Packaging Tapes Market to Reach $175.4 Billion by 2034 Driven by E-Commerce and Sustainability Demands

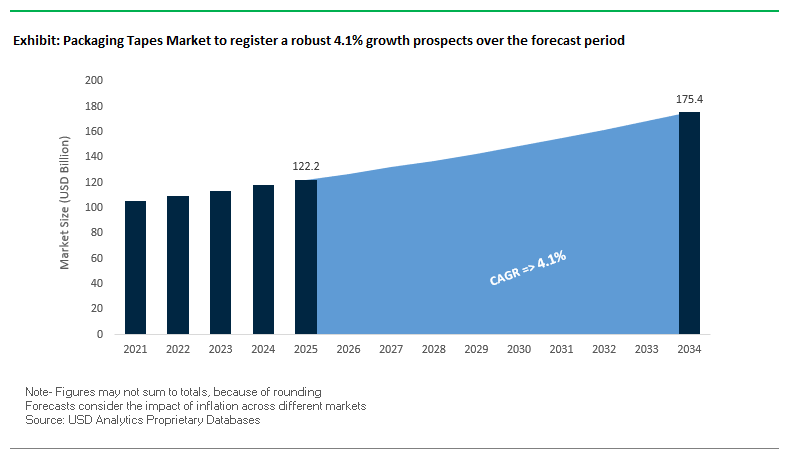

The Global Packaging Tapes Market is projected to grow from $122.2 billion in 2025 to $175.4 billion by 2034, representing a CAGR of 4.1%. The industry provides critical adhesive solutions that ensure the security, integrity, and efficiency of packages across supply chains. From carton sealing tapes to high-performance specialty tapes, packaging tapes are indispensable for logistics, e-commerce, and industrial sectors.

Key Insights for Industry Professionals:

- Sustainable Packaging Adoption: Growing demand for PCR-based tapes, paper backings, and water-based adhesives aligns with corporate ESG mandates and consumer expectations.

- Automation in E-Commerce Logistics: Tapes are increasingly engineered for high-speed case-sealing machines, enhancing throughput and reducing labor costs.

- Enhanced Security Features: Tamper-evident tapes with serial numbers or QR codes are critical for protecting high-value goods and pharmaceuticals.

- Digital Data Integration: Monitoring systems track tape usage, sealing defects, and operational efficiency, helping reduce waste and optimize end-of-line packaging.

- Innovation in Specialty Tapes: Development of filament, reinforced, and heat-resistant tapes addresses industry-specific challenges in industrial and logistics sectors.

Recent Strategic Developments in Packaging Tapes Highlight Sustainability, Innovation, and Market Consolidation

The Global Packaging Tapes Industry continues to evolve through technological innovation, sustainability initiatives, and strategic market moves. In August 2025, Intertape Polymer Group (IPG) achieved TRUE Gold Zero Waste Certification at its Chicago facility, underlining its commitment to circular economy practices. In July 2025, Shurtape Technologies launched the AP 251 Acrylic Packaging Tape, enhancing custom print clarity and UV resistance for branding applications.

In May 2025, Tesa SE introduced its tesa 60416 and 60418 adhesive solutions, featuring up to 60% recycled plastic content, demonstrating an industry-wide shift toward sustainable filmic tapes. April 2025 saw DIC Corporation establish a new sustainable coatings facility in Indonesia, supporting direct food contact materials and the growing demand for safe, eco-friendly packaging.

Sustainability and operational efficiency remained in focus with IPG’s TRUE Silver Certification in March 2025, and January 2025’s launch of Ahlstrom MasterTape® Cristal, a recyclable and compostable paper-based tape. Technological advancements include IPG’s October 2024 iTRACK™ Data Collection System, enabling real-time tracking of tape usage and sealing defects. Recognized in August 2024 by the Canadian Manufacturing Journal, IPG was named Large Enterprise Manufacturer of the Year, solidifying its leadership in sustainable and high-performance packaging solutions.

Trends and Opportunities Shaping the Future of the Packaging Tapes Market

Accelerated Shift to Water-Activated and Paper-Based Tapes

The packaging tapes market is undergoing a decisive transition from plastic-based solutions such as PVC and BOPP tapes to water-activated tapes (WAT) and paper-based alternatives, driven by both sustainability goals and security concerns. A large-scale e-commerce shipper study revealed that traditional pressure-sensitive tapes had a 3% claim rate due to failures or tampering, while packages sealed with WAT recorded only 0.2% claims, proving its superior tamper-evidence and bonding strength.

The shift also supports circular economy goals, as paper-based tapes simplify recycling by entering the paper stream without requiring separation. This enhances the overall recyclability of corrugated boxes, which is critical for brands with aggressive sustainability targets. Companies like Tesa have introduced certified bio-based paper tapes sourced from renewable forests, giving brands a certified alternative to fossil-fuel-based substrates. Additionally, WAT reduces material usage since a single strip provides a permanent seal, compared to multiple overlapping layers needed with plastic tapes. This improvement not only reduces material and labor costs but also lowers package failure risks across logistics networks.

Integration of On-Demand Printing for Automated Logistics

Another defining trend is the integration of on-demand printing technology into automated packaging lines, particularly in e-commerce and 3PL hubs. By printing variable data—such as barcodes, tracking numbers, and order IDs—directly onto the tape during sealing, companies eliminate the need for separate labeling steps. This enhances supply chain speed, reduces human error, and lowers overall costs.

On-demand printing also allows companies to cut warehousing costs by removing the need to stock large inventories of pre-printed tapes. This reduces waste from obsolete designs and offers greater operational flexibility for short-run and customized orders. Technology providers are responding with integrated tape dispensers and automated printing machinery that create end-to-end packaging solutions optimized for high-speed fulfillment. This trend reflects the industry’s push toward digitally enabled, flexible packaging systems designed for the complexities of global logistics.

Development of High-Performance Bio-Based Adhesives

One of the most promising opportunities in the packaging tapes market lies in replacing petroleum-based adhesives with bio-based and solvent-free alternatives. Companies like Henkel have already launched new adhesive systems derived from renewable resources, delivering comparable strength and bonding performance to conventional adhesives while reducing environmental impact.

Innovation is moving beyond sustainability to enhanced functionality. Biotechnology research is exploring enzyme-based adhesives for improved biodegradability and water-dispersible adhesives that can enable easier material separation during recycling or pulping. These developments support a circular economy framework, helping brands reduce waste and comply with tightening EPR (Extended Producer Responsibility) regulations across Europe and North America. With global CPG leaders embedding sustainability into procurement, the market for bio-based adhesive tapes is positioned for rapid, large-scale adoption.

Expansion of Smart Tapes with Integrated Tracking and Authentication

The integration of RFID, NFC, and printed security features into packaging tapes is creating new opportunities for supply chain traceability, brand protection, and consumer engagement. RFID-enabled tapes allow item-level visibility without line-of-sight scanning, enabling faster warehouse inventory management and real-time tracking across logistics networks.

For brand protection, invisible phosphorescent inks and tamper-evident water-activated tape seals provide both overt and covert layers of security. If a package is breached, the tape irreversibly damages the carton, offering an unmistakable indication of tampering. On the consumer-facing side, smart tapes can double as digital engagement platforms. QR codes or NFC-enabled adhesives link customers to product information, promotions, or authentication portals, turning a functional sealing medium into a branded, interactive experience.

Competitive Landscape of Packaging Tapes Shaped by Leaders Focusing on Innovation, Sustainability, and High-Performance Solutions

The global packaging tapes market is dominated by key players leveraging material science, adhesive technology, and digital printing expertise to deliver durable, high-performance, and eco-friendly solutions. These companies address demands for branding, security, automation, and sustainability across logistics and industrial applications.

3M: Leveraging a Century of Adhesive Innovation to Deliver High-Performance Packaging Tapes

3M combines advanced adhesive technology with durable backing materials under its Scotch® Brand. In July 2025, 3M celebrated 100 years of adhesive innovation and introduced ScotchBlue PROSharp Painter's Tape with Edge-Lock+ Technology. Its portfolio includes carton sealing tapes, reinforced tapes, water-activated tapes, and specialty adhesives designed for industrial and environmental demands. 3M focuses on material science-driven innovation to enhance efficiency, safety, and sustainability.

Tesa SE: Driving Sustainable and High-Performance Adhesive Solutions for Industrial Applications

Tesa SE, a subsidiary of Beiersdorf AG, specializes in adhesive solutions for industrial and packaging sectors. Recent launches include tesa 60416 and 60418 adhesives made from up to 60% recycled plastic, demonstrating its commitment to sustainability. Tesa offers carton sealing tapes, specialty tapes, and Softprint® foam tapes for flexographic printing, combining technology and service excellence to develop future-proof, eco-friendly packaging solutions.

Shurtape Technologies: Innovating PCR-Based Packaging Tapes for High-Performance and Security

Shurtape Technologies provides a diverse portfolio of high-performance tapes for industrial, professional, and consumer applications. In August 2025, it showcased secure and sustainable end-of-line tapes at PACK EXPO Las Vegas and launched AP 251 Acrylic Packaging Tape for enhanced branding. Its portfolio includes carton sealing tapes with hot melt, acrylic, and natural rubber adhesives, along with rAP 201 and rHP 235 tapes with high PCR content, emphasizing sustainability and operational performance.

Intertape Polymer Group (IPG): Leading Automation-Ready and Data-Driven Packaging Tape Solutions

IPG excels in carton-sealing tapes, water-activated tapes, and integrated packaging systems. Its Chicago facility achieved TRUE Gold Zero Waste Certification in August 2025, highlighting sustainability efforts. IPG’s iTRACK™ Data Collection System provides actionable insights on tape usage and sealing defects. Products include tamper-evident, printed, and high-performance tapes, supported by SealMatic and AMS case-sealing machines, enabling operational efficiency and eco-conscious packaging practices.

Nitto Denko Corporation: Pioneering High-Temperature and Specialty Adhesive Tapes with Sustainability Focus

Nitto Denko Corporation specializes in advanced adhesive tapes and films for industrial and specialty applications. Its offerings include high-performance packaging tapes, surface protection tapes, and double-sided bonding solutions. The company emphasizes sustainability management and material innovation, developing environmentally responsible products while meeting performance and security requirements for diverse industrial sectors.

Packaging Tapes Market Share Insights, 2025-2034

Acrylic Adhesives Dominate Market Share by Adhesive Type in the Packaging Tapes Industry

Acrylic adhesives hold 45% of the packaging tapes market, driven by their superior performance across diverse shipping environments. Their UV resistance, aging stability, and clarity make them the adhesive of choice for long-term storage and outdoor logistics, particularly in the booming e-commerce and global trade sectors where package integrity is paramount. Acrylic-based tapes are also valued for their compatibility with high-speed automated packaging lines, providing consistent performance while aligning with sustainability initiatives through solvent-free, water-based formulations. Hot-melt adhesives, holding 35% of the market, represent the fastest-growing segment, driven by their rapid setting time that ensures seamless integration with automated fulfillment centers. Their adoption is accelerating in industries where operational efficiency outweighs heat sensitivity concerns. Rubber-based adhesives, while losing share, maintain strategic relevance in cold-chain logistics and industrial applications, where high tack and adhesion to rough or low-energy surfaces are critical. Niche segments such as water-activated gummed tapes and silicone-based adhesives cater to highly specialized needs, offering tamper-evidence and high tensile strength for heavy-duty shipments in aerospace, defense, and automotive industries. The adhesive landscape demonstrates how acrylic continues to dominate mainstream applications, while hot-melt powers automation growth and specialized adhesives sustain niche industrial demands.

E-commerce & Logistics Lead Market Share by End-Use in the Packaging Tapes Industry

The e-commerce and logistics sector accounts for 42% of packaging tape demand, making it both the largest and fastest-growing end-use segment. This dominance is directly tied to the global surge in online retail and fulfillment networks, where tapes serve as both a functional security layer and a brand reinforcement tool through printable surfaces for logos, QR codes, and tamper-evident messaging. The operational need for automation-compatible tapes that deliver high-speed sealing without adhesive failure is fueling strong demand for both acrylic and hot-melt variants. Food and beverages remain a consistent user base, requiring FDA-compliant adhesives for direct and indirect contact packaging, and increasingly demanding recyclable and “clean-label” tape solutions that align with corporate sustainability pledges. Healthcare and pharmaceuticals represent a high-value, specification-intensive segment, where tapes must ensure sterility, tamper evidence, and performance in climate-controlled logistics. The rise of biologics and cold-chain shipping is further amplifying demand for specialized medical-grade adhesive formulations. The automotive industry, while a smaller consumer, requires high-shear strength tapes for heavy-duty parts handling and double-sided variants for assembly-line applications where residue-free removal is critical. Together, these segments reveal that while e-commerce drives volume, healthcare drives value, and automotive drives innovation, collectively shaping the strategic growth trajectory of the global packaging tapes market.

United States Packaging Tapes Market Fueled by Sustainability and E-Commerce Growth

The United States packaging tapes market is undergoing rapid transformation, led by the booming e-commerce sector and evolving sustainability regulations. State-level Extended Producer Responsibility (EPR) laws are reshaping the industry, pushing companies to develop recyclable and post-consumer recycled (PCR) content packaging tapes. At the federal level, government-backed programs are promoting advanced packaging technologies to support sustainable innovation across logistics and manufacturing.

Corporate investments are also redefining the competitive landscape. In August 2025, major players including General Mills, Mars, and PepsiCo launched the US Flexible Film Initiative (USFFI) to scale recycling solutions for flexible plastic packaging, a category that includes packaging tapes. Meanwhile, technological advancements are accelerating the shift toward water-activated kraft tapes and reinforced paper-based solutions, which are both biodegradable and compatible with cardboard recycling streams. With demand rising in online retail, food distribution, and agricultural packaging, the U.S. market is prioritizing eco-friendly, durable, and automation-ready packaging tapes.

Germany Packaging Tapes Market Driven by PPWR and Sustainable Adhesive Innovation

The Germany packaging tapes market is strongly regulated under the European Union’s Packaging and Packaging Waste Regulation (PPWR), effective February 2025, which mandates higher recyclability and minimum recycled content thresholds by 2030 and 2040. Alongside this, the expanded German Packaging Act (VerpackG) continues to set ambitious recycling targets, positioning Germany at the forefront of circular packaging practices.

Technological leadership is another defining factor, with German companies innovating in bio-based adhesives, water-based systems, and UV-curable inks to reduce VOC emissions. A notable development came in March 2025, when tesa SE won a sustainable engineering award for its Debonding on Demand technology, enabling adhesive bonds to be removed without residue to enhance recycling efficiency. The country’s packaging tape applications are strongest in food, beverage, cosmetics, and construction industries, where industrial sacks, cartons, and secure sealing solutions demand high-performance, environmentally responsible adhesives.

China Packaging Tapes Market Expanding with Dual-Carbon Goals and AI Integration

The China packaging tapes market is expanding rapidly under the government’s dual-carbon targets of reaching carbon peak by 2030 and neutrality by 2060. Regulatory momentum is evident through new express delivery sector laws (June 2025) promoting environmentally friendly and reusable materials, as well as nine new recycled plastics standards set to take effect in February 2026. These frameworks are pushing packaging tape producers to adopt recyclability-first designs and reduce environmentally harmful adhesives.

At the technological level, automation and AI adoption are transforming the industry. Manufacturers are deploying AI-enabled quality assurance systems and adhesive optimization platforms to boost efficiency and compliance. The 2023 China Adhesives & Tape Industry Annual Conference highlighted national strategies for low-VOC tapes and high-quality development, reinforcing alignment with sustainability policies. With 175 billion parcel deliveries in 2024, China’s dominance in e-commerce, electronics, and consumer goods is fueling record demand for eco-friendly, secure, and digitally traceable packaging tapes.

India Packaging Tapes Market Rising with Make in India and BOPP Tape Adoption

The India packaging tapes market is thriving under supportive policy initiatives like Make in India and the Production Linked Incentive (PLI) scheme, which are encouraging domestic manufacturing and investment in packaging technologies. The industry has seen accelerated expansion in adhesives and tapes manufacturing, with companies upgrading facilities and introducing advanced R&D lines to meet demand from packaging, logistics, and industrial users.

Technological adoption is also shaping growth, with robotics, AI, and automation in packaging lines reducing labor costs and boosting output efficiency. A key driver in India is the food and beverage sector, alongside a booming e-commerce industry, which relies heavily on BOPP (Biaxially Oriented Polypropylene) tapes due to their durability, cost-effectiveness, and branding opportunities. As online retail scales further, India’s packaging tapes market is positioned as a high-growth hub with sustainability-driven innovation and expanding export potential.

Japan Packaging Tapes Market Aligned with Positive List System and Circular Packaging Goals

The Japan packaging tapes market is adapting to the positive list system for food contact materials, effective June 1, 2025, which restricts allowable substances in packaging tapes and adhesives. This regulatory move is pushing companies to reformulate adhesives and coatings, ensuring compliance with food safety standards. Meanwhile, QR code-enabled e-labeling is becoming a norm, increasing demand for digitally printable tape surfaces.

Japanese firms are global leaders in sustainable packaging tape innovation, with companies like Stora Enso collaborating with local manufacturers to develop paper-based barrier materials suited for fragile and temperature-sensitive items. These solutions require advanced adhesive tapes designed for thermal and safety performance. Sustainability targets remain a driving force, as Japan aims to cut greenhouse gas emissions by 46% by 2030 and achieve net-zero by 2050. The country’s strong consumption of ready-to-drink beverages, snacks, and premium packaged goods creates sustained demand for aesthetic, lightweight, and recyclable packaging tapes.

Brazil Packaging Tapes Market Strengthened by PNRS and Food Safety Regulations

The Brazil packaging tapes market is guided by the National Solid Waste Policy (PNRS), which enforces principles of reuse, recycling, and responsible disposal across packaging sectors. In August 2025, Anvisa’s RDC No. 983/2025 was introduced to amend food contact packaging regulations, establishing a phase-out of certain materials and encouraging the adoption of safe and compliant adhesive tapes.

Innovation is emerging through sustainable tape formulations designed to meet both domestic regulations and international food safety standards. Brazil’s strong food and beverage sector, including its canned goods industry, remains the largest consumer of packaging tapes. Additionally, corporate investments in new technologies and regulatory updates by Conasq (National Commission for Chemical Safety) are reinforcing the shift toward eco-friendly adhesives and recyclable tapes, positioning Brazil as a key growth market in Latin America.

Packaging Tapes Market Report Scope

Packaging Tapes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$122.2 Billion

|

|

Market Size (2034)

|

$175.4 Billion

|

|

Market Growth Rate

|

4.1%

|

|

Segments

|

By Material Type (Paper, Plastic, Other Materials), By Adhesive Type (Acrylic, Rubber-based, Hot-Melt, Other Adhesive Types), By Product Form (Carton-Sealing, Masking & Painter's, Strapping & Bundling, Other Product Forms), By End-Use Industry (Food & Beverage, E-commerce & Logistics, Healthcare & Pharmaceutical, Automotive)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, Tesa SE (Beiersdorf AG), Shurtape Technologies, LLC, Nitto Denko Corporation, Intertape Polymer Group Inc., Avery Dennison Corporation, The Duck Brand (ShurTech Brands, LLC), Sika AG, PPI Adhesive Products, Ltd., Scapa Group plc, Lohmann GmbH & Co. KG, Adhesives Specialties, Godson Tapes Private Limited, W. L. Gore & Associates, Inc., Tesa Tapes (India) Private Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Packaging Tapes Market Segmentation

By Material Type

- Paper

- Plastic

- Other Materials

By Adhesive Type

- Acrylic

- Rubber-based

- Hot-Melt

- Other Adhesive Types

By Product Form

- Carton-Sealing

- Masking & Painter's

- Strapping & Bundling

- Other Product Forms

By End-Use Industry

- Food & Beverage

- E-commerce & Logistics

- Healthcare & Pharmaceutical

- Automotive

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Packaging Tapes Market

- 3M Company

- Tesa SE (Beiersdorf AG)

- Shurtape Technologies, LLC

- Nitto Denko Corporation

- Intertape Polymer Group Inc.

- Avery Dennison Corporation

- The Duck Brand (ShurTech Brands, LLC)

- Sika AG

- PPI Adhesive Products, Ltd.

- Scapa Group plc

- Lohmann GmbH & Co. KG

- Adhesives Specialties

- Godson Tapes Private Limited

- W. L. Gore & Associates, Inc.

- Tesa Tapes (India) Private Limited

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous and comprehensive research methodology to deliver accurate and actionable insights into the global Packaging Tapes Market. Our approach integrates extensive primary research, including interviews and consultations with key stakeholders such as tape manufacturers, adhesive technology providers, logistics and e-commerce operators, and regulatory authorities, alongside secondary research drawn from corporate reports, trade journals, government publications, and industry databases. Advanced analytical techniques and forecasting models are applied to assess market trends, growth drivers, and future opportunities across segments including material type, adhesive type, product form, and end-use industries. Regional analysis encompasses major markets such as the United States, Europe, China, India, Japan, and Brazil, with careful evaluation of sustainability initiatives, automation adoption, regulatory frameworks, and digital printing trends. USDAnalytics combines qualitative insights with quantitative data to provide a precise market outlook, emphasizing technological innovation, eco-friendly solutions, operational efficiency, and emerging opportunities in bio-based adhesives, smart tapes, and specialty high-performance products for logistics, industrial, and e-commerce sectors.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.