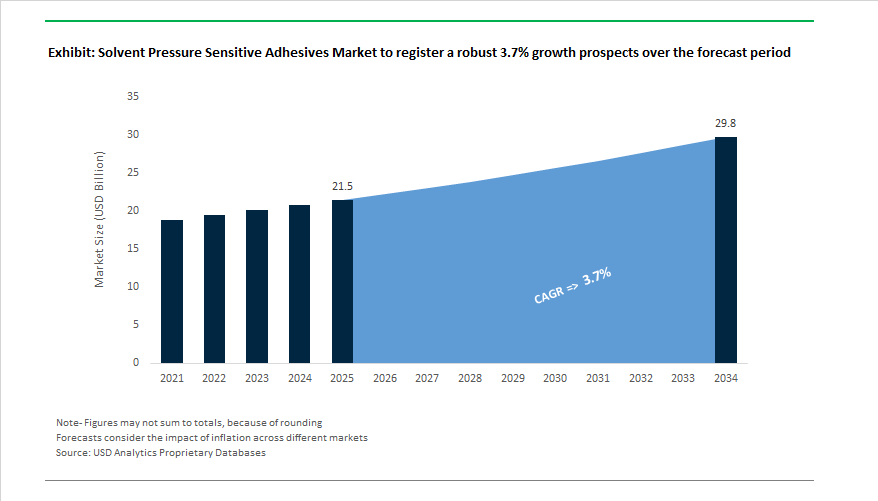

The Global Solvent Pressure Sensitive Adhesives Market is projected to expand from $21.5 billion in 2025 to $29.8 billion by 2034, growing at a CAGR of 3.7%. The market remains an essential segment of the adhesives industry, driven by automotive, electronics, medical, and industrial labeling applications where superior adhesion, clarity, and durability are paramount. Despite regulatory pressures on solvent emissions, solvent-based PSAs remain irreplaceable for high-performance, long-life bonding applications due to their excellent cohesive strength, aging resistance, and optical transparency.

The adoption of acrylic-based solvent PSAs underscores a continued preference for materials combining UV resistance, temperature tolerance, and substrate versatility. These systems are indispensable for automotive exterior trims, industrial labeling, and durable signage, offering longer service life than emulsion-based counterparts. Likewise, silicone solvent PSAs continue to dominate extreme-environment applications, such as aerospace and electronic insulation, withstanding operational temperatures from −65°C to +200°C, maintaining tack and adhesion where other polymers degrade.

In medical applications, solvent-based acrylic and silicone PSAs have gained regulatory favor for skin-safe, biocompatible adhesion, particularly in wound dressings, surgical tapes, and long-term wearable sensors. Manufacturers are tuning formulations to achieve low peel adhesion (<1 N/25 mm) and controlled removal without skin trauma—critical for patient comfort in remote monitoring devices.

Regulatory frameworks—especially the EU Industrial Emissions Directive (IED) and REACH VOC thresholds—continue to shape the market landscape, forcing adhesive producers to invest in closed-loop solvent recovery, high-solids formulations, and process optimization to meet sustainability targets without compromising product performance. High-solids solvent systems, exceeding 60% solids content, are enabling the transition to low-emission manufacturing while retaining the signature performance of solvent PSAs.

The Global Solvent Pressure Sensitive Adhesives (PSA) Market is undergoing a significant transformation as leading producers invest in sustainability, polymer innovation, and regional manufacturing diversification to meet the growing demand for high-performance, low-VOC PSAs across sectors.

In April 2025, Avery Dennison Performance Tapes introduced a Solar Panel Bonding Portfolio, an innovative line of solvent-based PSA tapes designed for UV stability, high peel strength, and durability in outdoor environments. The launch underscores a critical industry trend: leveraging solvent PSA formulations for renewable energy applications, where long-term weather resistance and automation compatibility are essential for solar module assembly.

In March 2025, a major U.S. chemical producer commissioned a new production line in Asia-Pacific for high-solids acrylic polymers, directly supporting solvent PSA manufacturers seeking low-VOC, high-performance resins for tapes and labels. This move reflects the growing localization of supply chains in Asia and the global shift toward environmentally responsible polymer synthesis.

By January 2025, a specialty monomer supplier completed the acquisition of a European distributor, strengthening the supply chain for acrylic building blocks crucial for next-generation medical-grade solvent PSAs used in wearable devices. This strategic integration ensures secure access to critical raw materials for producers serving regulated healthcare sectors.

Meanwhile, DIC Corporation introduced two advanced solvent-based PSA grades—Exp. STF-14S and STF-15H—in October 2024, engineered for high adhesion and flexibility on low-surface-energy substrates such as polyolefins, expanding their applicability across automotive and industrial labeling. Around the same period, an Asian electronics tape manufacturer made significant sustainability investments (August 2024) in solvent recovery systems, achieving VOC reduction levels surpassing European OEM requirements, showcasing the regional pivot toward environmental compliance leadership.

A major breakthrough in June 2024 came through a collaboration between a global tape company and an automotive OEM, focusing on solvent-based adhesive systems for EV structural bonding. These new PSAs provide enhanced thermal management and resistance to electrolyte exposure, directly addressing challenges in electric vehicle battery pack assembly.

Earlier in February 2024, European producers launched toluene-free solvent-based PSAs tailored for the graphic arts and sign-making industry, ensuring high clarity, UV resistance, and faster curing without regulatory risk. This movement toward solvent reformulation continues to reshape the competitive landscape, positioning bio-based solvents and high-solids blends as emerging differentiators.

Finally, technological efficiency is improving production economics. In November 2023, a coating equipment manufacturer unveiled a closed high-speed solvent coating line, reducing evaporation losses by 15% and improving material yield—key to maintaining profitability in a tightening emissions-regulated market.

Market Trend 1: Accelerated Substitution in Consumer-Facing Applications Due to VOC and Odor Regulations

The global solvent PSA market is experiencing a rapid contraction in consumer-oriented sectors—notably flexible packaging, hygiene products, and disposable medical supplies—due to rising VOC emission restrictions and growing awareness of indoor air quality (IAQ) impacts. Leading brand owners are mandating solvent-free adhesives as part of broader sustainability strategies that align with carbon-neutral goals and regulatory compliance mandates.

A major case study from Brilliant Polymers (India) exemplifies the transition: the company reported 72% solvent-free sales in 2025, up from 70% the previous year, citing a 40–60% carbon impact reduction and zero VOC emissions achieved through water-based and solvent-free adhesive systems. The demonstrates the measurable performance and environmental advantages driving rapid adoption in flexible packaging PSAs.

Meanwhile, data from the U.S. Environmental Protection Agency (EPA) drives the health and compliance impetus behind the shift, noting that indoor VOC levels can be up to 10 times higher than outdoor levels due to emissions from consumer adhesives, sealants, and coatings. Regulations such as California’s SCAQMD Rule 1168 and the EU’s Directive 2004/42/EC are enforcing strict VOC caps on consumer goods, accelerating the phase-out of traditional solvent-based PSAs in packaging and household applications.

Despite strong momentum toward water-based and hot-melt PSA technologies, technical barriers persist. Academic research highlights that water-based acrylic emulsions, though eco-friendly, continue to face challenges in water resistance and drying time due to their hydrophilic emulsifier systems. The gap underlines that while substitution in general-purpose PSAs is growing, solvent-based systems still dominate high-demand environments requiring immediate tack, low surface energy adhesion, and long-term durability.

Market Trend 2: Strategic Retention in High-Performance and Extreme Environment Applications

Even as regulatory measures constrain their broader use, solvent-based PSAs continue to lead in high-value applications requiring superior performance under extreme mechanical, chemical, or environmental stress. These include aerospace tapes, automotive under-hood bonding, industrial labels, and medical devices—sectors where adhesion reliability under heat, pressure, and chemical exposure remains critical.

In the automotive and aerospace industries, high-temperature PSAs (HT PSAs) have become indispensable, with performance ratings up to 500°C. These advanced systems are used for wire harness wrapping, insulation, and vibration-resistant bonding where neither hot-melt nor water-based PSAs can maintain adhesion under sustained thermal load. The technical superiority solidifies solvent PSAs as mission-critical materials in safety-sensitive applications.

Solvent-based acrylic PSAs also dominate industrial and outdoor labeling markets due to their exceptional resistance to solvents, moisture, and UV degradation, outperforming emulsion-based alternatives in long-term weathering tests. The makes them ideal for vehicle graphics, outdoor signage, and heavy-duty industrial tapes, where long-term color stability and adhesion integrity are vital.

Additionally, Dow Inc. has advanced solvent PSA technology by introducing Heptane-based Silicone PSAs, which eliminate BTX (Benzene, Toluene, Xylene) solvents while retaining silicone’s hallmark thermal and chemical stability. These next-generation solvent formulations maintain performance for medical and aerospace applications while addressing environmental and occupational safety concerns, signifying a key transitional innovation within the solvent PSA domain.

Market Opportunity 1: Development of Bio-VOC and Low-Global Warming Potential (GWP) Solvent Formulations

The evolution toward sustainable solvent chemistries is the most transformative opportunity in the solvent PSA industry, bridging performance requirements with regulatory and environmental compliance. Research in bio-derived solvent and polymer systems is enabling the creation of high-performance PSAs that meet VOC thresholds while reducing carbon footprint and toxicity.

Recent academic studies have successfully produced bio-based PSAs using biomass-derived monomers like limonene oxide—a renewable compound sourced from citrus waste. The resulting tri-block polymers achieved an impressive 180° peel force of 4 N/cm, matching or exceeding that of conventional petroleum-based PSAs. The breakthrough proves that renewable feedstocks can achieve commercial-grade adhesion while being biodegradable and sustainable.

Similarly, the use of Natural Deep Eutectic Solvents (NaDES) in adhesive systems represents a revolutionary step forward. Inspired by plant exudate mechanisms, these solvents combine bio-sourced components like hyaluronic acid to create bio-VOC compliant PSAs with zero reliance on petrochemicals. The potential of NaDES-based systems lies in their dual advantage—eliminating VOCs entirely while offering tunable adhesion and biodegradability, unlocking new applications in medical devices, food packaging, and consumer goods.

As industries align with the EU Green Deal, REACH directives, and corporate ESG sustainability frameworks, the commercial demand for bio-based, low-GWP solvent formulations is expected to surge, creating a profitable innovation race for adhesive manufacturers focused on compliant high-performance bonding.

Market Opportunity 2: Implementation of Closed-Loop Solvent Recovery Systems with Carbon Capture Integration

For manufacturers who remain reliant on solvent-based PSA production, the integration of closed-loop solvent recovery and carbon capture systems presents an economically viable and environmentally responsible pathway toward compliance and operational efficiency.

Techno-economic analyses of Pressure Swing Adsorption (PSA) and related gas separation technologies show that CO₂ capture costs can be as low as £16.89 per ton, indicating that similar technologies can feasibly recover solvent vapors and process emissions in PSA manufacturing plants. By capturing VOCs and CO₂ simultaneously, these systems transform traditional solvent loss into recoverable material and carbon credit assets.

Engineering models such as Fluor’s CO₂LDSepSM process—which captures 50–90% of CO₂ from tail gas streams—demonstrate the scalability of retrofitting carbon and solvent recovery modules into existing production infrastructure. When applied to solvent PSA manufacturing, the creates a dual benefit: reducing raw solvent purchases and lowering carbon intensity, positioning producers to monetize their carbon savings through verified emission reduction programs.

As environmental legislation increasingly ties carbon pricing mechanisms to industrial emissions, manufacturers deploying integrated solvent recovery and carbon capture will not only meet compliance mandates but also secure measurable cost advantages and improved sustainability credentials under corporate ESG frameworks.

Solvent Pressure Sensitive Adhesives Market Share Insights, 2025-2034

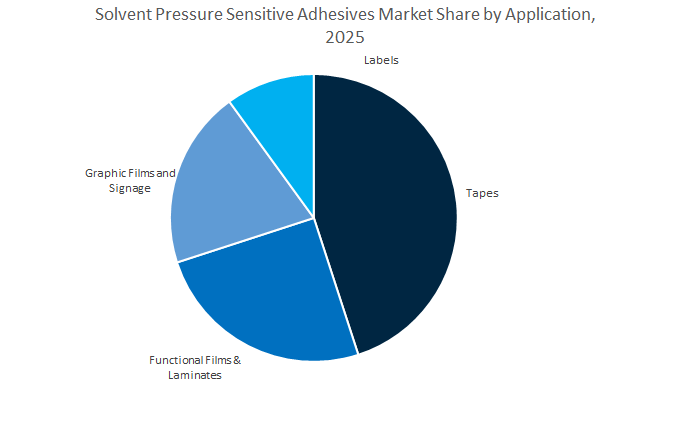

Market Share by Application

Tapes dominate the global solvent pressure sensitive adhesives (PSA) market, accounting for an estimated 43.6% of total demand by 2025, driven by their critical role across industrial, electrical, automotive, and specialty applications. Solvent-based PSA tapes offer superior adhesion, cohesion, and temperature resistance compared to water-based alternatives, making them indispensable for harsh or demanding environments such as high-temperature electrical insulation, heavy-duty packaging, and structural bonding in manufacturing. Their excellent wetting properties and fast adhesion allow bonding to low-energy surfaces like polyethylene and polypropylene, expanding their use in industrial splicing, wire harnessing, and high-performance masking applications. The rising demand from the electronics and automotive sectors, where solvent PSAs provide superior shear and peel performance under mechanical stress, continues to reinforce their dominance.

The Functional Films & Laminates segment represents a major and rapidly expanding market, driven by optical-grade adhesives, protective surface films, and multilayer laminates used in construction, electronics, and industrial processing. Solvent-based PSAs provide the clarity, uniformity, and resistance to moisture and solvents necessary for demanding film applications, including optical displays, automotive glass lamination, and solar modules. Meanwhile, Graphic Films and Signage hold a significant share, supported by global demand for durable, weather-resistant, and high-clarity films used in vehicle wraps, outdoor advertising, and architectural applications. Solvent-based systems’ exceptional UV stability and long-term adhesion make them the preferred choice for outdoor graphics that must withstand environmental exposure. The Labels segment, though smaller, remains strategically important, particularly in industrial, pharmaceutical, and logistics applications where long-lasting adhesion, chemical resistance, and tamper-proof properties are essential.

Market Share by Performance/Function

Permanent PSAs hold the largest share of the global solvent pressure sensitive adhesives market, accounting for approximately 39.4% of total demand by 2025, driven by widespread use in industrial tapes, automotive assembly, construction, and durable labels. Their dominance reflects solvent PSAs’ ability to deliver high initial tack, strong ultimate adhesion, and long-term stability under environmental stress, making them ideal for both permanent and semi-permanent bonding applications. Permanent solvent PSAs exhibit superior resistance to humidity, chemicals, and heat aging, enabling their use in high-performance and outdoor applications such as nameplates, decals, and insulation systems. Their unique formulation flexibility allows manufacturers to tailor adhesive properties for different substrates, ensuring compatibility with a wide range of materials from metals to plastics.

The High-Temperature Resistant and High-Shear PSA segments are growing rapidly, propelled by automotive, aerospace, and electronics manufacturing, where adhesives must perform reliably under prolonged exposure to heat, vibration, and dynamic stress. These high-performance PSAs are engineered to maintain bond integrity up to 200°C or higher, supporting critical uses in engine compartments, circuit assembly, and industrial insulation. Low-Surface Energy (LSE) Substrate PSAs are gaining notable traction as industries adopt advanced plastics and composites in lightweighting and sustainability initiatives. These adhesives feature specialized polymer backbones and tackifiers that provide strong adhesion to challenging materials such as polypropylene and polyethylene, expanding solvent PSA applications into new markets like EV battery assembly and consumer electronics.

Niche segments such as UV-Resistant, Removable, and Pressure-Activated PSAs serve specialized performance requirements, including solar panel assembly, display lamination, removable protective films, and clean-release labels. While smaller in volume, these categories are innovation-driven and crucial for technological applications where precision, optical clarity, or reversibility are essential. Solvent-based systems remain favored in these areas due to their superior chemical uniformity, controlled viscosity, and predictable curing behavior, which allow fine-tuning of adhesive properties for unique end-use needs.

The solvent PSA market remains dominated by globally diversified companies integrating polymer expertise, coating technology, and sustainable process innovation. The leading players—Avery Dennison, tesa SE, Lohmann, DIC Corporation, 3M, and Henkel AG & Co. KGaA—leverage advanced acrylic and silicone chemistries to deliver durable, high-tack, and weather-resistant adhesive solutions for critical applications.

Avery Dennison leads with its performance tapes and labeling division, focusing on solvent-based acrylic and rubber PSAs for automotive wraps, industrial labels, and solar panels. Its 2025 solar panel PSA portfolio exemplifies its strategy of aligning adhesive innovation with renewable energy trends. With a global manufacturing network and acquisitions like Thermopatch, Avery Dennison has expanded into industrial apparel and textile transfers, integrating solvent-based film adhesives for permanent bonding under high temperature and UV exposure.

tesa SE maintains a dominant position in automotive wire harnessing, component mounting, and industrial bonding applications using solvent-based acrylic and rubber PSAs. Its R&D efforts focus on high-solids, low-VOC solvent chemistries, ensuring compliance with stringent European regulations. The company’s double-sided and foam PSA tapes offer exceptional shear and heat resistance, serving electronics and appliance OEMs. tesa’s value proposition lies in custom-engineered solutions, fine-tuned for customer-specific peel and tack requirements.

Lohmann excels in medical-grade and industrial double-sided tapes, utilizing solvent-based systems designed for biocompatibility, breathability, and controlled adhesion. Its multi-layer adhesive constructions, often combining solvent-based and hot-melt layers, provide differential adhesion ideal for wearable sensors and diagnostic strips. Lohmann’s precision coating in ISO cleanroom environments ensures unmatched uniformity—essential for medical and electronics applications requiring consistent adhesive thickness and flawless film quality.

DIC Corporation stands out for its optically clear solvent PSAs (OCA), used in displays, touch panels, and protective films, offering superior clarity, non-yellowing, and plasticizer resistance. Its recent development of toluene-free solvent systems (QUICKMASTER series) supports global VOC compliance while maintaining performance integrity. Backed by strong presence across Asian electronics manufacturing hubs, DIC is a major supplier for automotive and industrial labeling, excelling in bonding polyolefin and film substrates for durable performance.

3M integrates its vast expertise in adhesives, materials science, and coatings to offer solvent-based acrylic PSAs for industrial tapes, construction panels, and graphics films. Products such as 3M VHB and double-coated tapes deliver mechanical fastener-level performance in transportation and heavy equipment assembly. 3M also leads in medical solvent-based PSAs, combining controlled adhesion, hypoallergenic formulations, and long-wear comfort. Its continued R&D investment in thermal durability and chemical resistance ensures leadership in demanding environments.

Henkel’s Adhesive Technologies division plays a pivotal role in labeling, packaging, and industrial PSA applications, leveraging rubber and acrylic solvent-based adhesives for high-speed conversion and strong initial tack. Henkel focuses on VOC compliance and high-solids innovation, assisting manufacturers in process optimization to meet regional emission standards in Europe and Asia. Its global technical network enables localized adhesive customization, reinforcing Henkel’s leadership in high-performance bonding and regulatory compliance.

Country Analysis: Strategic Developments in the Global Solvent-Based Pressure Sensitive Adhesives (PSA) Industry

China: Expanding Solvent PSA Production and High-End Manufacturing Integration

China continues to lead the global solvent-based pressure-sensitive adhesives (PSA) market, both in terms of production capacity and consumption, supported by its vast industrial infrastructure and policy-driven focus on advanced manufacturing. In September 2024, Henkel AG & Co. KGaA announced a EUR 180 million investment in expanding its Shanghai production facility, specifically targeting automotive and electronics applications—two of the country’s fastest-growing end-user segments. The state-of-the-art expansion integrates AI-driven automation and precision coating systems to ensure consistency and efficiency in high-shear solvent-based PSA formulations, meeting global OEM standards for performance and durability.

Government policies under China’s “Made in China 2025” and “High-End Manufacturing Modernization Plan” are incentivizing domestic R&D into specialty solvent acrylic PSAs with superior heat and chemical resistance. Moreover, rising e-commerce and logistics activity continues to boost the consumption of solvent-based packaging tapes, labeling adhesives, and durable freight seals across manufacturing and warehousing sectors. Environmental compliance, however, remains a key challenge, as regulators increasingly prioritize VOC reduction and solvent recovery systems in large-scale manufacturing zones.

United States: Regulatory Evolution and Advanced PSA Development for High-Tech Applications

The United States solvent PSA industry is advancing toward a high-value, regulation-compliant, and innovation-driven ecosystem. Regulatory oversight by the U.S. Environmental Protection Agency (EPA) continues to shape the market trajectory, particularly with its November 2024 proposal to revise VOC definitions by excluding certain low-reactivity compounds like HCFO-1224yd(Z)—a move expected to influence future solvent selection in adhesive formulations. Concurrently, leading manufacturers such as 3M Company are driving product innovation; in June 2024, 3M launched a new series of VHB™ tapes utilizing high-temperature-resistant solvent-based PSAs that cater to automotive lightweighting, battery protection, and high-shear bonding applications.

The healthcare and electronics industries remain major growth pillars. U.S.-based firms are developing medical-grade solvent acrylic PSAs engineered for long-term skin adhesion and advanced wound care applications, requiring exceptional biocompatibility and solvent purity. Meanwhile, digital transformation in labeling and logistics, led by companies like Avery Dennison, is propelling the demand for printable, high-clarity solvent PSAs suited for smart labels, RFID tags, and thermal transfer applications. As the industry adapts to VOC restrictions and sustainability targets, innovation in hybrid solvent systems, greener formulations, and advanced automation ensures the U.S. remains a leader in premium-grade PSA performance and process optimization.

Germany: Sustainable Solvent PSA Formulation and Automotive Integration

Germany remains the technological nucleus of Europe’s solvent PSA innovation, supported by its advanced chemical manufacturing infrastructure, stringent regulatory framework, and strong automotive engineering base. The country’s adhesive producers are heavily investing in low-VOC, high-solids solvent acrylic PSAs that maintain coating efficiency while minimizing environmental impact. German manufacturers are pioneering reduced-viscosity solvent systems, ensuring high tack and shear performance without compromising on sustainability.

In June 2024, under the European Union’s REACH Directive, chemical producers began phasing out restricted solvents such as DMAC and NEP, accelerating the transition to compliant solvent formulations. Germany’s automotive and industrial segments are key drivers of PSA consumption, particularly for vibration damping, trim bonding, and high-adhesion tapes in luxury vehicle assembly. Additionally, manufacturers are scaling production of industrial-grade laminating films and graphic films that rely on precision-coated solvent PSAs offering UV stability and long-term optical clarity. Supported by world-class R&D capabilities, firms like Henkel and BASF continue to lead the development of next-generation eco-compliant adhesives, reinforcing Germany’s role as the European benchmark for performance and regulatory alignment in the solvent PSA market.

India: Localized Manufacturing Growth and Sectoral Diversification Drive PSA Demand

India’s solvent-based PSA market is rapidly evolving, supported by the country’s expanding manufacturing, automotive, and packaging industries. In 2024, Henkel India announced the establishment of a new application lab in Chennai, scheduled to open in early 2025, aimed at localizing technical support and formulation development for regional customers. The facility strengthens Henkel’s R&D and customer collaboration footprint, enabling faster customization of solvent acrylic PSAs suited for tropical climates and high-humidity applications prevalent across South Asia.

The automotive sector, bolstered by the government’s EV-focused initiatives, is significantly driving demand for heat-resistant, high-bond solvent-based adhesives in battery assembly and electrical insulation. Similarly, the packaging and labeling industry—propelled by India’s booming e-commerce and pharmaceutical sectors—is accelerating the consumption of pressure-sensitive labeling materials and tamper-evident security tapes. Infrastructure-led growth, under initiatives like Gati Shakti and Make in India, further contributes to rising adoption of industrial-grade PSA tapes for construction sealing and temporary protection during large-scale projects. With increased foreign investments and domestic capability building, India is solidifying its position as a strategic manufacturing hub for solvent PSA technologies in the Asia-Pacific region.

Singapore: Sustainable Solvent PSA Manufacturing for the Future of High-Tech Industries

Singapore is emerging as a sustainability-focused hub for specialty chemical production, positioning itself at the forefront of green solvent PSA manufacturing in the Asia-Pacific region. In January 2024, Arkema S.A. inaugurated a EUR 150 million acrylic adhesive production facility, marking a significant investment in renewable energy-powered, circular-economy-driven manufacturing. The facility is designed to produce high-performance solvent-based and UV-curable PSAs that cater to the growing demand from the electronics, automotive, and medical device sectors.

Singapore’s strategic geographic positioning and advanced regulatory framework make it an ideal base for serving fast-growing regional markets, including Malaysia, Indonesia, and Vietnam. The city-state’s emphasis on precision, sustainability, and high-value production aligns with the global industry’s shift toward eco-friendly solvent PSA formulations. The Arkema plant not only enhances regional adhesive capacity but also reflects a larger industry transformation—where sustainable chemistry and innovation converge to redefine the standards of performance, efficiency, and environmental responsibility in solvent-based adhesives manufacturing.

Solvent Pressure Sensitive Adhesives Market Report Scope

Solvent Pressure Sensitive Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$21.5 Billion

|

|

Market Size (2034)

|

$29.8 Billion

|

|

Market Growth Rate

|

3.7%

|

|

Segments

|

By Chemistry Type (Solvent Acrylic, Solvent Rubber-Based, Solvent Silicone, Other Specialty), By Application Type (Tapes, Labels, Graphic Films and Signage, Functional Films & Laminates), By End-Use Industry (Automotive & Transportation, Packaging, Medical & Healthcare, Electronics & Electrical, Building & Construction, Industrial & General Manufacturing, Consumer Goods), By Resin Type (Acrylic Homopolymers, Acrylic Copolymers, Block Copolymers, Polyurethanes, Silicones), By Function (High-Shear, High-Temperature Resistant, Low-Surface Energy Substrate, UV Resistant, Removable, Permanent, Pressure-Activated

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, Avery Dennison Corporation, H.B. Fuller Company, Arkema S.A. (Bostik), The Dow Chemical Company, Sika AG, Wacker Chemie AG, Ashland Global Holdings Inc., Nitto Denko Corporation, LG Chem Ltd., Eastman Chemical Company, Lintec Corporation, Scapa Group PLC, Pidilite Industries Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Chemistry Type

- Solvent Acrylic

- Solvent Rubber-Based

- Solvent Silicone

- Other Specialty

By Application Type

- Tapes

- Labels

- Graphic Films and Signage

- Functional Films & Laminates

By End-Use Industry

- Automotive & Transportation

- Packaging

- Medical & Healthcare

- Electronics & Electrical

- Building & Construction

- Industrial & General Manufacturing

- Consumer Goods

By Resin Type

- Acrylic Homopolymers

- Acrylic Copolymers

- Block Copolymers

- Polyurethanes

- Silicones

By Performance/Function

- High-Shear

- High-Temperature Resistant

- Low-Surface Energy Substrate

- UV Resistant

- Removable

- Permanent

- Pressure-Activated

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Solvent Pressure Sensitive Adhesives Market

- Henkel AG & Co. KGaA

- 3M Company

- Avery Dennison Corporation

- H.B. Fuller Company

- Arkema S.A. (Bostik)

- The Dow Chemical Company

- Sika AG

- Wacker Chemie AG

- Ashland Global Holdings Inc.

- Nitto Denko Corporation

- LG Chem Ltd.

- Eastman Chemical Company

- Lintec Corporation

- Scapa Group PLC

- Pidilite Industries Ltd.

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Global Solvent Pressure Sensitive Adhesives (PSA) Market, mapping demand inflections across automotive, electronics, medical, industrial labeling, and renewable energy tape/film systems; it distills breakthroughs in high-solids solvent acrylics, BTX-free silicone PSAs, low-odor formulations, and closed-loop coating that lift shear endurance, optical clarity, and durability; our analysis reviews regulatory momentum (VOC/REACH/IED), substrate trends (LSE polyolefins, composites), and end-use qualification (high-temp, long-wear medical, outdoor UV) while benchmarking cost, line speed, and conversion yields; it highlights where solvent PSAs retain mission-critical advantages—temperature window, aging resistance, cohesion under load—versus emulsion or hot-melt alternatives, and frames capital priorities in solvent recovery and precision coating.

Scope Highlights

Segmentation:

- By Chemistry Type: Solvent Acrylic; Solvent Rubber-Based; Solvent Silicone; Other Specialty.

- By Application Type: Tapes; Labels; Graphic Films & Signage; Functional Films & Laminates.

- By End-Use Industry: Automotive & Transportation; Packaging; Medical & Healthcare; Electronics & Electrical; Building & Construction; Industrial & General Manufacturing; Consumer Goods.

- By Resin Type: Acrylic Homopolymers; Acrylic Copolymers; Block Copolymers; Polyurethanes; Silicones.

- By Performance/Function: High-Shear; High-Temperature Resistant; Low-Surface-Energy Substrate; UV Resistant; Removable; Permanent; Pressure-Activated.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Historical & Forecast Window: 2021–2024 history with 2025–2034 forecasts.

Companies Covered: 15+ company analyses/profiles.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.