Printed Tape Market Size, Overview, and Growth Outlook (2025–2034)

Printed Tape Market to Reach $61.5 Billion by 2034 as E-commerce and Branding Fuel Growth

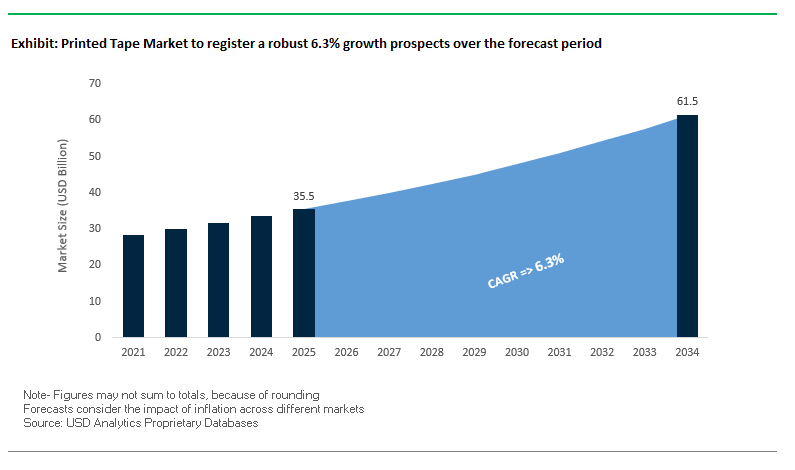

The global printed tape market is projected to grow from $35.5 billion in 2025 to $61.5 billion by 2034, reflecting a CAGR of 6.3%. Growth is primarily driven by the expansion of e-commerce, where companies increasingly use custom-printed tapes to elevate the unboxing experience, strengthen brand recognition, and communicate key messages directly to customers. Additionally, the market is witnessing a rising demand for security and tamper-evident solutions, where printed tapes with unique codes, sequential numbering, or “VOID” messages help protect products across the supply chain.

Key Insights for industry professionals and buyers:

- E-commerce Growth is Driving Volume: Online retail is fueling demand for branded packaging solutions that double as marketing tools.

- Security-Focused Tapes Gain Traction: Tamper-evident and sequentially numbered tapes enhance product integrity.

- Flexography Dominates Printing Technology: Cost-effective, high-speed printing for large-volume orders ensures brand consistency.

- Sustainability is Becoming Essential: Paper-based and bio-based adhesives, as well as solvent-free and PCR content materials, meet growing eco-conscious consumer demands.

- Innovations Enhance Product Appeal: UV-resistant, high-clarity, and durable tapes offer improved branding and functional performance.

- Integration with Packaging Equipment Boosts Efficiency: Applicators and dispensers designed for printed tapes reduce waste and speed up operations.

Market Analysis: Strategic Product Launches and Sustainability Innovations Are Shaping the Printed Tape Industry

The printed tape market has seen significant advancements in product innovation and sustainability. In August 2025, Shurtape Technologies showcased its secure and sustainable end-of-line packaging tapes at PACK EXPO Las Vegas, highlighting its commitment to eco-friendly solutions. The same month, Afera published a survey indicating that the European adhesive tape industry is preparing for potential global trade measures, emphasizing supply chain diversification and raw material sourcing strategies.

Innovations are driving both functionality and aesthetics. In July 2025, Shurtape launched AP 251, a UV-resistant acrylic printed tape offering clarity and legible messaging, while a Nano Letters study introduced a novel ALD ultrathin film method, potentially improving nanocoatings for high-performance printed tapes. Sustainability-focused research is also influencing market dynamics. In April 2025, Nfinite Nanotechnology and Amcor collaborated on nanocoatings to enhance recyclable and compostable packaging, demonstrating technology applications relevant for printed tapes with superior oxygen barrier performance.

Strategic acquisitions and expansion also define industry growth. In March 2025, Avery Dennison acquired Meridian Adhesives Group’s U.S. flooring adhesives business for $390 million, strengthening its specialty adhesives portfolio. Previously, in April 2024, Shurtape launched a curbside-recyclable paper packaging tape, showcasing the growing emphasis on sustainable solutions. Similarly, innovations in high-performance graphics, such as 3M’s Print Wrap Film IJ280 (November 2024), demonstrate the integration of speed, durability, and print quality, which indirectly supports broader trends in premium printed tape applications.

Emerging Trends and Opportunities Transforming the Printed Tape Market

Strategic Integration of Branded Tapes for Last-Mile Delivery Marketing

Printed tape is evolving from a simple packaging closure into a powerful branding and marketing tool, particularly in the booming e-commerce and direct-to-consumer (DTC) sectors. A 2024 case study from the collectibles retailer 7 Bucks a Pop demonstrated how custom-printed tape featuring its logo and website address turned every shipped parcel into a brand touchpoint. This approach ensures that the brand identity is reinforced the moment a customer receives their order, creating an immediate connection and recall value. For small and mid-sized businesses, printed tape provides a cost-effective branding alternative to fully customized corrugated boxes. According to Phoenix Tape & Supply, printed tape allows brands to maintain flexibility with smaller production runs while still achieving a professional, high-end look at a fraction of the cost of bespoke packaging. This trend underscores the strategic role of printed tape in last-mile delivery marketing and consumer engagement.

Adoption of Tamper-Evident and Security-Printed Tapes for Supply Chain Integrity

Security-driven innovation is another major trend shaping the printed tape market. Tamper-evident and security-printed tapes are now widely deployed in industries where product integrity is paramount. In the pharmaceutical sector, regulatory standards have long mandated their use to combat counterfeiting and tampering. A case study from Tamper Technologies highlighted that a pharmaceutical manufacturer successfully prevented three counterfeit attempts within six months by adopting tamper-evident tapes, saving millions in potential recall and brand damage costs. Beyond pharmaceuticals, industries handling high-value goods, electronics, and consumer products are also adopting these tapes. As reported by Pharmaceutical Technology, tamper-evident tapes with irreversible “VOID” or “OPENED” indicators act as a visual deterrent, instantly alerting handlers and consumers to package breaches. This trend reflects the growing convergence of printed tape with supply chain risk management and anti-counterfeiting strategies.

Development of High-Performance Water-Activated Tapes (WAT) with Sustainable Backings

The resurgence of water-activated tape (WAT) offers a clear growth opportunity for manufacturers, especially as e-commerce giants like Amazon adopt it for its superior performance. Adherex Packaging reported that one e-commerce shipper reduced its tape-related claim rate from 3% with pressure-sensitive tape to just 0.2% after switching to WAT, underscoring its strength and tamper-evident sealing capability. The sustainability aspect further amplifies its appeal. WAT, often made with paper substrates and starch-based biodegradable adhesives, aligns perfectly with corporate ESG goals and consumer preferences for eco-friendly packaging. According to an EIN Presswire release (August 2025), the global boom in WAT dispensers is directly linked to rising demand for sustainable packaging solutions. This opportunity positions WAT as both a high-performance and environmentally responsible alternative in the printed tape segment.

Integration of Smart Tapes with Embedded Tracking and Data Carriers

The evolution of printed tape into a digital enabler of supply chain visibility is one of the most disruptive opportunities in the market. Smart tapes, embedded with GPS trackers, temperature sensors, or shock indicators, transform packaging from passive containment into an active data carrier. Trackonomy’s SmartTape is a leading example, offering real-time visibility into location, condition, and handling of shipments across global supply chains. This technology addresses critical blind spots in last-mile delivery, enabling parcel-level tracking that helps reduce billions in annual losses from cargo theft, spoilage, or mishandling. For high-value sectors such as pharmaceuticals, electronics, and cold chain logistics, smart printed tapes present a breakthrough solution by combining branding, security, and real-time data collection in one innovation. As adoption scales, smart tapes will redefine printed tape from a consumable packaging accessory to a vital component of intelligent logistics.

Competitive Landscape: Leading Printed Tape Companies Are Driving Growth Through Innovation, Sustainability, and Integration Capabilities

The global printed tape industry is highly competitive, with leading companies focusing on advanced adhesives, digital solutions, and eco-friendly materials to differentiate in packaging, branding, and industrial applications. Companies are emphasizing product customization, high-performance tapes, and integrated applicator solutions to meet evolving customer demands.

3M Company: Leveraging Materials Science Expertise to Deliver High-Performance Printed Tapes

3M offers a comprehensive range of printed packaging tapes, including carton sealing, filament tapes, and specialty industrial tapes. Its Scotch® and VHB™ brands are recognized for durability and performance. 3M integrates tape applicators and dispensers for operational efficiency, enabling customers to reduce waste and enhance productivity. The company’s focus on materials science ensures innovative, high-quality solutions across industrial and e-commerce segments.

Avery Dennison Corporation: Expanding Specialty Adhesives and Driving Digital Transformation in Packaging

Avery Dennison’s Performance Tapes portfolio caters to commercial printing, retail, and e-commerce applications. The August 2025 acquisition of Meridian Adhesives Group strengthened its high-value adhesives segment. Avery Dennison leverages AI, IoT, and cloud-based platforms through atma.io for digital product passports, enhancing supply chain transparency and product traceability. Its deep application expertise enables custom solutions and R&D collaboration with clients for unique printed tape products.

Shurtape Technologies, LLC: Pioneering Sustainable and Secure End-of-Line Packaging Solutions

Shurtape provides a wide range of printed, masking, and specialty tapes for industrial and consumer applications. In July 2025, it launched AP 251, a high-clarity, UV-resistant acrylic printed tape, highlighting innovation in brand visibility. Shurtape’s expansion of its Catawba, North Carolina plant demonstrates its commitment to meeting rising market demand. Its Secure + Sustainable portfolio emphasizes eco-friendly and tamper-evident solutions.

Intertape Polymer Group (IPG): Driving Packaging Efficiency and Security With Innovative Tape Solutions

IPG offers printed carton sealing tapes, filament tapes, and water-activated tapes for branding and security. Its strategy focuses on product bundling, global expansion, and sustainability. IPG also provides automated packaging solutions and lab services, helping customers optimize packaging efficiency, reduce waste, and implement tamper-evident solutions.

Tesa SE: Advancing Sustainability and Precision in Industrial Printed Tape Applications

Tesa specializes in adhesive technology and self-adhesive products for paper, print, and industrial applications. Its tesa® Twinlock system provides a reusable, compressible, and eco-friendly alternative to traditional mounting tapes. Tesa’s portfolio includes plate mounting tapes, self-adhesive sleeves, and complementary products, ensuring high-quality printing performance with reliability and precision.

Printed Tape Market Share Insights, 2025-2034

Acrylic Adhesives Command Market Share by Adhesive Type in the Printed Tape Industry

Acrylic adhesives dominate the printed tape market with 55% share, reflecting their unmatched performance in demanding environments such as e-commerce logistics, cold-chain storage, and long-haul shipping. Their superior resistance to UV exposure, temperature fluctuations, and aging ensures packaging integrity across diverse conditions, making them the adhesive of choice for global supply chains. Hot melt adhesives, with a substantial 35% share, are preferred for high-volume, cost-sensitive applications due to their fast tack and quick bonding, which is critical for rapid packaging lines. Natural rubber adhesives, though declining, retain a small but specialized role in heavy-duty sealing applications, where their immediate grab strength is still valued. This segmentation highlights how functional resilience and cost efficiency drive adhesive type selection, with acrylic leading in performance-critical use cases while hot melt secures high-volume adoption in standardized packaging operations.

E-Commerce & Logistics Drive Market Share by End-Use Industry in the Printed Tape Industry

The e-commerce and logistics sector holds 45% of printed tape demand, positioning it as the primary growth engine of the industry. Beyond basic sealing, printed tape in this segment now serves as a last-mile marketing and security tool, integrating branding, QR codes, and tamper-evident messaging to improve customer engagement and safeguard packages. The food and beverage industry follows, where FDA-compliant adhesives and reliable cold-chain performance are crucial, particularly for refrigerated goods. Manufacturing and industrial applications account for a significant portion of demand, emphasizing durability, resistance to rough handling, and legible barcodes for supply chain efficiency. Consumer goods companies are increasingly adopting high-quality printed tape as a branding extension, reinforcing premium positioning during the unboxing experience. Automotive and construction end-uses remain smaller but strategically important, requiring specialized tapes for precision labeling, part tracking, and sealing heavy-duty materials. Collectively, these end-use insights underscore that the rise of e-commerce has redefined printed tape from a commodity into a critical branding and compliance-driven packaging tool.

United States: E-Commerce Growth and Digital Printing Transforming Demand

The United States printed tape market is being shaped by the expansion of e-commerce and retail packaging, which is driving demand for customized, branded, and tamper-evident solutions. Companies increasingly rely on printed tapes to enhance brand visibility, secure shipments, and engage customers through interactive features. Innovations in digital printing alongside traditional flexographic printing are enabling high-resolution graphics, rapid turnaround for short production runs, and variable data printing such as QR codes and barcodes. These advancements support both brand storytelling and supply chain efficiency.

Regulation also plays an important role. The U.S. Government Publishing Office (GPO) enforces strict quality and procurement standards for printed materials, indirectly shaping tape specifications. Meanwhile, U.S. Customs and Border Protection has guidelines on imported printed products that can influence supply chains. On the technical side, manufacturers are adopting specialized adhesive technologies to ensure printed tapes perform under harsh conditions such as extreme temperatures and humidity, especially in warehousing and logistics. A new wave of innovation includes AI-powered design automation software, which allows companies to create and customize printed tapes quickly, enhancing brand personalization while reducing design lead times.

European Union: Sustainability, Circular Economy, and PPWR Compliance

In the European Union, the printed tape market is undergoing transformation under the Packaging and Packaging Waste Regulation (PPWR), which came into effect in February 2025. This framework enforces recyclability, reusability, and circular economy compliance, pushing manufacturers to redesign their products with eco-friendly materials. A key industry response has been the exploration of sustainable chemistries and defossilization of adhesives, reducing dependency on fossil-based raw materials.

The European Adhesive Tape Association (Afera) plays a pivotal role in promoting industry alignment, with its European Tape Week 2025 spotlighting sustainability, digital transformation, and regulatory compliance. The EU’s requirement for a harmonized recycling label on all packaging by 2028 is also impacting the market, driving demand for clearer, standardized labeling on printed tapes. As a result, companies are investing in eco-friendly substrates and recyclable adhesive systems, positioning the EU as a leader in sustainable printed packaging innovation.

China: Regulatory Shifts and E-Commerce Growth Fueling Printed Tape Usage

China’s printed tape market is being propelled by its Dual Circulation strategy, which prioritizes domestic consumption as a growth engine, strengthening the role of e-commerce packaging. Demand for printed tapes is rising as online retailers seek secure, branded packaging to enhance consumer trust. Regulations introduced in June 2025 target delivery waste reduction, requiring greater adoption of recycled materials and reusable packaging systems, which directly affect printed tape production and material selection.

The National Development and Reform Commission (NDRC) and the Ministry of Ecology and Environment (MEE) continue to enforce measures to combat plastic pollution, pushing for environmentally safer substrates in adhesive tapes. At the same time, the General Administration of Customs of China (GACC) introduced a requirement for “Product Expiration Date” labeling on imported goods, influencing printing practices on packaging tapes. These regulatory shifts, combined with rising domestic demand, are fostering innovation in sustainable and compliant printed tape solutions tailored for China’s booming logistics sector.

India: Make in India Manufacturing and BOPP Tape Dominance

India’s printed tape market is expanding rapidly under the Make in India initiative, which promotes domestic manufacturing and localized production capacity. Demand is particularly strong in the MSME sector, where businesses seek cost-effective, durable solutions for everyday packaging needs. The market is also witnessing a surge in the adoption of BOPP (Biaxially Oriented Polypropylene) tapes, valued for their strength, durability, and cost-effectiveness, making them the most widely used option across industries.

Companies such as Flexibond Tapes are investing in modern infrastructure for high-precision printing and advanced adhesive coating, supporting the transition to customized and branded tape production. On the regulatory side, the Central Pollution Control Board (CPCB) enforces the Plastic Waste Management Rules (2016, amended 2022) with strong emphasis on Extended Producer Responsibility (EPR). This is driving manufacturers toward eco-friendly alternatives, including recyclable and biodegradable tapes, balancing affordability with sustainability.

Germany: High-Performance Tapes and Automotive Applications Driving Growth

Germany is recognized as a leading European market for high-quality printed tapes, driven by demand from industrial sectors that prioritize performance, reliability, and sustainability. The country has a mature printing infrastructure and distribution network, which facilitates widespread adoption of printed tapes across industries. Strong growth is observed in the automotive and fleet graphics sectors, where printed adhesive films are extensively used for vehicle wraps, branding, and protective applications.

German manufacturers are pioneering eco-friendly innovations, focusing on advanced adhesive chemistries and recyclable substrates. For example, INDUPLAST has introduced printed tape products with 70–95% recycled content, addressing both performance and sustainability requirements. The integration of recyclable materials with high mechanical strength makes Germany a hub for premium, sustainable printed tape production catering to both domestic and international markets.

Japan: Premium Graphics and EV Transition Driving Printed Tape Demand

Japan’s printed tape market is influenced by the Japan Vinyl Industry Association (JVIA) and regulatory bodies that enforce strict safety and quality standards for vinyl and adhesive products. The market is diverse, with printed tapes being used in carton sealing, bundling, tamper-evident packaging, and premium product branding. Japanese manufacturers emphasize aesthetic quality and precision graphics, making the country a hub for premium-grade printed tapes that appeal to consumer-facing industries.

A key growth driver is the transition to electric vehicles (EVs), which has expanded demand for innovative, heat-resistant, and durable tapes in battery packs and electronic components. This industrial shift complements the traditional demand for retail and logistics packaging, creating a multi-sectoral market opportunity. With its emphasis on high-performance materials, graphic quality, and industrial safety, Japan is positioning itself as a leader in premium and technology-integrated printed tape solutions.

Printed Tape Market Report Scope

Printed Tape Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$35.5 Billion

|

|

Market Size (2034)

|

$61.5 Billion

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Material (BOPP, PVC, Kraft Paper, WAT, Filament Tapes), By Adhesive Type (Acrylic, Hot Melt, Natural Rubber), By Printing Technology (Flexography, Digital Printing, Screen Printing), By Application (Packaging & Carton Sealing, Branding & Promotion, Tamper-Evident Security, Warnings & Instructions, Masking & Specialty), By End-Use Industry (Food & Beverages, E-commerce & Logistics, Manufacturing & Industrial, Consumer Goods, Automotive, Construction)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, Intertape Polymer Group Inc., Tesa SE, Nitto Denko Corporation, Shurtape Technologies, LLC, Berry Global, Inc., Mondi Group, Avery Dennison Corporation, Shiva Polymers, Logo Tape GmbH & Co. KG, Induplast Josef Löken GmbH & Co. KG, Flexibond Tapes, Uflex Ltd., Nan Ya Plastics Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Printed Tape Market Segmentation

By Material

- BOPP

- PVC

- Kraft Paper

- WAT

- Filament Tapes

By Adhesive Type

- Acrylic

- Hot Melt

- Natural Rubber

By Printing Technology

- Flexography

- Digital Printing

- Screen Printing

By Application

- Packaging & Carton Sealing

- Branding & Promotion

- Tamper-Evident Security

- Warnings & Instructions

- Masking & Specialty

By End-Use Industry

- Food & Beverages

- E-commerce & Logistics

- Manufacturing & Industrial

- Consumer Goods

- Automotive

- Construction

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Printed Tape Market

- 3M Company

- Intertape Polymer Group Inc.

- Tesa SE

- Nitto Denko Corporation

- Shurtape Technologies, LLC

- Berry Global, Inc.

- Mondi Group

- Avery Dennison Corporation

- Shiva Polymers

- Logo Tape GmbH & Co. KG

- Induplast Josef Löken GmbH & Co. KG

- Flexibond Tapes

- Uflex Ltd.

- Nan Ya Plastics Corporation

* List Not Exhaustive

Methodology

The research methodology for the Printed Tape Market integrates a combination of primary and secondary research approaches to deliver actionable insights for industry professionals. Primary research involved detailed interviews with key stakeholders, including tape manufacturers, packaging engineers, supply chain managers, sustainability experts, and R&D personnel across North America, Europe, Asia-Pacific, and emerging markets. Secondary research encompassed an exhaustive review of company reports, investor presentations, patents, trade publications, regulatory frameworks, and verified market studies, focusing on trends in e-commerce packaging, tamper-evident solutions, branded tape adoption, adhesive technologies, and printing innovations. USDAnalytics employed advanced data triangulation techniques to validate market sizing, CAGR projections, and segmentation insights, combining macroeconomic factors, raw material pricing trends, technological adoption, and regulatory influences. Both top-down and bottom-up forecasting approaches were utilized to ensure accuracy, while regional analyses were contextualized with domestic manufacturing initiatives, sustainability mandates, and industry-specific demand patterns. This methodology ensures that the report provides precise, reliable, and professional-grade intelligence for decision-makers in the printed tape industry.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.