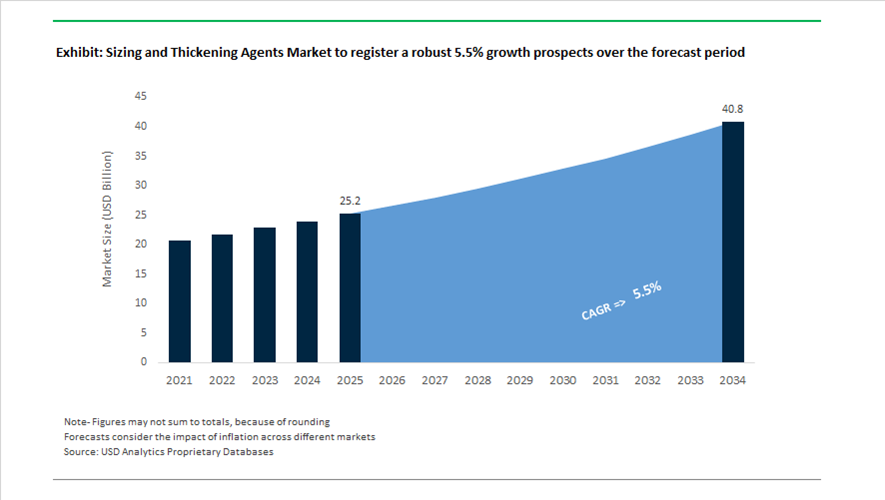

Sizing and Thickening Agents Market Valuation 2025–2034: $25.2 Billion to $40.8 Billion at 5.5% CAGR Anchored in Clean-Label Texturizers and Industrial Rheology Control

The global sizing and thickening agents market is valued at $25.2 billion in 2025 and is projected to reach $40.8 billion by 2034, registering a CAGR of 5.5%. Expansion is supported by strong demand for food hydrocolloids, starch derivatives, pectin, carrageenan, xanthan gum, cellulose ethers, synthetic polymer thickeners, and specialty dispersions used across food and beverages, clinical nutrition, pharmaceuticals, paper processing, textiles, coatings, adhesives, and construction materials. These agents enhance viscosity, suspension stability, mouthfeel, surface strength, and water retention while meeting tightening regulatory standards on clean-label formulations, biodegradability, and wastewater discharge. Fermentation-based biothickeners, plant-derived texturizers, and low-COD industrial sizing chemistries are emerging as strategic growth platforms across both consumer and industrial end markets.

In January 2024, DuPont Nutrition & Biosciences launched Danisco® PureSolve HM, a renewable thickener platform formulated to deliver enhanced texture and stability in beverages and liquid foods without synthetic additives. In March 2024, Ashland Global Holdings and Ingredion entered a strategic collaboration combining specialty chemical rheology expertise with plant-based texturizer technologies to co-develop advanced sizing and thickening systems for food and industrial uses. In May 2024, BASF completed the acquisition of Solvay’s European dispersions and thickeners business, strengthening its foothold in coatings, construction additives, and industrial rheology modifiers. In August 2024, Roquette introduced four new CLEARAM tapioca-based starches designed to improve viscosity control in dairy desserts and sauces while maintaining non-GMO positioning. In November 2024, Tate & Lyle finalized its $1.8 billion acquisition of CP Kelco, integrating global pectin, carrageenan, and specialty gum production into its Mouthfeel solutions portfolio.

Innovation and regulatory milestones accelerated through 2025. In February 2025, the European Commission approved a new class of microbial-derived thickeners for food applications, enabling scale-up of fermentation-based alternatives to seaweed and plant gums. In March 2025, Cargill introduced a starch-based pectin replacer at the AAHAR exhibition in India, targeting cost-sensitive gummy and jelly manufacturers with comparable gelling performance at lower formulation costs. Nestlé Health Science expanded the global rollout of its xanthan gum-based ThickenUp Clear technology through 2024–2025, addressing the growing dysphagia clinical nutrition market. On November 1, 2025, DuPont completed the spinoff of its Electronics business, repositioning its remaining nutrition and biosciences-related thickening technologies within healthcare and diversified industrial segments.

Operational optimization and manufacturing realignment intensified in 2026. In February 2026, Ingredion reported progress under its Cost2Compete restructuring initiative, prioritizing high-efficiency production plants for Texture & Healthful Solutions across Latin America and North America. These efforts focus on optimizing supply chains for starch-based thickeners and clean-label hydrocolloids. The convergence of renewable ingredient innovation, fermentation-enabled microbial thickeners, industrial dispersion technology integration, and geographic manufacturing rationalization is shaping the competitive architecture of the sizing and thickening agents market toward $40.8 billion by 2034.

Key Trends and High-Impact Opportunities in the Global Sizing and Thickening Agents Market

Bio-Based Clean Label Viscosity Systems Transforming Home and Fabric Care

The sizing and thickening agents market is undergoing a decisive shift as global consumer packaged goods companies replace fossil-derived rheology modifiers with bio-based, clean label alternatives. This transition is no longer driven solely by brand positioning but by hard sustainability metrics tied to supply chain decarbonization, microplastic elimination, and ingredient traceability. Conventional carbomers and synthetic acrylates are increasingly viewed as misaligned with emerging regulatory and consumer expectations, accelerating adoption of natural and bio-fermented viscosity modifiers.

Innovation momentum is particularly strong in biotechnology-enabled ingredients. In early 2025, Dow received a Silver Award at in-cosmetics Asia for its DEXCARE CD-2 Polymer, a bio-fermented dextran designed to function as a high-efficiency conditioning and deposition agent. This development reflects a broader industry pivot toward fermentation-derived polymers that offer consistent quality, lower environmental footprint, and superior stability compared with traditional plant extracts. At the corporate level, sustainability commitments are translating directly into formulation mandates. In March 2025, Unilever announced a major expansion of its Climate Transition Action Plan, targeting Net Zero across its value chain by 2039 and a 42% reduction in Scope 3 emissions by 2030. Central to this strategy is the accelerated use of renewable and recycled feedstocks in home and fabric care, structurally lifting demand for bio-based sizing and thickening agents across emerging markets such as India.

Precision Rheology Requirements for Advanced Technical Ceramics in EVs and Electronics

A second structural trend is emerging from advanced manufacturing, where precise rheology control is becoming mission critical for technical ceramics used in electric vehicles, power electronics, and semiconductor fabrication. The production of high-purity alumina and aluminum nitride components relies on specialized organic binders and thickeners to regulate slurry flow, particle dispersion, and green body integrity during tape casting and injection molding.

As of December 2025, the global semiconductor ceramics market is projected to exceed $2.71 billion, driven by the construction of new fabrication facilities worldwide and the push toward device miniaturization below five nanometers. This expansion directly increases demand for high-performance thickening systems capable of operating under ultra-clean conditions. The trend is reinforced by the growth of wide-bandgap semiconductors. In June 2024, Kyocera showcased advanced ceramic substrates for silicon carbide and gallium nitride power devices at PCIM Europe. These modules operate under extreme thermal loads, requiring thickeners that maintain slurry uniformity and prevent sedimentation during the manufacture of ceramic-filled laminates used in EV onboard chargers, 5G base stations, and power conversion systems.

Salt-Tolerant Thickeners for Ultra-Concentrated Laundry Formats

The rapid shift toward ultra-concentrated laundry pods and unit-dose detergents has exposed a significant technical gap in traditional rheology modifiers. Many conventional thickeners lose viscosity or phase stability in high-electrolyte and high-surfactant environments, creating a premium opportunity for salt-tolerant associative thickeners engineered for concentrated systems.

This opportunity is reinforced by both regulatory and performance dynamics. As powdered detergents decline in urban markets, formulators are increasingly pairing bio-based surfactants such as rhamnolipids and alkyl polyglucosides with advanced associative thickeners to achieve eco-label certification in North America and Europe. Stability under reuse conditions is also becoming critical in industrial settings. In May 2024, Tetra Pak launched its Factory Sustainable Solutions platform, enabling recovery of up to 90% of Clean-in-Place liquids via nanofiltration. This shift is driving demand for detergents and thickening agents that retain performance after repeated recovery cycles in high-pressure cleaning systems, positioning salt-tolerant rheology modifiers as a yield and efficiency enabler.

Functional Sizing for Advanced Non-Woven Filtration and Hygiene Applications

The evolution of non-woven materials from basic mechanical filters to engineered nanofiber media is creating a high-growth opportunity for functional sizing agents. These next-generation sizings are designed to impart properties such as hydrophilicity, antimicrobial activity, and mechanical reinforcement directly during fiber formation, eliminating the need for post-treatment.

Indoor air quality regulations are a key catalyst. The introduction of ASHRAE 241 in 2024 is compelling commercial buildings to upgrade from MERV 8 to MERV 13 and higher filtration standards, requiring non-woven media capable of capturing sub-three-micron particles without excessive pressure drop. Achieving this balance depends on sizing agents that strengthen electro-spun nanofibers in the 20 to 200 nanometer range while preserving airflow. Parallel momentum is coming from healthcare and hygiene. Initiatives led by the U.S. Department of Health and Human Services to localize non-woven manufacturing are accelerating adoption of biodegradable sizing agents in medical disposables. With non-wovens accounting for roughly 60% of polypropylene consumption in these applications, demand is rising for sizing systems that enable HEPA-grade filtration efficiency of 99.999% while aligning with sustainability and medical safety requirements.

Sizing and Thickening Agents Market Share and Segmentation Insights

Synthetic Agents Lead the Sizing and Thickening Agents Market Through Advanced Polymer Performance

Synthetic agents accounted for 42.80% of the sizing and thickening agents market in 2025, establishing them as the dominant product category across industrial processing applications. Materials such as acrylic polymers, polyacrylates, polyurethanes, and styrene-acrylic copolymers provide highly controlled rheological properties, formulation stability, and consistent performance, making them widely used in textile sizing, industrial thickening systems, and paper coating formulations. These agents enable precise viscosity control and surface modification in manufacturing processes where predictable material behavior is essential. A major 2025 development is the emergence of high-performance multifunctional synthetic thickeners designed to deliver shear-thinning application behavior, rapid viscosity recovery after shear, and combined thickening with surface modification, improving production efficiency and finished product performance.

Food & Beverage Industry Drives Global Demand for Thickening Agents

Food and beverage represent the largest end-use segment in the sizing and thickening agents market, accounting for 32.80% of total demand in 2025 due to the extensive use of thickening agents in processed food formulations. Hydrocolloids, starches, and cellulose derivatives are widely used to control texture, viscosity, mouthfeel, and stability in products such as sauces, dressings, dairy products, beverages, and ready-to-eat foods. While sizing agents play a limited role in food production, thickening functionality remains critical for product formulation and consumer sensory experience. A major 2025 market trend is the growing demand for clean label food ingredients, where manufacturers increasingly adopt native starches, plant-derived hydrocolloids, and cellulose-based thickeners to replace synthetic additives while maintaining the required product texture and shelf stability.

Sizing and Thickening Agents Market Competitive Landscape

The global sizing and thickening agents market in 2026 is defined by clean-label hydrocolloid adoption, modified starch innovation, and multifunctional rheology systems. Industry leaders are investing in bio-based texturizers, localized GMP production, and dual-function agents that enhance texture, stability, and sustainability across food, pharmaceutical, and industrial applications.

Ingredion Incorporated Scales Clean-Label Starch Thickeners and Simplistica™ Systems for Functional Food Applications

Ingredion Incorporated leads the clean-label thickening agents segment with strong financial momentum, reporting $11.13 adjusted EPS and $944 million operating cash flow in 2025. Its Indianapolis facility expansion strengthens specialty starch capacity, supporting rising demand for modified starch thickeners in convenience foods and industrial sizing. The Simplistica™ platform integrates tapioca starch and guar gum into single-unit systems, optimizing texture, stability, and formulation efficiency in dairy-free and plant-based products. Ingredion’s advanced film-forming technologies improve oil reduction and enhance barrier strength in food-contact paper applications. Its focus on plant-based hydrocolloids and high-amylose starch aligns with global regulatory pressure on synthetic additives. The company’s vertically integrated innovation strategy reinforces leadership in clean-label rheology modifiers.

Tate & Lyle PLC Transforms into Hydrocolloid Powerhouse Through CP Kelco Integration and Xanthan Innovation

Tate & Lyle PLC has significantly strengthened its position in the hydrocolloid and thickening agents market following the $1.8 billion acquisition of CP Kelco, creating a unified leader in pectin, xanthan gum, and starch systems. Its ThickenUp Clear product, an amylase-resistant xanthan gum thickener, is gaining traction in clinical nutrition and dysphagia management. The integration expands fermentation-derived hydrocolloid capabilities, enabling carbon-neutral alternatives to petroleum-based thickeners aligned with Scope 3 reduction goals. The company’s Global Solution Centers provide advanced rheology testing and customized sizing formulations for food and pharmaceutical clients. This strategic consolidation enhances its ability to deliver high-performance stabilizing and gelling systems. Tate & Lyle’s focus on sustainable hydrocolloids and functional texture solutions positions it strongly in high-growth segments.

Cargill Inc. Strengthens Localized Production and Sustainable Supply Chains for Functional Texturizers

Cargill Inc. is reinforcing its leadership in supply chain resilience and clean-label ingredient systems through localized manufacturing and sustainability-driven logistics. Its Beijing plant expansion, including new functional systems production lines, supports Asia-Pacific demand for thickening agents and coated food applications. The IngredienTracker™ 2025 insights are shaping its product portfolio toward minimally processed, transparent texturizers aligned with consumer preferences. Cargill’s new India facility integrates specialized thickening agents into animal nutrition, expanding its footprint in agricultural value chains. The adoption of green methanol-powered shipping reduces the carbon footprint of hydrocolloid and starch exports. Its “local-for-local” strategy enhances operational agility while meeting ESG and regulatory requirements. The company’s scale and logistics innovation strengthen its competitive positioning in global texturizer markets.

Kerry Group PLC Enhances Texture and Salt-Reduction Technologies Through Functional Fiber Innovation

Kerry Group PLC is leveraging its Taste & Nutrition platform to drive growth in specialty thickening agents and functional texturizers, reporting €6.76 billion in 2025 revenue with a 17.9% EBITDA margin. Its Tastesense™ technology utilizes functional fibers to replicate the mouthfeel of sodium-rich formulations, enabling effective salt reduction without compromising sensory quality. Strong growth in the APMEA region, particularly in bakery and ready-meal categories, highlights demand for advanced texture-modifying systems. Kerry’s enzyme-based solutions enhance viscosity, stability, and processing efficiency across food applications. Strategic capital allocation includes €300 million in Capex to modernize production infrastructure for high-value ingredients. Its focus on nutrition-driven innovation aligns with global health mandates and clean-label trends. Kerry’s integrated approach positions it as a leader in multifunctional thickening systems.

Ashland Inc. Focuses on High-Margin Cellulose Thickeners and Biofunctional Rheology Modifiers

Ashland Inc. is executing a strategic shift toward high-margin specialty additives, optimizing its portfolio around cellulose-based thickeners such as carboxymethylcellulose (CMC) and methylcellulose (MC). The company’s portfolio restructuring reduced overall sales but enhanced profitability and operational focus on Life Sciences and Personal Care markets. Its biofunctional thickening agents are driving double-digit growth, particularly in microbial protection and personal care formulations. Ashland continues to innovate in low-VOC rheology modifiers for coatings, aligning with environmental regulations and future construction market recovery. Its expertise in viscosity control and stabilization supports diverse industrial applications. The company’s disciplined capital allocation and innovation pipeline position it for above-market growth in specialty additives. Ashland’s focus on sustainable rheology solutions strengthens its competitive edge.

BASF SE Expands Polymeric Sizing and Thickening Capacity Through Zhanjiang Verbund and Cost Optimization

BASF SE is advancing its position in the sizing and thickening agents market through large-scale production expansion and cost discipline under its “Winning Ways” strategy. The Zhanjiang Verbund site in China enables localized manufacturing of polymeric sizing agents and industrial thickeners for key end-use industries. With €59.7 billion in 2025 sales and projected 2026 EBITDA of €6.2–€7.0 billion, BASF is leveraging financial strength to invest in sustainable chemical innovation. Its cost-saving program achieved €1.7 billion in annual reductions, with a €2.3 billion target for 2026 supporting green transformation initiatives. The company is balancing emissions from new capacity by transitioning European operations to renewable electricity. BASF’s integrated production model and focus on sustainable binders enhance its competitiveness in high-performance rheology solutions.

United States Sizing and Thickening Agents Market Driven by Clean-Label Formulation and Biopolymer Substitution

The United States market is being reoriented toward clean-label performance, digital formulation tools, and bio-based substitution across food, pharmaceutical, and industrial applications. In July 2025, Ingredion introduced its Texture Equation℠ framework at IFT FIRST, a proprietary digital platform that enables formulators to deploy starch-based thickening agents that replicate the mouthfeel of fats and sugars in reduced-calorie products. This capability is accelerating adoption of native and functional starches in beverages, dairy alternatives, and prepared foods, particularly where rapid viscosity development and label transparency are required. Parallel to food applications, the U.S. Department of Agriculture expanded late-2024 funding for cellulose-based aerogel thickeners, signaling federal backing for replacing petroleum-derived rheology modifiers in industrial coatings and construction materials.

Infrastructure and portfolio consolidation are reinforcing domestic depth. Roquette inaugurated a Customer Technical Services Application Lab in Geneva, Illinois, in September 2025 to support sizing solutions for agriculture and pharmaceuticals, while its May 2025 acquisition of IFF Pharma Solutions integrated a substantial portfolio of cellulosic thickeners, including METHOCEL™ and Lattice®, into the U.S. drug delivery ecosystem. Regulatory anticipation is also shaping formulation strategy, as U.S. manufacturers accelerate the phase-out of select ethoxylated surfactants ahead of the EPA’s 2026 updates, pivoting toward bio-fermented rhamnolipids. Demand-side momentum is evident in convenience foods, with cold-water-swelling starches increasingly specified to deliver instant viscosity in high-pressure processed beverages.

Brazil Sizing and Thickening Agents Market Anchored by Citrus Fiber Upcycling and Regenerative Sourcing

Brazil has consolidated its position as a global hub for upcycled, nature-based thickening agents, leveraging scale citrus processing and circular manufacturing. In May 2024, CP Kelco completed a USD 60 million expansion at its Matão facility, lifting capacity of its NUTRAVA® and KELCOSENS™ citrus fiber lines to approximately 5,000 metric tons. This expansion directly addresses global demand for label-friendly alternatives to modified starches and synthetic stabilizers, particularly in emulsified sauces, dressings, and plant-based foods.

Brazil’s advantage extends beyond capacity to system-level sustainability. The country now supplies over 30% of the world’s high-purity citrus fiber, underpinned by integrated upcycling infrastructure that converts citrus peel byproducts into high-functionality rheology modifiers for food and personal care. Collaborative programs between CP Kelco and regional growers emphasize regenerative fiber sourcing, aligning thickening agents with Scope 3 emissions targets of multinational CPG companies. Brazil is also piloting ethanol-derived solvents for more sustainable extraction of pectin and related hydrocolloids, leveraging its bio-ethanol ecosystem to lower environmental intensity across thickener production.

China Sizing and Thickening Agents Market Shaped by Polymer Innovation and Mandatory Compliance

China’s market is advancing through high-performance polymerization, regulatory enforcement, and strategic self-sufficiency in electronics and packaging. In November 2025, BASF commissioned a next-generation dispersant and sizing agent line at the Jiangbei New Material Technology Park in Nanjing, employing Controlled Free Radical Polymerization to produce advanced rheology modifiers with precise molecular control. Regulatory pressure is accelerating reformulation, as GB 4806.16-2025 mandates the elimination of non-compliant volatile compounds from food-contact paper coatings by September 2026.

China is also prioritizing ultra-high-purity sizing agents for semiconductor manufacturing, targeting a 70% self-sufficiency rate in core electronic materials by 2026. In packaging, the expansion of the Kemira–Tiancheng joint venture in late 2024 has cemented China’s role as the primary global exporter of Alkyl Ketene Dimer for liquid packaging board. Policy support under the “New Normal” framework includes a CNY 40 billion fund to transition textile sizing from synthetic PVA to biodegradable starch-based alternatives, accelerating adoption across mills nationwide.

Germany and the European Union Sizing and Thickening Agents Market Defined by Climate-Neutrality and Rheology Specialization

The Germany-led EU market is characterized by stringent food safety updates, climate-neutral product design, and high-shear rheology expertise. Regulation (EU) 2025/351, issued in February 2025, tightened purity requirements for substances used in food-contact materials, directly impacting specifications for sizing adhesives and varnishes. In response, BASF launched biomass-balanced sizing agents in late 2024, using renewable feedstocks at the start of the value chain to reduce product carbon footprints toward near-zero levels.

Technical differentiation is deepening in coatings and mobility. Evonik advanced its Smart Effects strategy in 2025 by integrating silica and silanes to create hybrid thickening systems that deliver high-shear stability for eco-certified automotive coatings. Regulatory-driven reformulation is also visible in beverages, following the October 2025 update to authorized uses of Quillaia extract as a thickening agent, which forced compositional adjustments across the EU. In footwear, BASF’s December 2025 partnership with San Fang and Nichetech is developing sustainable TPU films and sizing agents aligned with long-term net-zero objectives.

India Sizing and Thickening Agents Market Accelerated by Textile Modernization and Quality Standardization

India’s market is expanding through loom modernization, regulatory tightening, and a pivot toward renewable hydrocolloids. The Ministry of Textiles reported rapid uptake of low-viscosity synthetic sizing agents compatible with 5G-enabled high-speed looms, improving weaving efficiency by an estimated 12% across hubs such as Tiruppur. Cost pressures are shaping formulation economics, as BASF South Asia announced late-2025 price increases for MDI and TDI precursors, prompting downstream substitution and optimization.

Quality assurance is moving up the agenda. The Bureau of Indian Standards has proposed new quality control orders for Carboxymethyl Cellulose used in food and pharma, mandating a minimum purity of 99.5% for domestic production. Sustainability-driven substitution is accelerating in paper and pulp, where guar-based thickeners sourced from Rajasthan are increasingly favored over synthetic polyacrylates, aligning performance with renewable sourcing and domestic agricultural value chains.

Comparative Snapshot: Country-Level Sizing and Thickening Agents Dynamics

Sizing and Thickening Agents Market County Level Snapshot

|

Country / Region

|

Core Demand Drivers

|

Strategic Focus Areas

|

Regulatory and Policy Influence

|

|

United States

|

Clean-label foods, pharma excipients, coatings

|

Digital formulation, cellulose biopolymers

|

EPA chemical safety updates

|

|

Brazil

|

Sauces, plant-based foods, personal care

|

Citrus fiber upcycling, regenerative sourcing

|

Sustainability-led procurement

|

|

China

|

Packaging, semiconductors, textiles

|

CFRP polymers, AKD exports, starch transition

|

GB 4806.16-2025, green subsidies

|

|

Germany / EU

|

Food-contact materials, coatings, footwear

|

Biomass-balanced sizing, hybrid rheology

|

EU 2025/351, additive reclassification

|

|

India

|

Textiles, paper and pulp

|

Loom modernization, guar-based thickeners

|

BIS purity mandates, pricing dynamics

|

Sizing and Thickening Agents Market Report Scope

Sizing and Thickening Agents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$25.2 Billion

|

|

Market Size (2034)

|

$40.8 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Product Type (Natural Agents, Synthetic Agents, Cellulose Derivatives, Bio-Based Hydrocolloids), By Form (Liquid, Powder, Aqueous Solutions), By Application (Sizing Agents, Thickening Agents), By End-Use Industry (Textile & Apparel, Food & Beverage, Pulp & Paper, Pharmaceutical & Personal Care, Industrial & Construction)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Ingredion Incorporated, Dow Inc., Archer Daniels Midland Company, Roquette Frères, Solenis, CP Kelco, Kemira Oyj, Ashland Inc., Cargill Incorporated, Archroma, Shin-Etsu Chemical Co. Ltd., Evonik Industries AG, Zhejiang Xinan Chemical Industrial Group, Tate & Lyle PLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Sizing and Thickening Agents Market Segmentation

By Product Type

- Natural Agents

- Modified Starch

- Guar Gum

- Xanthan Gum

- Pectin

- Gelatin

- Casein

- Synthetic Agents

- Polyvinyl Alcohol

- Polyacrylic Acid

- Styrene Maleic Anhydride

- Polyacrylates

- Cellulose Derivatives

- Carboxymethyl Cellulose

- Methylcellulose

- Hydroxypropyl Methylcellulose

- Bio-Based Hydrocolloids

- Alginates

- Carrageenan

- Agar

By Form

- Liquid

- Powder

- Aqueous Solutions

By Application

- Sizing Agents

- Thickening Agents

By End-Use Industry

- Textile & Apparel

- Food & Beverage

- Pulp & Paper

- Pharmaceutical & Personal Care

- Industrial & Construction

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Sizing and Thickening Agents Industry

- BASF SE

- Ingredion Incorporated

- Dow Inc.

- Archer Daniels Midland Company

- Roquette Frères

- Solenis

- CP Kelco

- Kemira Oyj

- Ashland Inc.

- Cargill Incorporated

- Archroma

- Shin-Etsu Chemical Co. Ltd.

- Evonik Industries AG

- Zhejiang Xinan Chemical Industrial Group

- Tate & Lyle PLC

*- List not Exhaustive