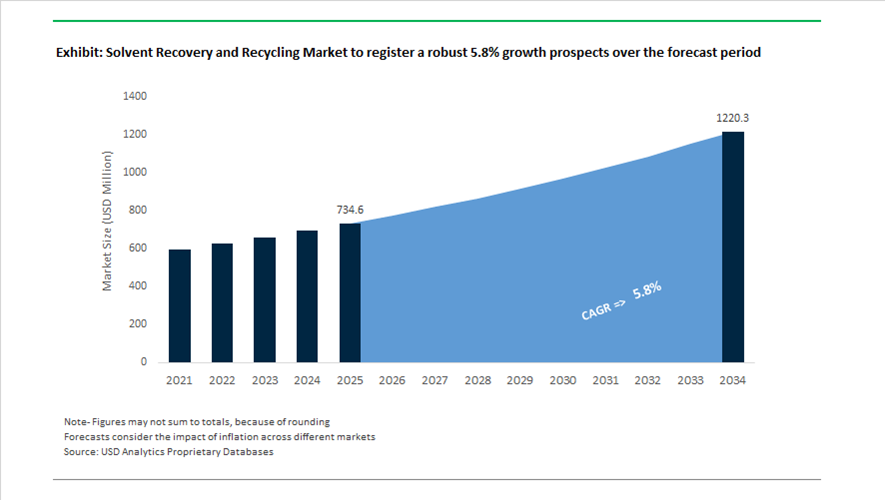

Solvent Recovery and Recycling Market Valuation 2025–2034: $734.6 Million to $1,220.2 Million at 5.8% CAGR Driven by Hazardous Waste Regeneration and Closed-Loop Manufacturing

The global solvent recovery and recycling market is valued at $734.6 million in 2025 and is projected to reach $1,220.2 million by 2034, expanding at a CAGR of 5.8%. Market growth is propelled by tightening hazardous waste regulations, rising disposal costs, decarbonization mandates, and increasing adoption of circular chemical management models across pharmaceuticals, semiconductors, petrochemicals, coatings, and agrochemicals. Industrial solvent regeneration via fractional distillation, thin-film evaporation, membrane separation, and thermal treatment is gaining traction as manufacturers seek to displace virgin solvent procurement, reduce Scope 3 emissions, and improve ESG performance. Closed-loop solvent recovery systems and on-site solvent recycling units are increasingly embedded into capital planning across high-volume chemical processing sectors.

In early 2024, Veolia launched its GreenUP 2024–2027 strategic plan, identifying hazardous waste treatment and solvent regeneration as core growth pillars. In April 2024, Tradebe Environmental Services and Veolia North America formed a long-term partnership granting Tradebe access to Veolia’s Gum Springs, Arkansas thermal treatment and recovery facility, scheduled to open in 2025 to meet growing hazardous waste processing demand. In August 2024, Veolia expanded its Garston, UK solvent recovery facility to 86,000 tonnes per year capacity, utilizing advanced fractional distillation to regenerate pharmaceutical- and semiconductor-grade solvents while reducing an estimated 172,000 tonnes of CO2e annually. These investments reinforced Europe and North America as mature but expanding solvent regeneration hubs.

Operational scaling accelerated in 2025. In early 2025, Indaver began operations at its industrial-scale Plastics2Chemicals plant in Antwerp, applying solvent-intensive depolymerization technologies to recover chemical building blocks with a targeted capacity of 65,000 tonnes per year. In March 2025, Nuveen Private Equity Impact invested $30 million in CleanPlanet Chemical to scale its Recycling-as-a-Service model, which deploys on-site solvent recovery units without upfront CAPEX. CleanPlanet further commercialized its Athena™ real-time solvent tracking platform in 2025, enabling industrial users to monitor solvent recovery volumes and greenhouse gas reductions via IoT-enabled analytics. In April 2025, Tradebe acquired Florachem to deepen integration of sustainable solvent recovery services into U.S. life sciences and fragrance markets. In September 2025, Clean Harbors reported recycling 1.9 million metric tons of materials in 2024, managing nearly 400 million gallons of hazardous liquids including used solvents, achieving its 2030 recycling target six years ahead of schedule.

Strategic infrastructure expansion continued into 2026. In late 2025, Indaver announced a £750 million UK investment plan including a dedicated closed-loop solvent recycling facility at Syngenta’s Huddersfield site, designed to recover 15,000 tonnes of acetonitrile annually for reuse in pesticide manufacturing. In February 2026, Clean Harbors signed a $130 million agreement to acquire select Depot Connect International businesses, adding five U.S. Gulf Coast locations to expand its industrial solvent and hazardous waste management network. These developments highlight how circular manufacturing mandates, digital solvent traceability, on-site regeneration technologies, and consolidation among hazardous waste operators are collectively driving the solvent recovery and recycling market toward $1.22 billion by 2034.

Key Trends and High-Impact Opportunities in the Solvent Recovery and Recycling Market

Mandated On-Site Solvent Recovery in Pharmaceuticals and Electronics

The solvent recovery and recycling market is undergoing a structural shift as large manufacturers internalize solvent regeneration to meet ESG targets, secure supply chains, and reduce operational risk. Solvents are increasingly treated as strategic in-house feedstocks rather than waste liabilities, enabling companies to cut Scope 1 emissions while avoiding the regulatory and safety risks associated with off-site hazardous waste transport. This transition is particularly pronounced in pharmaceuticals, where solvent purity, traceability, and compliance with Good Manufacturing Practice are non-negotiable.

During 2024 and 2025, the pharmaceutical industry emerged as the largest adopter of Solvent Recovery Units, accounting for roughly 28% of global installations. API manufacturers are investing in capital-intensive multi-stage distillation columns, vacuum systems, and high-efficiency condensers capable of restoring solvents to 99% purity. These systems allow continuous reuse of high-value solvents while supporting corporate net-zero commitments and reducing dependence on volatile virgin solvent markets.

A parallel trend is unfolding in electronics manufacturing. Semiconductor producers are scaling advanced recovery technologies to address the enormous volumes of solvents and process gases used in wafer fabrication. As of late 2024, Samsung Semiconductor had expanded its fleet of Regenerative Catalytic Systems to more than 52 operational units. Third-generation catalyst upgrades have lifted treatment efficiencies to approximately 97%, significantly lowering the direct greenhouse gas footprint of semiconductor fabrication and reinforcing solvent recovery as a core decarbonization lever rather than a peripheral environmental control.

Contract Recycling Expansion Across the Battery and EV Supply Chain

The rapid expansion of lithium-ion battery manufacturing is creating a specialized and high-growth demand for solvent recovery, particularly for N-Methyl-2-pyrrolidone. NMP is indispensable for electrode slurry preparation, yet it represents one of the highest recurring operating costs in battery production. To manage this exposure, battery manufacturers are increasingly entering long-term contracts with third-party solvent recyclers, embedding recovery into the core economics of gigafactory operations.

By 2025, the global market for lithium battery NMP recovery and purification reached an estimated valuation of $3.11 billion, reflecting the scale of solvent volumes involved. The industry is moving toward centralized recovery parks, especially in China and India, where multiple battery producers can access shared high-capacity purification infrastructure. In India, government policy is accelerating this model. The Production Linked Incentive scheme offers subsidies of up to 15% for chemical and pharmaceutical recovery installations, incentivizing localized recycling of battery-grade solvents and reducing import dependency.

Strategic partnerships are reinforcing circularity across adjacent sectors. In December 2025, Prysmian and Versalis announced a collaboration to chemically recycle complex polymeric waste such as cross-linked polyethylene into high-performance raw materials. Similar service-based circularity models are becoming standard for NMP, where recovered solvent is routinely purified to electronic grade exceeding 99.9% purity and fed directly back into battery cell production lines.

Mobile and Modular Recovery Units for Small-Batch Solvent Generators

A fast-emerging opportunity lies in mobile and modular solvent recovery systems designed for small and medium-sized generators. Many SMEs and short-duration industrial campaigns lack the scale or capital to justify permanent recovery facilities, yet they still face rising disposal costs and tightening VOC regulations. Containerized and truck-mounted systems are addressing this gap by delivering recovery capabilities without long-term infrastructure commitments.

Modular units now account for nearly 28% of new equipment demand, driven by industries such as printing, coatings, and specialty chemicals where solvent waste streams are diverse and intermittent. These plug-and-play systems allow facilities with limited floor space to recover solvents on-site, achieving payback periods of 12 to 24 months by cutting virgin solvent purchases and disposal fees. Service-based models are expanding alongside equipment sales. Truck-mounted recovery units are increasingly deployed to process hazardous waste directly at customer sites, eliminating transportation liabilities and ensuring compliance with stringent emission controls. In North America, this recovery-on-wheels approach is gaining traction as facilities seek to comply with Maximum Achievable Control Technology standards enforced by the U.S. Environmental Protection Agency for volatile organic compound emissions.

Advanced Purification Technologies for Complex and Azeotropic Waste Streams

Traditional distillation technologies are often insufficient for the complex solvent mixtures generated in agrochemicals, specialty polymers, and advanced materials manufacturing. This limitation is opening a high-margin opportunity for advanced purification technologies capable of handling azeotropes, trace contaminants, and multi-component waste streams.

Membrane-based and hybrid separation technologies are at the forefront of this shift. The EU-funded Mem4Bat project, which completed a major development phase in late 2024, demonstrated nanofiltration membranes capable of removing trace metals and water from spent NMP streams. These systems enable recovered solvents to achieve near-virgin performance, making them suitable for reuse in the most sensitive battery and semiconductor applications. Beyond recovery, advanced purification is enabling waste-to-chemicals innovation. In October 2025, the Global Impact Coalition, comprising BASF, Clariant, and Covestro, partnered with ETH Zurich to explore gasification and downstream purification routes that convert heterogeneous waste into C2 plus chemical building blocks. These initiatives signal a structural evolution where solvent recovery hubs are transformed from cost centers into revenue-generating assets within circular chemical value chains.

Solvent Recovery and Recycling Market Share and Segmentation Insights

Distillation Technology Dominates Solvent Recovery Systems Through Versatility and Process Efficiency

Distillation accounted for 52.80% of the solvent recovery and recycling market in 2025, making it the most widely deployed technology across industrial solvent recovery operations. Distillation systems are capable of processing diverse solvent streams with varying compositions, enabling the recovery of high-purity solvents suitable for reuse in manufacturing processes. Both batch distillation units and continuous distillation systems are commonly used across industries such as pharmaceuticals, chemicals, coatings, and electronics. A key 2025 industry advancement is the focus on energy efficiency optimization in solvent distillation, where technologies such as heat integration, vapor recompression systems, and advanced column internals have reduced energy consumption by approximately 30 to 50%, improving the economic viability of solvent recycling compared with purchasing virgin solvents and managing hazardous waste disposal.

Pharmaceutical Industry Drives Demand for Solvent Recovery and Recycling Systems

Pharmaceutical manufacturing represents the largest end-use segment in the solvent recovery and recycling market, accounting for 32.80% of global demand in 2025 due to the extensive use of organic solvents in drug synthesis and formulation processes. Pharmaceutical production often involves high-value solvents that must meet strict purity and regulatory standards, making solvent recovery economically attractive. Recycling systems help manufacturers reduce raw material costs, hazardous waste generation, and environmental emissions while maintaining solvent quality. A major 2025 industry trend is the increasing adoption of continuous pharmaceutical manufacturing, where solvent recovery units are integrated directly into production lines. These in-line solvent recycling systems enable real-time solvent purification and reuse, reducing solvent inventory levels and improving process sustainability.

Solvent Recovery and Recycling Market Competitive Landscape

The global solvent recovery and recycling market in 2026 is driven by closed-loop recycling mandates, high-purity solvent reclamation, and PFAS-compliant processing technologies. Industry leaders are investing in fractional distillation, pervaporation, and integrated waste management platforms to enhance resource security, reduce Scope 3 emissions, and ensure pharmaceutical- and semiconductor-grade solvent purity.

Veolia Expands High-Purity Solvent Recovery Through Hazardous Waste Integration and AI-Driven Circular Platforms

Veolia is leading the solvent recovery and recycling market with €44.4 billion in 2025 revenue and strong growth in its Hazardous Waste segment. Its Gum Springs facility in Arkansas sets a benchmark for solvent recovery using advanced thermal treatment and renewable-powered operations. The company’s GreenUp strategy is accelerating acquisitions and strengthening its circular economy platform for industrial solvent valorization. AI-driven optimization contributes significantly to efficiency gains, enhancing distillation and separation of complex waste streams. Veolia’s integrated water and waste technologies enable high-purity solvent recovery aligned with pharmaceutical and semiconductor requirements. Its focus on circular synergies and digitalization strengthens its leadership in closed-loop solvent systems.

Clean Harbors Strengthens PFAS-Compliant Solvent Recycling and High-Margin Environmental Services Growth

Clean Harbors, through its Safety-Kleen division, is dominating the North American solvent recycling market with $6.03 billion in 2025 revenue and strong EBITDA margins of 25.9%. The company has exceeded its 2030 recycling targets, processing 1.9 million metric tons of waste and recycling nearly 16 million gallons of solvents annually. Its “Total PFAS Solution” integrates sampling, transport, and near-total destruction of PFAS contaminants within solvent recovery workflows. The Phoenix Hub enhances logistics and treatment efficiency for used oil and solvent recycling across the Western U.S. Clean Harbors’ focus on technical recycling services and compliance-driven solutions strengthens its competitive positioning. Its advanced infrastructure supports high-purity solvent recovery for critical industries.

Tradebe Environmental Services Advances Closed-Loop Solvent Recycling with Integrated Logistics and VOC Abatement

Tradebe Environmental Services is positioning itself as a high-agility provider of closed-loop solvent recycling solutions for pharmaceutical and industrial clients. Its agreement with Veolia ensures access to advanced thermal treatment capacity for complex hazardous waste streams. Tradebe’s model focuses on collecting, purifying, and returning solvents to original specifications, supporting circular chemical use. Integration of tank and railcar cleaning operations enhances logistics efficiency and reduces contamination risks. The company is expanding vapor recovery units to capture VOC emissions during solvent processing, aligning with environmental compliance standards. Its end-to-end service capability strengthens its role in high-purity solvent recovery markets.

Crystal Clean Expands Renewable Solvent Solutions and PFAS Remediation Through Strategic Acquisitions

Crystal Clean is strengthening its presence in solvent recovery through the acquisition of Worldwide Recovery Systems, expanding capacity across the U.S. West Coast. Its Solvent Exchange program provides recyclable chlorinated and non-chlorinated solvents tailored for industrial cleaning applications. The company’s 4never™ PFAS solution enables on-site remediation of contaminated solvent streams, reducing environmental liability. Its SAFF®10 technology supports decentralized treatment and enhances operational flexibility for industrial clients. Re-refined solvents and base oils deliver up to 77% lower greenhouse gas emissions compared to virgin products, supporting sustainability-driven procurement. Crystal Clean’s focus on renewable solutions and compliance technologies enhances its competitiveness.

GFL Environmental Strengthens Liquid Waste Processing and Recycling Infrastructure for Industrial Solvent Streams

GFL Environmental is expanding its role in solvent recovery through its Environmental Services division, supported by projected 2026 revenue of $7.0 billion and strong EBITDA performance. The company’s strategic focus on liquid waste management enables processing of diverse solvent streams, including oil-water mixtures and glycol-based waste. Investments in Extended Producer Responsibility infrastructure support the capture and recycling of solvent-contaminated materials. Its relocation to Miami Beach and improved financial leverage position GFL for further acquisitions in recycling infrastructure. The company’s growth capital deployment enhances sorting and processing capabilities for solvent recovery. GFL’s integrated waste management platform supports the increasing demand for closed-loop recycling systems.

United States Solvent Recovery and Recycling Market Driven by EPA Enforcement and On-Site Systems

The United States solvent recovery and recycling industry is being reshaped by stricter hazardous waste enforcement, state-level VOC caps, and rapid adoption of on-site recovery technologies. In April 2024, Veolia North America and Tradebe Environmental Services entered a three-year strategic agreement centered on the high-temperature thermal treatment facility in Gum Springs, Arkansas, which became operational in late 2025. This facility has strengthened national capacity for handling high-risk solvent residues and complex hazardous waste streams from pharmaceuticals, chemicals, and advanced manufacturing. Parallel to centralized infrastructure, decentralized recovery is accelerating. Maratek reported record deployments of on-site solvent recovery units in 2025 across automotive manufacturing and flexographic printing, with customers achieving solvent reuse rates exceeding 90%.

Regulatory pressure is a primary catalyst. Following a 2024 ruling by the Environmental Protection Agency, pharmaceutical manufacturers are now expected to reach 90% solvent recovery to avoid non-compliance penalties that can exceed USD 200,000 per violation. Chemical majors such as DuPont have responded by integrating solvent recovery units directly into production lines to comply with tightened federal hazardous air pollutant limits. At the state level, stringent VOC regulations in California are accelerating adoption of vacuum distillation for high-value solvents such as NMP and acetone. Corporate behavior is also shifting, with more than 78% of Fortune 500 industrial firms now disclosing solvent recovery performance within 2025 ESG reporting frameworks.

Germany Solvent Recovery and Recycling Market Anchored by EU Directives and Circular Economy Law

Germany’s solvent recovery market is defined by regulatory precision, industrial compliance, and system-wide circularity. Under the EU Industrial Emissions Directive, German manufacturers in coatings and adhesives are now achieving mandated solvent recovery rates of 95% for high-volume applications. This has driven widespread investment in advanced distillation, adsorption, and membrane-based recovery systems across chemical parks. In mid-2024, BASF SE introduced a portfolio of bio-based flocculants and separation agents engineered to reduce carbon footprints by 25% compared with petroleum-derived alternatives, enhancing both recovery efficiency and sustainability metrics.

National policy has reinforced adoption. Updates to Germany’s Circular Economy Act have incentivized Waste-to-Resource models, resulting in roughly 70% of domestic chemical producers deploying advanced solvent recovery systems by early 2025. Compliance readiness extends to chemical safety, with German firms completing the removal of restricted siloxanes from recycling processes ahead of the 2026 EU REACH deadline. Automotive manufacturing illustrates the economic upside. Volkswagen reported in late 2024 that integrated paint-shop solvent recovery reduced virgin solvent procurement costs by 30%, validating recovery as both a compliance and margin lever.

India Solvent Recovery and Recycling Market Expanded by EPR Rules and Textile Digitalization

India’s solvent recovery and recycling industry is expanding through regulatory expansion, textile sector modernization, and municipal integration with energy recovery. The 2025 Plastic Waste Management Amendments issued by the Ministry of Environment, Forest and Climate Change introduced mandatory traceability via a centralized digital portal, covering solvent-intensive polymer recycling operations. This has increased demand for auditable solvent recovery systems across plastics and packaging value chains. Complementing this, the BioE3 policy launched in 2024 has funded bio-foundries to commercialize bio-based solvents and recycle agricultural-waste-derived chemicals such as solketal, embedding solvent recovery within broader Waste-to-Wealth objectives.

Industrial adoption is visible at cluster level. In Gujarat, more than 200 textile manufacturers have installed on-site solvent recovery units to manage effluents from digital inkjet printing, delivering estimated operational cost reductions of 15% while improving compliance. The expansion of Extended Producer Responsibility rules in 2025 to include used oils and industrial solvents has further formalized recovery obligations. At the municipal scale, cities such as Indore and Pune have integrated solvent-sludge treatment into Waste-to-Energy plants, reducing landfill reliance and improving overall waste system efficiency.

China Solvent Recovery and Recycling Market Shaped by Five-Year Plan Targets and Semiconductor Purity

China’s solvent recovery and recycling market is characterized by scale, policy enforcement, and strategic alignment with advanced manufacturing. By the end of 2025, China met its target of 90% harmless disposal for urban industrial sludge and solvent waste under mandates from the National Development and Reform Commission. Achieving this milestone required extensive deployment of solvent recovery, thermal treatment, and residue minimization technologies across industrial zones.

Investment support is accelerating SME participation. The Ministry of Industry and Information Technology established a CNY 40 billion fund in 2025 to subsidize transitions toward low-VOC manufacturing and solvent recovery systems, particularly for small and medium-sized factories. Strategic industries are prioritized. Semiconductor producers are advancing ultra-high purity solvent recovery to secure domestic supply of electronic-grade isopropyl alcohol for 5 nm chip fabrication. In packaging, enforcement of GB 4806.16-2025 has eliminated non-compliant volatile substances from food-contact solvent systems, embedding recovery and recycling as prerequisites for market access.

Comparative Snapshot: Country-Level Solvent Recovery and Recycling Dynamics

Solvent Recovery and Recycling Market County Level Snapshot

|

Country

|

Primary Drivers

|

Strategic Focus Areas

|

Structural Impact

|

|

United States

|

EPA enforcement, VOC caps, ESG disclosure

|

On-site SRUs, vacuum distillation, HAP compliance

|

Rapid decentralization and corporate adoption

|

|

Germany

|

EU IED, Circular Economy Act, REACH

|

Bio-based separation aids, high recovery thresholds

|

System-wide circular compliance

|

|

India

|

EPR expansion, textile digitalization

|

Cluster-level on-site recovery, WTE integration

|

Formalization and cost efficiency gains

|

|

China

|

Five-Year Plan targets, SME subsidies

|

UHP solvent recovery, low-VOC manufacturing

|

Policy-driven scale and supply chain security

|

Solvent Recovery and Recycling Market Report Scope

Solvent Recovery and Recycling Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$734.6 Million

|

|

Market Size (2034)

|

$1220.2 Million

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Technology (Distillation, Membrane Separation, Adsorption, Extraction, Cryogenic Recovery), By Solvent Type (Aromatic Solvents, Alcohols, Ketones, Chlorinated Solvents, Esters, Glycols & Glycol Ethers), By End-Use Industry (Pharmaceuticals, Paints, Coatings & Adhesives, Printing & Packaging, Automotive, Electronics & Semiconductors, Chemical Manufacturing), By Service Model (On-Site Recycling, Off-Site Recovery)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia Environmental Services, Clean Harbors Inc., Suez SA, BASF SE, Tradebe Environmental Services, Kemira Oyj, Maratek Environmental Inc., Solenis, CycleSolv LLC, Clean Planet Chemical, Ecolab Inc., Kurita Water Industries Ltd., Mitsubishi Chemical Group, Bebington Machinery, Zhejiang Xinan Chemical Industrial Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Solvent Recovery and Recycling Market Segmentation

By Technology

- Distillation

- Membrane Separation

- Adsorption

- Extraction

- Cryogenic Recovery

By Solvent Type

- Aromatic Solvents

- Alcohols

- Ketones

- Chlorinated Solvents

- Esters

- Glycols & Glycol Ethers

By End-Use Industry

- Pharmaceuticals

- Paints, Coatings & Adhesives

- Printing & Packaging

- Automotive

- Electronics & Semiconductors

- Chemical Manufacturing

By Service Model

- On-Site Recycling

- Off-Site Recovery

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Solvent Recovery and Recycling Industry

- Veolia Environmental Services

- Clean Harbors Inc.

- Suez SA

- BASF SE

- Tradebe Environmental Services

- Kemira Oyj

- Maratek Environmental Inc.

- Solenis

- CycleSolv LLC

- Clean Planet Chemical

- Ecolab Inc.

- Kurita Water Industries Ltd.

- Mitsubishi Chemical Group

- Bebington Machinery

- Zhejiang Xinan Chemical Industrial Group

*- List not Exhaustive