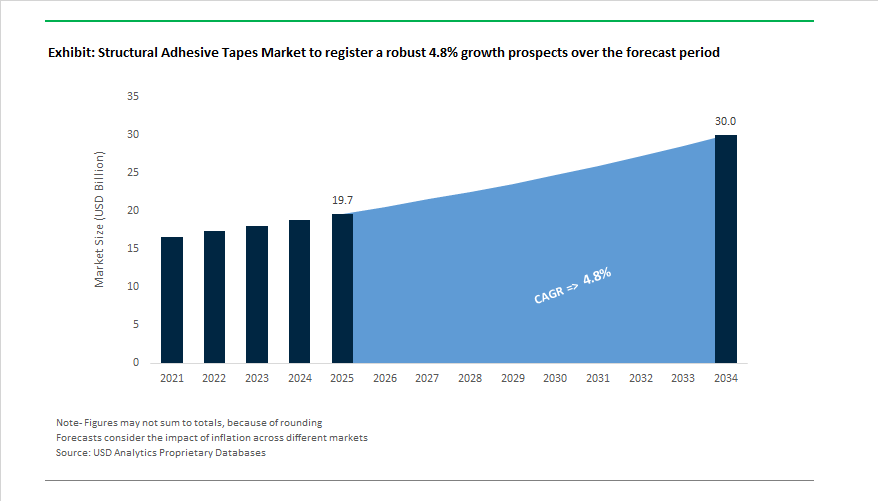

The Global Structural Adhesive Tapes Market is projected to grow from USD 19.7 billion in 2025 to USD 30 billion by 2034, advancing at a CAGR of 4.8%, reflecting a structural re-rating of adhesive tapes within industrial joining strategies. Structural adhesive tapes are increasingly specified as primary load-bearing bonding systems that replace rivets, screws, spot welding, and liquid structural adhesives. This shift is being driven by OEM imperatives around lightweighting, fatigue resistance, vibration damping, corrosion mitigation, and takt-time reduction, particularly in transportation, electronics enclosures, and modular construction.

From a manufacturer perspective, market leadership is defined by viscoelastic engineering and adhesive–foam–film system design, rather than basic adhesion strength. Suppliers such as 3M (VHB™ structural acrylic tapes), tesa (ACXplus™ series), Saint-Gobain (Norbond™ and structural bonding tapes), and Nitto Denko have built portfolios where tapes are engineered to sustain continuous static and dynamic loads, distribute stress across bonded interfaces, and maintain bond integrity under thermal cycling and differential material expansion. Acrylic foam-based structural tapes, in particular, are designed to absorb micro-movement and vibration—capabilities that mechanical fasteners and rigid epoxies struggle to deliver without inducing stress concentrations or crack initiation over time.

A critical market driver is the replacement of multi-step joining processes with single-step tape bonding. Structural tapes eliminate drilling, surface damage, curing ovens, and rework associated with liquid adhesives, enabling immediate handling strength and predictable bond-line thickness. This process simplification has measurable downstream impact: reduced assembly time, lower scrap rates, and improved cosmetic quality by avoiding fastener heads and weld marks. As a result, structural tapes are increasingly qualified early in product design cycles, particularly for mixed-material assemblies involving aluminum, coated steels, composites, and engineered plastics where galvanic corrosion and thermal mismatch are persistent challenges.

Material innovation is also reshaping market dynamics. Manufacturers are expanding high-temperature-resistant acrylic systems, epoxy-based structural tapes for higher modulus requirements, and hybrid constructions that balance peel strength, shear load, and environmental durability. Parallel to performance gains, sustainability constraints are influencing formulation and backing selection. Structural tape producers are advancing solvent-free adhesive systems, thinner high-strength constructions, and recyclable-compatible backings, aligning with OEM sustainability targets without compromising mechanical performance—an increasingly non-negotiable requirement in automotive and electronics supply chains.

The global structural adhesive tapes industry is witnessing an unprecedented wave of innovation, M&A activity, and sustainability initiatives led by top-tier chemical and material science companies.

In October 2025, 3M deepened its technology footprint by joining the JOINT3 semiconductor packaging consortium, marking a major pivot into advanced microelectronic bonding and thermal management adhesives. Just a month earlier, at IAA Mobility 2025 (September 2025), 3M highlighted its next-generation lightweighting and EV bonding solutions, demonstrating leadership in automotive electrification and adhesive integration. Celebrating a century of innovation in July 2025, 3M’s Scotch™ Brand reaffirmed its industrial legacy spanning automotive, construction, and electronics applications.

Avery Dennison has been equally active, launching EV battery wrapping tapes with PET facestock in June 2025 to enhance dielectric protection and safety, while also expanding into the flooring adhesives sector through the August 2025 acquisition of Meridian Adhesives’ business. Earlier, in February 2025, Avery Dennison introduced a dedicated PSA tape portfolio for the appliance industry, engineered to optimize NVH damping and assembly efficiency.

In June 2025, Henkel made significant strides at The Battery Show Europe, unveiling AI-driven virtual adhesive modeling and 12 MPa debonding technologies that enable battery disassembly and recycling. tesa SE, on the other hand, took a major sustainability step in May 2025 by connecting its Hamburg facility to the hydrogen network, planning to produce the world’s first hydrogen-based adhesive tapes by 2027. Sika AG, through its January 2025 acquisitions and manufacturing expansions, continues to strengthen its construction bonding and industrial assembly portfolio, while Henkel’s Pattex launch in September 2024 introduced removable structural adhesives for the DIY market, signaling the blurring boundaries between industrial and consumer-grade adhesive technologies.

Market Trend 1: Rapid Adoption in Electric Vehicle Battery Pack Assembly for Lightweighting and Thermal Management

The rise of electric mobility has created a transformative opportunity for structural adhesive tapes in EV battery pack assembly. By replacing traditional mechanical fasteners and liquid adhesives, these tapes offer reduced vehicle weight, enhanced thermal regulation, and improved assembly efficiency.

Leading OEM collaborations, such as Avery Dennison’s partnership with EV manufacturers, exemplify the shift. Their pressure-sensitive bonding tapes deliver instant adhesion for cell-to-cell and module-level bonding, eliminating curing times and minimizing assembly downtime. With thinner profiles and lower density, these tapes contribute directly to lightweighting initiatives, improving EV range and sustainability metrics.

Material performance has become the defining factor. Acrylic foam adhesive tapes, for instance, demonstrate superior stress absorption, shock resistance, and high chemical and thermal stability—essential for withstanding the demanding conditions of lithium-ion battery enclosures. In addition, safety-focused innovation is underway, as seen with Coroplast Tape’s high-temperature battery insulation tapes, engineered to mitigate thermal runaway and maintain intercellular insulation.

By offering **multifunctionality—adhesion, sealing, insulation, and fire protection—**these tapes are positioned as strategic enablers of next-generation battery module design and high-volume EV manufacturing. Their contribution to weight savings, automation compatibility, and durability underpins their rapid market penetration in the automotive and e-mobility ecosystem.

Market Trend 2: Proliferation of High-Temperature, Electrically Conductive Tapes for Electronics Shielding and Grounding

The growing complexity and miniaturization of 5G infrastructure, automotive electronics, and aerospace systems are propelling demand for multifunctional structural tapes that combine mechanical bonding strength with electrical conductivity and EMI protection.

Modern electrically conductive acrylic adhesive tapes—especially those using metallized fabric or conductive foam carriers—deliver isotropic conductivity (X, Y, and Z-axis) and provide robust EMI shielding across the 450 MHz to 3.8 GHz spectrum, critical for maintaining data integrity in 5G and IoT devices. These tapes replace traditional soldering or screw-based assemblies, simplifying production while enabling rework-friendly, flexible connections.

Polyimide film-based tapes have emerged as a cornerstone material due to their exceptional thermal endurance (−269°C to +400°C) and resistance to radiation and solvents. Their versatility in high-power aerospace, defense, and industrial electronics ensures stability in extreme environments where conventional adhesives fail.

Additionally, the convergence of thermal conductivity and flame retardancy has resulted in hybrid designs that achieve thermal conductivities up to 2 W/mK while meeting UL 94 V-0 safety standards. These advanced structural tapes serve dual roles—mechanical joining and heat dissipation—reducing the need for separate thermal interface materials in dense electronic architectures like servers and EV control units.

Market Opportunity 1: Development of Debondable/Reversible Structural Tapes for Electronics Repair and Recycling

The shift toward circular economy principles and right-to-repair legislation is opening a breakthrough frontier for reversible structural adhesives. As the electronics and EV sectors move toward sustainable product lifecycles, the ability to debond components without damage is becoming a core differentiator in adhesive innovation.

Emerging materials like Pressure-Sensitive Ionoadhesive (PSIA) tapes demonstrate controlled debonding efficiency of over 90% separation within one minute under low electrical voltages, providing safe and energy-efficient disassembly of electronics. These reversible tapes enable manufacturers to reclaim high-value substrates—such as aluminum frames or display panels—without resorting to destructive dismantling.

Regulatory momentum is accelerating the demand. The EU’s Right to Repair Directive, mandating repairability for up to 10 years for certain electronics, reinforces the market opportunity for debonding-on-demand tapes. Manufacturers like Henkel are actively addressing the need with trigger-based debondable adhesives, which can release structural bonds under heat or electrical stimuli while maintaining high adhesion strength (up to 12 MPa) during use.

Such innovation not only enhances end-of-life recyclability but also aligns with corporate sustainability commitments and EPR (Extended Producer Responsibility) mandates, positioning reversible structural tapes as key enablers of circular manufacturing ecosystems.

Market Opportunity 2: Engineering of Vibration-Damping Structural Tapes for Urban Air Mobility and Advanced Robotics

As industries like Urban Air Mobility (UAM) and industrial robotics expand, the demand for vibration-damping structural tapes has emerged as a high-value application area. These sectors require materials that combine strong adhesion, dynamic load absorption, and acoustic damping to protect sensitive components and ensure operational precision.

In high-precision robotics, vibration mitigation directly impacts component reliability and sensor performance. A 2022 study documented a 19% reduction in hard-drive failure rates in systems utilizing specialized vibration-damping adhesives, showcasing the measurable benefits of controlled energy absorption in high-frequency operational environments.

In parallel, the aerospace industry has validated the performance of damping tapes, with interior panel applications achieving 6–8 decibel noise reduction—a performance metric equally relevant to eVTOL aircraft seeking to meet stringent acoustic certification standards.

Structural damping designs typically utilize acrylic foam tapes applied over 30% of the bonded surface area to achieve optimal vibration and noise suppression without adding significant mass. The lightweight yet high-damping characteristic is critical for both airframe construction and robotic systems, where weight and precision are engineering constraints.

As autonomous robotics, drones, and air taxis enter mass production, the integration of vibration-damping structural tapes is expected to play a pivotal role in ensuring component longevity, passenger comfort, and system stability in next-generation transportation and automation systems.

Structural Adhesive Tapes Market Share Insights, 2025-2034

Market Share by Product Thickness

The thick gauge structural adhesive tapes segment, primarily comprising foam-based tapes, holds the largest share of the global structural adhesive tapes market, accounting for 43.2% of total demand in 2025. These tapes dominate due to their superior gap-filling capabilities, vibration damping, and sound absorption properties, which make them indispensable in automotive, construction, and appliance manufacturing applications. Their ability to bond dissimilar and uneven surfaces provides both mechanical stability and design flexibility, aligning with the global trend toward lightweighting and assembly simplification. Medium gauge tapes maintain a significant presence across electronics and industrial assembly applications, balancing flexibility and high shear strength to support panel bonding, electronic module attachment, and enclosure sealing. Meanwhile, thin gauge transfer tapes cater to highly specialized applications requiring minimal thickness, precision bonding, and thermal stability — critical attributes in semiconductor packaging, display assembly, and flexible electronics manufacturing.

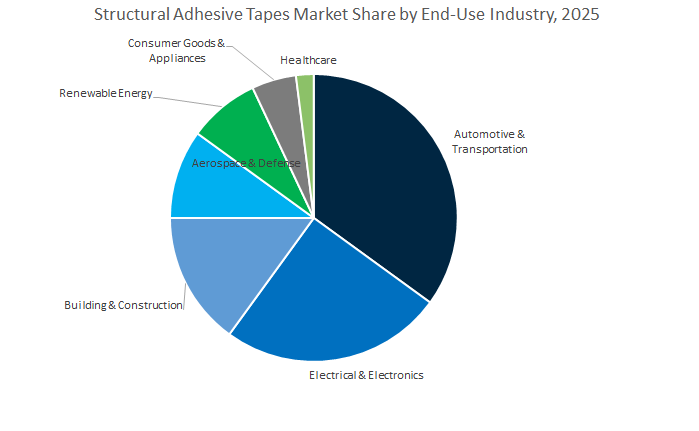

Market Share by End-Use Industry

The automotive and transportation segment remains the largest end-use industry for structural adhesive tapes, commanding an estimated 34.3% share of the global market in 2025. This dominance stems from their widespread adoption in vehicle body assembly, trim attachment, emblems, and EV battery systems, where they replace traditional welding and mechanical fasteners to reduce weight and enhance design flexibility. The increasing production of electric vehicles (EVs) has intensified demand for high-performance structural tapes capable of withstanding thermal stress, vibration, and high-voltage environments. Electrical and electronics applications are expanding rapidly, driven by miniaturization and the need for reliable bonding and heat management in smartphones, wearables, and display modules. The building and construction sector remains a crucial market, employing structural tapes for facade panels, curtain walls, and glazing systems requiring durability, UV resistance, and long-term adhesion. Aerospace and renewable energy sectors collectively represent high-value growth areas, using structural tapes in composite bonding, solar module lamination, and wind turbine blade manufacturing, where performance consistency and load-bearing strength are essential.

The structural adhesive tapes market is characterized by the presence of diversified global leaders—3M, Henkel, tesa SE, Avery Dennison, and Sika AG—each leveraging R&D excellence, sustainability initiatives, and strategic partnerships to redefine industrial bonding. Their continuous investment in viscoelastic, debond-on-demand, and bio-based adhesive systems is reshaping performance standards across automotive, aerospace, and electronics manufacturing.

3M Company remains the undisputed leader in pressure-sensitive adhesive (PSA) innovation with its globally recognized VHB™ series. Its viscoelastic acrylic foam technology provides exceptional stress distribution, vibration damping, and sealing performance, making it ideal for automotive, electronics, and building façades. Beyond traditional applications, 3M is venturing into semiconductor packaging and microelectronics, leveraging its participation in the JOINT3 consortium (October 2025). By offering FEA data integration for engineers, 3M bridges adhesive science with predictive simulation, enhancing performance design for structural glazing and vehicle assembly.

Henkel, the world’s largest adhesive manufacturer, continues to revolutionize bonding through Debond-on-Demand technology and AI-powered virtual adhesive platforms. In June 2025, it demonstrated structural adhesives capable of 12 MPa bonds with controlled debonding, a breakthrough for EV battery recycling and maintenance. Henkel’s Pattex No More Nails Stick & Peel (September 2024) further diversified its presence into consumer structural adhesives. Its portfolio includes thermal management solutions capable of enduring temperatures up to 1400°C, meeting safety and performance standards for electric vehicle (EV) and aerospace applications.

tesa SE is at the forefront of sustainability-driven adhesive innovation. With its Hydrogen Technology initiative (May 2025), tesa aims to produce the world’s first hydrogen-powered adhesive tapes by 2027. The company’s Sparta, USA plant, fully solvent-free, achieved a 38% reduction in CO₂ emissions since 2024, reinforcing its decarbonization roadmap. tesa’s extensive integration in the automotive and electronics assembly supply chain, where up to 130 tesa® tapes are used per vehicle, underscores its leadership in high-precision, bio-based, and recyclable bonding solutions.

Avery Dennison continues to expand its influence through targeted innovation and acquisitions. In February 2025, it launched a 40-product PSA tape portfolio for appliance assembly, emphasizing gasket bonding and NVH damping performance. The company’s June 2025 EV battery tape line introduced dielectric safety and corrosion-resistant adhesives, aligning with U.S. IRA regulatory standards. The August 2025 acquisition of Meridian Adhesives’ flooring division strategically extended its materials expertise into construction adhesives, capitalizing on the growing synergy between structural bonding and architectural applications.

Sika AG remains a dominant force in construction and automotive structural adhesives, integrating polyurethane, silane-modified, epoxy, and acrylate technologies into its high-performance product portfolio. In 2024, Sika expanded its manufacturing capabilities in Singapore and Xi’an, reinforcing its infrastructure adhesives footprint in Asia. The acquisition of Cromar Building Products (2025) strengthened its construction tape and sealing systems, creating new cross-selling channels in roofing and structural sealing. Sika’s continuous investment in R&D-driven, lightweight, and high-strength bonding systems aligns with global trends in energy-efficient and sustainable mobility.

Country Analysis: Regional Dynamics Shaping the Global Structural Adhesive Tapes Industry

China – EV Electrification and High-Tech Manufacturing Propel Structural Tape Expansion

China remains the global leader in structural adhesive tapes production and consumption, driven by the government’s “Made in China 2025” initiative and the country’s dominant electric vehicle (EV), electronics, and renewable energy sectors. The widespread use of structural foam and acrylic tapes in EV battery pack encapsulation, lightweight bonding, and heat management continues to expand, as automotive OEMs prioritize high-performance bonding solutions over traditional mechanical fasteners. New fire-resistance regulations in 2024 for EV battery modules have accelerated R&D in flame-retardant and high-temperature acrylic structural tapes, particularly for lithium-ion battery safety applications.

The surge in solar photovoltaic and wind energy investments is driving demand for UV-resistant, weatherproof structural tapes used in solar panel framing and wind turbine blade assembly. Meanwhile, the electronics manufacturing hubs in Shenzhen and Suzhou are adopting precision-engineered, low-VOC structural acrylic tapes for compact device assembly and display bonding. Domestic producers are expanding capacity for double-sided and permanent bonding tapes, integrating automation in high-speed production lines to serve global clients. The expansion reinforces China’s strategic role as a high-volume, high-tech hub for EV structural tapes, solar PV adhesive systems, and advanced electronic bonding materials.

Germany – Advanced Engineering and Circular Design Drive Structural Tape Innovation

Germany stands at the forefront of automotive lightweighting, advanced construction, and structural glazing applications, leveraging its engineering precision and sustainability-first industrial framework. Leading automotive manufacturers, including Volkswagen, BMW, and Mercedes-Benz, are replacing welding and mechanical fasteners with high-strength structural adhesive tapes to achieve mixed-material joining essential for meeting stringent EU CO₂ reduction targets. A recent multi-million Euro investment by a major German adhesive producer expanded European capacity for structural foam tapes engineered for architectural façade bonding and insulation systems, supporting sustainable construction practices.

The country’s commitment to the circular economy is influencing R&D toward debondable and recyclable structural tapes, improving repairability and end-of-life recycling in automotive and construction applications. Additionally, Germany’s KfW energy-efficient building programs are fostering the adoption of non-mechanical fastening tapes in thermal insulation and cladding systems. Collaborative research between German universities and industrial labs is also accelerating the development of conductive and sensor-integrated structural tapes for vehicle electronics and EMI shielding. Germany thus remains a global leader in EU-compliant lightweight bonding, structural glazing tapes, and recyclable adhesive innovations.

United States – Aerospace, EV Infrastructure, and Defense Modernization Fuel Market Growth

The United States structural adhesive tapes market is being redefined by large-scale aerospace, defense, and EV battery manufacturing investments. Federal initiatives such as the Inflation Reduction Act (IRA) and the Bipartisan Infrastructure Law are strengthening domestic supply chains for advanced materials, particularly thermal management and electrically insulating structural tapes used in EV battery module production. In aerospace, major OEMs and Tier-1 suppliers are qualifying epoxy-based structural tapes for composite bonding, enhancing fatigue resistance and weight reduction in next-generation aircraft.

U.S.-based adhesive manufacturers are introducing low-VOC, solvent-free structural acrylic tapes to comply with stricter EPA and OSHA air quality standards, expanding their use in interior construction and public infrastructure. The defense sector continues to integrate impact-resistant structural tapes in armor assemblies and vehicle panels through DoD-funded innovation programs. Industrial manufacturers are also substituting rivets with VHB-style permanent bonding tapes to improve efficiency and aesthetics in heavy equipment production. The integration of fire-rated and high-strength epoxy structural tapes into commercial building codes highlights the U.S. leadership in sustainable, performance-driven adhesive technologies.

Japan – Advanced Materials R&D and Miniaturization Propel Precision Structural Tape Applications

Japan’s structural adhesive tape market continues to lead in precision electronics, advanced materials, and sustainable innovation. Companies like Nitto Denko Corporation and Toray Industries are spearheading developments in ultra-thin structural transfer tapes and double-sided foam bonding solutions designed for micro-assembly, flexible displays, and next-generation sensors. Patent filings across Japan highlight advancements in high-shear, heat-resistant, and pressure-sensitive structural tapes, optimized for miniaturized devices and 5G communication equipment.

Beyond electronics, Japan’s aging infrastructure is driving the adoption of structural repair tapes for seismic reinforcement and retrofitting of bridges and buildings, enhancing long-term durability. In the medical field, manufacturers are producing biocompatible silicone-based structural tapes for wearable medical devices and diagnostic patches, reflecting diversification into healthcare applications. Government-backed initiatives promote bio-based and renewable adhesive formulations, aligning with Japan’s long-term sustainability objectives. The advancements position Japan as a pioneer in precision-engineered, heat-activated, and bio-based structural adhesive systems.

India – Manufacturing Incentives and Infrastructure Expansion Accelerate Adhesive Tape Adoption

India’s structural adhesive tapes industry is rapidly expanding in line with automotive electrification and infrastructure modernization. The Production Linked Incentive (PLI) Scheme for the automotive sector has catalyzed domestic production of EV components and lightweight bonding materials, boosting demand for high-tack structural tapes in vehicle assembly. Large-scale projects such as metro, highway, and high-speed rail construction are creating new opportunities for sealing and weather-resistant structural bonding tapes for long-term durability in tropical conditions.

The rise in foreign direct investment (FDI) in automotive and electronics manufacturing has led to localized tape conversion and adhesive application facilities, strengthening India’s supply chain resilience. Additionally, HVAC and appliance manufacturers are increasingly switching from mechanical fasteners to structural tapes to cut production costs and improve efficiency. The government’s safety-focused mandates for flame-retardant materials in public transport are fostering demand for fire-resistant and high-humidity adhesion solutions.

Structural Adhesive Tapes Market Report Scope

Structural Adhesive Tapes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$19.7 Billion

|

|

Market Size (2034)

|

$30 Billion

|

|

Market Growth Rate

|

4.8%

|

|

Segments

|

By Adhesive Technology (Pressure-Sensitive, Heat-Activated, Water-Based, Solvent-Based, Hot Melt, UV-Curable), By Resin Type (Acrylic, Epoxy, Rubber, Silicone, Polyurethane, Methyl Methacrylate), By Backing Material (Structural Foam, Film, Non-Woven, Cloth/Fabric, Paper/Tissue, Metal Foil), By Product Thickness (Thin Gauge, Medium Gauge, Thick Gauge), By End-Use Industry (Automotive & Transportation, Aerospace & Defense, Building & Construction, Electrical & Electronics, Renewable Energy, Healthcare, Consumer Goods & Appliances

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, tesa SE, Nitto Denko Corporation, Avery Dennison Corporation, Lohmann GmbH & Co. KG, Lintec Corporation, Saint-Gobain Tape Solutions, Henkel AG & Co. KGaA, Berry Global Group, Inc., Shurtape Technologies, LLC, Intertape Polymer Group (IPG), Scapa Group plc, DuPont, H.B. Fuller Company, Adchem Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Adhesive Technology

- Pressure-Sensitive

- Heat-Activated

- Water-Based

- Solvent-Based

- Hot Melt

- UV-Curable

By Resin Type

- Acrylic

- Epoxy

- Rubber

- Silicone

- Polyurethane

- Methyl Methacrylate

By Backing Material / Carrier Type

- Structural Foam

- Film

- Non-Woven

- Cloth/Fabric

- Paper/Tissue

- Metal Foil

By Product Thickness

- Thin Gauge

- Medium Gauge

- Thick Gauge

By End-Use Industry

- Automotive & Transportation

- Aerospace & Defense

- Building & Construction

- Electrical & Electronics

- Renewable Energy

- Healthcare

- Consumer Goods & Appliances

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Structural Adhesive Tapes Market

- 3M Company

- tesa SE

- Nitto Denko Corporation

- Avery Dennison Corporation

- Lohmann GmbH & Co. KG

- Lintec Corporation

- Saint-Gobain Tape Solutions

- Henkel AG & Co. KGaA

- Berry Global Group, Inc.

- Shurtape Technologies, LLC

- Intertape Polymer Group (IPG)

- Scapa Group plc

- DuPont

- H.B. Fuller Company

- Adchem Corporation

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates how structural adhesive tapes are redefining high-strength, fast-curing, and lightweight bonding across automotive, aerospace, electronics, and construction, translating materials-science breakthroughs in acrylic, epoxy, and polyurethane platforms into scalable, production-ready solutions; our analysis reviews specification trends, qualification data, durability/performance envelopes (shear, peel, temperature, fatigue, NVH), and supply innovations including solvent-free chemistries and hydrogen-enabled manufacturing, and highlights the implications for cost, weight, throughput, and circularity as OEMs replace mechanical fasteners with viscoelastic, high-bond tapes—positioning sourcing teams and engineers to benchmark alternatives, de-risk transitions, and capture total-cost benefits; crafted for decision makers and technical stakeholders, this report is an essential resource for portfolio planning, line-rate optimization, compliance road-mapping, and competitive strategy, etc……

Scope Highlights

Segmentation:

- By Adhesive Technology: Pressure-Sensitive; Heat-Activated; Water-Based; Solvent-Based; Hot Melt; UV-Curable

- By Resin Type: Acrylic; Epoxy; Rubber; Silicone; Polyurethane; Methyl Methacrylate

- By Backing Material / Carrier Type: Structural Foam; Film; Non-Woven; Cloth/Fabric; Paper/Tissue; Metal Foil

- By Product Thickness: Thin Gauge; Medium Gauge; Thick Gauge

- By End-Use Industry: Automotive & Transportation; Aerospace & Defense; Building & Construction; Electrical & Electronics; Renewable Energy; Healthcare; Consumer Goods & Appliances

- By Region: North America; Europe; Asia Pacific; South & Central America; Middle East & Africa

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast data 2025–2034.

Companies Covered: Analysis/profiles of 15+ companies — 3M Company; tesa SE; Nitto Denko Corporation; Avery Dennison Corporation; Lohmann GmbH & Co. KG; Lintec Corporation; Saint-Gobain Tape Solutions; Henkel AG & Co. KGaA; Berry Global Group, Inc.; Shurtape Technologies, LLC; Intertape Polymer Group (IPG); Scapa Group plc; DuPont; H.B. Fuller Company; Adchem Corporation.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.