Market Overview: Growth Driven by Food Packaging and rPET Adoption

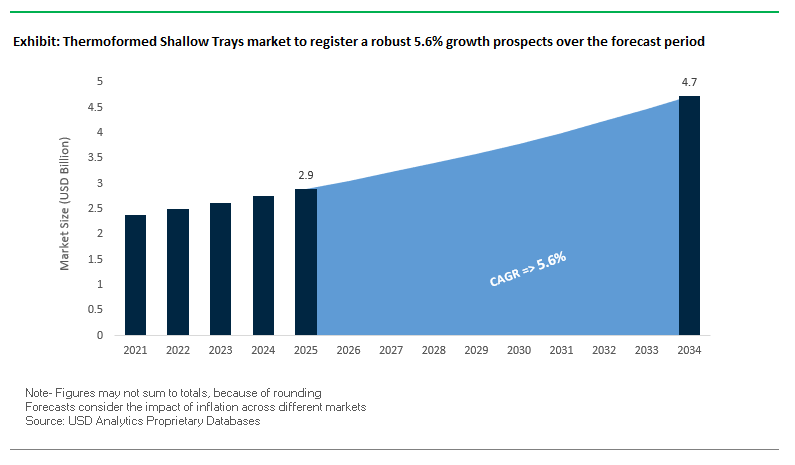

The global thermoformed shallow trays market is projected to grow from USD 2.9 billion in 2025 to USD 4.7 billion by 2034, registering a robust CAGR of 5.6%. This growth trajectory is underpinned by surging demand from the food industry, medical packaging, and personal care sectors. For buyers and industry professionals, the critical consideration lies in how thermoformed shallow trays can simultaneously deliver convenience, cost efficiency, and sustainability while complying with increasingly strict regulations on food safety and recycling.

Food packaging accounts for over 40% of global demand, with shallow trays widely used for fresh produce, meat, and ready-to-eat meals. A significant trend is the rise of recycled PET (rPET) as a preferred material, as it meets stringent food safety requirements while enabling circular economy solutions. North America leads the market due to its well-developed food processing, retail, and logistics infrastructure. Meanwhile, automation in thermoforming production lines featuring robotic feeding systems and servo-driven movements continues to enhance manufacturing efficiency and cost savings.

Key Insights for Industry Professionals:

- Food packaging leadership: Over 40% share, driven by fresh produce and ready-meal demand.

- Sustainability push: rPET adoption accelerating, meeting recycling mandates.

- North America dominance: Largest market with strong food processing and retail sectors.

- Automation integration: Robotics and servo-driven thermoforming systems reducing costs.

Market Analysis: Recent Industry Developments Driving Expansion

The thermoformed shallow trays market is experiencing mergers, acquisitions, and facility expansions that are reshaping its global footprint.

In July 2025, Sonoco launched a new thermoformed tray for the frozen food industry, engineered for stackability and reduced material use, reinforcing its leadership in innovation. The following month, in June 2025, a major European food retailer committed to sourcing 100% of its trays from closed-loop recycling systems by 2028, signaling strong demand for circular packaging models.

Consolidation trends are also shaping the sector. Amcor’s USD 8.4 billion acquisition of Berry Global (finalized in May 2025) significantly expanded its rigid and flexible thermoforming capacity. Earlier in January 2025, Sonoco acquired Thermoform Engineered Quality (TEQ), boosting its footprint in medical and electronics packaging. Smaller players are also scaling up: Lacerta Group acquired a New Jersey thermoforming facility in April 2025, while Placon added a new production line in Madison, Wisconsin (October 2024) to meet demand for sustainable food-grade trays.

Innovation is also driving new applications. Constantia Flexibles partnered with a global pharmaceutical company in September 2024 to develop recycled PET blister packs, highlighting how thermoforming is diversifying into pharma beyond food.

Emerging Trends and Opportunities Shaping the Thermoformed Shallow Trays Market

Accelerated Adoption of Post-Consumer Recycled (PCR) Content Driven by Brand Commitments

The thermoformed shallow trays market is experiencing a decisive shift as major consumer packaged goods (CPG) companies and retailers impose stringent sustainability requirements on their suppliers. This has pushed PCR integration from a niche innovation into a core procurement standard across multiple food, personal care, and retail packaging categories. Brands such as PepsiCo, which has committed to achieving 40% or greater recycled content in its plastic packaging by 2035, and Henkel, aiming for 100% recyclability and a 50% reduction in virgin plastic use by 2025, are setting ambitious sustainability benchmarks. These commitments cascade down to packaging converters, creating intense pressure to deliver trays with high PCR inclusion.

To address growing demand, investments in recycling infrastructure are accelerating. For example, Hindustan Unilever Limited (HUL) has acquired a 14.3% stake in Lucro Plastecycle, strengthening its ability to secure recycled content for packaging applications. Similarly, investment firms such as Circulate Capital are co-developing PCR polyethylene film solutions with material suppliers like Dow, demonstrating the collaborative approach required to close the loop in circular packaging systems. This multi-stakeholder alignment is transforming PCR adoption into a global industry standard, ensuring thermoformed shallow trays align with regulatory compliance, corporate ESG goals, and consumer expectations.

Material Diversification and Monomaterial Development to Enhance Recyclability

Another defining trend is the transition away from multi-material trays that complicate recycling processes. With regulatory frameworks such as the EU Packaging and Packaging Waste Regulation (PPWR) mandating that all packaging be recyclable in an economically viable manner by 2030, manufacturers are investing heavily in monomaterial tray development.

Companies like Mondi have introduced recyclable Monoformable barrier films, designed from a single polymer such as polypropylene (PP) or polyethylene (PE), eliminating the challenges posed by traditional mixed-material trays. Sukano’s innovation in clear CPET-light packaging demonstrates how PET can now replace PP in hot-fill applications, creating a tray that maintains recyclability while withstanding temperatures of up to 100°C. Beyond plastics, fiber-based solutions are gaining traction. Walki’s fiber-based trays with thin PET linings, recyclable in paper streams, highlight the growing role of hybrid fiber packaging in enhancing end-of-life outcomes. Collectively, these advances mark a critical industry pivot toward high-performance recyclability, ensuring thermoformed trays remain competitive under tightening sustainability regulations.

Penetration of the E-Commerce Ready Meal Delivery Sector

The meteoric growth of meal kit services and prepared food delivery platforms has created a lucrative expansion avenue for thermoformed shallow trays. These trays meet the critical technical requirements of durability, freshness preservation, and lightweight shipping, making them indispensable to the fast-growing e-commerce food sector.

Thermoformed trays are well-suited for Modified Atmosphere Packaging (MAP) and Vacuum Skin Packaging (VSP), both of which extend shelf life by regulating oxygen and gas levels within the package. This ensures meats, produce, and prepared meals remain fresh during long supply chains and last-mile delivery. Their inherent rigidity also provides superior crush resistance compared to flexible packaging, reducing food waste from damage during shipping. For meal kit brands, tray design plays a central role in consumer experience and convenience multi-cavity trays allow separation of ingredients, while transparent lids enhance product appeal by offering a clear view of the contents. With e-commerce food sales expected to continue their upward trajectory, thermoformed trays are strategically positioned as the backbone packaging format for meal delivery logistics.

Integration of Smart Packaging and Anti-Counterfeiting Features

Beyond traditional food applications, thermoformed shallow trays are emerging as platforms for smart packaging integration, particularly in pharmaceuticals, premium foods, and high-value consumer electronics. Regulatory mandates such as the U.S. DSCSA (Drug Supply Chain Security Act) and the EU Falsified Medicines Directive are making serialized identifiers QR codes, RFID tags, and covert markers a legal requirement to combat counterfeiting.

This creates a twofold opportunity. First, it enhances product authentication, empowering consumers to verify product legitimacy in real time with a smartphone scan. Second, it opens avenues for interactive consumer engagement for instance, scanning a QR code could direct customers to ingredient transparency portals, cooking tutorials, or promotional campaigns. Additionally, embedding IoT-enabled sensors into trays unlocks supply chain visibility, allowing manufacturers and retailers to track conditions such as temperature and humidity for sensitive goods. For high-value pharmaceuticals and premium food brands, this integration not only ensures compliance but also elevates consumer trust and brand loyalty, transforming thermoformed trays from static containers into dynamic, data-driven platforms.

Competitive Landscape: Leading Companies in the Thermoformed Shallow Trays Market

The thermoformed shallow trays industry is highly competitive, with players differentiating through sustainable materials, geographic expansions, and integration of advanced automation. The market is witnessing consolidation as large multinationals strengthen their portfolios while regional manufacturers innovate in rPET-based solutions.

Amcor plc: Strengthening Thermoforming Capabilities Through Acquisition

Amcor offers an extensive portfolio of thermoformed trays for food, healthcare, and personal care markets. Its April 2025 acquisition of Berry Global for USD 8.4 billion expanded its rigid plastics portfolio. Amcor’s focus on 100% recyclable or compostable packaging by 2025 aligns with global sustainability mandates. Its HealthCare OrthoSecure line for medical devices showcases innovation in high-value segments.

Sonoco Products Company: Expanding in Food and Healthcare Packaging

Sonoco is a major supplier of thermoformed trays for food and consumer products. Its July 2025 launch of frozen food trays demonstrated product optimization for stacking and protection. The TEQ acquisition in January 2025 strengthened its medical and electronics packaging capabilities. Sonoco is also integrating thermoforming and flexible packaging into a single operational platform, enhancing efficiency and innovation.

Pactiv LLC: Leveraging Scale in Food Packaging Solutions

Pactiv is a dominant force in supermarket and food service packaging, with a large share of trays used for meat, poultry, bakery, and produce. Its strength lies in oxygen-barrier thermoformed trays that extend food shelf life. Pactiv’s scale enables customized tray solutions while advancing the use of recycled materials, reinforcing its commitment to sustainability.

Berry Global Inc.: Innovating With Recycled Content in Thermoformed Trays

Prior to its acquisition by Amcor, Berry Global was a global leader in rigid packaging, including thermoformed trays. It focused heavily on circularity, introducing products with high post-consumer recycled content. The integration into Amcor creates a comprehensive global portfolio, enhancing both rigid and flexible packaging solutions for multinational clients.

Placon Corporation: Pioneering Closed-Loop PET Recycling Systems

Placon specializes in sustainable, food-grade thermoformed trays made from rPET. Its October 2024 production line expansion in Wisconsin demonstrates its capacity to meet rising demand. With an in-house PETE recycling process that transforms discarded bottles into new trays, Placon exemplifies a closed-loop production model. Its product range spans bakery, deli, and fresh produce applications.

Thermoformed Shallow Trays Market Share Insights

Food & Beverages Dominate Thermoformed Shallow Trays Market Share by Application

Food and beverages account for 65% of the thermoformed shallow trays market in 2025, making it the largest and most influential application segment. The dominance of this category is anchored in its universal use across supermarkets, bakeries, butchers, and ready-meal producers, where trays provide rigidity, leakage control, and visibility for perishable goods. The format has become indispensable in the pre-packaged fresh food supply chain, from meat and poultry to seafood, baked goods, and grab-and-go meals. Beyond basic functionality, thermoformed trays deliver high-impact branding through printable surfaces and comply with stringent food labeling mandates. Rising consumer demand for convenience and hygiene, coupled with the explosive growth of retail-ready packaging, continues to reinforce this leadership. Other segments such as pharmaceuticals & medical, electronics, and cosmetics leverage trays for precision, compliance, and aesthetic presentation, but their combined share remains significantly smaller compared to the overwhelming dominance of food packaging.

Food & Beverage Industry Leads Thermoformed Shallow Trays Market Share by End-Use

The food and beverage industry captures 60% of the thermoformed shallow trays market by end-use in 2025, cementing its position as the largest consumer segment. The sector’s demand is driven by the continuous expansion of supermarkets, quick-service restaurants, and online grocery delivery, all of which require reliable and cost-effective packaging solutions. Trays made from rPET, rPP, and other recycled content are seeing rapid adoption as global sustainability regulations tighten, creating opportunities for mono-material tray innovations that simplify recyclability. Healthcare, electronics, and consumer goods collectively represent high-value niches, but their scale is overshadowed by food’s consistent, high-volume consumption. In healthcare, trays are engineered for sterility and seamless automation compatibility, while in electronics, they are tailored for static protection and precision handling. However, the sheer indispensability of thermoformed shallow trays in food supply chains ensures the food & beverage industry remains the anchor of overall market share.

United States: EPR Laws, Food Industry Demand, and Material Innovation Accelerate Thermoformed Shallow Trays Growth

The U.S. thermoformed shallow trays market is expanding quickly, largely shaped by state-level Extended Producer Responsibility (EPR) regulations such as California’s SB-54, which mandate sustainability and recyclability in packaging. These policies are creating strong incentives for manufacturers to invest in eco-friendly, recyclable, and reusable tray designs, reducing reliance on virgin plastics while ensuring compliance with future legislation.

The food and beverage sector is the biggest growth catalyst, as the rising demand for ready-to-eat meals, fresh produce, and packaged snacks requires durable, lightweight, and hygienic packaging solutions. A key development is the industry’s push toward post-consumer recycled (PCR) plastics, especially PET-based shallow trays, which help reduce environmental footprints and meet corporate sustainability goals. At the same time, technological integration in thermoforming machinery is driving efficiencies by minimizing material waste and enabling highly customized, precision-molded trays for niche product applications, positioning the U.S. as a hub of innovation in sustainable packaging.

Germany: Circular Economy Leadership and EU PPWR Compliance Redefine Thermoformed Shallow Trays Market

The German thermoformed shallow trays market is driven by the country’s strict regulatory framework, particularly the EU Packaging and Packaging Waste Regulation (PPWR) that came into effect in February 2025. These rules mandate reductions in excessive packaging, enforce recyclability standards, and require increased use of recycled content, compelling manufacturers to innovate. Germany’s role as a leader in the circular economy has spurred collaboration between producers and end-users to develop trays that are lightweight, recyclable, and environmentally efficient.

Eco-design is a defining trend, with companies focusing on material reduction, flat-pack formats for transport efficiency, and water-based or soy-based inks to minimize environmental impact. Governmental mandates embedded within PPWR are also accelerating the industry’s transition toward high-recycled-content trays that address both consumer demand and EU-level sustainability targets. As a result, Germany has become a benchmark market for sustainable thermoformed tray innovation in Europe.

China: Industrial Expansion, Sustainability Push, and Food Demand Propel Thermoformed Shallow Trays Market

China’s thermoformed shallow trays market benefits from the country’s vast manufacturing and industrial capacity, coupled with its booming e-commerce and logistics industries. The need for secure and efficient packaging to protect goods during complex shipping and handling processes is a primary driver. Simultaneously, the food and beverage sector especially fresh produce and ready-to-eat foods has become a key application area for thermoformed trays, further boosting demand.

China’s market direction is also strongly influenced by the government’s “dual carbon” goal, which pushes for carbon peak and carbon neutrality. As part of this effort, authorities are mandating eco-friendly, reduced, and reusable packaging solutions, compelling tray manufacturers to replace traditional plastics with recyclable and bio-based alternatives. Combined with rising consumer environmental awareness, these sustainability policies are reshaping China into a high-volume but increasingly green packaging market.

India: Sustainability Regulations and Food Processing Expansion Drive Thermoformed Shallow Trays Market

The Indian thermoformed shallow trays market is growing rapidly, underpinned by regulatory and industrial developments. The Plastic Waste Management (Amendment) Rules banning several categories of single-use plastics, including trays, have created strong momentum for biodegradable, recyclable, and paper-based packaging alternatives. This regulatory push aligns with rising consumer and corporate interest in sustainable packaging solutions.

At the same time, the food processing sector’s rapid expansion particularly in bakery, meat, and ready-to-eat meals is a primary growth driver, as demand increases for lightweight, hygienic, and durable shallow trays. Government initiatives such as the Integrated Cold Chain and Value Addition Infrastructure scheme are also driving adoption by supporting cold chain logistics and perishable food transport. These trends are positioning India as an emerging growth hub for sustainable thermoformed shallow trays, with strong domestic demand and government support fueling long-term opportunities.

Thermoformed Shallow Trays Market Report Scope

Thermoformed Shallow Trays market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.9 Billion

|

|

Market Size (2034)

|

$4.7 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Material Type (PET, PP, PVC, HIPS, Other Materials), By Application (Food & Beverages, Pharmaceuticals & Medical, Cosmetics & Personal Care, Electronics & Electricals, Other Applications), By End-Use Industry (Consumer Goods, Electronics, Healthcare, Food & Beverage, Industrial, Other End-use Industries)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sonoco Products Company, Amcor plc, Berry Global Inc., DS Smith Plc, Huhtamäki Oyj, Tekni-Plex, Inc., Novolex, Pactiv LLC, Sealed Air Corporation, D&W Fine Pack LLC, Placon Corporation, Lacerta Group, Inc., Sonoco Protective Solutions, Alpack, Inc., E3 Sustainable Solutions

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Thermoformed Shallow Trays Market Segmentation

By Material Type

- PET

- PP

- PVC

- HIPS

- Other Materials

By Application

- Food & Beverages

- Pharmaceuticals & Medical

- Cosmetics & Personal Care

- Electronics & Electricals

- Other Applications

By End-Use Industry

- Consumer Goods

- Electronics

- Healthcare

- Food & Beverage

- Industrial

- Other End-use Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Thermoformed Shallow Trays Market

- Sonoco Products Company

- Amcor plc

- Berry Global Inc.

- DS Smith Plc

- Huhtamäki Oyj

- Tekni-Plex, Inc.

- Novolex

- Pactiv LLC

- Sealed Air Corporation

- D&W Fine Pack LLC

- Placon Corporation

- Lacerta Group, Inc.

- Sonoco Protective Solutions

- Alpack, Inc.

- E3 Sustainable Solutions

*List not Exhaustive

Research Coverage

This comprehensive report by USDAnalytics investigates the global thermoformed shallow trays market, highlighting breakthroughs in sustainable materials, rPET adoption, automation, and multi-sector application expansion. The analysis reviews key trends driving growth across food packaging, pharmaceuticals, and personal care sectors while emphasizing innovations in monomaterial tray development, post-consumer recycled (PCR) content integration, and smart packaging solutions for e-commerce and premium products. The report highlights strategic M&A, capacity expansions, and technological advancements, offering insights into supply chain optimization, regulatory compliance, and circular economy initiatives. This report is an essential resource for manufacturers, brand owners, and packaging professionals seeking to navigate evolving consumer demands, sustainability mandates, and operational efficiencies. By combining historic performance data from 2021 to 2024 with forecasts through 2034, USDAnalytics equips stakeholders with actionable intelligence to drive product innovation, expand market presence, and leverage advanced manufacturing capabilities in a competitive global landscape.

Scope Highlights:

- Segmentation: By Material Type (PET, PP, PVC, HIPS, Other Materials); By Application (Food & Beverages, Pharmaceuticals & Medical, Cosmetics & Personal Care, Electronics & Electricals, Other Applications); By End-Use Industry (Consumer Goods, Electronics, Healthcare, Food & Beverage, Industrial, Other End-use Industries)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic data from 2021 to 2024; forecast data from 2025 to 2034.

- Companies Covered: Analysis/profiles of 15+ companies including Sonoco Products Company, Amcor plc, Berry Global Inc., DS Smith Plc, Huhtamäki Oyj, Tekni-Plex, Inc., Novolex, Pactiv LLC, Sealed Air Corporation, D&W Fine Pack LLC, Placon Corporation, Lacerta Group, Inc., Sonoco Protective Solutions, Alpack, Inc., E3 Sustainable Solutions.

Methodology

The research methodology for this report combines extensive primary and secondary research to ensure a robust and reliable market analysis of thermoformed shallow trays. Primary insights were obtained from interviews with executives, R&D leaders, and supply chain managers across leading manufacturers and end-user industries. Secondary research included company reports, trade publications, regulatory documentation, and sustainability disclosures. Market sizing and forecast calculations employed a top-down approach, integrating historical consumption trends, production capacities, and regional demand patterns across materials, applications, and end-use industries. Competitive benchmarking evaluated mergers, acquisitions, capacity expansions, and technological innovation. Key trends, including PCR content adoption, monomaterial development, smart packaging integration, and automation, were assessed using scenario analysis and market modeling. This methodology ensures actionable intelligence for stakeholders seeking to optimize operations, adopt sustainable practices, and align with regulatory and ESG requirements.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.