable paper packaging tape, further advancing sustainable packaging solutions. In February 2025, a merger between two European adhesive companies created a new leader in high-performance industrial tapes, enhancing competitive capabilities.

Technological integration and recognition are additional market drivers. In October 2024, IPG launched its iTRACK™ Data Collection System for case-sealing machines, improving automation efficiency and real-time monitoring. The market also witnessed recognition of excellence, as November 2024 saw a major tape manufacturer awarded “Vendor of the Year” by a leading industry cooperative, reflecting superior customer service and operational performance.

Sealing and Strapping Packaging Tapes Market: Emerging Trends and High-Value Opportunities

Rapid Adoption of Paper-Based and Recyclable Tape Solutions

The sealing and strapping packaging tapes market is undergoing a structural shift toward paper-based and recyclable tape solutions, driven by stringent Extended Producer Responsibility (EPR) frameworks. The EU’s Packaging and Packaging Waste Regulation (PPWR), enforced in February 2025, mandates that all packaging placed on the market must be recyclable in an economically viable way by 2030. This directive, along with similar rules in Asia-Pacific and North America, is pushing companies to adopt recyclable tapes that integrate seamlessly into paper recycling streams. Unlike traditional plastic tapes, which can contaminate fibers and reduce recyclability, paper-based tapes enable closed-loop recycling with corrugated boxes, simplifying waste handling and avoiding financial penalties. Corporates and e-commerce leaders are accelerating this transition. For example, Amazon’s July 2025 announcement highlighted its switch to paper-based sealing tapes across fulfillment centers as part of its 2030 net-zero carbon roadmap. Logistics providers are following suit, recognizing that the elimination of plastic-based tapes is not only a regulatory compliance measure but also a brand-enhancing sustainability strategy that resonates with eco-conscious consumers.

Strategic Investment in Automation-Compatible High-Performance Tapes

With the explosion of e-commerce and logistics, automation-compatible sealing and strapping tapes are becoming a core operational requirement. Modern fulfillment centers operate at extremely high throughput, where any downtime from tape failure can translate into significant costs. A 2025 research report emphasized that these tapes must deliver a high initial tack, consistent unwind tension, and uniform thickness to perform reliably on automated lines. High-performance tapes can seal thousands of cartons per roll, minimizing line interruptions and reducing material changeovers. Case studies from large automated hubs show that consistent, automation-ready tapes directly reduce material waste and labor hours, reinforcing their cost-effectiveness despite higher unit prices. The strategic investments by leading manufacturers in developing machine-optimized tapes highlight their importance in reducing operational inefficiencies, meeting same-day delivery expectations, and sustaining the rapid growth of e-commerce supply chains worldwide.

Development of Bio-Based and Compostable Adhesive Formulations

The adhesive component of tapes presents one of the biggest sustainability challenges—and therefore, one of the largest opportunities. Traditional petroleum-based adhesives are non-biodegradable, hindering recycling and increasing environmental impact. Innovation is accelerating in bio-based adhesives derived from natural rubber and plant-based resins, creating solutions that are both functional and compostable. A March 2025 industry article on compostable adhesives highlighted new formulations certified for home composting, capable of decomposing naturally while maintaining strong adhesion during use. These adhesives not only align with consumer expectations for sustainable packaging but also create a competitive differentiator for brands seeking circular packaging credentials. With major food and consumer goods companies demanding certified compostable sealing solutions, adhesive innovation is set to reshape the product mix in the sealing and strapping tape market, opening avenues for new entrants and R&D-driven partnerships.

Integration of Smart and Track-and-Trace Features

Sealing and strapping tapes are evolving from simple utility products into smart packaging enablers. By integrating QR codes, serialized IDs, or digital watermarks directly onto tape surfaces, companies can transform every package into a trackable and interactive asset. This integration provides multiple benefits: authentication for brand protection, consumer engagement through scannable content, and full supply chain traceability. A late 2024 smart packaging case study highlighted how brands used serialized tape identifiers to combat counterfeiting while simultaneously providing consumers with product provenance. From a logistics perspective, embedded IDs enable end-to-end visibility, allowing companies to monitor package movement, detect diversion, and optimize delivery routes. As industries like pharmaceuticals, electronics, and luxury goods face mounting risks of counterfeiting, smart tape adoption will accelerate, providing both a security layer and a data-driven platform for supply chain intelligence.

Competitive Landscape: Leading Tape Manufacturers Are Shaping the Future of Sealing, Strapping, and Sustainable Packaging

The global sealing and strapping packaging tapes market is highly competitive, driven by companies investing in innovation, sustainability, and advanced adhesive technologies. Key players are providing eco-friendly solutions, smart tapes, and high-performance products for industrial, e-commerce, and logistics applications.

3M Company: Innovating Adhesive Tapes for High-Performance Industrial and Commercial Applications

3M offers a diverse portfolio of sealing and strapping tapes under Scotch® and Scotch-Weld™ brands, ranging from general-purpose carton sealing to high-performance aerospace tapes. The company’s VHB™ tapes provide permanent bonding as an alternative to mechanical fasteners, and specialty tapes address thermal management, EMI shielding, and electrical insulation. R&D capabilities and intellectual property allow 3M to develop custom solutions for complex industrial applications, ensuring durability, reliability, and innovation leadership.

tesa SE: Leading Sustainability and Advanced Sealing Solutions for Industrial Applications

tesa SE manufactures adhesive tapes for industrial and professional applications, including filmic, paper, and reinforced tapes for secure carton sealing. The company focuses on sustainable, bio-based tapes without compromising performance. Recent innovations include high-temperature-resistant sealing tapes and flying splice tapes to improve production efficiency. Durable and moisture-resistant, tesa tapes serve automotive, electronics, and food industries, combining sustainability with reliability.

Intertape Polymer Group Inc. (IPG): Integrating Sustainability with High-Performance Industrial Tape Solutions

IPG produces pressure-sensitive and water-activated paper and film tapes for logistics and industrial applications. In 2024, 75% of revenue came from recyclable, reusable, or compostable products, surpassing sustainability goals early. In August 2025, its Chicago facility achieved TRUE Gold Zero Waste Certification, and in October 2024, it launched iTRACK™ Data Collection System to optimize case-sealing automation. IPG combines tape products with automation solutions, offering tamper-evident and high-quality packaging for e-commerce and logistics.

Shurtape Technologies, LLC: Expanding Sustainable and Customizable Tape Solutions for Logistics and Industrial Applications

Shurtape Technologies offers acrylic, hot melt, and paper-based tapes, including AP 251 Acrylic Packaging Tape and Curbside Recyclable Paper Packaging Tape introduced in 2025. The company focuses on sustainability and brand customization while meeting evolving e-commerce and industrial requirements. Its products are widely used for carton sealing, HVAC, construction, and automotive applications, delivering durability and compliance with industry standards.

Nitto Denko Corporation: High-Performance Tapes for Specialized Industrial and Packaging Applications

Nitto Denko provides industrial and specialty tapes for carton sealing, bundling, thermal management, and electrical insulation. The company emphasizes R&D-driven innovation, developing tapes with specific functional properties for demanding applications. Nitto’s tapes are used in automotive, electronics, and medical sectors, offering reliability, durability, and advanced adhesive performance.

Sealing and Strapping Packaging Tapes Market Share Insights, 2025-2034

Carton Sealing Dominates Market Share by Application in the Sealing and Strapping Packaging Tapes Industry

Carton sealing commands 65% of the sealing and strapping tapes market, underscoring its universal role in securing corrugated shipping boxes across global industries. With e-commerce and omnichannel retail driving exponential growth in parcel volumes, polypropylene (PP) and acrylic-based sealing tapes have become the backbone of high-speed fulfillment centers and logistics networks. Increasingly, water-activated gummed paper tapes are penetrating the market due to their superior tamper resistance, recyclability, and compliance with sustainability mandates. As corrugated box demand expands in both developed and emerging markets, carton sealing remains the most critical and volume-driven application of industrial tapes.

E-commerce and Logistics Lead Market Share by End-Use in the Sealing and Strapping Packaging Tapes Industry

E-commerce and logistics represent the largest end-use segment at 40%, reflecting the direct correlation between online shopping growth and demand for secure, durable sealing tapes. Billions of parcels shipped annually require high-speed, automated tape application that ensures package integrity throughout complex supply chains. Beyond simple sealing, the e-commerce sector increasingly demands tamper-evident, weather-resistant, and sustainable tape solutions to enhance consumer trust and reduce environmental impact. While food & beverage, building & construction, automotive, and pharmaceuticals each represent vital users with specialized requirements, e-commerce and logistics continue to set the pace for innovation and scale in the sealing and strapping packaging tapes industry.

United States: EPR Laws, Smart Tape Adoption, and Recycling Infrastructure Boost

The United States sealing and strapping packaging tapes market is being reshaped by regulatory and industry-led sustainability initiatives. Seven states, including Maryland, have passed Extended Producer Responsibility (EPR) laws, requiring a Producer Responsibility Organization (PRO) to finance 90% of packaging waste management costs by 2030. These policies are pushing brands to redesign packaging formats and accelerate the adoption of eco-friendly tapes. In parallel, the U.S. Environmental Protection Agency’s goal to raise the national recycling rate to 50% by 2030 is spurring investment in recycling infrastructure, particularly for pressure-sensitive adhesives used in strapping tapes.

Demand is strongest in logistics, e-commerce, and food & beverage industries, where high-performance strapping and sealing tapes are critical for withstanding automated warehousing and complex supply chains. A defining trend is the rise of smart packaging tapes with RFID and QR technologies, providing real-time inventory visibility and tamper evidence. This is particularly valuable in pharmaceuticals and high-value e-commerce products. Infrastructure improvements, backed by the Infrastructure Investment and Jobs Act, are further encouraging local production and recycling of adhesive-backed tapes, positioning the U.S. as a leader in smart and sustainable tape solutions.

European Union: PPWR, ESPR, and Material Innovation Driving Circular Economy Adoption

The European Union sealing and strapping tapes market is being significantly shaped by the Packaging and Packaging Waste Regulation (PPWR), which took effect in February 2025. The regulation enforces reuse and recycled content targets, accelerating the shift from multi-material laminates to mono-material and paper-based tapes that are easier to recycle. Complementing this, the Ecodesign for Sustainable Products Regulation (ESPR), effective mid-2024, introduces a Digital Product Passport (DPP) to enhance traceability of adhesives, raw materials, and recyclability credentials.

By August 2026, the EU will enforce a ban on PFAS in food contact packaging, prompting innovation in adhesive technologies to ensure compliance while maintaining durability and strength. In Germany, a hub for precision engineering and high-performance industries, there is growing demand for specialized sealing tapes in automotive and electronics manufacturing, which require stringent quality and reliability standards. Collectively, these regulatory and industrial drivers are pushing the EU toward becoming a benchmark market for sustainable and high-performance strapping and sealing tapes.

China: E-Commerce Growth and Green Technology Incentives Reshaping Tape Market

The China sealing and strapping packaging tapes market is advancing under the government’s 14th Five-Year Plan, which emphasizes plastic pollution control and green manufacturing. From June 1, 2025, express delivery companies are mandated to use eco-friendly, reduced, or reusable packaging, creating direct demand for sustainable sealing and strapping solutions. The scale of China’s e-commerce sector, with its need for lightweight, cost-effective, and durable tapes, is the single largest growth driver in the region.

The National Development and Reform Commission (NDRC) and the Ministry of Ecology and Environment (MEE) are working to reduce plastic waste, while tax incentives for green technology adoption are encouraging tape manufacturers to invest in recyclable and bio-based adhesive technologies. Major logistics players such as JDL Express and SF Express are deploying reusable circulation boxes, reinforcing the demand for high-strength strapping tapes that complement reusable systems. These combined regulatory and market trends are making China a hub for innovative, eco-friendly adhesive packaging tapes.

India: EPR Rules, Traceability Mandates, and Rising E-Commerce Driving Adoption

The India sealing and strapping packaging tapes market is strongly influenced by the Plastic Waste Management (Amendment) Rules, 2024, which emphasize Extended Producer Responsibility (EPR) for producers and brand owners. From July 1, 2025, all plastic packaging, including tapes, must be traceable through barcodes or QR codes, ensuring accountability across the value chain. While MSMEs are exempt from EPR obligations, the responsibility falls on larger manufacturers and importers, accelerating compliance-driven innovation in adhesive tapes.

A critical growth driver is India’s rapidly expanding e-commerce and organized retail sectors, which require reliable sealing and strapping solutions for secure last-mile delivery. With the country’s price-sensitive market, demand is growing for cost-effective yet durable tapes that balance affordability with recyclability. The regulatory focus on traceability and recycled content is expected to create opportunities for domestic and multinational players to introduce sustainable adhesive and strapping tape solutions tailored to India’s packaging ecosystem.

Japan: Plastic Resource Circulation Strategy and Advanced Tape Innovation

The Japan sealing and strapping tapes market is undergoing transformation under the Plastic Resource Circulation Strategy, which requires all plastic packaging to be recyclable or reusable by 2025. Additionally, the government aims to double renewable material usage by 2030 and enforce strict waste sorting regulations. The Plastic Resource Circulation Promotion Law (2025) further mandates the reduction or redesign of 12 single-use plastic products, directly impacting adhesive-based tapes.

Japanese companies are focusing on innovating with bio-based adhesives and compostable substrates to align with these circular economy goals. The country’s industrial sectors, including electronics and precision machinery, also demand high-performance strapping tapes with strong adhesive properties that maintain integrity under challenging storage and logistics conditions. This dual focus on sustainability and advanced material performance positions Japan as a pioneer in eco-innovative sealing and strapping packaging tapes.

Brazil: Reverse Logistics and Solid Waste Laws Driving Sustainable Tape Usage

The Brazil sealing and strapping packaging tapes market is governed by the National Solid Waste Policy (PNRS), which mandates a reverse logistics system holding producers accountable for post-consumer tape recycling and disposal. In January 2025, Law No. 15,088 came into effect, banning the import of plastic and other waste, compelling domestic industries to build localized recycling capacity and promote sustainable packaging solutions.

Brazil’s emphasis on reuse, recycling, and reduction is boosting demand for eco-friendly strapping tapes in food, beverage, and logistics sectors. With increasing consumer and regulatory pressure, manufacturers are investing in MAP (Modified Atmosphere Packaging) compatible adhesive tapes that extend the shelf life of food products while maintaining secure closures. Together, Brazil’s reverse logistics model and regulatory restrictions are pushing the country toward a circular economy framework in the sealing and strapping packaging tapes market.

Sealing and Strapping Packaging Tapes Market Report Scope

Sealing and Strapping Packaging Tapes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$19.8 Billion

|

|

Market Size (2034)

|

$30.7 Billion

|

|

Market Growth Rate

|

5%

|

|

Segments

|

By Material (PP, Paper, PVC, PET, Nylon), By Adhesive Type (Acrylic, Hot Melt, Rubber-based, Water-Activated), By Application (Carton Sealing, Bundling & Unitizing, Palletizing, Tamper-Evident Security), By End-Use Industry (E-commerce & Logistics, Food & Beverage, Automotive, Building & Construction, Healthcare & Pharmaceuticals, Electronics)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, Tesa SE, Intertape Polymer Group Inc., Nitto Denko Corporation, Shurtape Technologies, LLC, Avery Dennison Corporation, Mondi Group, Amcor plc, Sealed Air Corporation, Saint-Gobain Performance Plastics, Scapa Group Ltd., Lintec Corporation, Nichiban Co., Ltd., Berry Global, Inc., Greif, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Sealing and Strapping Packaging Tapes Market Segmentation

By Material

By Adhesive Type

- Acrylic

- Hot Melt

- Rubber-based

- Water-Activated

By Application

- Carton Sealing

- Bundling & Unitizing

- Palletizing

- Tamper-Evident Security

By End-Use Industry

- E-commerce & Logistics

- Food & Beverage

- Automotive

- Building & Construction

- Healthcare & Pharmaceuticals

- Electronics

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Sealing and Strapping Packaging Tapes Market

- 3M Company

- Tesa SE

- Intertape Polymer Group Inc.

- Nitto Denko Corporation

- Shurtape Technologies, LLC

- Avery Dennison Corporation

- Mondi Group

- Amcor plc

- Sealed Air Corporation

- Saint-Gobain Performance Plastics

- Scapa Group Ltd.

- Lintec Corporation

- Nichiban Co., Ltd.

- Berry Global, Inc.

- Greif, Inc.

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous and integrated research methodology to provide precise insights into the global sealing and strapping packaging tapes market. Our approach combines extensive secondary research, including industry reports, corporate sustainability disclosures, regulatory filings, and trade publications, with primary interviews involving tape manufacturers, adhesive technology experts, logistics operators, and end-user companies in e-commerce, industrial, and food & beverage sectors. Market sizing and forecasting incorporate detailed segmentation by material (PP, paper, PVC, PET, nylon), adhesive type (acrylic, hot melt, rubber-based, water-activated), application (carton sealing, bundling, palletizing, tamper-evident), and end-use industries, while accounting for regional dynamics such as EU PPWR and ESPR regulations, U.S. EPR laws, China’s green technology incentives, India’s traceability mandates, Japan’s Plastic Resource Circulation Strategy, and Brazil’s PNRS reverse logistics framework. The methodology also evaluates innovation trends in sustainable, bio-based, and compostable adhesives, automation-compatible high-performance tapes, smart and track-and-trace solutions, and brand-customized printed tapes. Competitive landscape analysis examines mergers, acquisitions, and product launches by industry leaders such as 3M, Tesa SE, Intertape Polymer Group, Shurtape Technologies, and Nitto Denko, enabling professionals to identify growth drivers, regulatory compliance strategies, and market opportunities within the evolving sealing and strapping tapes ecosystem.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.