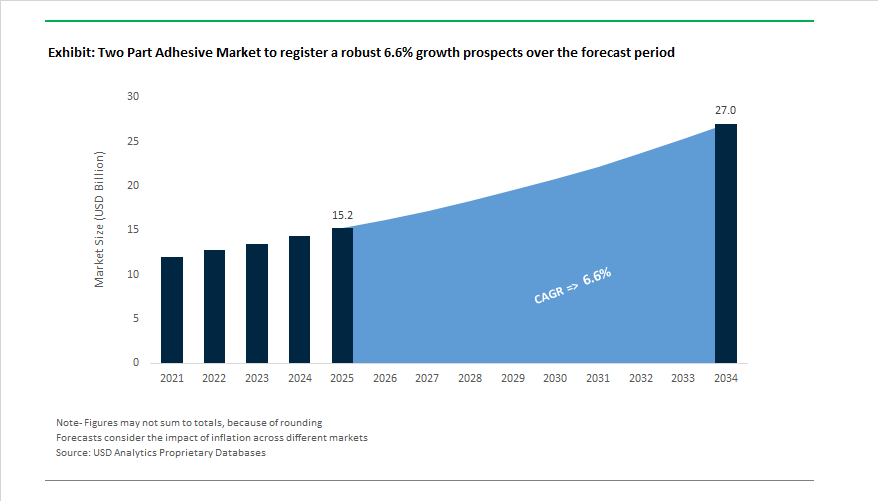

The Global Two-Part Adhesive Market is projected to expand from USD 15.2 billion in 2025 to USD 27 billion by 2034, advancing at a CAGR of 6.6%, as manufacturers increasingly redesign products and production lines around structural bonding rather than mechanical joining. Growth is being driven not by commoditized volume applications, but by the rising reliance on engineered, cure-controlled adhesive systems that deliver predictable strength, extended open time, and process flexibility across complex assemblies.

Two-part epoxies, acrylics, and polyurethanes are becoming load-bearing enablers in automotive platforms, rail cars, wind blades, construction modules, and industrial equipment—applications where joint performance must be tuned independently of ambient humidity or substrate variability. Unlike one-component systems, two-part adhesives allow manufacturers to decouple working time, cure speed, and final mechanical properties, a capability that is increasingly valued as takt times shorten and product geometries become more complex.

Automotive and transportation remain the largest value pools, but the demand signal is structural rather than cyclical. OEMs and Tier-1 suppliers are specifying long-open-time epoxies and fast-fixture acrylics to enable mixed-material bonding between aluminum, high-strength steel, SMC, CFRP, and thermoplastics—often within the same assembly station. Suppliers such as Henkel (Loctite structural epoxies), Sika, 3M, Arkema (Bostik), and Huntsman have expanded portfolios with formulations offering open times exceeding 60 minutes, fixture times under 10 minutes, and lap shear strengths exceeding 20–30 MPa, enabling both manual and robotic dispensing strategies.

A notable shift is occurring toward low-temperature and low-exotherm curing systems, particularly in Asia-Pacific manufacturing hubs where thin substrates, electronics integration, and energy efficiency are critical constraints. Two-part polyurethanes and modified epoxies that cure effectively below 10–15°C are gaining traction in EV battery housings, rail interiors, and modular construction, reducing the need for energy-intensive heat curing. At the same time, controlled exotherm profiles are becoming a key specification in thick bond lines and encapsulation applications, protecting heat-sensitive components and coatings.

From a production standpoint, two-part adhesives are increasingly selected for their process robustness. Meter-mix-dispense (MMD) systems—often co-developed with equipment suppliers—allow precise ratio control, inline monitoring, and rapid formulation switching. This is particularly relevant in renewable energy and industrial equipment manufacturing, where bond dimensions, cure schedules, and service loads vary significantly across SKUs. Adhesive suppliers are responding by offering application-specific systems, not just chemistries, integrating rheology control, gap-filling behavior, and surface tolerance into validated bonding packages.

The global market is witnessing rapid portfolio expansion, regional capacity builds, and specialty electronics innovations. Sika accelerated a build-and-buy strategy: it acquired Kwik Bond Polymers (March 2024) for concrete refurbishment systems, opened a new fiber facility in Lima (April 2024), completed Chema in Peru (September 2024), more than doubled capacity at Bekasi, Indonesia (August 2024), and opened a Liaoning, China plant (January 2024)—collectively boosting APAC and LATAM reach for two-component systems across infrastructure and construction.

Henkel strengthened its specialty electronics position: two innovations earned high honors (April 2024), while the Bergquist® Hi Flow THF 5000UT TIM film gained distinctions from mid-2023, underscoring thin-bond-line excellence for high-performance computing. In April 2024, Henkel also highlighted conformal coatings (e.g., Loctite® Stycast CC 8555, VOC-free, UL-rated)—relevant where two-part encapsulants/coatings converge with structural adhesive ecosystems in EVs and servers.

Strategic portfolio plays continued at Arkema (Bostik), which finalized the acquisition of Dow’s flexible packaging laminating adhesives business (December 2024) to deepen adhesive solutions scope and synergies. Throughout 2024, Huntsman ran polyurethane technology forums focused on battery electric vehicles, aligning two-component chemistries with thermal management and lightweighting priorities.

Market Trend 1: Proliferation of Rapid-Cure, High-Strength Epoxies for Electric Vehicle Battery Assembly and Repair

The surge in EV manufacturing and repair applications is driving significant demand for two-part epoxy systems that combine rapid fixture, structural strength, and thermal conductivity for high-performance battery assembly. Manufacturers are prioritizing adhesive solutions that enhance production throughput, crash resistance, and power module durability, meeting both efficiency and safety standards required by global automakers.

A recent DuPont case study highlighted how its custom-engineered two-component structural epoxy for a luxury EV battery housing achieved crash-durable strength and torsional stiffness, allowing full fixture within minutes. The rapid-cure technology ensures high bond strength while cutting assembly times to align with automated EV production cycles, directly addressing the need for speed and precision in next-generation manufacturing environments.

Equally critical is the role of thermal management. Modern two-part thermal adhesives, particularly epoxy and polyurethane hybrids, deliver thermal conductivity (TC) between 1 and 5 W/m·K, compared to 0.3 W/m·K in standard systems. The improvement allows for efficient heat dissipation across high-power lithium-ion cells, mitigating the risk of thermal runaway and improving battery lifespan and performance. These adhesives are crucial in power-dense EV modules, where mechanical bonding and thermal transfer properties must coexist without compromising electrical insulation.

Market Trend 2: Adoption of Non-Isocyanate, Bio-Based Two-Part Systems for Sustainable Manufacturing

Sustainability and regulatory compliance are reshaping adhesive innovation, prompting a major shift toward bio-based and non-isocyanate two-part adhesives. The goal is to deliver VOC-free, recyclable systems with mechanical performance parity to petrochemical alternatives.

Academic breakthroughs have introduced acid-cleavable amine-modified epoxies, achieving a biocarbon content exceeding 28% and exhibiting controlled chemical recyclability—a major milestone in circular chemistry. These sustainable two-part systems allow end-of-life disassembly without hazardous byproducts, aligning perfectly with global circular economy mandates.

Complementing these innovations are Non-Isocyanate Polyurethane (NIPU) adhesives, formulated using renewable lignin and soy-based polyols. Life Cycle Assessments (LCA) demonstrate these systems deliver up to 35% improved environmental performance scores while maintaining comparable tensile strength and durability to conventional structural adhesives. The positions bio-based two-part adhesives as ideal solutions for applications in engineered wood panels, automotive interiors, and green electronics, where low-VOC and sustainability certifications are key purchasing criteria.

Market Opportunity 1: Development of Debondable/Reversible Two-Part Adhesives for Electronics Repair and Recycling

The rising global momentum behind right-to-repair and e-waste reduction initiatives is opening a lucrative niche for stimuli-responsive, debondable two-part adhesives. These systems promise high-strength permanent adhesion during use but can reversibly debond when activated through heat, electricity, or specific chemical triggers, enabling non-destructive disassembly and recycling of valuable components.

A landmark example comes from Apple’s integration of electrically-released adhesive tapes in smartphones to facilitate battery replacement, signaling a broader shift toward adhesives designed for controlled release. Translating the principle to two-part liquid adhesives unlocks immense potential for modular electronics assembly, where components such as screens, PCBs, and batteries must be replaced or recycled efficiently.

Research on stimuli-responsive polymer networks confirms that such reversible adhesives can enhance metal recovery rates in complex assemblies like lithium-ion battery packs, which typically rely on permanent epoxies that complicate recycling. These debonding-on-demand (DoD) systems allow the recovery of technology-critical metals without resorting to energy-intensive pyrolysis, lowering environmental impact while preserving material value.

Market Opportunity 2: Engineering of Thermally Conductive, Electrically Insulative Epoxies for Power Electronics

The growth of wide-bandgap (WBG) semiconductors such as Silicon Carbide (SiC) and Gallium Nitride (GaN) in power electronics, EV inverters, and 5G modules is creating high-value opportunities for thermally conductive yet electrically insulative two-part epoxies. These adhesives play a dual role: ensuring mechanical bonding and dissipating heat efficiently from compact, high-power devices.

Research demonstrates that hybrid epoxy composites incorporating Aluminum Nitride (AlN) and Boron Nitride (BN) fillers at 75 wt% loading can achieve thermal conductivities up to 10.18 W/m·K—a remarkable 46× improvement over standard epoxy matrices (0.22 W/m·K). The advancement meets the stringent heat dissipation requirements of next-generation SiC and GaN power modules, ensuring operational stability at extreme temperatures and high switching frequencies.

Further studies indicate that incorporating functionalized filler systems into epoxy matrices can boost impact strength by 300% and bending stress tolerance by 194%, significantly improving adhesive reliability under thermal cycling and mechanical shock. These performance gains make advanced two-part thermally conductive adhesives indispensable for power-dense electronics, EV control units, and high-frequency 5G infrastructure, where both heat management and insulation integrity are critical.

Two Part Adhesive Market Share Insights, 2025-2034

Market Share by Technology

The Reactive Adhesives segment, encompassing standard two-component epoxies, polyurethanes, and acrylic systems, commands the largest share of the global two-part adhesive industry with a projected 61.4% of the 2025 market. This dominance stems from the unmatched versatility and mechanical performance of these formulations, which are integral to structural and semi-structural bonding across diverse industries including automotive, construction, aerospace, and electronics. Reactive two-part adhesives are prized for their high shear and peel strength, excellent durability under thermal and chemical stress, and adaptability to dissimilar substrates such as metals, composites, and plastics. Their proven track record in applications requiring long-term stability, resistance to fatigue, and environmental exposure makes them the foundation of the global structural adhesives market. Furthermore, advancements in mixing technologies, automation compatibility, and fast-curing chemistries have enhanced their use in high-throughput assembly operations, reinforcing their market leadership.

Meanwhile, Reactive Hot-Melt Adhesives (RHMAs) and UV/Light-Cured Dual-Cure Systems represent the fastest-growing subsegments, fueled by manufacturing trends emphasizing speed, precision, and energy efficiency. RHMAs—particularly reactive polyurethane-based systems—combine the instant tack and handling strength of thermoplastics with the final cross-linked strength of thermosets, positioning them as a preferred solution in furniture, packaging, and automotive assembly. Similarly, UV/Light-Cured systems are gaining traction in electronics, optics, and medical device assembly, where controlled, on-demand curing delivers precision and minimal heat distortion. Their adoption reflects the market’s gradual shift toward high-performance, clean-processing adhesive technologies compatible with automated production lines. Conversely, Water-Based two-part adhesives occupy a smaller but vital niche, primarily in eco-sensitive applications where low-VOC, non-flammable, and sustainable bonding solutions are prioritized—particularly in construction, flooring, and packaging sectors.

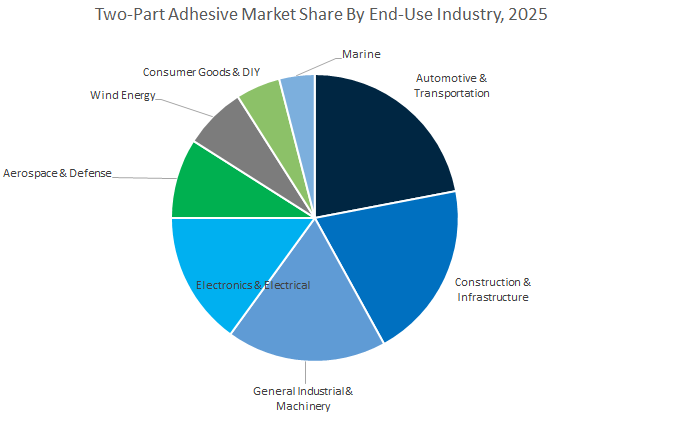

Market Share by End-Use Industry

The Automotive & Transportation sector leads the global two-part adhesive market, accounting for a projected 22.9% of 2025 market share, followed closely by the Construction & Infrastructure sector. In automotive manufacturing, the shift toward lightweight vehicle designs, electric mobility, and advanced material integration has exponentially increased the reliance on structural adhesives to replace traditional mechanical fasteners. Two-part systems—particularly epoxy and polyurethane formulations—are widely employed in bonding structural panels, composite parts, and EV battery components, offering superior strength and long-term resistance to dynamic stresses, vibration, and thermal cycling. The Construction & Infrastructure industry represents a parallel growth engine, with these adhesives used in concrete repair, facade bonding, flooring installation, and waterproofing applications. Their ability to bond diverse materials like concrete, glass, metal, and composites under variable environmental conditions makes them indispensable for sustainable building systems and large-scale infrastructure projects.

Beyond these high-volume markets, Electronics and Aerospace & Defense constitute premium, high-value application areas, characterized by stringent performance specifications and tight process control requirements. In electronics manufacturing, two-part adhesives play critical roles in potting, encapsulation, heat dissipation, and circuit assembly, especially for 5G devices, high-power components, and miniaturized systems. The Aerospace & Defense sector demands ultra-reliable bonding solutions that deliver exceptional fatigue resistance, low outgassing, and tolerance to extreme thermal and pressure variations, especially in composite structures, radomes, and aircraft interiors. Meanwhile, the Wind Energy sector continues to emerge as a fast-growing consumer, leveraging two-part epoxy systems in blade fabrication, nacelle bonding, and turbine assembly where large-scale, high-strength adhesive solutions are critical. General Industrial applications—encompassing machinery assembly, maintenance, and repair operations (MRO)—provide a stable backbone of consistent demand, ensuring market continuity.

Global leaders are winning on chemistry depth (epoxy, PUR, acrylic), process latitude (low-temp induction cure, long open-time), application coverage (auto, infrastructure, electronics), and global ops. Success hinges on cartridge/packaging precision (Duo-Pak), automated dispensing compatibility, and field technical support to assure repeatable bond quality at scale.

3M’s Scotch-Weld™ two-part epoxies, urethanes, and low-odor acrylics—delivered in Duo-Pak cartridges—enable accurate mix-ratio and bead control. 3M™ SA9820 targets carbon composite-to-aluminum bonding with broad cure windows and low-temperature options, supporting automotive lightweighting and NVH gains. Strategically, 3M advances fastener-replacement to improve stress distribution, aesthetics, and corrosion resistance, reducing total cost per assembly.

Henkel’s Loctite® range covers 2K epoxies, acrylics, and PURs for industrial assembly, MRO, and e-mobility. Its Loctite® Stycast CC 8555 (VOC-free, UL-rated) and award-winning TIM/conformal coating breakthroughs (April 2024) highlight electronics reliability alongside structural strength. Expansion focuses on high-growth e-mobility and HPC, leveraging global application labs to tune open time, viscosity, and cure profiles for automated lines.

Sika offers SikaForce® (2K PUR) and SikaPower® (2K epoxy) platforms, including SmartCore Technology for impact resistance rivaling 1K systems. It executed multiple expansions—Liaoning (Jan 2024), Bekasi capacity (Aug 2024)—and acquired Chema (Sep 2024) plus KBP (Mar 2024) to widen construction and infrastructure reach. Purform® ultra-low free-monomer PUR advances REACH compliance and applicator safety for high-volume plants.

Huntsman delivers 2K epoxy, PUR, and acrylic systems for aerospace/defense where weight savings up to 75% vs. fasteners matter, and for energy (wind, solar, oil & gas) where durability and chemical resistance are critical. Ongoing R&D with external partners targets anti-ballistic composites and thermal/damage performance. 2024 programming emphasized BEV adhesives, aligning 2K PUR with battery module protection and thermal pathways.

Arkema (Bostik) dedicates 24% of R&D to sustainable, efficient adhesive solutions, with robust 2K acrylic/epoxy offerings in electronics, renewables, and medical. The December 2024 acquisition of Dow’s flexible packaging laminating adhesives expands technology breadth and synergy capture (targeted EBITDA uplift over five years). The group leverages AI to accelerate formulation discovery and process optimization, compressing time-to-qualification for structural 2K products.

Country Analysis: Structural Bonding Development Hubs Transforming the Global Two-Part Adhesive Industry

United States – Advanced Structural Adhesive Innovation Driving Aerospace and EV Expansion

The United States continues to dominate the global Two-Part Adhesives market, driven by a surge in high-performance Epoxy, Acrylic, and Polyurethane formulations tailored for next-generation aerospace, automotive, and energy applications. In 2024, 3M Company introduced its latest line of High-Performance Acrylic Structural Adhesives engineered for multi-substrate bonding and optimized cycle time reduction in EV battery assembly—a critical development addressing scalability and efficiency in electric mobility manufacturing. Similarly, H.B. Fuller expanded its North American R&D and production capacity for specialized Two-Part Polyurethane Adhesives used in wind turbine blade bonding and repair, reinforcing the nation’s leadership in renewable infrastructure.

DuPont’s investment in lightweight structural solutions further underscores the shift from mechanical fasteners to adhesive-based composites for aerospace fuselage and non-metallic aircraft structures, improving overall fuel efficiency and structural integrity. The U.S. Department of Energy (DOE) continues to fund cutting-edge projects in multi-material joining technologies, particularly focusing on aluminum-carbon fiber bonding for advanced vehicle Body-in-White (BiW) structures.

Germany – European Adhesive Technology Leader under REACH-Compliant Manufacturing

Germany stands at the forefront of European Two-Part Adhesive innovation, blending regulatory excellence with technological leadership. The nation’s **chemical industry giants—Henkel AG & Co. KGaA and BASF SE—**are setting new standards for sustainability and performance. Henkel launched its MicroEmission Two-Component Polyurethane (PU) Adhesive range in 2024, engineered with less than 0.1% diisocyanate monomer content, making it fully compliant with the EU’s 2023 REACH regulations on workplace safety and environmental protection. The marks a milestone in the shift toward low-VOC, industrial-grade adhesives for automotive, aerospace, and structural applications.

Meanwhile, the German automotive industry’s lightweighting strategy is accelerating adoption of Two-Part Epoxy Structural Adhesives for battery enclosures, aluminum chassis, and carbon fiber components in EV assembly lines. BASF SE continues to invest in bio-based feedstocks and polymer precursors for eco-friendly two-component adhesives, supporting the European Green Deal and circular manufacturing goals. As Germany strengthens its position as the epicenter of reactive adhesive R&D, its focus on high durability, recyclability, and emission control cements its influence in the European industrial adhesives market.

China – Scaling Epoxy and Polyurethane Adhesive Manufacturing for Industrial Growth

China remains the fastest-growing hub for Two-Part Epoxy and Polyurethane Adhesive production, underpinned by rapid industrialization and strong state-backed manufacturing policies. The country’s expansion in wind turbine blade fabrication, high-speed rail construction, and automotive assembly continues to drive massive demand for high-strength structural adhesives. The “Made in China 2025” policy is a cornerstone initiative promoting technological self-reliance and the localization of advanced structural bonding materials for aerospace, electronics, and renewable energy applications.

Recent capacity expansions by domestic producers and acquisitions by global players—such as Sika AG’s acquisition of a specialized waterproofing and sealing manufacturer in China—are enhancing the region’s adhesive production ecosystem. The integration supports both high-volume manufacturing efficiency and customized adhesive solutions for demanding industries like construction, automotive composites, and solar panel lamination. China’s ongoing efforts to develop next-generation epoxy and PU formulations are positioning the nation as a critical global supplier of structural bonding materials.

Japan – Pioneering Cyanoacrylate Hybrid and High-Precision Two-Part Adhesives

Japan continues to lead in high-precision Two-Part Adhesive development, leveraging its expertise in electronics miniaturization and advanced material science. Japanese chemical innovators are pioneering Cyanoacrylate-Epoxy Hybrid Structural Adhesives, combining rapid curing with exceptional long-term durability for miniaturized electronics and precision devices. The adhesives provide a unique balance between speed, adhesion strength, and resistance to heat cycling, critical for smartphones, sensors, and semiconductor assembly.

R&D investments in Silicone-based Two-Component Adhesives are accelerating to meet the growing need for thermal stability and reliability in semiconductor manufacturing, EV battery modules, and renewable energy systems. Three Bond Holdings Co., Ltd. is at the forefront of developing Reactive Adhesives engineered for high-vibration automotive sensors and thermal management systems, enabling performance in harsh environments. Japan’s continued innovation focus on multi-functional adhesives—balancing mechanical, electrical, and environmental performance—positions it as a global technology hub for precision bonding applications.

South Korea – Automotive and Display Technology Integration through Two-Part Adhesives

South Korea’s Two-Part Adhesive market is rapidly evolving alongside its dominant automotive and electronics industries, particularly in EVs and display technologies. Leading Korean automotive OEMs are standardizing the use of Two-Part Acrylic Structural Adhesives for composite body panel bonding, leveraging their high fatigue resistance, low weight, and minimal surface preparation. The shift aligns with the nation’s push toward next-generation electric mobility solutions and carbon-neutral manufacturing.

In the display and electronics sectors, Korean manufacturers are advancing the use of transparent, high-clarity Two-Component Epoxy and Polyurethane Adhesives for curved OLED/LCD panels and premium automotive displays. Continuous R&D collaborations between adhesive formulators and display manufacturers are yielding materials with high optical transparency, UV resistance, and flexible curing profiles for next-generation infotainment and flexible screens. South Korea’s dual focus on innovation and precision integration cements its role as a strategic player in high-technology structural bonding across Asia.

Switzerland – Premium Two-Part Construction Adhesives for Infrastructure Longevity

Switzerland is a benchmark nation for infrastructure-grade structural adhesives, led by Sika AG’s global innovation ecosystem. The company continues to launch high-modulus Two-Part Epoxy Adhesives tailored for structural reinforcement and concrete restoration in aging infrastructure. The products deliver superior mechanical performance, chemical resistance, and long-term stability—qualities essential for large-scale civil engineering projects such as bridges, tunnels, and hydroelectric facilities.

Additionally, Swiss R&D in eco-friendly reactive adhesives is expanding, with a focus on solvent-free formulations that meet stringent EU and national environmental standards. Specialized cementitious-polymer hybrid systems are gaining traction for underground waterproofing and tunnel sealing applications, ensuring both performance and sustainability. As global infrastructure modernization accelerates, Switzerland continues to set the standard for durable, high-performance Two-Part Construction Adhesives engineered for structural resilience and environmental compliance.

India – Expanding Domestic Manufacturing and Adhesive Diversification

India’s Two-Part Adhesives industry is expanding rapidly, supported by large-scale manufacturing incentives and infrastructure modernization under government-backed programs. The Production Linked Incentive (PLI) scheme has catalyzed the growth of domestic automotive and electronics manufacturing, indirectly boosting the demand for high-quality Two-Part Epoxy and Polyurethane Adhesives. The materials are increasingly used in vehicle body assembly, EV battery integration, and electronic component bonding to meet global export standards.

Pidilite Industries Ltd., India’s market leader, is spearheading expansion efforts in industrial-grade adhesive manufacturing, focusing on construction, furniture, and wood lamination sectors. The company’s R&D centers are actively developing high-strength, low-VOC adhesive formulations suited to India’s diverse climatic and substrate conditions. As industrial clusters continue to modernize, India is quickly emerging as a key regional hub for Two-Part Adhesive production, blending cost competitiveness with advanced material innovation.

Two Part Adhesive Market Report Scope

Two Part Adhesive Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$15.2 Billion

|

|

Market Size (2034)

|

$27 Billion

|

|

Market Growth Rate

|

6.6%

|

|

Segments

|

By Resin Type (Epoxy, Polyurethane, Acrylic, Silicone), By Technology (Reactive, Hot-Melt, UV-Cured, Water-Based), By End-User (Automotive, Aerospace, Construction, Electronics, Wind Energy, Marine, General Industrial, Consumer Goods

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, Sika AG, H.B. Fuller Company, Arkema Group, DuPont de Nemours, Inc., BASF SE, Huntsman Corporation, Dow Inc., Wacker Chemie AG, Illinois Tool Works Inc., RPM International Inc., Jowat SE, Pidilite Industries Ltd., DELO Industrial Adhesives

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type

- Epoxy

- Polyurethane

- Acrylic

- Silicone

By Technology

- Reactive

- Hot-Melt

- UV-Cured

- Water-Based

By End-Use Industry

- Automotive

- Aerospace

- Construction

- Electronics

- Wind Energy

- Marine

- General Industrial

- Consumer Goods

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Two Part Adhesive Market-

- Henkel AG & Co. KGaA

- 3M Company

- Sika AG

- H.B. Fuller Company

- Arkema Group

- DuPont de Nemours, Inc.

- BASF SE

- Huntsman Corporation

- Dow Inc.

- Wacker Chemie AG

- Illinois Tool Works Inc.

- RPM International Inc.

- Jowat SE

- Pidilite Industries Ltd.

- DELO Industrial Adhesives

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Two Part Adhesive Market end-to-end—connecting demand signals from EVs, electronics, infrastructure, wind energy, and precision manufacturing to chemistries and processing windows—while our analysis reviews cost structures, supply resilience, and specification drivers behind low-temperature cure and long open-time systems; it synthesizes recent breakthroughs in induction-cure epoxies, storage-stable subassemblies, and conformal/encapsulant crossovers for power electronics, and highlights how capital deployment, APAC localization, and sustainability policies are reshaping mix, throughput, and quality assurance. Built for engineers, sourcing leaders, and product managers, this report is an essential resource for aligning bond performance, takt-time flexibility, EHS compliance, and automated dispensing with multi-substrate joining strategies, etc……

Scope Highlights

Segmentation:

- By Resin Type: Epoxy; Polyurethane; Acrylic; Silicone

- By Technology: Reactive; Hot-Melt; UV-Cured; Water-Based

- By End-Use Industry: Automotive; Aerospace; Construction; Electronics; Wind Energy; Marine; General Industrial; Consumer Goods

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast data 2025–2034.

Companies Covered (analysis/profiles of 15+): Henkel AG & Co. KGaA; 3M Company; Sika AG; H.B. Fuller Company; Arkema Group; DuPont de Nemours, Inc.; BASF SE; Huntsman Corporation; Dow Inc.; Wacker Chemie AG; Illinois Tool Works Inc.; RPM International Inc.; Jowat SE; Pidilite Industries Ltd.; DELO Industrial Adhesives.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.