Market Overview: High-Growth Trajectory Driven by Regulatory Enforcement and Technological Innovation

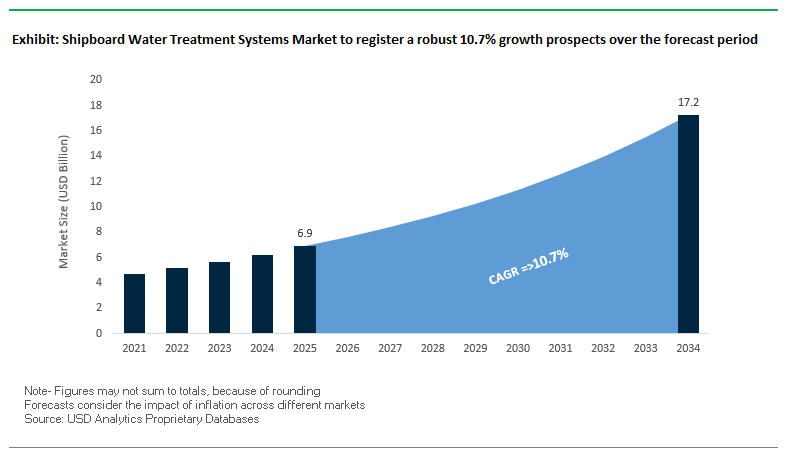

The shipboard water treatment systems market is set to expand from USD 6.9 billion in 2025 to USD 17.2 billion by 2034, registering a robust CAGR of 10.7%. The growth is fueled by a convergence of factors including stricter environmental regulations, rapid technological advancements, and rising onboard water demand for both commercial and defense vessels.

Central to the momentum is the International Maritime Organization’s (IMO) Ballast Water Management (BWM) Convention, particularly the D-2 standard, which mandates active treatment of ballast water to prevent the spread of invasive aquatic species. Between September and November 2025, Port State Control authorities under the Paris and Tokyo MOUs will execute a Concentrated Inspection Campaign (CIC) on ballast water systems, signaling intensified enforcement and compliance scrutiny.

The market is also benefiting from innovations in ballast water treatment systems (BWTS), including hybrid solutions that combine UV disinfection and electrochlorination for higher efficiency across varying water conditions. Reverse osmosis (RO) desalination systems are increasingly standard in cruise ships, naval fleets, and cargo vessels, addressing the growing need for onboard freshwater production. Meanwhile, new regulatory frameworks are driving integrated wastewater and graywater treatment solutions, such as membrane bioreactor (MBR) and ultrafiltration (UF) systems, enabling safe discharge or reuse of treated water.

Strategic Imperatives for Stakeholders

- Invest in hybrid and automated BWTS to meet evolving IMO standards.

- Expand R&D in compact, energy-efficient desalination and wastewater systems.

- Develop modular, retrofit-friendly solutions for aging fleets.

- Integrate digital monitoring platforms for operational optimization.

- Leverage regulatory shifts, such as electronic Ballast Water Record Books, to differentiate offerings.

Market Analysis: Technological Shifts and Regulatory Milestones Accelerating Adoption

The market in 2025 is being reshaped by landmark contracts, regulatory amendments, and innovation pipelines. In September 2025, Veolia secured a multi-million-dollar agreement with Petrobras to supply advanced seawater desalination systems for two FPSOs in Brazil, underscoring the offshore sector’s demand for compact, high-reliability solutions. The same month, Port State Control initiated a CIC on ballast water compliance, aligning with IMO’s D-2 enforcement push.

In October 2025, IMO amendments introducing electronic Ballast Water Record Books (eBWRBs) came into effect, streamlining compliance management and standardizing operational documentation across global fleets. The digital shift reflects a broader industry trend towards automation and remote monitoring, evident in Veolia’s AI-powered Hubgrade platform and Xylem’s Rivo™ I system for real-time water treatment control.

Technological innovation is also transforming pretreatment and desalination capabilities. DuPont Water Solutions launched its Multibore™ PRO UF membranes in March 2025, tailored for high-performance seawater RO pretreatment in space-constrained marine environments. SUEZ began construction in April 2025 of the Philippines’ largest SWRO desalination facility, deploying pre-treatment technologies that can be adapted for large cruise and naval vessels. Outside direct maritime applications, Kurita Water Industries partnered with ispace in August 2025 to develop ultra-compact, low-energy water purification systems for lunar missions and technologies with potential adaptation for extreme marine conditions.

Sustainability is also becoming a decisive competitive factor. Veolia’s inauguration of a solar-powered desalination plant in November 2023 highlights growing integration of renewables with water treatment infrastructure, a trend gaining traction for environmentally compliant marine operations.

Trends and Opportunities in Shipboard Water Treatment Systems Market

Trend 1: Stricter IMO Regulations Drive Adoption of Advanced Ballast Water Treatment

The implementation of the International Maritime Organization’s (IMO) Ballast Water Management (BWM) Convention has created a regulatory mandate for all ships to adopt advanced ballast water treatment systems (BWTS). The regulation, ratified by 86 countries representing over 91% of global merchant shipping tonnage, requires ships to meet the D-2 performance standard, effectively preventing the spread of invasive aquatic species. Compliance has driven a surge in retrofitting existing vessels with type-approved BWTS and equipping all new ships with these systems. Common technologies include UV-based physical disinfection and chemical treatments such as electrochlorination. Despite the high investment of up to $5 million per retrofit, the regulatory imperative ensures widespread adoption, positioning BWTS as a critical component of sustainable maritime operations and global environmental compliance.

Trend 2: Electrochlorination Gains Traction for Marine Desalination

Electrochlorination is increasingly being adopted aboard ships as a safe, reliable, and cost-effective method for water treatment and biofouling control. By electrolyzing seawater to produce sodium hypochlorite on-site, the technology eliminates the need to store hazardous chemicals, reducing safety risks and logistical challenges. Beyond biofouling prevention in cooling systems, electrochlorination can disinfect potable water and treat wastewater before discharge, providing a versatile solution for marine operations. While initial capital costs can be substantial, the lower operational costs of on-site chlorine generation compared to bulk chemical handling result in significant long-term savings. The technology is particularly appealing to vessel operators seeking efficient, multi-purpose water treatment solutions that comply with environmental and safety regulations.

Opportunity 1: UV-LED Disinfection for Low-Power Shipboard Water Treatment

UV-LED technology is emerging as a compact, energy-efficient alternative to traditional mercury-based lamps and chemical disinfection for shipboard water treatment. With minimal power consumption, instant-on functionality, and a small footprint, UV-LED systems are ideal for vessels with space and energy limitations. They enable rapid disinfection without warm-up delays, providing instantaneous treatment as water flows through the system. The chemical-free nature of UV-LEDs ensures no byproducts, taste, or odor changes in potable water, enhancing crew safety and passenger health. Its compact design allows easy integration into both new ship builds and retrofitting projects, presenting a key opportunity for operators prioritizing low-energy, environmentally friendly solutions.

Opportunity 2: Smart Monitoring Systems for Real-Time Water Quality on Cruise Ships

Cruise lines are increasingly investing in smart water quality monitoring systems to ensure passenger safety and regulatory compliance. IoT-enabled sensors and data analytics platforms allow continuous, real-time monitoring of key parameters such as pH, turbidity, chlorine residuals, and temperature. Automated alerts enable immediate corrective action, reducing the risk of waterborne illnesses aboard ships. Additionally, these systems streamline compliance reporting with international health authorities like the CDC while enhancing operational efficiency by optimizing chemical usage and system performance. For large passenger vessels, smart monitoring provides a proactive approach to water safety, operational cost management, and overall service quality.

Shipboard Water Treatment Systems Market Share Insights

Commercial Shipping Dominates with 65% Market Share

Commercial vessels represent the core market for shipboard water treatment systems, accounting for approximately 64.7% of global demand in 2025. Container ships, bulk carriers, tankers, and cargo vessels require reliable freshwater and process water systems, emphasizing low operational costs and high durability. In comparison, naval and defense vessels demand specialized systems built to strict redundancy, shock-resistance, and contaminant-tolerant specifications, ensuring strategic water independence under operational and emergency conditions. Specialized vessels, such as cruise ships and offshore support vessels, increasingly drive demand for high-capacity, advanced treatment systems to meet hotel-quality water standards and environmental compliance in sensitive maritime zones.

Freshwater Generation Captures 61% as the Essential Utility

Freshwater generation systems remain the largest segment, with an estimated 61.2% market share, reflecting their critical role in sustaining crew and operational needs across all vessel types. Seawater distillation using engine waste heat is the traditional workhorse, particularly on large commercial ships where energy is abundant and free. Reverse Osmosis (RO) systems are gaining traction, especially for naval ships, LNG carriers, and smaller vessels where waste heat is limited, offering compact, flexible, and energy-efficient desalination solutions. Wastewater treatment systems are increasingly vital, driven by MARPOL Annex IV compliance, with growing adoption of greywater and blackwater treatment systems to meet stricter environmental mandates.

.png)

Medium-Sized Fleets Drive 40% of System Capacity Demand

Systems for medium-sized fleets, accounting for 40.4% of market share, form the backbone of global shipping water treatment, balancing capacity, space, and energy efficiency. Large ship systems are optimized for high-volume output, supporting VLCCs and container ships with extensive freshwater and process water needs. Megaships, primarily cruise liners, require industrial-scale treatment plants capable of supplying thousands of passengers with potable water and treating complex wastewater streams. Small vessels emphasize compact, efficient RO-based systems, ideal for tugs, fishing boats, and yachts where engine waste heat is not available.

Engine Waste Heat Powers 54.7% of Water Treatment Systems

Main engine waste heat remains the dominant energy source, powering approximately 54.7% of freshwater generation systems globally. The approach leverages otherwise wasted thermal energy, offering maximum energy efficiency and cost savings, particularly on large commercial vessels. Auxiliary generator-powered systems primarily drive RO desalination and wastewater treatment, providing reliability when the main engine is off or during port operations. Hybrid electric systems and emergency manual operation are niche but strategically important, enabling dynamic energy optimization and uninterrupted freshwater availability, especially for critical naval and passenger vessels.

Country Analysis of the Shipboard Water Treatment Systems Market

United States: Driving Demand for USCG-Approved Ballast Water Systems

The United States maintains one of the most stringent regulatory environments for maritime water treatment, with the U.S. Coast Guard (USCG) enforcing ballast water management regulations that often surpass international standards. The has spurred significant demand for USCG-approved ballast water treatment systems (BWTS), particularly for retrofit installations on older vessels to avoid costly penalties. Innovative solutions such as portable and containerized BWTS, including the InTankFITT Container and UniBallast B.V., provide flexibility for temporary or shared use. The U.S. market favors UV-based, non-chemical treatment systems, meeting both USCG and IMO discharge standards. Additionally, governmental funding exceeding $300 million for water recycling and desalination projects indirectly supports advancements in shipboard water treatment technologies, reinforcing the broader adoption of efficient marine water solutions.

China: Policy-Driven Growth in Coastal and Port Water Treatment

China’s “War on Pollution” and “Water Ten Plan” have a direct impact on the shipboard water treatment sector, particularly in coastal waters and major ports. Policies such as the “Bay Chief System” aim to regulate near-shore resource development and reduce seawater pollutants, driving adoption of advanced shipboard water treatment systems. The 20th Party Congress’s strategic plan for a “strong marine country” underscores the long-term government commitment to marine ecological protection. Between 2017 and 2022, over RMB 673 billion was allocated to water pollution control, incentivizing domestic shipyards and maritime companies to develop innovative ballast water and shipboard treatment solutions that meet both national and international regulations.

South Korea: Rising Global Competitiveness in BWTS

South Korea is positioning itself as a global leader in USCG-type-approved ballast water treatment systems, with support from the Ministry of Oceans and Fisheries (MOF) for R&D in new maritime water technologies. The Korean Register of Shipping (KR) provides accreditation for USCG-type approvals, giving domestic companies a competitive edge. Firms like Techcross Inc. have successfully obtained approval, while major shipbuilders including Samsung Heavy Industries and Panasia Co. Ltd. are actively pursuing certification. South Korea leverages its historical expertise in thermal desalination technologies to innovate in the shipboard water treatment market, combining energy-efficient solutions with advanced compliance capabilities.

Japan: Innovating Microplastics Collection and Sustainable Water Treatment

Japanese companies are at the forefront of marine pollution control, particularly for microplastics management. Collaborative developments, such as the cyclone separator installed on a car carrier by Mitsui O.S.K. Lines, Ltd. and Miura Co., Ltd., can process 70 times more seawater than previous generations to collect microplastics. Japan also excels in seawater desalination and wastewater reuse; Hitachi’s system mixes seawater with reclaimed wastewater, reducing pumping costs and energy consumption by over 30%. Advanced aquaculture water treatment, such as Kawasaki’s MINATOMAÉ System, prevents pathogen entry and extracts microplastics. Innovations like the KUBOTA Submerged Membrane Unit further highlight Japan’s emphasis on efficient, sustainable shipboard water treatment for regulatory compliance and environmental protection.

Europe (Germany): Regulatory Compliance and Intelligent Onboard Water Management

Europe, particularly Germany, is a critical market for eco-friendly shipboard water treatment systems due to regulatory frameworks such as the Ballast Water Management (BWM) Convention and the EU Emissions Trading System (ETS). These policies drive demand for energy-efficient, high-compliance solutions for both new vessels and retrofits. Companies like RWO Water Technologies provide intelligent onboard water management systems, including oily water separators, wastewater treatment, and ballast water treatment systems. RWO’s products adhere to standards like IMO MEPC.107(49), emphasizing regulatory compliance, operational safety, and sustainable performance. High-quality components and comprehensive after-sales support are key competitive differentiators in the European market.

Competitive Landscape: Global Leaders Driving Marine Water Treatment Innovation

The shipboard water treatment systems market is highly competitive, with global players leveraging cross-sector expertise, strong R&D pipelines, and digital integration capabilities to secure market share.

Veolia Environnement S.A.: Delivering Ecological Transformation for Marine Operations

Veolia offers a full lifecycle approach to marine water management, integrating RO desalination, MBR wastewater treatment, and bilge water processing into modular, retrofit-ready systems. The company’s contract with Petrobras in September 2025 reinforced its dominance in offshore energy water solutions. Veolia’s Hubgrade digital platform enables real-time monitoring and predictive maintenance, enhancing compliance and reducing operating costs for ship operators.

SUEZ S.A.: Circular and Compliant Water Solutions for All Vessel Classes

SUEZ’s marine strategy focuses on compact, energy-efficient systems meeting IMO and MARPOL requirements. Its portfolio spans BWTS, membrane wastewater treatment, and freshwater generators. The company’s land-based expertise (such as April 2025 Philippines SWRO project) translates into high-performance maritime applications, particularly for cruise liners and bulk carriers.

Kurita Water Industries Ltd.: Chemical Expertise Meets Extreme Environment Engineering

Kurita specializes in advanced chemical and physical treatment systems for cooling, boiler, and wastewater applications in ships. Its August 2025 lunar water purification project with ispace showcases its ability to engineer ultra-compact, low-energy systems, adaptable for marine vessels operating in harsh conditions. Kurita’s AOX-free and phosphate-free treatment options position it as a sustainability leader.

Xylem Inc.: Smart, Interconnected Marine Water Management

Xylem focuses on integrating hardware like pumps and mixers with digital analytics platforms for intelligent shipboard water management. Its Rivo™ I system offers modular, real-time control and optimized chemical dosing to meet IMO D-2 compliance. Xylem’s strength lies in creating interconnected, data-driven marine systems for improved efficiency and sustainability.

Shipboard Water Treatment Systems Market Report Scope

Shipboard Water Treatment Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.9 Billion

|

|

Market Size (2034)

|

$17.2 Billion

|

|

Market Growth Rate

|

10.7%

|

|

Segments

|

By Vessel Type (Commercial Shipping, Naval & Defense, Specialized Vessels), By System Type (Freshwater Generation, Wastewater Treatment, Water Quality Management), By Capacity Range (Small Vessels, Medium Fleet, Large Ships, Megaships), By Energy Source (Main Engine Waste Heat, Auxiliary Generator Power, Hybrid Electric Systems, Emergency Manual Operation)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Alfa Laval, Wärtsilä, Veolia Water Technologies, Xylem Inc., Panasia, Techcross, Desmi, Ecochlor, Trojan Marinex, Mitsubishi Heavy Industries, Hyde Marine, Qingdao Sunrui, JFE Engineering

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Shipboard Water Treatment Systems Market Segmentation

By Vessel Type

- Commercial Shipping

- Container Ships

- Bulk Carriers

- Tankers

- Cruise Ships

- Naval & Defense

- Aircraft Carriers

- Destroyers/Frigates

- Submarines

- Specialized Vessels

- Offshore Support

- Research Vessels

- Fishing Fleets

By System Type

- Freshwater Generation

- Wastewater Treatment

- Water Quality Management

By Capacity Range

- Small Vessels (<10 m³/day)

- Medium Fleet (10-100 m³/day)

- Large Ships (100-1,000 m³/day)

- Megaships (>1,000 m³/day)

By Energy Source

- Main Engine Waste Heat

- Auxiliary Generator Power

- Hybrid Electric Systems

- Emergency Manual Operation

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Shipboard Water Treatment Systems Market

- Alfa Laval

- Wärtsilä

- Veolia Water Technologies

- Xylem Inc.

- Panasia

- Techcross

- Desmi

- Ecochlor

- Trojan Marinex

- Mitsubishi Heavy Industries

- Hyde Marine

- Qingdao Sunrui

- JFE Engineering

* List Not Exhaustive

Research Coverage

This report investigates the Global Shipboard Water Treatment Systems Market, delivering authoritative analysis reviews on technological breakthroughs, regulatory milestones, and strategic imperatives shaping the industry’s growth from 2025 to 2034. Published by USDAnalytics, the study highlights the accelerating influence of IMO’s Ballast Water Management (BWM) Convention, the transition to electronic Ballast Water Record Books, and landmark contracts such as Veolia’s Petrobras FPSO agreement. It further emphasizes breakthroughs in hybrid ballast water treatment solutions, compact reverse osmosis desalination, and integrated wastewater treatment systems that are redefining shipboard efficiency and compliance. By profiling leading companies, assessing innovation pipelines, and analyzing regional regulatory strategies, this report is an essential resource for shipowners, shipbuilders, maritime regulators, EPC contractors, and technology providers navigating one of the fastest-evolving segments of marine water infrastructure.

Scope Includes:

- Segmentation: By Technology (Ballast Water Treatment Systems, RO Desalination, Wastewater & Graywater Treatment, UV, Electrochlorination, MBR, UF), By Vessel Type (Commercial, Naval, Offshore, Specialized), By Capacity (Small, Medium, Large, Megaship), By Energy Source (Engine Waste Heat, Auxiliary Generators, Hybrid Systems), By End Use (Freshwater Generation, Wastewater, Ballast).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Historic Data: 2021 to 2024, and Forecast Data: 2025 to 2034.

- Companies: Profiles and analysis of 15+ key players including Veolia, SUEZ, Kurita, Xylem, Techcross, and RWO Water Technologies.

Methodology

The research methodology applied by USDAnalytics combines primary and secondary research to ensure precision, credibility, and strategic relevance. Primary insights were gathered from ship operators, maritime regulators, technology providers, and shipyards through structured interviews, validating market adoption trends, regulatory impacts, and technology preferences. Secondary data was sourced from company filings, maritime project databases, IMO and USCG regulations, and peer-reviewed publications. Market size was derived through top-down and bottom-up triangulation, aligning vessel fleet data with adoption rates of ballast water treatment, desalination, and wastewater systems. Forecasts were modeled under scenarios reflecting regulatory tightening, digital monitoring penetration, retrofit adoption, and energy-efficient technology scaling, resulting in robust projections for stakeholders across the global shipping ecosystem.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Shipboard Water Treatment Systems Market

1. Executive Summary

1.1. Market Highlights and Growth Drivers

1.2. Strategic Imperatives for Key Stakeholders

1.3. Global Market Snapshot

2. Shipboard Water Treatment Systems Market Overview & Outlook (2025–2034)

2.1. Introduction to the Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $6.9 Billion

2.2.2. Forecasted Market Size (2034): $17.2 Billion at 10.7% CAGR

2.3. Key Drivers and Market Dynamics

2.3.1. Regulatory Enforcement of IMO's BWM Convention (D-2 Standard)

2.3.2. Technological Advancements in BWTS, RO, and MBR Systems

2.3.3. Rising Onboard Water Demand for Commercial and Naval Vessels

3. Market Analysis: Technological Shifts and Regulatory Milestones

3.1. Overview of Key Strategic Developments in 2025

3.1.1. Veolia's Contract with Petrobras for FPSO Desalination

3.1.2. Port State Control's Concentrated Inspection Campaign (CIC)

3.1.3. IMO's Amendments for Electronic Ballast Water Record Books (eBWRBs)

3.2. Innovation Pipelines and Partnerships

3.2.1. DuPont's Multibore™ PRO UF Membranes

3.2.2. Kurita Water Industries' Partnership for Lunar Water Purification

3.3. Sustainability and Digitalization in Marine Water Treatment

4. Trends and Opportunities in Shipboard Water Treatment Systems

4.1. Trend 1: Stricter IMO Regulations Drive Adoption of Advanced BWTS

4.1.1. Compliance with the D-2 Performance Standard

4.1.2. Surge in Retrofit Installations and New Vessel Equipping

4.2. Trend 2: Electrochlorination Gains Traction for Marine Desalination and Biofouling Control

4.2.1. On-Site Production of Sodium Hypochlorite

4.2.2. Safety, Cost-Effectiveness, and Versatility

4.3. Opportunity 1: UV-LED Disinfection for Low-Power Water Treatment

4.3.1. Energy-Efficient, Compact, and Chemical-Free Solutions

4.3.2. Ideal for Space and Energy-Constrained Vessels

4.4. Opportunity 2: Smart Monitoring Systems for Real-Time Water Quality

4.4.1. Ensuring Passenger Safety and Regulatory Compliance on Cruise Ships

4.4.2. Optimizing Operations and Chemical Usage

5. Competitive Landscape: Global Leaders Driving Marine Water Treatment Innovation

5.1. Veolia Environnement S.A.: Delivering Ecological Transformation for Marine Operations

5.2. SUEZ S.A.: Circular and Compliant Water Solutions for All Vessel Classes

5.3. Kurita Water Industries Ltd.: Chemical Expertise Meets Extreme Environment Engineering

5.4. Xylem Inc.: Smart, Interconnected Marine Water Management Platforms

5.5. Other Key Players: Alfa Laval, Wärtsilä, Panasia, and more.

6. Market Share and Segmentation Insights: Shipboard Water Treatment Systems

6.1. By Vessel Type

6.1.1. Commercial Shipping Dominates with 65% Market Share

6.1.2. Naval & Defense and Specialized Vessels Segments

6.2. By System Type

6.2.1. Freshwater Generation Captures 60% as the Essential Utility

6.2.2. Wastewater Treatment Systems and Water Quality Management

6.3. By Capacity Range

6.3.1. Medium-Sized Fleets Drive 40% of System Demand

6.3.2. Large Ships, Megaships, and Small Vessels

6.4. By Energy Source

6.4.1. Main Engine Waste Heat Powers 55% of Systems

6.4.2. Auxiliary Generator Power and Hybrid Electric Systems

7. Country Analysis of the Shipboard Water Treatment Systems Market

7.1. United States: Driving Demand for USCG-Approved BWTS

7.2. China: Policy-Driven Growth in Coastal and Port Water Treatment

7.3. South Korea: Rising Global Competitiveness in BWTS

7.4. Japan: Innovation in Microplastics Collection and Sustainable Water Treatment

7.5. Europe (Germany): Regulatory Compliance and Intelligent Onboard Water Management

7.6. Other Country Analysis

8. Market Size Outlook by Region (2025–2034)

8.1. North America Market Size Outlook to 2034

8.1.1. By System Type

8.1.2. By Vessel Type

8.1.3. By Capacity

8.2. Europe Market Size Outlook to 2034

8.2.1. By System Type

8.2.2. By Vessel Type

8.2.3. By Capacity

8.3. Asia Pacific Market Size Outlook to 2034

8.3.1. By System Type

8.3.2. By Vessel Type

8.3.3. By Capacity

8.4. South America Market Size Outlook to 2034

8.4.1. By System Type

8.4.2. By Vessel Type

8.4.3. By Capacity

8.5. Middle East and Africa Market Size Outlook to 2034

8.5.1. By System Type

8.5.2. By Vessel Type

8.5.3. By Capacity

9. Research Coverage & Methodology

9.1. Report Scope and Focus

9.2. Research Methodology

9.3. Deliverables

10. Appendix

10.1. List of Tables

10.2. List of Figures

10.3. Abbreviations