Water Disinfection Equipment Market Overview – Growth Outlook and Strategic Imperatives for 2025–2034

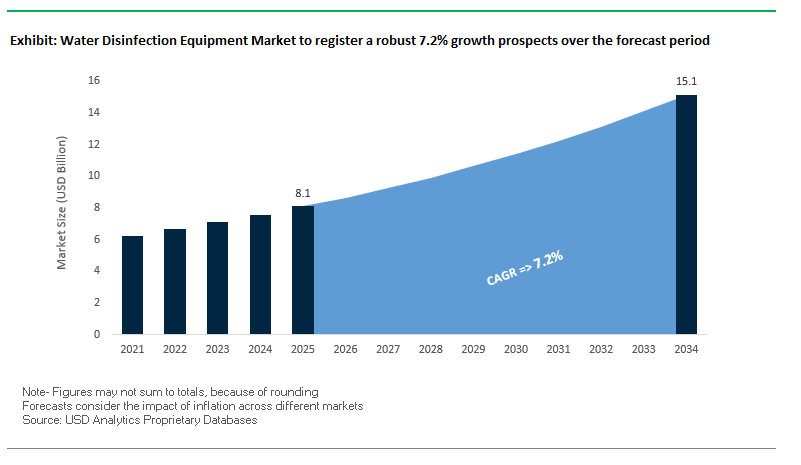

The global water disinfection equipment market is projected to grow from USD 8.1 billion in 2025 to USD 15.1 billion by 2034, registering a CAGR of 7.2%. The growth is driven by a strong push toward chemical-free water disinfection technology, increasingly stringent regulatory frameworks, and a surge in water reuse initiatives to combat scarcity. The market is benefiting from a rapid shift toward UV disinfection, ozonation, and advanced oxidation processes (AOPs), which are favored for their ability to inactivate pathogens without generating harmful disinfection byproducts (DBPs) such as trihalomethanes (THMs).

Government bodies, particularly the U.S. Environmental Protection Agency (EPA), are tightening standards not only for traditional pathogens but also for emerging contaminants like pharmaceuticals, pesticides, and PFAS. The regulatory momentum is pushing municipalities and industries to invest in advanced disinfection systems that integrate automation and IoT sensors for real-time monitoring, predictive maintenance, and compliance reporting. Furthermore, tertiary disinfection is becoming essential in large-scale water reuse projects, enabling recycled water to meet stringent safety standards for both potable and non-potable applications.

Strategic imperatives for market stakeholders:

- Invest in non-chemical disinfection technologies such as UV and AOP to align with tightening regulatory requirements.

- Integrate IoT-based monitoring for operational efficiency and long-term compliance.

- Capitalize on water reuse projects as high-growth segments, particularly in water-scarce regions.

- Develop PFAS-targeted solutions to address the next wave of contaminant regulations.

- Expand service and maintenance capabilities to differentiate offerings in mature markets.

Market Analysis – Technological Advancements and Regulatory Developments Driving Growth

The past 24 months have seen a series of high-impact developments shaping the competitive and technological trajectory of the water disinfection equipment market. In June 2025, Trojan Technologies launched its TrojanUV AOP Demonstration System at ACE 2025, providing municipalities and industries with a platform to evaluate the effectiveness of advanced oxidation processes in eliminating persistent contaminants. Around the same period, Veolia unveiled its patented Drop® PFAS destruction technology, capable of achieving up to 99.9999% elimination rates, representing a major leap in addressing regulatory concerns over “forever chemicals.

In October 2024, SUEZ secured a €4.5 million contract in Denmark to upgrade a wastewater treatment plant with inline ozonation and granular activated carbon (GAC) filtration, directly targeting pharmaceutical residues. The aligns with broader European initiatives to enhance removal of micropollutants. Meanwhile, Xylem introduced the Rivo™ I modular control platform in August 2024, offering utilities real-time operational intelligence to optimize disinfection and chemical dosing. The company’s acquisition of Evoqua Water Technologies and the latter’s earlier investment in a UK-based global UV center of excellence (June 2022) underline an industry-wide race for technological leadership.

From a financial and infrastructure perspective, De Nora reported in May 2025 that its water business revenues grew over 12% in Q1, with backlog orders up 17% compared to the end of 2024. Large-scale capital deployments such as H2O America’s July 2025 acquisition of Quadvest and planned $500 million infrastructure investment are also reshaping the market for advanced disinfection systems in Texas and beyond. Regulatory support has been equally strong, with the U.S. EPA reaffirming decentralized wastewater treatment guidelines in June 2025, signaling an ongoing shift toward distributed, modular disinfection systems for rural and remote communities.

Trends and Opportunities in Water Disinfection Equipment Market

Trend 1: Chlorine Alternatives Gain Traction Due to Byproduct Concerns (THMs, HAAs)

Increasing awareness of disinfection byproducts (DBPs) such as trihalomethanes (THMs) and haloacetic acids (HAAs) is driving the water disinfection equipment market towards alternative technologies. Municipalities are adopting chloramine, ozone, and ultraviolet (UV) disinfection methods to minimize harmful DBPs while ensuring safe drinking water. Chloramine, a combination of chlorine and ammonia, produces lower DBP levels and maintains a longer-lasting residual in distribution systems. Ozone offers potent pathogen inactivation, including for chlorine-resistant microorganisms like Cryptosporidium, without forming THMs or HAAs. UV disinfection provides a chemical-free, environmentally friendly solution by inactivating microorganisms through DNA disruption. Regulatory frameworks like the U.S. EPA’s Stage 1 and Stage 2 Disinfectants and Disinfection Byproducts Rules (DBPRs) reinforce the shift, setting maximum contaminant levels for THMs and HAAs and prompting utilities to explore safer alternatives.

Trend 2: Automated Chemical Dosing Systems for Precision Disinfection in Municipal Plants

Municipal water treatment plants are increasingly implementing automated chemical dosing systems to optimize disinfection, reduce chemical waste, and enhance compliance. These systems continuously monitor water quality parameters such as pH, turbidity, and chlorine residual to adjust dosing in real-time, ensuring consistent disinfection even with fluctuating source water quality. Automation eliminates human error, prevents over- or under-dosing, and provides detailed digital records for regulatory reporting. The ability to optimize chemical usage reduces operational costs and environmental impact while maintaining reliable water safety standards. These systems are becoming integral to modern municipal water treatment infrastructure due to their precision, efficiency, and regulatory alignment.

Opportunity 1: Electrochemical Disinfection for On-Demand Pathogen Killing in Remote Areas

Electrochemical disinfection represents a critical opportunity for remote or off-grid communities where transporting and storing traditional chemicals is challenging. These systems generate disinfectants such as sodium hypochlorite on-site via the electrolysis of brine or seawater, providing a safe, sustainable, and reliable solution. Low energy requirements allow integration with renewable energy sources like solar or wind, ensuring uninterrupted operation. Electrochemical systems effectively inactivate a broad spectrum of pathogens making them highly suitable for decentralized water treatment applications in rural, remote, or resource-limited regions.

Opportunity 2: Combined Chlorine-UV Systems for Multi-Barrier Protection in Hospitals

Hospitals and healthcare facilities require stringent water safety measures to prevent healthcare-associated infections (HAIs). Multi-barrier disinfection systems combining UV and chlorine offer enhanced protection by leveraging complementary strengths: UV rapidly inactivates pathogens, including chlorine-resistant organisms like Cryptosporidium, while chlorine provides residual protection throughout the facility’s distribution network. The approach reduces overall chemical usage, lowers DBP formation, and minimizes corrosion in plumbing infrastructure. Combined systems help healthcare facilities meet CDC and other regulatory standards, ensuring safe water for vulnerable patient populations while providing operational efficiency and environmental benefits.

Water Disinfection Equipment Market Share Insights

Chemical Disinfection Retains Leadership with 40% Market Share

Chemical disinfection remains the largest segment in 2025, accounting for roughly 40.3% of the global water disinfection equipment market. Technologies such as chlorination, chloramination, ozone, and chlorine dioxide dominate municipal water treatment due to their cost-effectiveness, proven pathogen control, and ability to maintain residual disinfectant in distribution networks. Physical disinfection (35.6%), particularly UV disinfection, is rapidly growing as a chemical-free alternative, valued for broad-spectrum pathogen inactivation, including chlorine-resistant organisms like Cryptosporidium, and compact deployment in residential, wastewater reuse, and food & beverage applications. Emerging disinfection technologies, including plasma, photocatalytic (TiO₂ + UV), and ultrasonic systems, cater to niche or industrial segments requiring high-efficiency, compact, or multi-barrier pathogen control.

.png)

Municipal Water Treatment Dominates Applications at 45%

Municipal water treatment represents the largest application segment, with a projected 45% market share in 2025, driven by regulatory mandates and public health priorities. It encompasses both drinking water and wastewater effluent disinfection, reflecting a stable, regulation-driven market. Industrial applications (30.7%) cover food & beverage, pharmaceuticals, and power/manufacturing, where chemical-free and multi-barrier disinfection systems are essential for product safety, process water quality, and microbial control. Commercial and residential applications are increasingly adopting point-of-use UV and ozone systems in homes, hotels, hospitals, and offices to safeguard occupant health and prevent Legionella outbreaks, reflecting the growing health and wellness-driven demand.

System Capacity Trends Highlight High-Capacity Municipal Demand

Systems with capacities exceeding 1,000 m³/day (51,4%) dominate the market in value terms, serving large water treatment plants, major wastewater facilities, and expansive industrial complexes. Mid-range systems (100–1,000 m³/day) are ideal for mid-sized industrial facilities, smaller municipal plants, and large commercial buildings, balancing performance, footprint, and cost. Small-capacity systems (<100 m³/day) cater to point-of-use residential units, small commercial sites, and remote communities, offering convenience and targeted pathogen control.

Water Utilities Drive 40% of End-User Demand

Water utilities remain the primary end-users (39.8%), purchasing disinfection equipment to meet stringent public health mandates and regulatory compliance. Healthcare facilities require ultra-reliable pathogen control to prevent healthcare-associated infections and Legionella proliferation. The hospitality sector invests in UV and ozone disinfection systems to protect guests, comply with health codes, and maintain brand reputation. Agriculture and aquaculture rely on disinfection for irrigation water safety, crop protection, and recirculating aquaculture systems, while other industrial sectors utilize disinfection equipment to ensure water quality for diverse manufacturing processes.

Country Analysis of the Water Disinfection Equipment Market

United States: Boosting Water Safety Through Smart Disinfection Technologies

The United States market for advanced water disinfection equipment is strongly driven by the Bipartisan Infrastructure Law, which allocates over $50 billion for upgrading essential water and wastewater infrastructure. The EPA’s tightening of regulations, including legally enforceable standards for PFAS (per- and polyfluoroalkyl substances), is fueling adoption of advanced oxidation processes (AOPs), combining UV disinfection with hydrogen peroxide to break down persistent contaminants. Key technological trends include IoT-enabled smart monitoring systems, providing real-time water quality data to optimize disinfection, reduce chemical usage, and ensure regulatory compliance. Recent market developments include H2O America’s $540 million acquisition of Quadvest in Texas, with plans for extensive infrastructure modernization, emphasizing on-site disinfection solutions like electrochlorination that generate disinfectants on-demand. These initiatives position the U.S. as a leader in efficient, modular, and scalable water disinfection technologies.

China: Policy-Driven Expansion of UV and Automated Disinfection Systems

China’s Water Ten Plan and Beautiful China initiative are central to national water safety, promoting significant investments in modern water infrastructure. The government targets 95% wastewater treatment for all county-level cities, which drives the need for high-performance water disinfection equipment, particularly UV systems for municipal wastewater. The Ministry of Ecology and Environment mandates real-time emission disclosure for key enterprises, creating demand for automated, continuously monitored disinfection systems. Funding for water pollution control exceeded RMB 673 billion between 2017 and 2022, further supporting large-scale industrial and municipal disinfection projects. Notably, the minimum liquid discharge plant in Da Tang Industrial Park, Foshan, uses advanced filtration and disinfection to treat 160,000 m³/day, underscoring the integration of tertiary treatment and UV technologies in industrial applications.

India: Expanding IoT-Enabled and Decentralized Disinfection Solutions

India’s Jal Jeevan Mission is transforming rural water supply systems by deploying sensor-based IoT devices in over six lakh villages, creating a robust market for smart, connected water disinfection equipment. The Central Pollution Control Board (CPCB) has introduced stringent discharge standards for all STPs, accelerating the adoption of advanced UV and ozone disinfection technologies for municipal and industrial applications. The government is also promoting water ATMs, containerized purification units that rely on on-site disinfection to ensure safe drinking water. Initiatives like the Namami Gange Mission support decentralized treatment systems in smaller cities and rural areas, where conventional centralized plants are impractical, highlighting the critical role of final-stage disinfection technologies in India’s water safety strategy.

Germany (Europe): Driving Decentralized and Energy-Efficient Disinfection Solutions

Germany’s market for water disinfection equipment is influenced by the EU’s Urban Wastewater Treatment Directive, which mandates treatment for communities above 1,000 population-equivalents. The directive also enforces Extended Producer Responsibility for pharmaceuticals and cosmetics, supporting tertiary treatment and advanced disinfection technologies like AOPs. Germany emphasizes energy efficiency and resource recovery, driving the integration of membrane bioreactors and intelligent monitoring systems to enhance operational effectiveness and reduce energy usage. There is a growing trend toward decentralized wastewater treatment systems, particularly in rural areas, positioning Germany as a leader in sustainable and modular water disinfection solutions.

South Korea: Advancing Filtration-Integrated Disinfection Technologies

South Korea has positioned its water technology sector as a strategic growth area, providing R&D support for advanced disinfection systems to meet international standards. Companies like Inosep are developing polymer membranes for microfiltration, ultrafiltration, nanofiltration, and reverse osmosis (RO), ensuring optimal pretreatment before disinfection. The Korean Register of Shipping facilitates U.S. Coast Guard-type approval certificates, giving local companies a competitive edge in maritime applications, where disinfection systems are critical. South Korea’s focus on advanced filtration technologies integrated with disinfection stages enhances both municipal and residential water treatment capabilities, ensuring high-quality and compliant water supply solutions.

Japan: Leading Innovations in Microplastics Removal and IoT-Enabled Disinfection

Japan is at the forefront of advanced water disinfection equipment, particularly for applications targeting microplastics and high-efficiency water reuse. Mitsui O.S.K. Lines and Miura Co., Ltd. developed devices to collect microplastics at sea, serving as a pre-treatment stage that enhances disinfection effectiveness. Companies like Kubota have deployed submerged membrane units that reclaim effluent efficiently, reducing wastewater discharge. Advanced IoT-enabled sensors and machine learning systems enable predictive water quality monitoring, while innovative ultrafiltration membranes in Fukuoka desalination plants improve stability and reduce maintenance needs, further boosting final-stage disinfection efficiency. Japan’s strong regulatory framework and sustainability focus ensure that disinfection technologies remain energy-efficient, reliable, and technologically advanced.

Competitive Landscape – Leading Innovators in Water Disinfection Technology

The water disinfection equipment market is dominated by multinational players with strong R&D pipelines, integrated portfolios, and established regulatory expertise. The competitive edge lies in combining sustainability, smart automation, and versatility across municipal, industrial, and residential applications.

Xylem Inc. – Integrating Digital Intelligence with Water Disinfection

Xylem leverages its global engineering capabilities and Wedeco brand to deliver UV, ozone, and AOP solutions integrated with pumps, filtration, and analytics. Its recent launch of the Rivo™ I platform strengthens its position in real-time monitoring and process optimization. The company’s competitive advantage lies in its digital ecosystem and strong after-sales network, enabling customers to maintain compliance while improving operational efficiency.

Trojan Technologies – Pioneering Environmentally Friendly UV and AOP Solutions

Operating as a Xylem brand, Trojan Technologies focuses on chemical-free pathogen inactivation and removal of challenging contaminants. Its TrojanUV AOP Demonstration System showcases real-world efficacy in treating complex water quality issues. With over 11,000 municipal installations in 100 countries, Trojan is widely regarded for its reliability and regulatory compliance.

De Nora – Electrochemical Expertise Driving Sustainable Disinfection

De Nora’s portfolio includes Capital Controls® ozone generators, AOP systems, and on-site electrochlorination solutions. The company’s Q1 and Q2 2025 growth, alongside expanded operations in South America, underscores its global reach. Its SORB™ PFAS removal systems further position De Nora as a leader in emerging contaminant treatment.

Veolia Environnement S.A. – Holistic Ecological Transformation Solutions

Veolia integrates UV, ozonation, and chemical dosing into large-scale treatment and reuse projects, supported by digital optimization through its Hubgrade platform. Its patented Drop® PFAS technology adds a high-value, regulatory-compliant innovation to its portfolio. With operations across multiple continents, Veolia offers a full-lifecycle water management approach.

Pentair – Dual Market Focus on Residential and Industrial Applications

Pentair provides UV disinfection and filtration under its Everpure brand for foodservice and residential markets, while serving industrial customers with advanced treatment solutions. Its acquisition of Porous Media expanded its filtration and separation capabilities, enhancing its role in PFAS removal and other high-demand applications. Its dual-market strategy allows cross-leveraging of technology and brand recognition.

Water Disinfection Equipment Market Report Scope

Water Disinfection Equipment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.1 Billion

|

|

Market Size (2034)

|

$15.1 Billion

|

|

Market Growth Rate

|

7.2%

|

|

Segments

|

By Technology Type (Chemical Disinfection, Physical Disinfection, Plasma Disinfection, Photocatalytic Disinfection (TiO₂ + UV), Ultrasonic Disinfection), By Application (Municipal Water Treatment, Industrial Applications, Commercial & Residential, Emergency & Mobile Systems), By System Capacity (<100 m³/day, 100–1,000 m³/day, >1,000 m³/day), By End-User Industry (Water Utilities, Healthcare Facilities, Hospitality Industry, Agriculture & Aquaculture),

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, Xylem Inc., SUEZ, Ecolab, Pentair, Evoqua Water Technologies (now part of Xylem), Trojan Technologies, Kurita Water Industries, DuPont, Calgon Carbon Corporation, Aquatech International LLC, Grundfos Holding A/S, Kemira Oyj, De Nora S.p.A., Danaher Corporation (including Hach)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Water Disinfection Equipment Market Segmentation

By Technology Type

- Chemical Disinfection

- Physical Disinfection

- Plasma Disinfection

- Photocatalytic Disinfection (TiO₂ + UV)

- Ultrasonic Disinfection

By Application

- Municipal Water Treatment

- Industrial Applications

- Commercial & Residential

- Swimming pools & spas

- Point-of-use water purifiers

- Emergency & Mobile Systems

By System Capacity

- <100 m³/day

- 100–1,000 m³/day

- >1,000 m³/day

By End-User Industry

- Water Utilities

- Healthcare Facilities

- Hospitality Industry

- Agriculture & Aquaculture

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Water Disinfection Equipment Market

- Veolia

- Xylem Inc.

- SUEZ

- Ecolab

- Pentair

- Evoqua Water Technologies (now part of Xylem)

- Trojan Technologies

- Kurita Water Industries

- DuPont

- Calgon Carbon Corporation

- Aquatech International LLC

- Grundfos Holding A/S

- Kemira Oyj

- De Nora S.p.A.

- Danaher Corporation (including Hach)

* List Not Exhaustive

Research Coverage

This report investigates the Global Water Disinfection Equipment Market, offering detailed analysis reviews of breakthrough technologies, regulatory momentum, and high-impact contracts reshaping the industry landscape between 2025 and 2034. Published by USDAnalytics, the study highlights how the shift toward chemical-free disinfection, UV and ozone-based systems, and advanced oxidation processes (AOPs) is accelerating under stricter U.S. EPA and European Union regulations targeting PFAS, pharmaceuticals, and DBPs. The report also reviews major technology launches such as Trojan’s UV-AOP systems, Veolia’s patented Drop® PFAS solution, and Xylem’s Rivo™ I modular intelligence platform, along with acquisitions that are redefining competition. By integrating market trends with insights into municipal, industrial, and decentralized applications, this report is an essential resource for utilities, regulators, water technology providers, and investors seeking to align with the global transition toward sustainable, smart, and regulation-driven disinfection solutions.

Scope Includes:

- Segmentation: By Technology (Chemical, UV, Ozone, AOP, Electrochemical, Emerging Systems), By Application (Municipal, Industrial, Residential, Commercial), By System Capacity (<100 m³/day, 100–1,000 m³/day, >1,000 m³/day), By End User (Water Utilities, Healthcare, Hospitality, Agriculture & Aquaculture, Other Industries).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Historic Data: 2021 to 2024, and Forecast Data: 2025 to 2034.

- Companies: Profiles and competitive analysis of 15+ leading companies including Xylem, Trojan Technologies, Veolia, SUEZ, De Nora, and Pentair.

Methodology

The research methodology adopted by USDAnalytics is based on a hybrid approach of primary and secondary research, ensuring accurate and actionable findings. Primary inputs were derived from interviews with water utilities, regulatory bodies, technology developers, and plant operators to validate adoption trends, technology performance, and compliance drivers. Secondary research incorporated company reports, government regulations, scientific publications, and global water project databases to establish a strong evidence base. Market sizing was determined using top-down and bottom-up modeling, aligning installed capacity data, contract awards, and technology penetration rates with regulatory mandates. Forecasts were stress-tested under scenarios such as accelerated PFAS compliance, higher adoption of IoT-enabled monitoring, and the rise of decentralized disinfection systems, delivering reliable insights for stakeholders across the value chain.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Water Disinfection Equipment Market

1. Executive Summary

1.1. Market Highlights

1.2. Strategic Imperatives for Market Stakeholders

1.3. Global Market Snapshot

2. Water Disinfection Equipment Market Overview & Outlook (2025–2034)

2.1. Introduction to the Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $8.1 Billion

2.2.2. Forecasted Market Size (2034): $15.1 Billion at 7.2% CAGR

2.3. Key Drivers and Market Dynamics

2.3.1. Shift to Non-Chemical Disinfection Technologies

2.3.2. Increasingly Stringent Regulatory Frameworks

2.3.3. Surge in Water Reuse Initiatives

3. Market Analysis: Technological Advancements and Regulatory Developments

3.1. Overview of Key Strategic Developments (2024–2025)

3.1.1. Trojan Technologies' Launch of UV AOP System (June 2025)

3.1.2. Veolia's Patented Drop® PFAS Destruction Technology (June 2025)

3.1.3. SUEZ's Contract for Micropollutant Removal in Denmark (October 2024)

3.1.4. Xylem's Rivo™ I Modular Control Platform (August 2024)

3.2. Financial and Infrastructure Investments

3.2.1. De Nora's Q1 2025 Financial Performance

3.2.2. H2O America's Acquisition of Quadvest (July 2025)

3.3. Regulatory Support for Decentralized Solutions

4. Trends and Opportunities in Water Disinfection Equipment Market

4.1. Trend 1: Chlorine Alternatives Gain Traction Due to Byproduct Concerns

4.1.1. Inactivation of Pathogens without Harmful DBPs

4.1.2. Regulatory Reinforcement by U.S. EPA

4.2. Trend 2: Automated Chemical Dosing Systems for Precision Disinfection

4.2.1. Real-Time Performance Tracking and Reduced Chemical Waste

4.2.2. Enhancing Compliance and Operational Efficiency

4.3. Opportunity 1: Electrochemical Disinfection for On-Demand Pathogen Killing

4.3.1. Safe, Sustainable Solutions for Remote and Off-Grid Areas

4.3.2. Integration with Renewable Energy Sources

4.4. Opportunity 2: Combined Chlorine-UV Systems for Multi-Barrier Protection

4.4.1. Preventing Healthcare-Associated Infections (HAIs)

4.4.2. Reducing Overall Chemical Usage and DBP Formation

5. Water Disinfection Equipment Market Share Insights

5.1. By Technology Type

5.1.1. Chemical Disinfection Retains Leadership with 40% Share

5.1.2. Physical and Emerging Disinfection Technologies

5.2. By Application

5.2.1. Municipal Water Treatment Dominates at 45%

5.2.2. Industrial, Commercial, and Residential Applications

5.3. By System Capacity

5.3.1. High-Capacity Systems (>1,000 m³/day) Lead in Value

5.3.2. Mid-Range and Small-Capacity Systems

5.4. By End-User Industry

5.4.1. Water Utilities Drive 40% of Demand

5.4.2. Healthcare, Hospitality, and Other Industries

6. Country Analysis of the Water Disinfection Equipment Market

6.1. United States: Boosting Water Safety Through Smart Disinfection

6.2. China: Policy-Driven Expansion of UV and Automated Systems

6.3. India: Expanding IoT-Enabled and Decentralized Solutions

6.4. Germany (Europe): Driving Decentralized and Energy-Efficient Solutions

6.5. South Korea: Advancing Filtration-Integrated Disinfection

6.6. Japan: Leading Innovations in Microplastics Removal and IoT-Enabled Disinfection

6.7. Other Country Analysis

7. Competitive Landscape: Leading Innovators

7.1. Xylem Inc.: Integrating Digital Intelligence

7.2. Trojan Technologies: Pioneering Environmentally Friendly Solutions

7.3. De Nora: Electrochemical Expertise for Sustainable Disinfection

7.4. Veolia Environnement S.A.: Holistic Ecological Transformation

7.5. Pentair: Dual Market Focus on Residential and Industrial Applications

8. Market Size Outlook by Region (2025–2034)

8.1. North America Market Size Outlook to 2034

8.1.1. By Technology

8.1.2. By Application

8.1.3. By End-User

8.2. Europe Market Size Outlook to 2034

8.2.1. By Technology

8.2.2. By Application

8.2.3. By End-User

8.3. Asia Pacific Market Size Outlook to 2034

8.3.1. By Technology

8.3.2. By Application

8.3.3. By End-User

8.4. South America Market Size Outlook to 2034

8.4.1. By Technology

8.4.2. By Application

8.4.3. By End-User

8.5. Middle East and Africa Market Size Outlook to 2034

8.5.1. By Technology

8.5.2. By Application

8.5.3. By End-User

9. Research Coverage & Methodology

9.1. Report Scope and Focus

9.2. Research Methodology

9.3. Deliverables

10. Appendix

10.1. List of Tables

10.2. List of Figures

10.3. Abbreviations